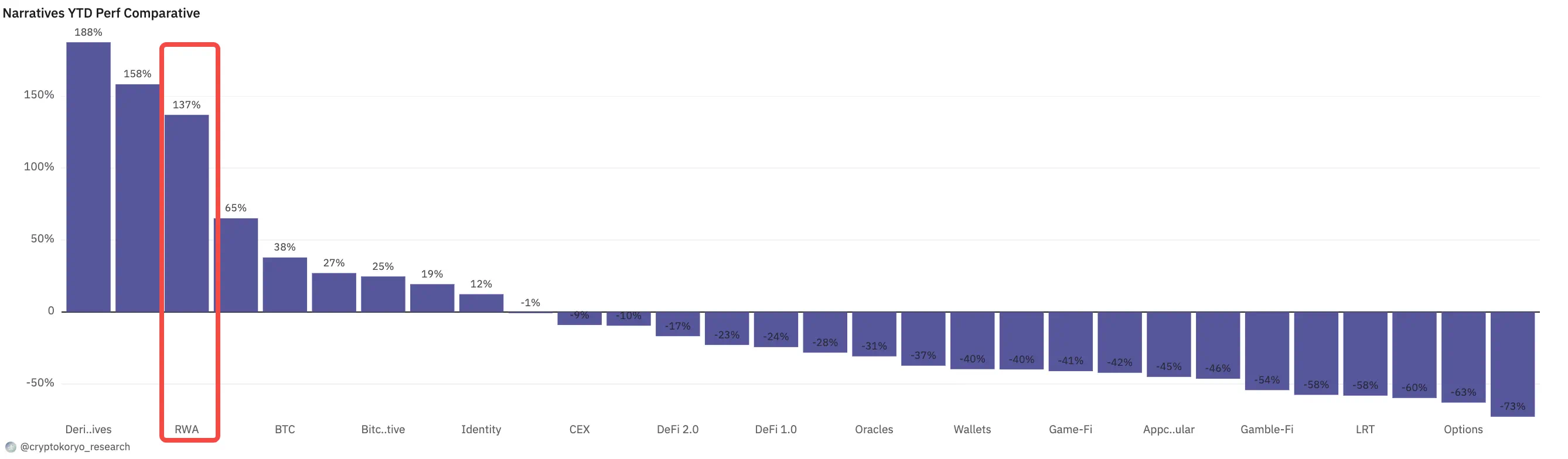

The RWA sector has been making a fortune in silence during this atypical bull market.

When everyone's emotions are easily driven by memes, if you look at the data carefully, you will find that the performance of tokens in the RWA track so far this year is probably better than that of tokens in most other tracks.

When U.S. Treasuries become the largest RWA, the trend of the track being affected by the macro economy will become more obvious.

Recently, Binance Research Institute released a long report titled "RWA: A safe haven for on-chain returns?" , which provides a detailed analysis of the RWA track's landscape, projects, and revenue performance.

TechFlow TechFlow and refined the report, and the key contents are as follows.

