Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

One week after the election, spot prices have shown remarkable strength, with BTC reaching new all- time highs following an explosive rise. ETH, while not yet at record levels, has also gained upward momentum, displaying a steady increase since the election date. In the derivatives market, sentiment has strengthened for both tokens: futures implied yields, perpetuals funding rates, and skew all indicate a highly positive outlook. ATM implied volatility, which initially dropped after the election event risk passed, has since surged, inverting the term structure. Both BTC and ETH now benefit from a powerful combination of spot price gains and robust bullish derivatives activity, signalling strong demand to participate in further upside potential.

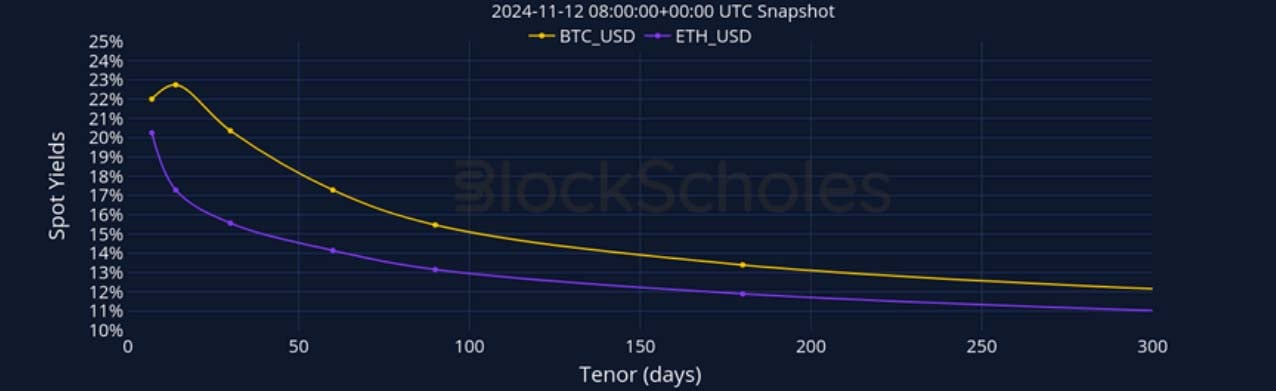

Futures Implied Yield, 1-Month Tenor

ATM Implied Volatility, 1-Month Tenor

Crypto Senti-Meter

BTC Derivatives Sentiment

ETH Derivatives Sentiment

Futures

BTC ANNUALISED YIELDS – BTC’s yield term structure levels have risen strongly across all tenors but more so at the front end of the structure.

ETH ANNUALISED YIELDS – ETH’s yield curve remains inverted, showing rising levels for all tenors.

