In the world of cryptocurrency, algorithmic stablecoins have always been the sweet spot for investors and developers, representing an ideal state that can maintain stable value even in the most uncertain market environment.

Ethena completed a financing of 20.5 million US dollars last year and this year, attracting the attention of a number of heavyweight institutions including Binance, OKX, Dragonfly, etc. VCs are not only optimistic about this field, but also actively participate in it to jointly promote the development of this innovative financial tool. When it was first launched, Ethena's issuance mechanism also ensured fairness. Even large users can only gradually obtain their shares through linear unlocking.

Ethena has built a derivatives infrastructure to achieve "Delta neutrality" to obtain stable returns . In addition, it also provides an annualized rate of return of up to 35%, which combined provides investors with a strong storage motivation.

In terms of marketing, Ethena has received support from a group of the most influential KOLs in this bull market, such as @CryptoHayes, as well as endorsements from many venture capital companies. This has brought huge exposure and trust.

The world is impermanent, like a dream bubble

Just when Ethena, the algorithmic stablecoin project known as Luna2.0, was at its peak, the crisis quietly arrived.

The Ethena Season 2 airdrop activity will officially end today. According to Coingecko data, ENA fell below $0.22 today, falling to $0.2186, setting a new record low. As of press time, ENA was trading at $0.2318, down 84% from its historical high of $1.52.

We can't help but wonder, what exactly happened to Ethena?

TVL

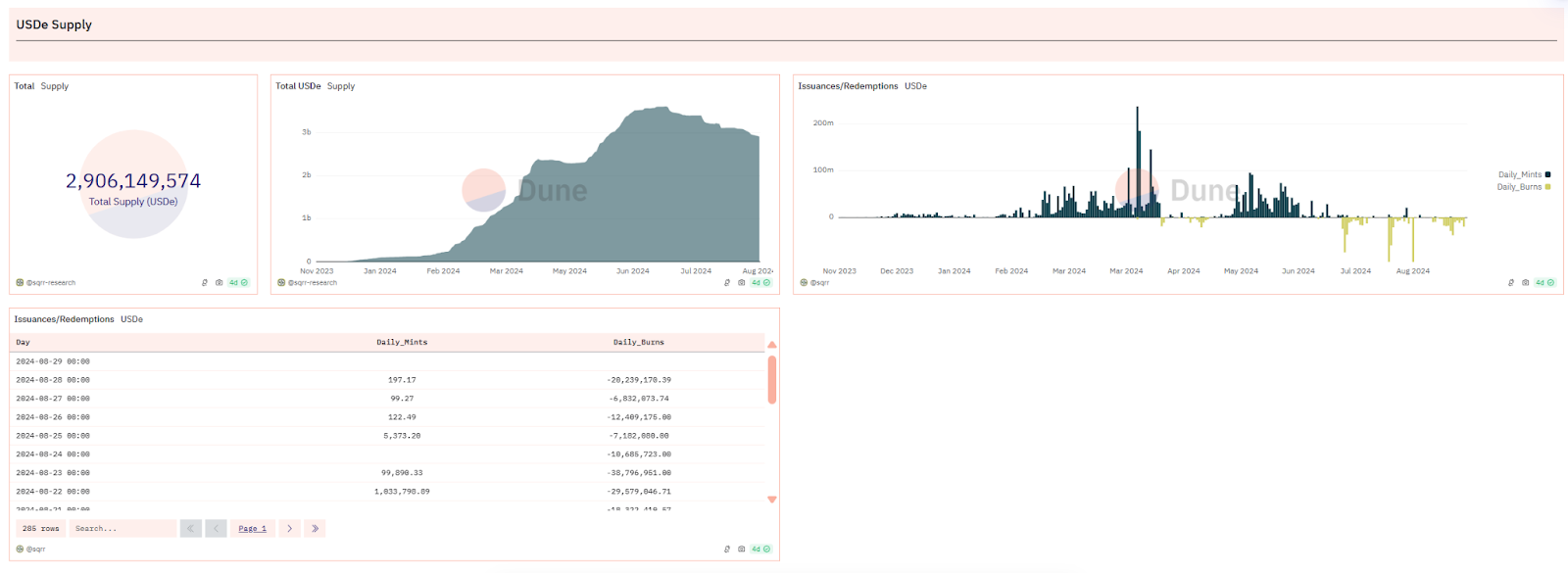

According to DeFiLama, Ethena TVL is currently $2.73 billion, falling below the $3 billion mark, a decrease of nearly $900 million from the peak of $3.612 billion in early July. Ethena Labs' revenue has dropped significantly since March. Revenue in August was only $1.03 million, down about 96% from the peak of $26.26 million. Based on the revenue in the last 30 days, Ethena Labs' annual revenue is expected to be only $12.55 million.

This trend is not difficult to understand: non-stablecoin stakers may choose to sell before the airdrop to avoid price drops, while stablecoin stakers may also give up the last few days of point gains and look for projects with higher returns.