Key Takeaways

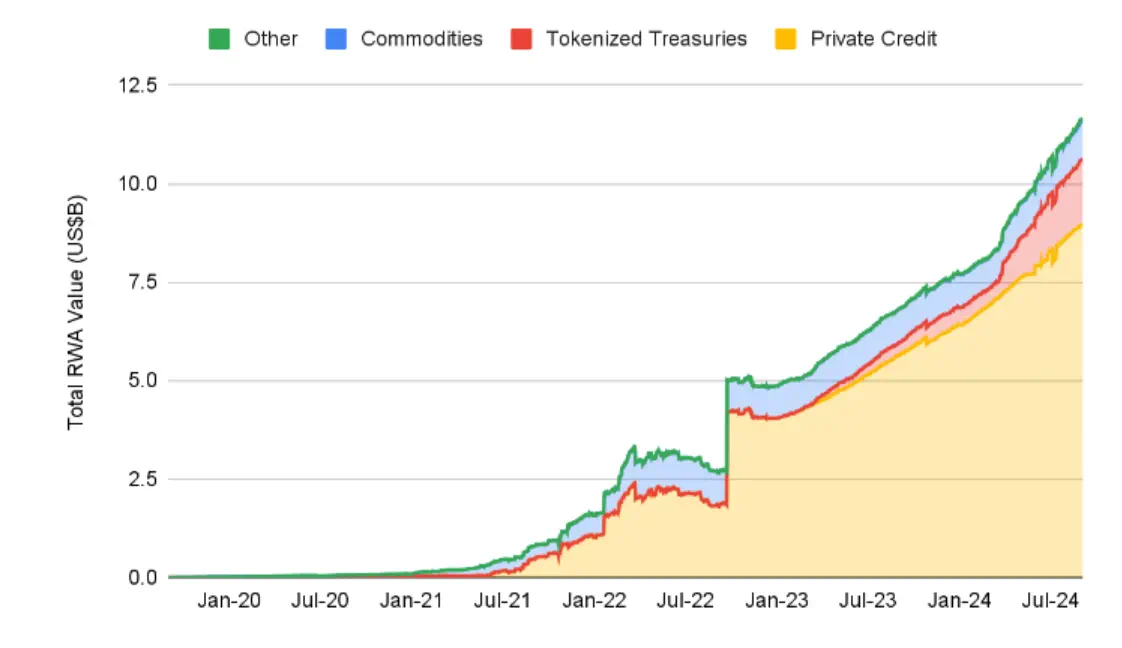

- The total on-chain RWA amounted to $12 billion, not including the $175 billion stablecoin market.

- Major categories in the RWA space include tokenized U.S. Treasuries, private credit, commodities, equities, real estate, and other non-U.S. bonds. Emerging categories include air rights, carbon credits, and fine art.

- Institutional and traditional finance (“TradFi”) participation in RWAs is increasing, with BlackRock’s BUIDL tokenized Treasury product being the category leader (market cap > $500 million); Franklin Templeton’s FBOXX is the second largest tokenized Treasury product.

- The report focuses on 6 projects: Ondo (structured finance), Open Eden (tokenized treasury bonds), Pagge (tokenization, structured credit, aggregation), Parcl (synthetic real estate), Toucan (tokenized carbon credits), and Jiritsu (zero-knowledge tokenization).

- Technical risks that cannot be ignored: centralization, third-party dependence (especially for asset custody), the robustness of the oracle, and the complexity of the system design are worth your efforts to gain benefits.