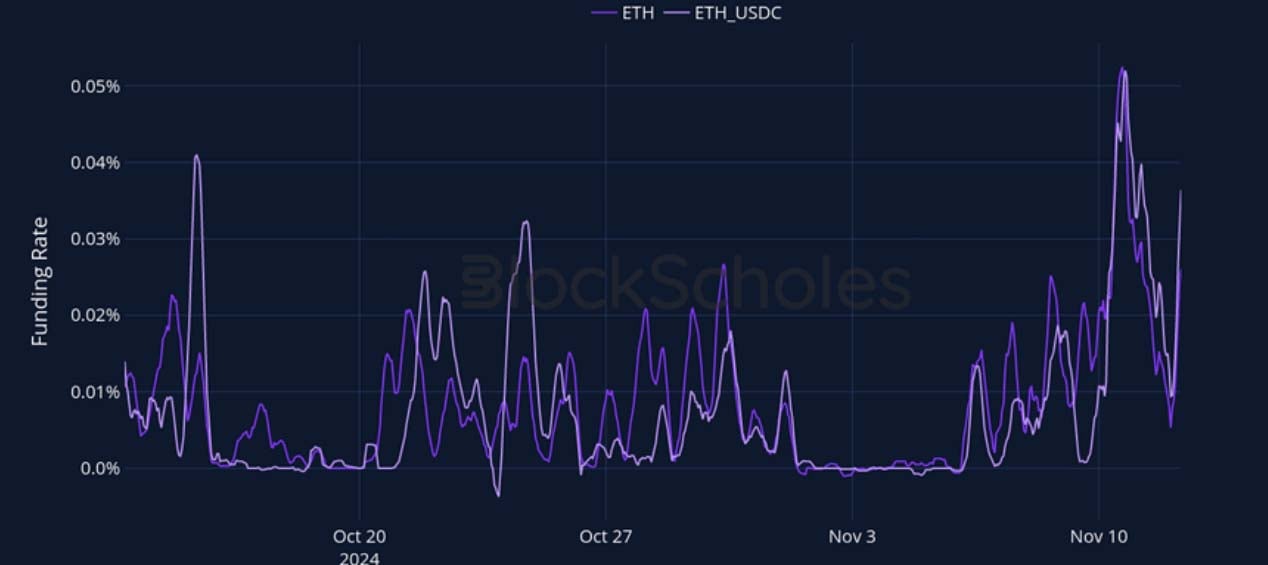

Perpetual Swap Funding Rate

BTC FUNDING RATE – BTC’s perpetual funding rates return strongly positive after the election, showing increased demand for participation in the rally.

ETH FUNDING RATE – ETH’s funding rate is similar to BTC’s recent movements, returning to positive after a period of neutral levels.

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – The term structure of volatility has re- inverted and shows growing levels across tenors, especially at the front end.

BTC 25-Delta Risk Reversal – Skew levels are positive across all tenors, indicating an overall strong bullish sentiment.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – ETH’s implied volatility term structure remains heavily inverted, mirroring BTC’s sharply increasing levels.

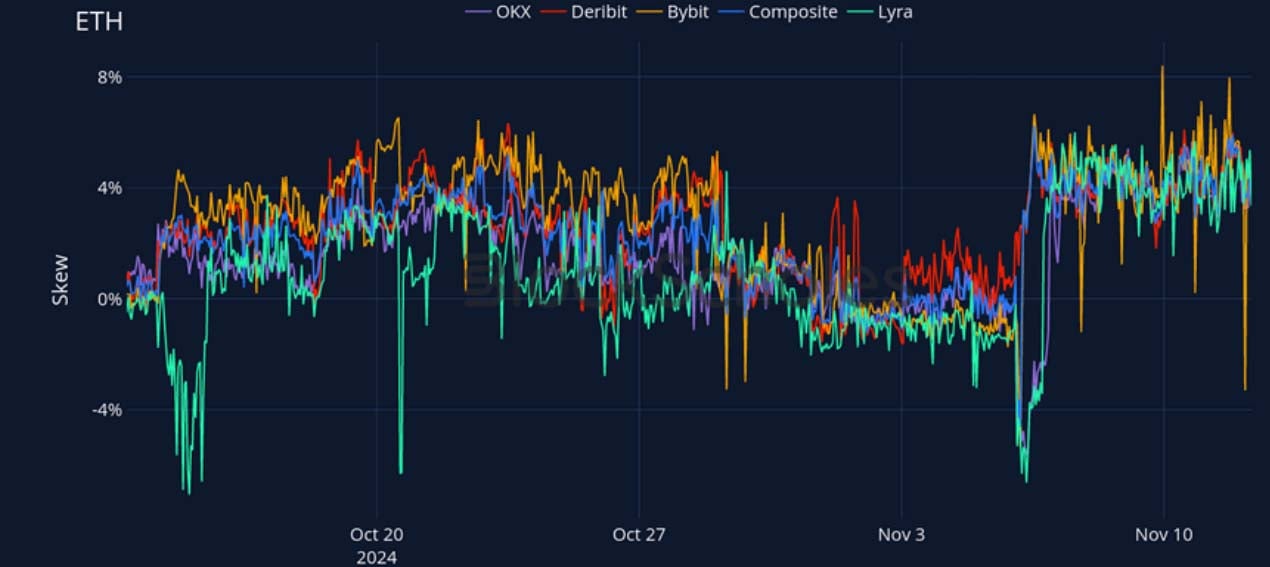

ETH 25-Delta Risk Reversal – ETH’s volatility smiles now indicate a strong demand for upside exposure across the term structure.