According to Dune Analytics, USDe has experienced multiple destruction events worth tens of millions of dollars in the past month, which usually indicates that a large amount of collateral has been redeemed. In addition, the supply of sUSDe (USDe pledge certificate token) also shows that more than $100 million of sUSDe has completed pledge release in the past week.

It was reported that three accounts of Abraxas Capital Mgmt redeemed up to $91.22 million USDDe from Ethena in the past week, and its redemption funds ranked first among all redemption accounts.

Protocol Rate of Return

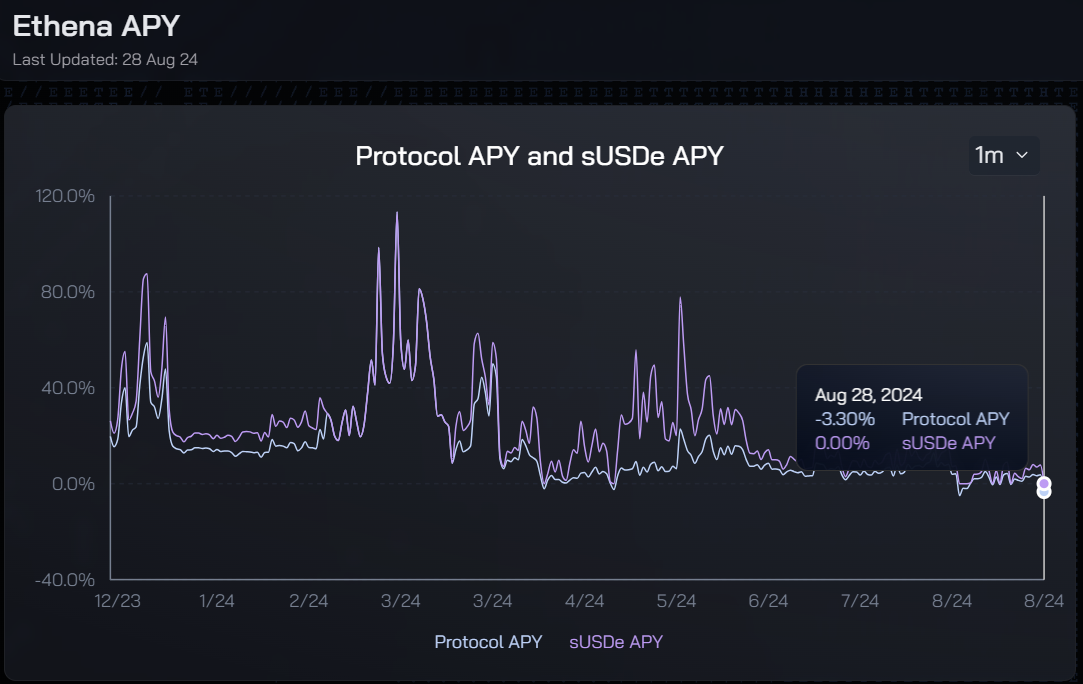

According to Ethena Dashboard data, its protocol yield and sUSDe yield reached a peak of 113.34% in early March. As of 08.28, the protocol yield has been negative -3.3%, and the sUSDe yield has changed to 0.