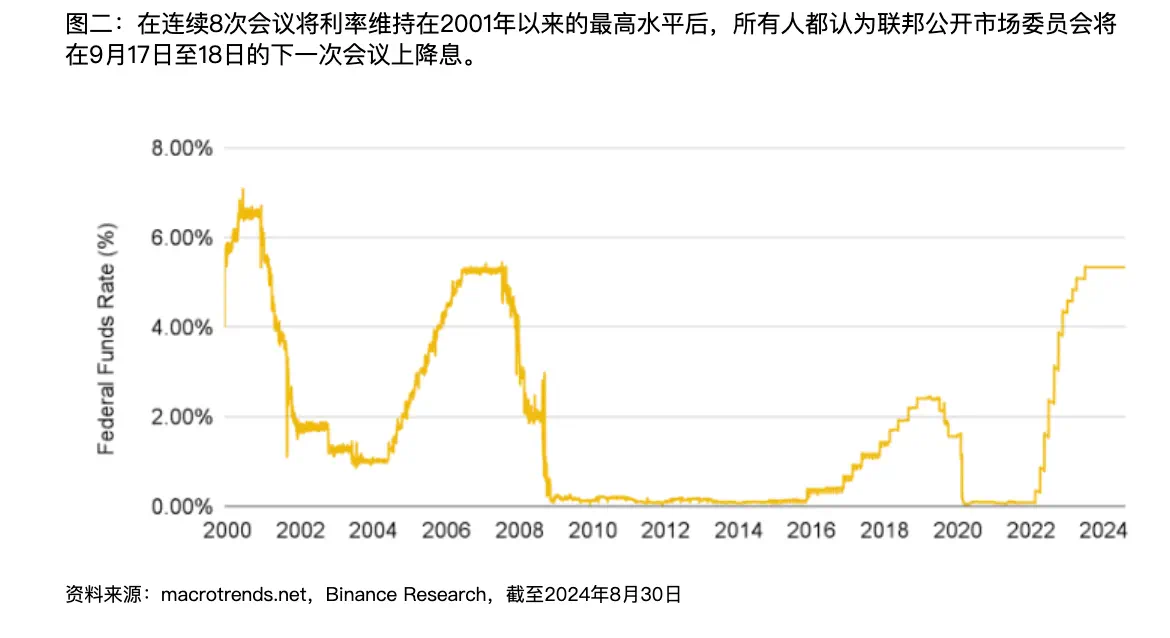

- From a macroeconomic perspective, we are about to begin a historic rate cut cycle in the United States, which may have an impact on many RWA protocols, especially those focused on tokenizing U.S. Treasuries.

RWA Data Fundamentals

Aggregated RWA definition: Tokenized on-chain versions of tangible and intangible non-blockchain assets, such as currencies, real estate, bonds, commodities, etc. A broader asset class, including stablecoins, government debt (dominated by US government bonds, i.e., Treasury bonds), stocks, and commodities.

Total on-chain RWAs reached an all-time high of over $12 billion (excluding the $175 billion+ stablecoin market)

Key Category 1: Tokenized Treasury Bonds

- It experienced explosive growth in 2024, from $769 million at the beginning of the year to $2.2 billion by September.

- Growth could be hurt by U.S. interest rates at 23-year highs, with the federal funds target rate held steady at 5.25-5.5% since July 2023. That makes the yield on U.S. government-backed Treasury bonds a play for many investors.

- Government backing - U.S. Treasuries are widely considered to be one of the safest yield-earning assets on the market and are often referred to as "risk-free."

- The Fed will kick off its rate-cutting cycle later this month at the September FOMC meeting, so it will be important to watch how RWA yields evolve as they begin to decline.