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

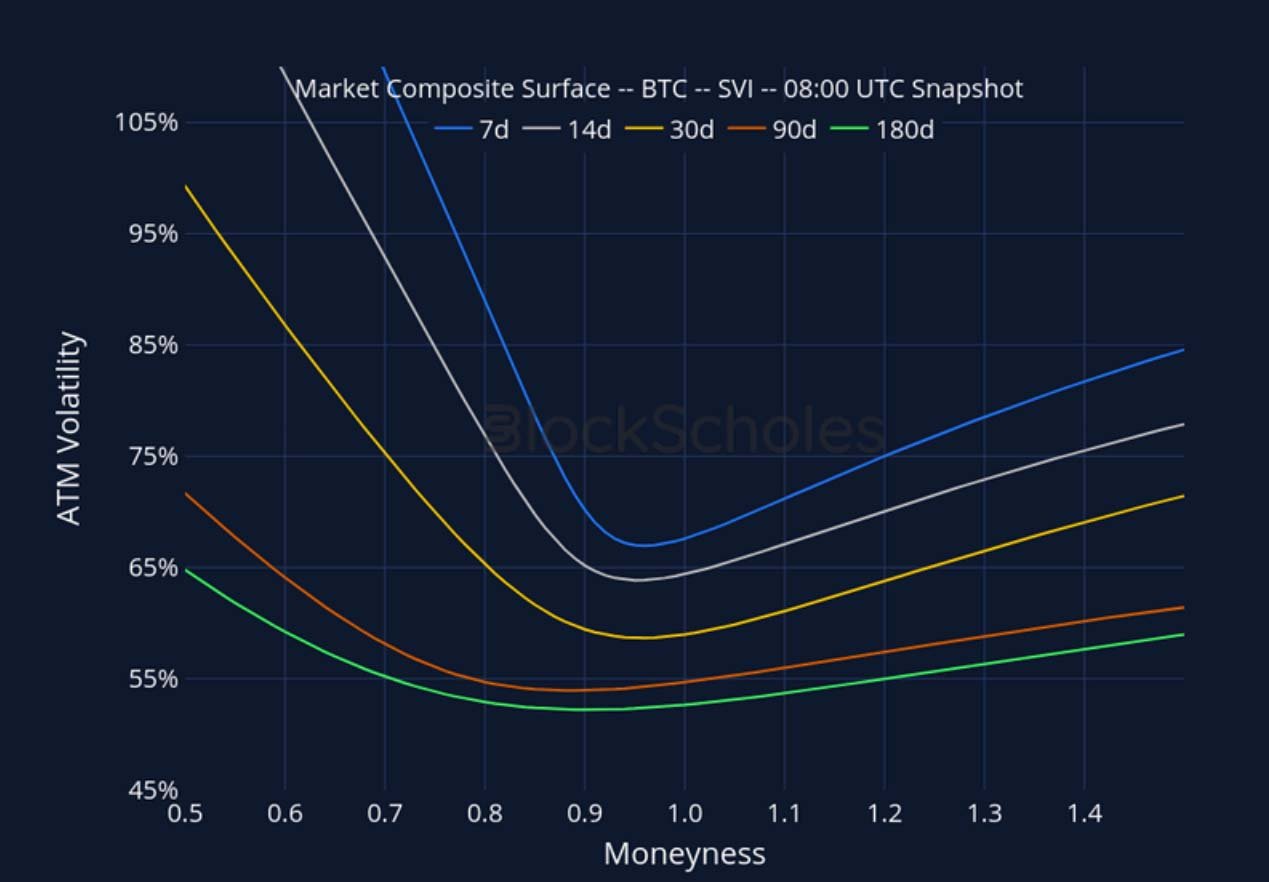

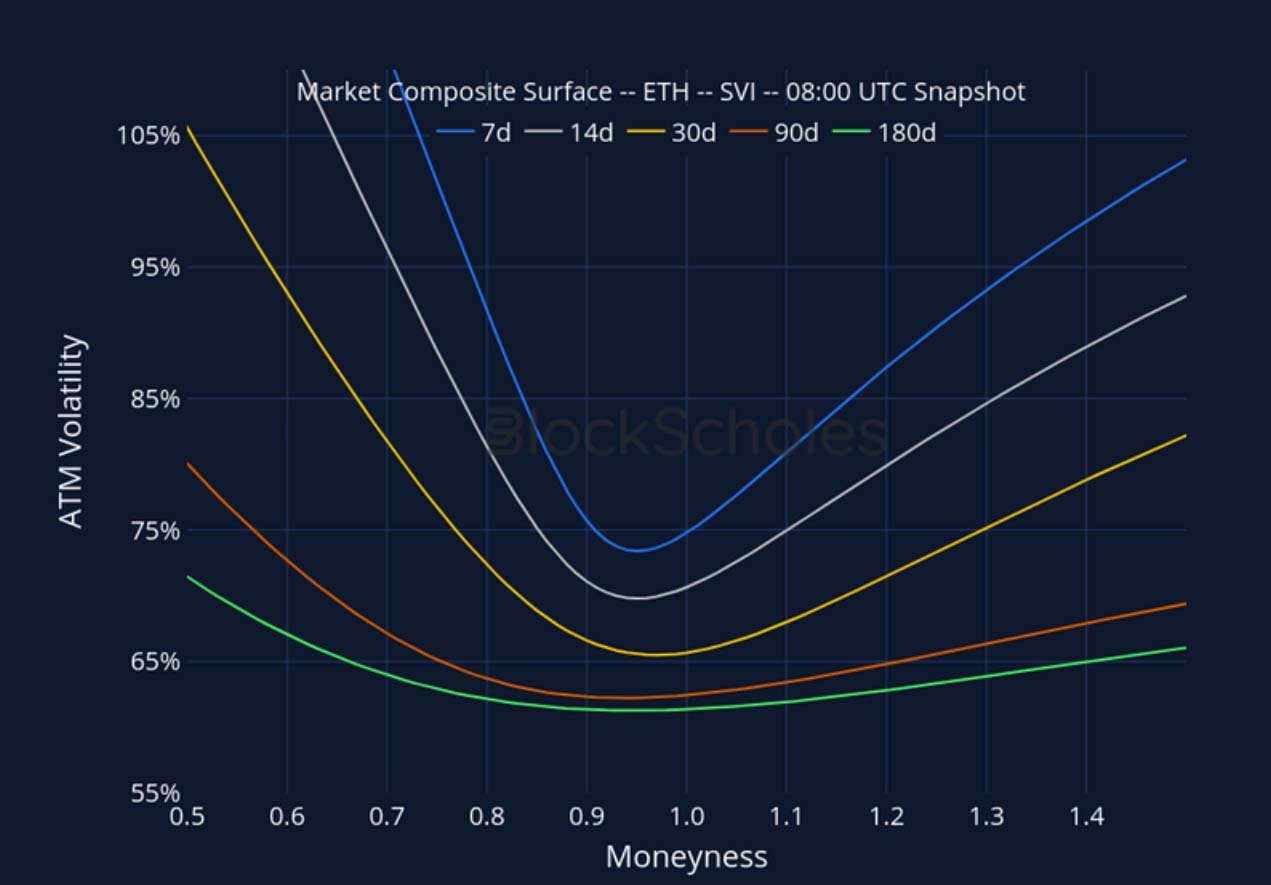

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 8:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 8:00 UTC Snapshot.

