Written by:Chainalysis

Compiled by: Felix, PANews

Over the past few years, cryptocurrencies have become a mainstream asset class, with institutional investment being a driver of global crypto adoption. In 2024, several notable developments solidified the position of cryptocurrencies in traditional finance (TradFi). Institutions such as BlackRock, Fidelity, and Grayscale launched Bitcoin and Ethereum ETPs, providing retail and institutional investors with easier access to these digital assets. These financial products have drawn attention to the investment value of cryptocurrencies compared to traditional securities.

Additionally, the tokenization of real-world assets (such as bonds and real estate) is also gaining popularity, enhancing the liquidity and accessibility of financial markets. Siemens issued a $330 million digital bond, indicating that traditional financial institutions (FIs) are adopting blockchain to improve operational efficiency. While many similar institutions have already started incorporating crypto technology into their service offerings, others are still in the evaluation stage.

This article outlines the considerations for launching crypto products, enabling financial institutions to assess market opportunities while addressing regulatory and compliance requirements.

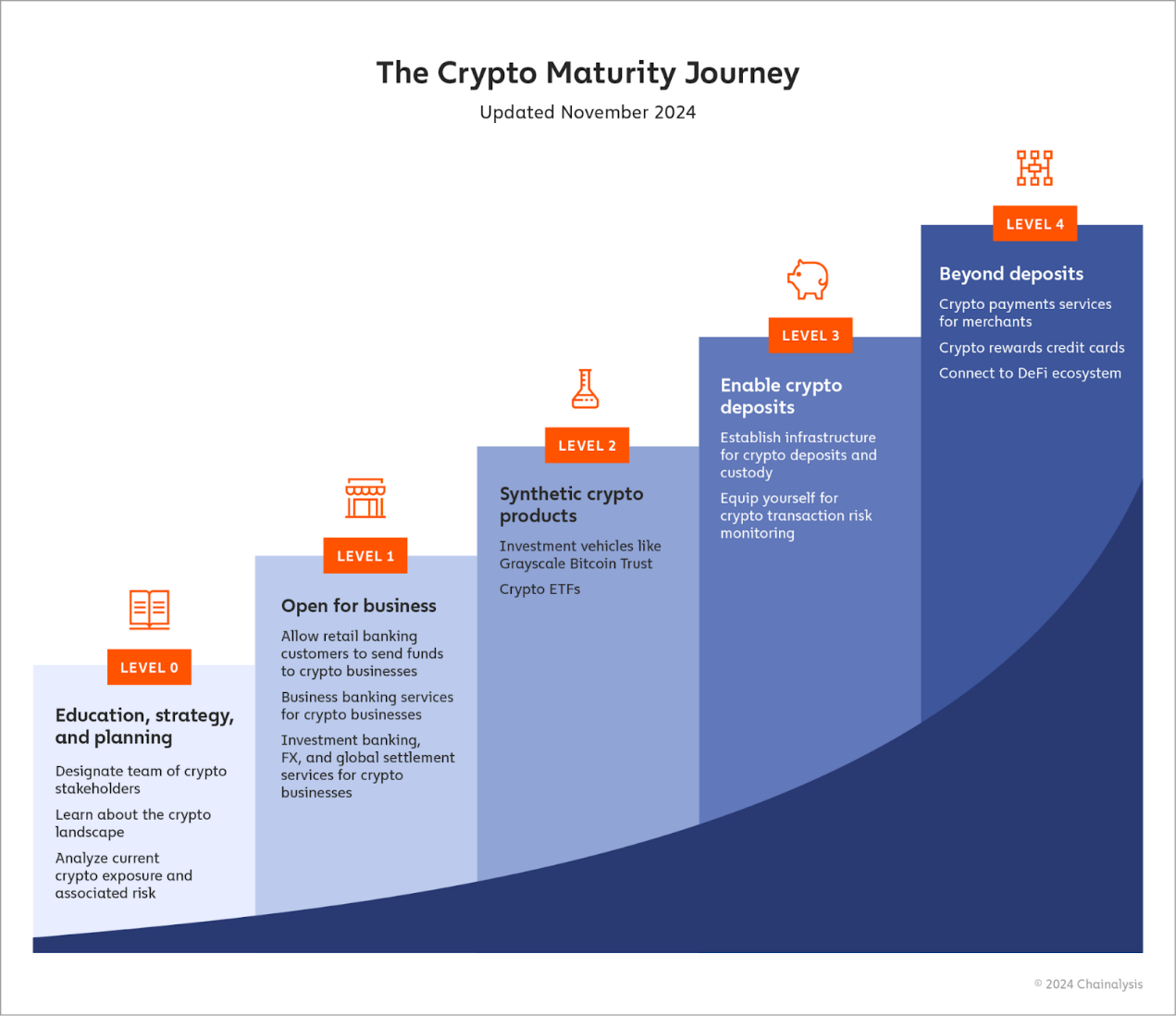

The article explores five typical maturity levels for financial institutions adopting cryptocurrencies:

Level 0: Education, Strategy, and Planning

Level 1: Open for Business

Level 2: Synthetic Crypto Products

Level 3: Enabling Crypto Deposits

Level 4: Complex Products, DeFi, etc.

Level 0: Education, Strategy, and Planning

Considering entering the crypto space typically starts by designating key stakeholders across multiple functional areas, as well as the person responsible for leading this work. This person may be hired from the crypto industry, although external hiring can also wait until the business is open, when the firm is exploring how to support cryptocurrencies or launching a crypto program. Generally, the designated stakeholders can be divided into two categories:

Those directly dealing with cryptocurrencies or crypto business; such as investment bankers, commercial bankers, traders, corporate lenders, and wealth managers.

Enterprise risk professionals; they will determine which crypto products are feasible, such as specialists in market risk, KYC, AML/CFT, sanctions, financial crime and fraud, and compliance.

These are just examples, but these two groups will be the major participants in launching any crypto products. However, when these products become a reality, they may require coordination and support across the entire company, as well as executive support and involvement.

Once the initial crypto team is established, bringing them together to understand how to enter crypto in a way that fits the institution's risk appetite, and identify the learning gaps that must be filled to properly assess the risks of any crypto opportunity, including any compliance risks. This includes training the team to use Block chain analysis tools.