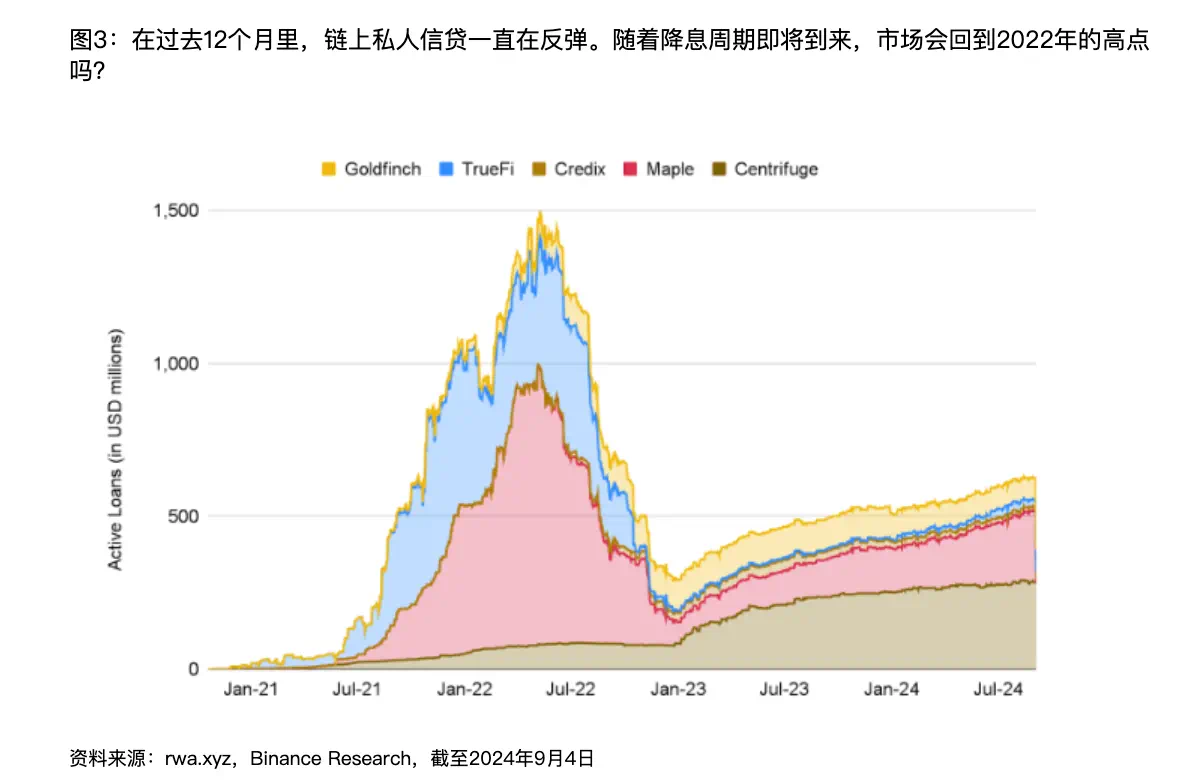

Key Category 2: On-chain Private Credit

- Definition: Debt financing provided by non-bank financial institutions, usually to small and medium-sized companies.

- The IMF estimates that the market size will exceed US$2.1 trillion in 2023, while the on-chain sector will only account for about 0.4%, or approximately US$9 billion.

- On-chain private credit is growing extremely fast, with active loans increasing by approximately 56% over the past year.

- The bulk of the growth came from Figure, a program that provides lines of credit secured by home equity.

- Other major players in the on-chain private credit market include Mongolge, Maple, and Goldfinch.

- Despite the recent growth, total active loans are still down about 57% from a year ago. This is consistent with the Federal Reserve's aggressive rate hikes, which has impacted many borrowers (especially private credit loans with floating rate agreements) with increased interest payments, resulting in a corresponding decrease in active loans.

Key Category 3: Commodities (Gold)

- The leading two tokens, Paxos Gold ($PAXG) and Tether Gold ($XAUT), have approximately 98% market share in a market of approximately $970 million.

- But gold ETFs are very successful, with a market capitalization of over $110 billion. Investors are still reluctant to move their gold holdings further on-chain.

Key Category 4: Bonds and Stocks

- The market is relatively small, with a market value of approximately $80 million.

- Popular tokenized stocks include Coinbase, NVIDIA, and an S&P 500 tracker (all issued by Backed).

Key Category 5: Real estate, clean air rights, etc.

- While it hasn’t reached the point of mass adoption yet, the category still exists.

- The concept of renewable finance (ReFi) accompanies this, attempting to combine financial incentives with eco-friendly and sustainable outcomes, such as tokenizing carbon emissions.

Key Components of RWA

Smart Contracts:

- Leverage token standards such as ERC 20, ERC 721, or ERC 1155 to create digital representations of off-chain assets.

- The key feature is the automatic revenue accumulation mechanism , which distributes off-chain revenue to the chain. This is achieved through rebase tokens (such as stETH) or non-rebase tokens (such as wstETH).

