Original: Liu Jiaolian

On the 24th, three departments (the People's Bank of China, the State Financial Supervision and Administration Bureau, and the China Securities Regulatory Commission) jointly released a major financial policy, which attracted global attention. This article will focus on thinking and judging how this set of policies will affect the future of the A-share market, Chinese bonds, and BTC.

Let’s first summarize the key points of this policy, that is, the clauses with real money. The first step is to distinguish between the weapon of criticism (verbal guidance) and the criticism of the weapon (real money). There are three main aspects:

First, lower the reserve requirement ratio and interest rates.

Among them, the reserve requirement ratio is to reduce the bank deposit reserve ratio by 50bp, which can immediately release liquidity of about 1 trillion RMB. It may be further reduced by 25-50bp this year.

The interest rate cut was made through the 7-day reverse repo tool, with the operating rate reduced by 20bp - double the usual 10bp reduction pace - from 1.7% to 1.5%. This will directly affect the deposit and loan market, guiding the LPR (loan market benchmark rate) and deposit rates to decline simultaneously. This will help maintain the net interest margin and avoid compressing the profits of commercial banks. At the same time, it will lower the ceiling of treasury bond yields, which will help guide funds in the treasury bond market.

The market interest rate we usually refer to is the LPR. The central bank did not follow the Fed's pace of interest rate cuts, which means that the LPR will remain unchanged for the time being. Currently, the 1-year LPR is 3.35%, and the LPR for more than 5 years is 3.85%.

What is the current deposit interest rate? According to the data adjusted by ICBC on July 25, 2024, the current deposit rate is 0.15%, the 3-month fixed deposit rate is 1.05%, the 6-month fixed deposit rate is 1.25%, the 1-year fixed deposit rate is 1.35%, the 2-year fixed deposit rate is 1.45%, the 3-year fixed deposit rate is 1.75%, and the 5-year fixed deposit rate is 1.8%.

What about government bonds? Data as of September 20: 3 months 1.4%, 6 months 1.43%, 1 year 1.39%, 2 years 1.38%, 3 years 1.5%, 5 years 1.73%, 7 years 1.91%, 10 years 2.04%, 30 years 2.15%.

What do you think of the above data? First of all, the long-term and short-term yields of Chinese bonds are relatively normal, unlike the serious inversion of US bonds - that is, the long-term bond yield is lower than the short-term bond - which shows that China's economic situation is relatively normal, because common sense should be that the longer the repayment time is, the longer the funds are occupied, and the higher the interest paid.

The second thing is abnormal: the yield of the treasury bonds is too low, isn’t it? For example, the 5-year 1.73% is even lower than the 5-year time deposit rate of 1.8%. Isn’t this way out of the norm?

As I mentioned before, bond yields are inversely proportional to their prices. The low yields on government bonds indicate that some funds are desperately buying government bonds, to an almost irrational degree!

This has resulted in a phenomenon whereby Chinese bond yields have been bought at an extremely abnormally low point.

The central bank has long been publicly warning institutions not to rush into government bonds, but the weapon of criticism seems to be ineffective, so this time it directly brought out a heavy-duty move to criticize the market with weapons.

This big move is the new tool introduced for the first time: interchange convenience.

Secondly, new monetary policy tools were introduced: swap facilities and special re-loans for stock repurchases and share purchases.

Why is this swap facility a big move? Because the emergence of this tool has unprecedentedly allowed the central bank to milk the A-share market in a targeted manner.

Someone said with tears in his eyes that every time there was monetary regulation in the past, there would be a prohibition on entering the stock market, but this time it was actually specified that entry into the stock market was mandatory. It really was “the bleak autumn wind is here again, and the world has changed”!

So how does this so-called swap facility work? Simply put, the central bank allows non-bank institutions (such as securities, funds, insurance and other institutions) to pledge assets with general liquidity (such as bonds, stock ETFs, CSI 300 constituent stocks, etc.) to the central bank for high-liquidity assets (such as government bonds, central bank bills, etc.) for the first time.

Please note that what the institutions get in exchange are treasury bonds and bills, not RMB. They need to sell them in the secondary market first, such as selling treasury bonds, before they can get RMB. Oh my god, didn’t the teaching chain just say that now treasury bonds are bought at a very high price by some institutions that don’t listen to advice? Now it’s good, good words can’t persuade the damn ghost, the central bank directly released a bunch of treasury bond shorts, and smashed the market at a high level.

Do the Treasury bond bulls want to continue to fight and try to defeat the central bank, or do they listen to the advice and quickly withdraw from the Treasury bond market? From the bottoming out and rebound of Treasury bond yields, we can see their thoughts and movements.

The last and most important step is that institutions that sell treasury bonds and get RMB are required to reinvest the money in the A-share market. That is, the funds are designated for use: the funds obtained through swap facilities can only be used to invest in the stock market, aiming to improve the liquidity and stability of the capital market.