Banks at Level 0 can also start by understanding their current crypto exposures and measuring the risks arising from them. Given the current adoption levels, many banks have some financial connection to the crypto industry, whether through retail banking programs, cross-border financial services, or corporate lending programs. In this process, banks may need to understand the specific crypto businesses they or their clients interact with, and consider using industry intelligence tools to screen them.

Finally, any financial institution interested in entering the crypto space should start by learning as much as possible about the industry. There are many resources available.

Educational content: Industry leaders regularly publish content that can help institutions better understand the opportunities and risks in the crypto ecosystem.

Social media: The crypto industry is one of the most active on social media, with Crypto X being a focal point. For example, Vitalik regularly shares his views on the latest industry developments, and a large group of insightful online journalists, commentators, and amateur investigators.

Community: The crypto community can also be broadly engaged in real-time dialogue, as almost every project has its own Discord or Telegram channel where users gather to chat. In an active channel, an hour can be equivalent to hours of research. Additionally, these chats often provide opportunities for in-person meetings and socializing.

Personalized consulting: You can schedule with experts to learn how to better utilize these tools and gain more industry information.

Level 1: Open for Business

Once a financial institution has identified its key stakeholders, educated them on the crypto ecosystem, and established its risk appetite and compliance procedures, it can start considering its customers. The first step is to start supporting and engaging with crypto businesses, just like you would with any other business.

In retail banking, this means allowing customers to transact with crypto businesses that fit their risk appetite. Historically, financial institutions have struggled to accurately assess retail banking business.

Due to the lack of standardized regulatory frameworks, reliable data sources, and transparency in crypto market activities, the reduced risk exposure of customers and other crypto business counterparties has posed challenges in effectively assessing risk. But with tools like crypto compliance solutions, many banks have successfully modified their processes to properly assess the risk of individual crypto businesses and expand their exposure to the industry in a secure and regulated manner.

Crypto-friendly banks can also start accepting crypto businesses as customers. Notably, BankProl (formerly Provident Bank), one of the oldest banks in the US, now offers services specifically tailored for crypto businesses, including US dollar-denominated accounts and crypto-to-fiat conversions. Banks like AllyBank and Monzo also allow customers to connect their accounts to external crypto exchanges, reducing the friction between crypto and TradFi, and making it easier for users to manage their crypto as well as traditional assets.