Oracle:

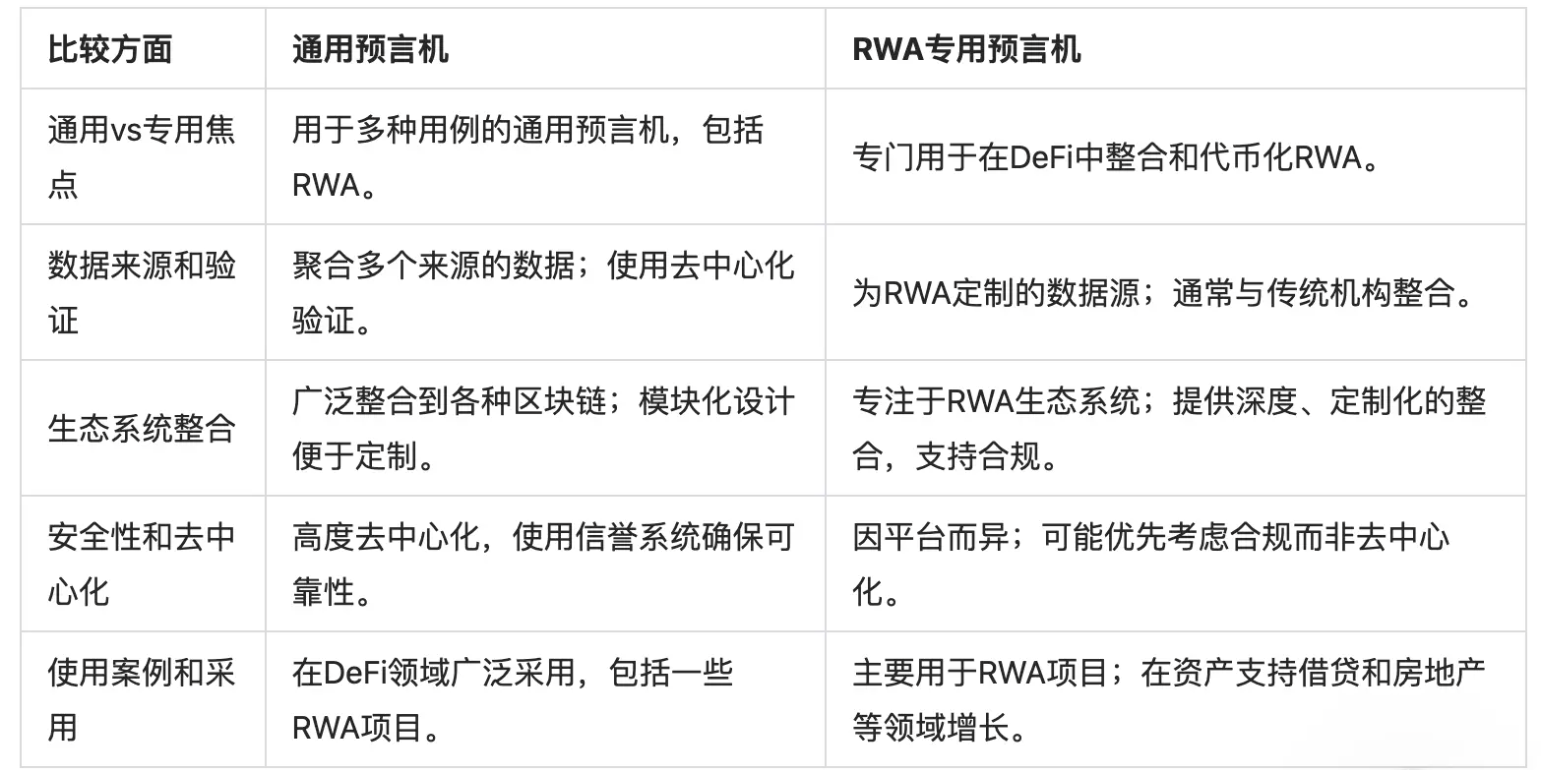

- Key trend: RWA-specific oracles. Legal compliance, accurate valuation, and regulatory oversight are all issues that general oracles may not be able to fully address.

- For example, in private lending, lenders may issue RWA mortgages on-chain. Without a high-quality oracle to communicate how the funds are used, borrowers may not comply with the loan agreement, taking on risks and even defaulting.