In other words, these participating institutions can only short government bonds and go long on the A-share market.

Another point is that the central bank emphasized that the swap facility is not to give money directly, and will not expand the scale of base money. Instead, it is carried out through the method of "bond-for-bond", aiming to improve the financing capacity of non-bank institutions without injecting base money.

The meaning of not injecting base currency is to clearly tell the market that this is a zero-sum game and a process of wealth redistribution, forcing the wealth out of the bond market and transferring it to the stock market in a targeted manner.

Some time ago, some treasury bond bulls tried their best to withdraw liquidity from the A-share market and move it to the bond market. The national team quietly buy the dips the bottom below 3,000 points for more than half a year. Many KOL laughed at them for not being able to hold the bottom, desperately trying to trick retail investors into selling at the bottom and exchanging dollars to buy U.S. stocks at high prices. After the Fed cut interest rates, they tricked retail investors into buying bonds, saying that interest rate cuts were good for bonds, etc. But their suggestions were almost never correct.

Now the national team has almost finished buy the dips fishing. The Federal Reserve has also cut interest rates, and the exchange rate pressure has been relieved. The market has also been eagerly waiting for policies for a long time. The right time, right place, and right people.

Institutions that have accumulated a large number of low-priced, high-quality chips can exchange stocks for bonds with the central bank, smash the bond market for money, use the money to boost the stock market, and then exchange the purchased stocks for bonds from the central bank... This cycle of operation will kill the bulls in the bond market and explode the bears in the stock market.

This swap facility is a long-term tool, not a short-term emergency measure. The first phase of 500 billion yuan will be used to test the waters, and there will be a steady stream of hundreds of billions and trillions of yuan waiting to be used.

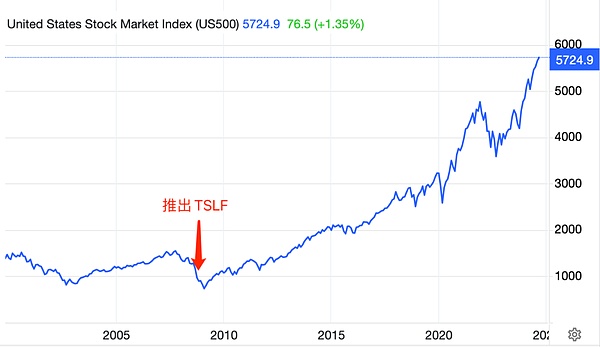

In fact, the Federal Reserve has already had similar tools. The Federal Reserve's swap facility is called the Term Securities Lending Facility (TSLF). This tool allows primary dealers to use less liquid securities as collateral to borrow more liquid Treasury bonds from the Federal Reserve, making it easier to raise funds in the market and boosting the market. It was launched during the 2008 financial crisis and was used again during the 2020 epidemic.

Let's appreciate the 15-year bull run of the U.S. stock market after the Fed applied TSLF: (see the figure below)

As for the other tool, the special re-loan for stock repurchase and increase, it is to guide banks to provide loans to listed companies and major shareholders to support the repurchase and increase of stock holdings. If the major shareholders are confident that they can run the company well, the profit dividend, that is, the dividend rate, can carry trade as long as it exceeds the special loan interest rate, which will help motivate the company's shareholders to repurchase and increase the stock price, and run the company well and give dividends back to shareholders. Of course, as a lever, it is definitely risky. I will not go into details.

The third aspect is the support for the housing market. Continuing to reduce the stock of mortgage loans is not so much to support the housing market as to release the money in the hands of ordinary people to stimulate the consumer market. The only thing that is really related to the housing market is to unify the down payment ratio of the second house with the first house to 15%. Compared with the above big support for the stock market, it seems a bit bland and tasteless.

Obviously, things change over time. From the focus of the policy, we can also see that the country has made up its mind to change its development model, get rid of its dependence on real estate, and guide capital to the stock market and to high-quality enterprises that match the development direction of advanced productivity.

The teaching chain has said, " As for the A-share market, it will also usher in its 20-year wedge breakthrough. "

Complaining too much may break your heart, so you should take a broad view of things.

The above teaching chain has carefully analyzed that the launch of the heavyweight long-term tool swap facility by the central bank will hit the bond market in the short term, push up government bond yields, and push up the stock market.

We can also judge that when the long-term Chinese bond yields bottom out and rebound in a short period of time, it will often be accompanied by a bull market wave of BTC.

This month, China and the United States have seen major turning points in their monetary policies, which coincides with the end of this year's half-yearly BTC cut and the prelude to next year's bull market. As the market is shifting from divergence to finding the direction of a bull market, one cannot help but sigh that there is indeed God's will in the dark.

I am happy to see the rice and beans rolling in waves, and heroes all over the place in the evening mist.