Banks can provide more services to crypto customers. For example, in 2018, JPMorgan Chase and Goldman Sachs advised Coinbase on a direct listing. Recently, Coinbase sought advisory services from M&A specialist Architect Partners to acquire the derivatives exchange FairX, after Architect had merged with crypto investment bank Emergent. Many crypto businesses have now grown into global operations and also need foreign exchange (FX) services, as well as more robust global settlement mechanisms.

Architect's acquisition of Emergent highlights another key need: to enter the crypto space, Architect required the crypto expertise that Emergent possessed. Fortunately, this can be achieved through targeted hiring rather than full-scale acquisitions. Building one or more digital asset teams means recruiting experienced crypto experts in key areas, such as compliance, security, and any other specific services the company wishes to offer.

Level 2: Synthetic Crypto Products

Once banks are comfortable working with crypto businesses, they may want to help retail and institutional clients access the crypto markets. However, this does not mean they must accept crypto deposits or hold crypto on behalf of clients. Instead, financial institutions can offer synthetic investment products based on cryptocurrencies, allowing clients to gain some of the upside of cryptocurrencies without actually holding the crypto deposits.

In 2024, Bitcoin ETPs emerged as a breakthrough tool for providing crypto exposure. The most prominent ETPs include BlackRock's iShares Bitcoin Trust (lBlT) and Fidelity's Wise Origin Bitcoin ETP (FBTC), both of which hold Bitcoin. Similarly, Ethereum ETPs have also gained traction. Major funds like VanEck and ArkInvest's Ethereum ETPs launched in 2024, allowing investors to indirectly hold the native token Ether of the Ethereum network. Given the critical role of Ethereum and smart contracts in DeFi, these ETPs provide a direct way to invest in the development of the blockchain.

Looking to the future, ETP may also appear on other blockchains such as Solana. Although ETP on Solana and others have not yet been approved, investors can already invest through products like Grayscale's SolanaTrust (GSOL). As the Solana blockchain ecosystem continues to expand, more ETP may emerge to meet the growing demand from investors.

Level 3: Enabling Crypto Deposits

At Level 3, banks allow customers direct access to the crypto market, allowing them to deposit digital assets, and may even custody these assets on their behalf. By 2024, while only a few traditional financial institutions have taken this step, the growing interest from retail and institutional clients is driving more banks to support crypto deposits.

Similarly, BNY Mellon did not build transaction monitoring tools from scratch, but instead integrated Chainalysis software, using our product suite for real-time transaction monitoring, viewing real-time risk information on crypto companies that clients may interact with, and investigating suspicious activity. This allows them to roll out crypto solutions faster, with fewer upfront resources, while also leveraging crypto-native expertise.

Fortunately, financial institutions are not exploring this space alone. Partnerships with crypto-native companies allow banks to outsource the technological complexity of holding digital assets. BNY Mellon launched its own digital asset custody solution in 2022. BNY Mellon did not build the entire platform itself, but collaborated with digital asset security firm Fireblocks to obtain the infrastructure they needed.

Level 4: Complex Products, DeFi, etc.

In terms of crypto adoption, few financial institutions offer products beyond accepting deposits, but that does not mean unheard of. For example, Fidelity expanded its custody services to allow institutional clients to pledge Bitcoin as collateral in DeFi-based lending, while SEBA Bank continues to collaborate with DeFi native companies like DeFi Technologies, which may be the fastest growing and most exciting area in crypto.

Payments is another area where crypto adoption is progressing. Visa continues to lead in this space, recently expanding its stablecoin settlement capabilities to allow USDC to be transacted with merchant acquirers. Similarly, PMC's IP Coin continues to support commercial transaction payments, further integrating blockchain into traditional banking.

Conclusion

As crypto becomes more mainstream, banks are recognizing ways they can help their clients, while driving revenue and trying to incorporate it into a larger strategy. While it may seem daunting at first, banks can adopt crypto in a structured, incremental way, allowing them to test and refine their products at each step.

The key is determining the right types of products and services to build at each step, and the inherent transparency of crypto makes this easier. With the right tools, financial institutions can interact their blockchain-based transaction data with their own proprietary records, observe how funds flow between different types of wallets and services, and use this data to inform business decisions, identifying which crypto services best suit their target customer base. From there, it's a matter of hiring the right talent or partnering with the right crypto-native firms to build the necessary infrastructure and compliance tools for new crypto products.