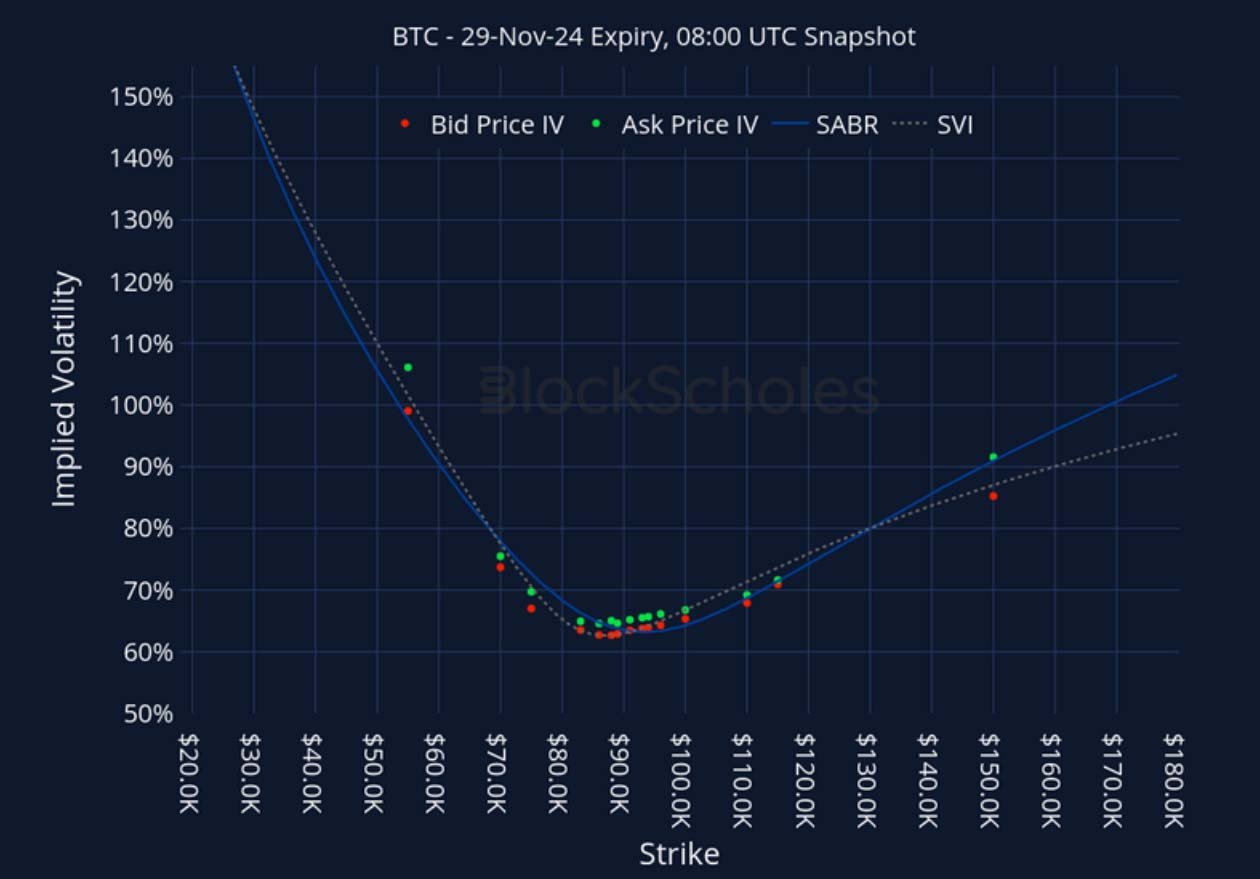

Listed Expiry Volatility Smiles

BTC 29-NOV EXPIRY – 8:00 UTC Snapshot.

ETH 29-NOV EXPIRY – 8:00 UTC Snapshot.

