The tokenization of Real World Assets (RWA) is accelerating, attracting the attention of many Web3 entrepreneurs and traditional financial institutions. Recently, Binance Research released a research report on the theme of "RWAs: On-chain Revenue Havens." Reports show that the participation of traditional financial institutions, such as BlackRock and Franklin Templeton, has pushed the tokenized Treasury market to new highs. Private bonds, credit, commodities, stocks, real estate and other non-U.S. debt are all major areas of RWA, and emerging categories also include air rights, carbon rights and art. In addition, some new startups are also building blockchains based on their own RWA.

Table of Contents

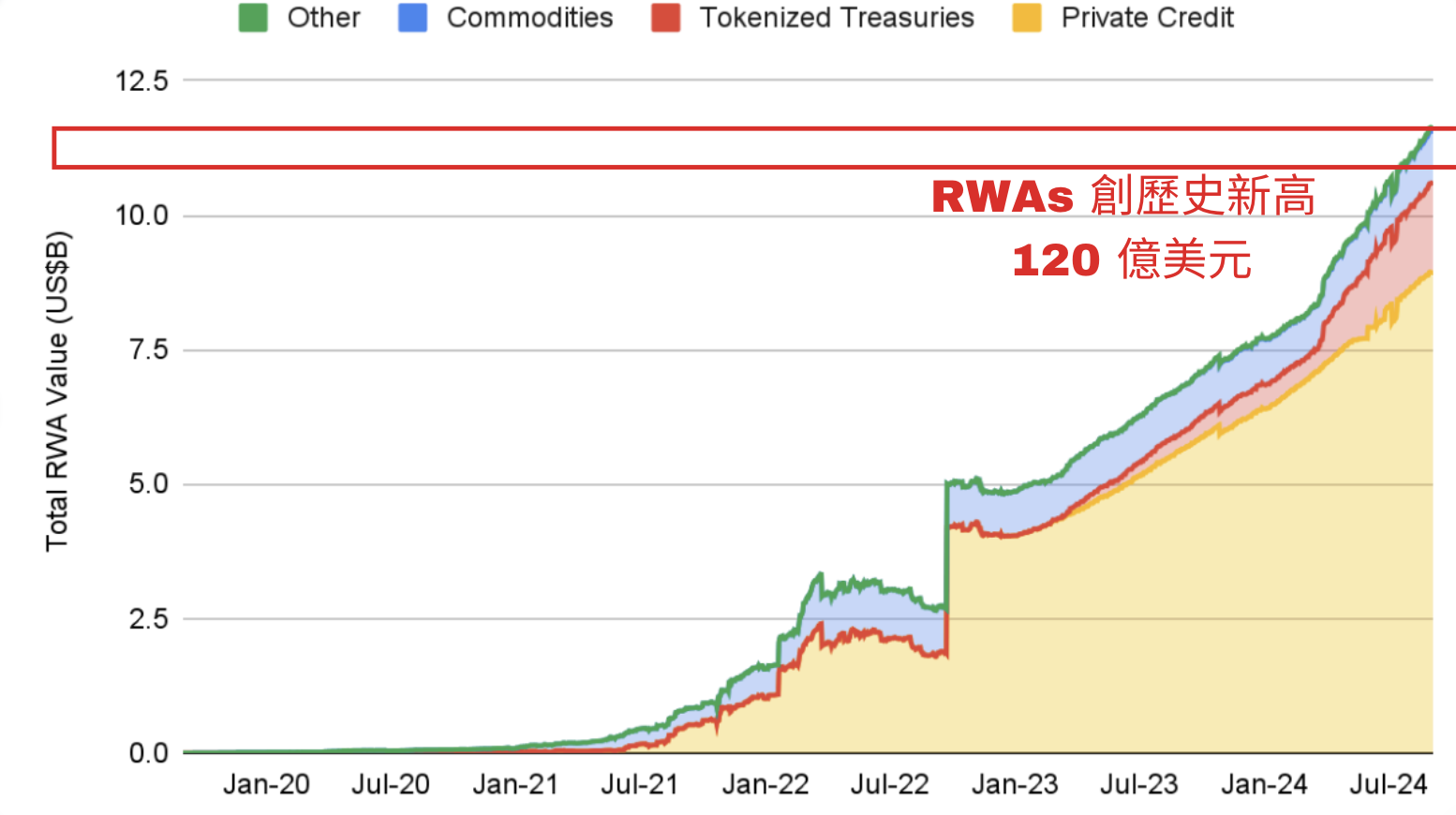

ToggleRWA’s current market capitalization exceeds US$12 billion and will surely exceed that level in the future

RWA stands for Real World Assets, which represents the integration of many physical or intangible assets in the non-blockchain world, such as real estate, currencies, bonds, commodities, etc. that can be found everywhere, through tokenization technology. Import it into the blockchain and turn it into an asset that can be traded on the chain, which is "real asset tokenization."