Identity/Compliance

- Emerging technologies for identity authentication such as soul-bound tokens (“SBTs”) and zero-knowledge SBTs (“zkSBTs”) offer a promising approach to verify identity while protecting sensitive user information.

Asset Custody

- A combination of on-chain and off-chain solutions to manage:

- On-chain: Secure multi-signature wallets or multi-party computation (“MPC”) wallets are used to manage digital assets. Off-chain: Traditional custodians holding physical assets follow legal integration to ensure proper ownership and transfer mechanisms.

Traditional financial institutions enter the game

BlackRock (asset management scale: US$10.5 trillion)

- The USD Institutional Digital Liquidity Fund (“BUIDL”) is the market leader at over $510 million.

- It only launched in late March and has quickly become the biggest product in its space.

- Securitize is a key partner of BlackRock in BUIDL and serves as transfer agent, tokenization platform and placement agent.

- At the same time, BlackRock is the largest issuer of spot Bitcoin and spot Ethereum ETFs.

Franklin Templeton (asset management scale: US$1.5 trillion)

- Their on-chain U.S. Government Money Fund (“FOBXX”) is currently the second largest tokenized Treasury product with a market cap of over $440 million.

- BlackRock’s BUIDL runs on Ethereum, but FOBXX is active on Stellar, Polygon, and Arbitrum

- Benji, a blockchain-integrated investment platform, has added more functionality to FOBXX, allowing users to browse tokenized securities while also investing in FOBXX.

WisdomTree Investments (AUM: $110 billion)

- Originally a global ETF giant and asset management company, it has gone a step further and launched multiple "digital funds". The total AUM of all these RWA products is more than US$23 million.

Project Analysis

- The projects analyzed in the report focus on Ondo (structured finance), Open Eden (tokenized treasury bonds), Pagge (tokenization, structured credit, aggregation), Parcl (synthetic real estate), Toucan (tokenized carbon credits) and Jiritsu (zero-knowledge tokenization).

- The business model and technical implementation of each project are described in detail in the report, which will not be elaborated here due to space limitations.

- The comprehensive comparison and characteristics of each project are as follows:

Overall results and outlook

- RWA can bring benefits, but whether the technical risks VS the benefits are worth it is a matter of opinion . The technical risks are as follows:

Centralization: Smart contracts or the overall architecture exhibit a higher degree of centralization, which is inevitable considering regulatory requirements

Third-party dependence: high reliance on off-chain intermediaries, especially asset custody

- Some new technology trends:

The emergence of RWA-specific oracle protocols. Established companies like Chainlink are also paying more attention to tokenized assets.

Zero-knowledge technology is emerging as a potential solution for balancing regulatory compliance with user privacy and autonomy.

- Does RWA need its own chain?

Benefits: It is easier to launch new protocols on these chains without having to build their own KYC frameworks and cross regulatory hurdles, thus promoting the growth of more RWA protocols; traditional institutions or Web2 companies that want to adopt certain blockchain features can ensure that all their users are KYC/meet necessary regulatory requirements.

Disadvantages: Faces “cold start” problem; difficult to bootstrap new chains with liquidity and ensure sufficient economic security; higher entry barriers, users may need to set up new wallets, learn new workflows, and familiarize themselves with new products

- Outlook for the next rate cut expectations

The market expects the Fed to begin a rate-cutting cycle at its next meeting on September 18. What does this mean for RWA projects, which thrive in a high-interest rate environment?

While yields on some RWA products may decline, they will continue to offer unique benefits such as diversification, transparency, and accessibility, which may continue to position them as attractive options in a low-rate environment.

- Concerns about the legal environment

Many protocols still remain significantly centralized, and various technologies, including zk, have a lot of room for improvement.

Decentralize authority while still maintaining regulatory compliance; this may also require some changes to traditional compliance systems to recognize new forms of verification.

Most RWA protocols still have some way to go before they can truly preserve financial products for professional investors and enable permissionless access.