Briefly describe the principle of Ethena

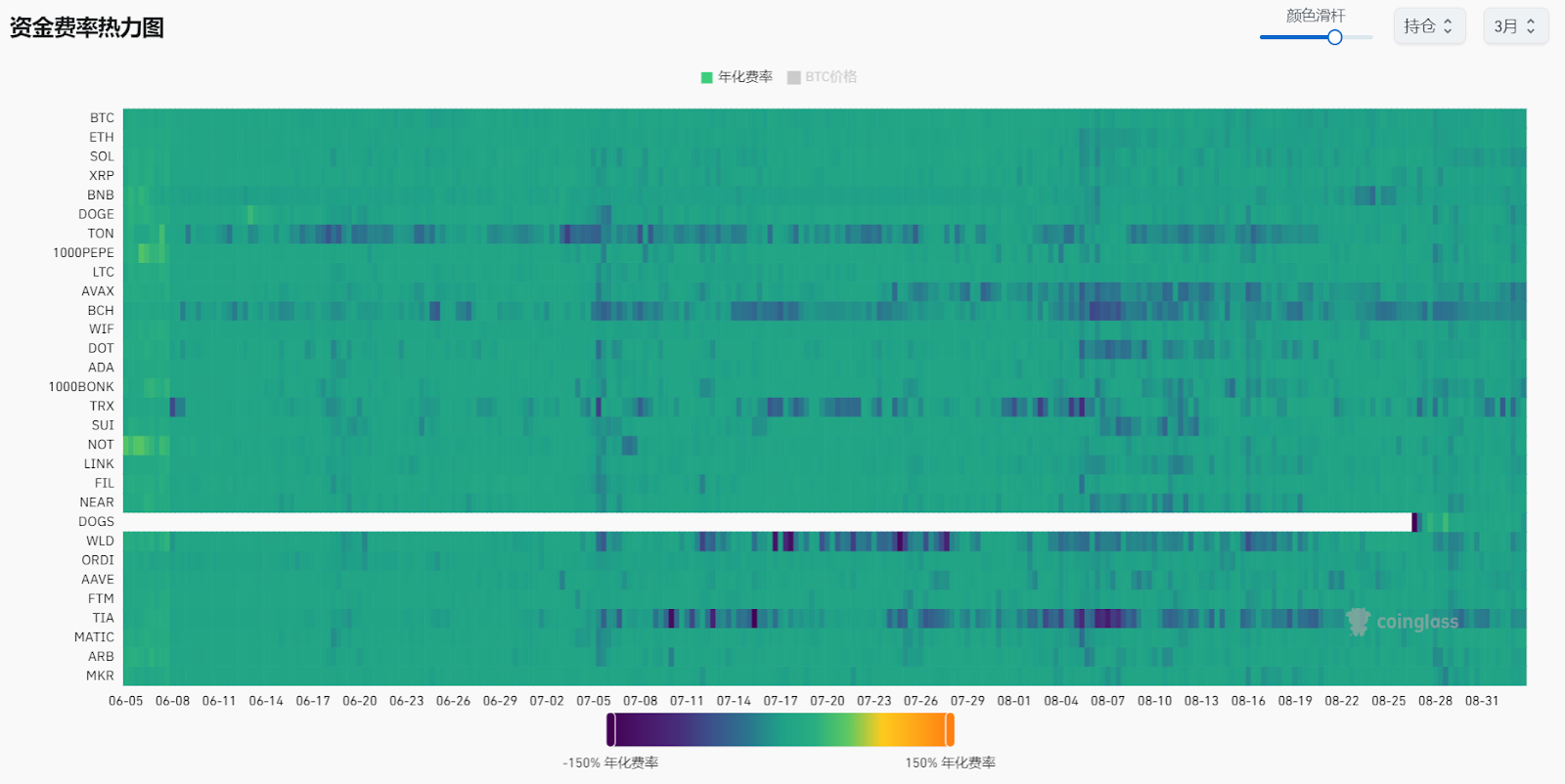

As we all know, the core feature of perpetual contracts is that investors need to pay funding rates whether they hold long or short positions. When the market buying power exceeds the selling power, the funding rate is positive for short investors and negative for long investors. This mechanism helps ensure that the price of perpetual contracts keeps pace with the price of the spot market. In order to maintain their positions, investors must provide margin, which is a kind of collateral used to cover the debt incurred by changes in the funding rate. If the funding rate is negative, it will gradually reduce the investor's margin balance until it reaches the level of forced liquidation.

In addition, margin also has a compound interest effect, that is, holding margin can make the value of assets grow. For example, in Ethena, holding stETH is equivalent to holding a long position. If investors also hold a short position of stETH through perpetual contracts, risk hedging can be achieved in theory, that is, the loss of the short position can be offset by the profit of the long position.

In summary, by purchasing stETH and using it as margin, investors can open corresponding short positions in perpetual contracts to achieve theoretical risk hedging and obtain the compound interest income of stETH (about 3%) while assuming the risks brought about by changes in funding rates.

It can be found that due to Ethena's product mechanism, the platform yield is very obviously positively correlated with the market conditions. The pledge income and short funding rate in a bull market will bring it considerable income. On the contrary, it will be relatively weak when the market is cold or bearish.

According to Coinglass data, since the market entered a period of volatility in May, funding rates have gradually decreased, and in many cases have even turned negative, which means that Ethena's margin (collateral) will begin to be eroded or even liquidated, and at that time there will only be an asset left without any support.

Summarize

In the first half of the year, USDe's issuance has grown rapidly due to the expected effect of its airdrops and the high returns provided by spot and futures arbitrage strategies. The total amount of USDe minting once reached a peak of 3.6 billion US dollars. It not only surpassed projects supported by industry leaders such as FRAX, crvUSD, and GHO in the decentralized stablecoin track, but also seems to have the potential to continue to expand and challenge DAI's leading position in the market.

Ethena mentioned in its recently updated token economic model that starting from June 17, all users who received ENA through airdrops must lock at least 50% of their tokens, otherwise they will lose the unallocated portion. This measure is intended to alleviate the market selling pressure that may be brought about by airdrops to avoid a sharp drop in the value of ENA tokens, but at present, this downward spiral seems unstoppable.

The past is a lesson for the future

Two years ago, Luna's death spiral is still vivid in people's minds. The risk of algorithmic stablecoins depegging and the potential risks in the re-mortgage process are something that people have to think deeply about. Can there be a perfect model for algorithmic stablecoins? This question may be as thought-provoking and fascinating as the Blockchain Trilemma in the blockchain field.