Allowing traditional finance (TradFi) to benefit from the efficiency, transparency and speed of blockchain technology. At the same time, Web3 may be exposed to traditional financial investment products. And as a bridge between TradFi and DeFi, it enables traditional financial assets to operate in the DeFi world and injects a large amount of liquidity.

As of September 12, 2024, the market value of on-chain RWAs has exceeded US$12 billion (excluding the stablecoin market of US$175 billion). And hit a record high, especially tokenized products such as U.S. Treasury bonds account for a considerable proportion of the market.

U.S. debt has grown explosively, but credit still ranks first

Key categories in the RWA space include tokenized U.S. Treasuries, private credit, commodities, stocks, real estate and other non-U.S. debt securities. The following is the tokenized market capitalization of each category as of September 2024:

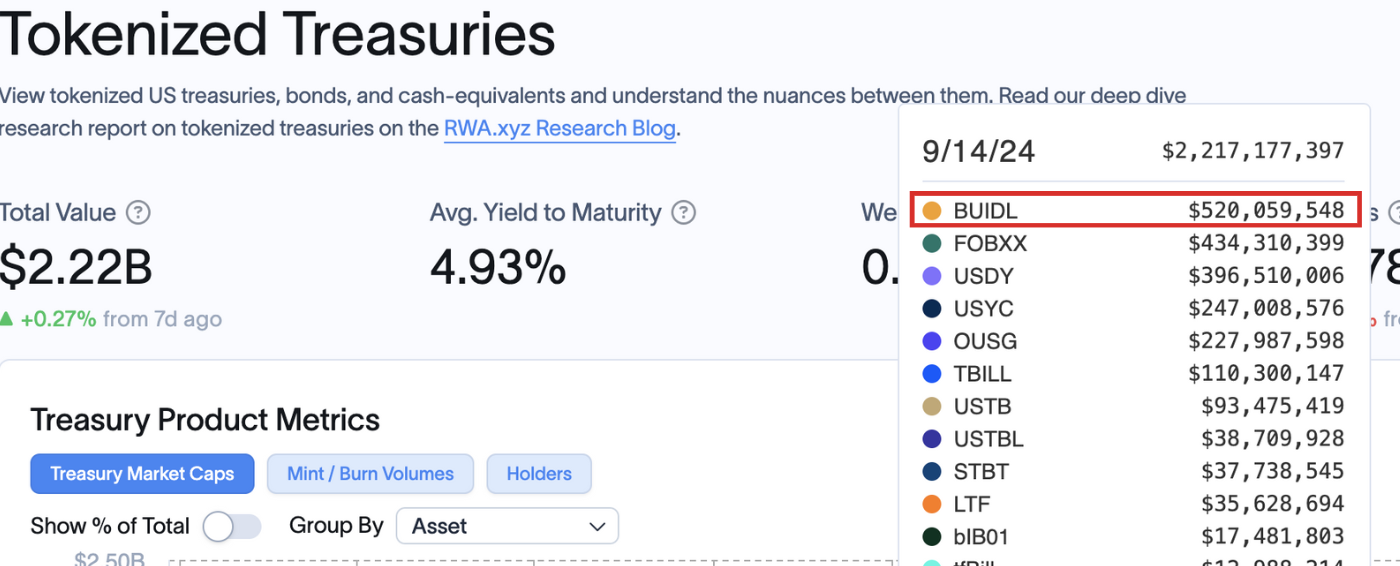

U.S. Treasury Debt

With a market capitalization of US$2.2 billion, the extent and frequency of interest rate cuts by the Federal Reserve have become the focus of market attention, currently represented by BlackRock Tokenization Fund ( BUIDL ).

Personal Credit (Small and Medium Enterprise Financing)

With a market capitalization of US$9 billion, the issuer is represented by Figure . As banks face tighter lending standards since the 2008 financial crisis, private credit's overall share of the macroeconomy has grown, with active lending growing 56% over the past year.

Gold (representative of commodities)

The market capitalization is US$990 million, represented by Paxos Gold (PAXG) and Tether Gold (XAUT) .

Non-U.S. bonds, corporate bonds and stocks

With a market capitalization of $80 million, these markets are much smaller and in an emerging stage of development.

The real estate, carbon rights and air rights markets are stable, and the art market is rising.

The report shows that the real estate, carbon rights, and air rights markets are gradually developing steadily. For example, Parcl , which is developing the real estate tokenization market on the Solana blockchain, Toucan, which integrates regenerative finance (ReFi), focuses on the tokenization of carbon rights, and the startup SkyTrade tokenizes air rights on land. In addition, companies like Plume Network adopt flexible strategies to develop modular L2 blockchain platforms with the goal of tokenizing assets such as watches and artwork, which has potential in the future.

Traditional financial institutions have successively participated in the RWA market

BlackRock

The USD Institutional Digital Liquidity Fund (BUIDL) launched by BlackRock is currently the leader in the tokenized fund market, with a market value of more than $520 million. In addition to entering the tokenized fund market, BlackRock is also an important player in the US spot ETF market and currently owns the Bitcoin and Ethereum spot ETFs with the largest market capitalization.