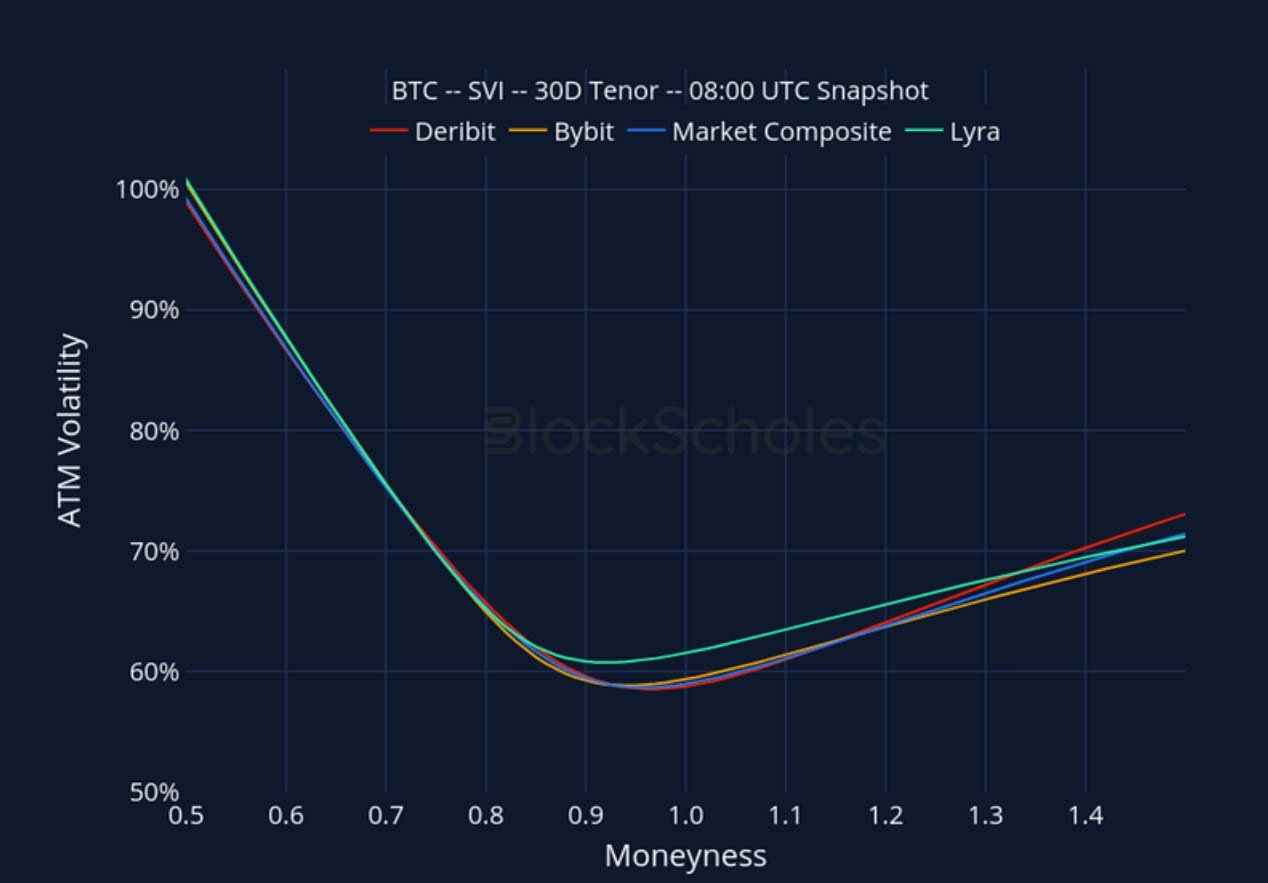

Cross-Exchange Volatility Smiles

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

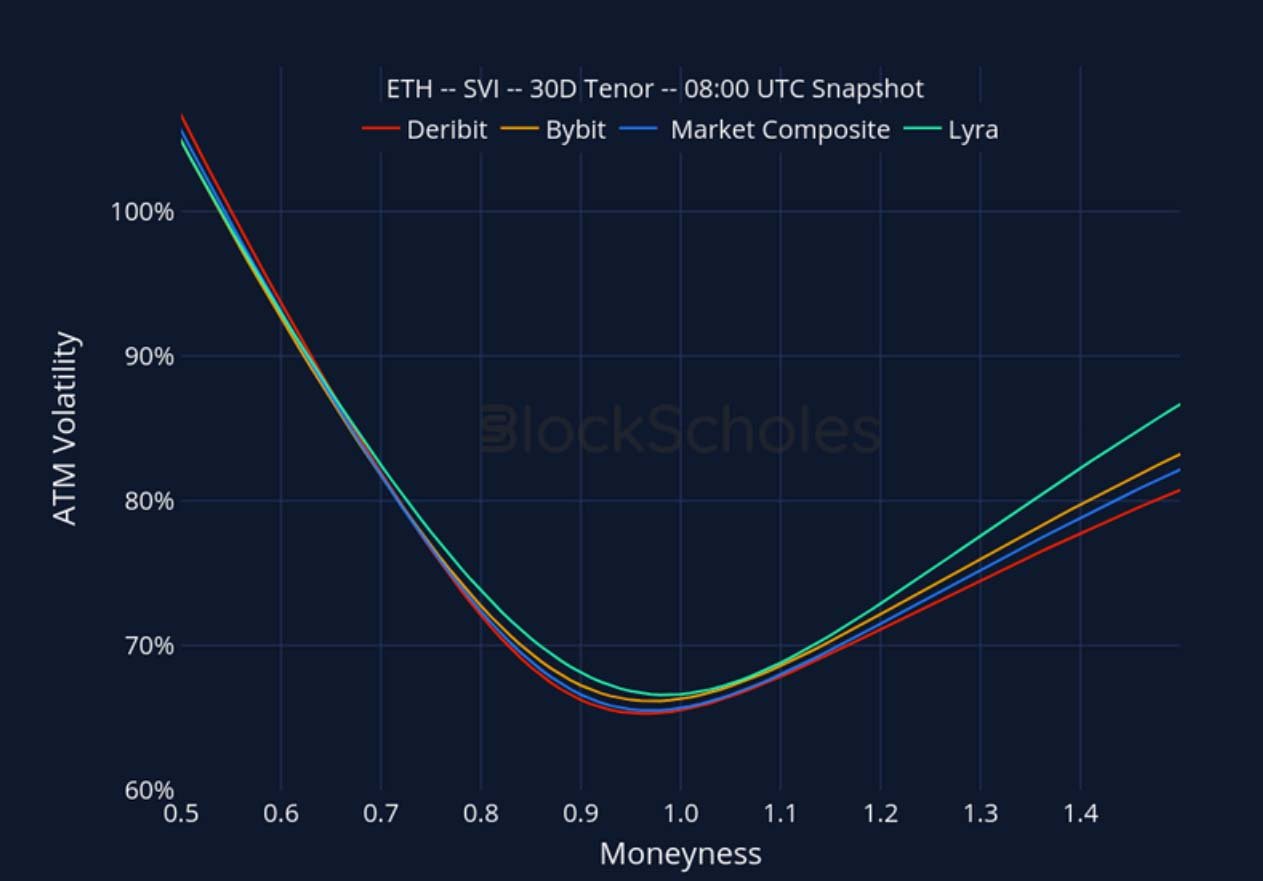

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

Constant Maturity Volatility Smiles

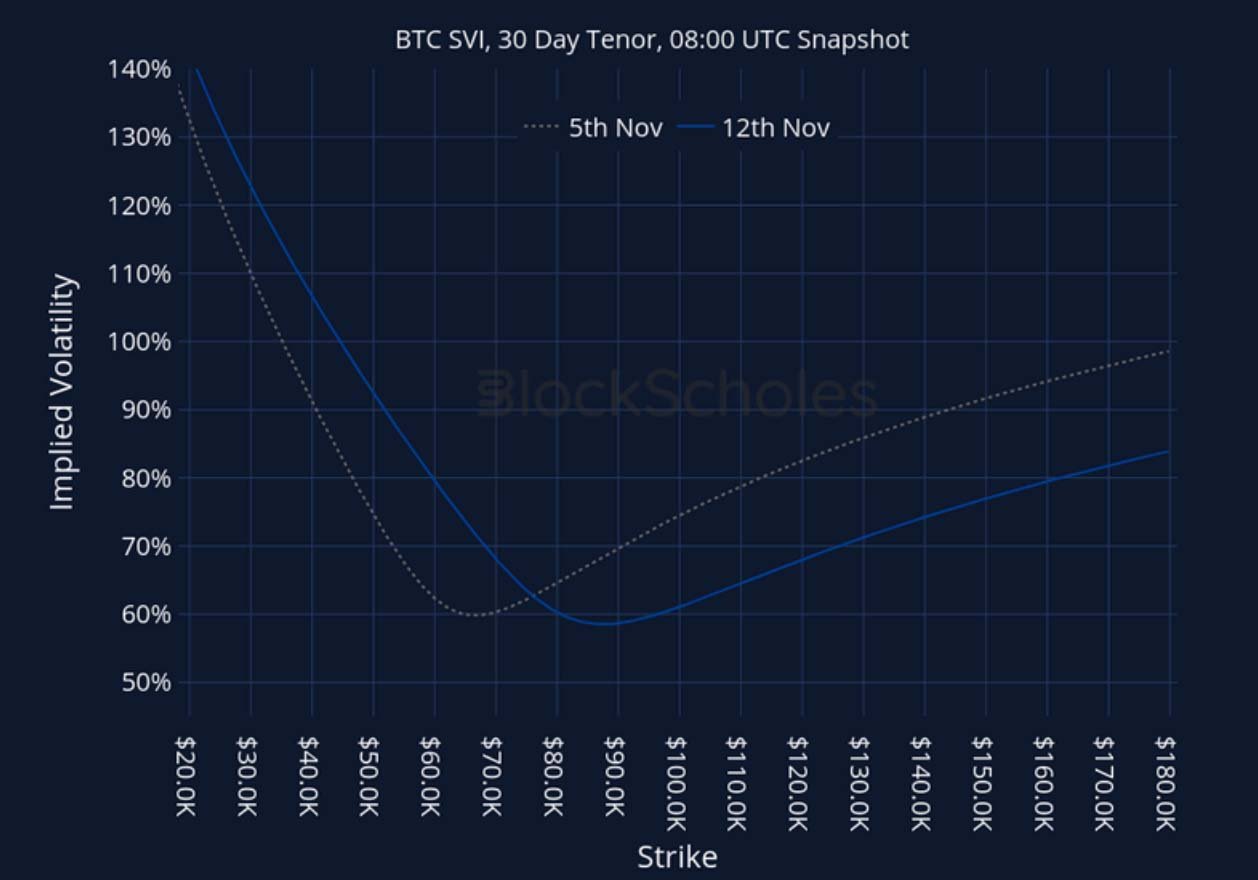

BTC SVI, 30D TENOR – 8:00 UTC Snapshot.

ETH SVI, 30D TENOR – 8:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.

RECENT ARTICLES

Crypto Derivatives: Analytics Report – Week 46

Block Scholes2024-11-12T20:29:59+00:00November 12, 2024|Industry|

Crypto Derivatives: Analytics Report – Week 45

Block Scholes2024-11-06T08:49:40+00:00November 6, 2024|Industry|

Crypto Derivatives: Analytics Report – Week 44

Block Scholes2024-10-31T09:08:42+00:00October 31, 2024|Industry|

The post Crypto Derivatives: Analytics Report – Week 46 appeared first on Deribit Insights.