Franklin Templeton

Franklin Templeton has gradually penetrated into the real world assets (RWA) market and launched the OnChain US Government Money Fund (FOBXX), which is currently the second largest tokenized fund market with a market value of more than US$440 million and a market value of up to US$430 million on the Stellar chain.

WisdomTree Investments

As a world-renowned ETF giant and asset management company, WisdomTree Investments has gone a step further and launched a number of "digital funds", including tokenized treasury bills, stocks and other strategic funds. The total assets under management of these digital funds currently exceed US$23 million.

Oracles are worth paying attention to, analyzing six different projects

In order to build a strong foundation for RWA, key technologies are indispensable. Such as smart contracts, oracles, identity and compliance, and custody solutions. The oracles responsible for the exchange of smart contracts and real-world information are very important. It also helps initiate on-chain operations based on off-chain legal agreements and trigger smart contracts to respond to loan defaults. The report stated that it is also worth paying attention to the development of oracles for RWA in the future.

The report also analyzes six different RWA projects, including Ondo (structured finance), Open Eden (treasury bond tokenization), Centrifuge (tokenization, structured credit, aggregation), Parcl (synthetic real estate), Toucan (carbon credit tokenization) and Jiritsu (zero-knowledge tokenization).

Ondo structured finance, tokenized funds for bulk

Backed by short-term U.S. debt and bank deposits, it mainly invests in BlackRock's tokenized funds BUIDL and FedFund, and supports multiple blockchains such as Ethereum, Solana, Sui, and Arbitrum.

OpenEden treasury bond tokenization, 24-hour short-term U.S. debt tokenization service

It provides 24-hour on-chain U.S. short-term Treasury bond investment services. Since its establishment in 2023, it has become Asia's largest issuer of Treasury bond tokenization products, supporting Ethereum and Arbitrum.

Centrifuge bills proof tokenization, RWA is minted into NFT

Centrifuge is a Substrate-based L1 blockchain that focuses on tokenizing various invoices, notes, securities, real estate, royalties and other real assets (RWA) into NFTs, which are then used as collateral for lending on the DeFi platform. .

Parcl real estate tokenization, easy purchase of real estate index

Parcl is a tokenized real estate protocol that allows users to buy and sell partial tokens of real estate indexes. For example, buying real estate indexes in Los Angeles, New York, or other cities around the world does not require the purchase of physical real estate and lowers the investment threshold.

Toucan carbon rights tokenization to respond to global warming and save energy and reduce carbon emissions

Due to the impact of global warming, many countries have joined the ranks of mitigating and controlling carbon emissions. Toucan protocol is a carbon rights tokenization platform that uses tokens to represent carbon emission offsets. Enables companies and individuals to purchase, trade and destroy carbon rights in a decentralized manner to offset carbon emissions.

Jiritsu uses zero-knowledge proofs combined with oracles to verify the compliance of tokenized assets

Jiritsu is an L1 blockchain based on Avalanche Subnet technology stack. It uses zero-knowledge proof (ZKP) combined with multi-party computation (MPC) as a technically supported oracle machine. It uses a double verification system to verify asset compliance and the presence of real assets in the market. to support the tokenization of various assets including gold, real estate and traditional financial assets.

The technical risks and prospects of RWA, but problems remain when establishing a new chain

The report stated that several technical challenges have also emerged in the RWA field, such as centralization risks (due to the nature of assets and compliance requirements), risks of relying on third-party intermediaries, and the technical complexity of the system is not necessarily proportional to the benefits. In the future, A more robust oracle will shorten the information time difference, maintain accuracy, and ultimately maintain personal data security and compliance.

More and more RWA protocols choose to build their own L1 or L2 blockchain, which can better control compliance and regulations, easily conduct KYC authentication for users, and accelerate protocol optimization. But this also creates problems such as network security and insufficient liquidity. For the new RWA protocol, it is easier to run on main chains such as L1 or L2, because these blockchains already have built-in compliance tools and KYC systems, and there is no need to build them from scratch. However, new chains often encounter "cold start" problems and have higher barriers to entry for users, such as setting up wallets and learning new usage procedures.

The Fed’s interest rate adjustments and the direction of legal supervision still require attention

The report also mentioned that from a macroeconomic perspective, the United States is about to enter an interest rate cutting cycle. As the U.S. dollar weakens as the Federal Reserve begins to cut interest rates on September 18, 2024, and most of the RWA market is supported by U.S. Treasury bonds and cash assets, returns are bound to decrease. However, because RWA has diversification, transparency and other factors, it may This makes RWA a quite attractive investment option in a low interest rate environment.

Even though most RWAs operate on public chains, if users want to use them, they still have to complete KYC certification or go through verification steps such as identity (general and professional investors). Other products also require a minimum amount to be transferred. In other words, RWA is still no different from traditional financial assets.

In summary, although the RWA protocol uses blockchain technology, there is still room for improvement in terms of laws and regulations and user identity restrictions, and it is still some distance away from truly decentralized, zero-verification financial products.