Last week, Bounce raised an €18m Series B for its short-term storage network that’s seen >750x growth over the past four years. It works like this:

Local businesses sign up to rent out their unused space on Bounce

Travelers use Bounce’s mobile app to find nearby available storage space

Travelers pay $3-5/day to store their luggage safely inside a local businesses

Bounce insures the luggage against theft/loss/damage up to $10k

Bounce’s growth has been nothing short of outstanding: since launching in Seattle in ‘19, their network now extends to 13k+ businesses across 4k+ cities globally. I’ve personally used Bounce >30 times, on four continents, and have had a smooth experience every time—even in countries where I don’t speak the local language.

Thanks for reading Reaching Escape Velocity! Subscribe for free to receive new posts and support my work.

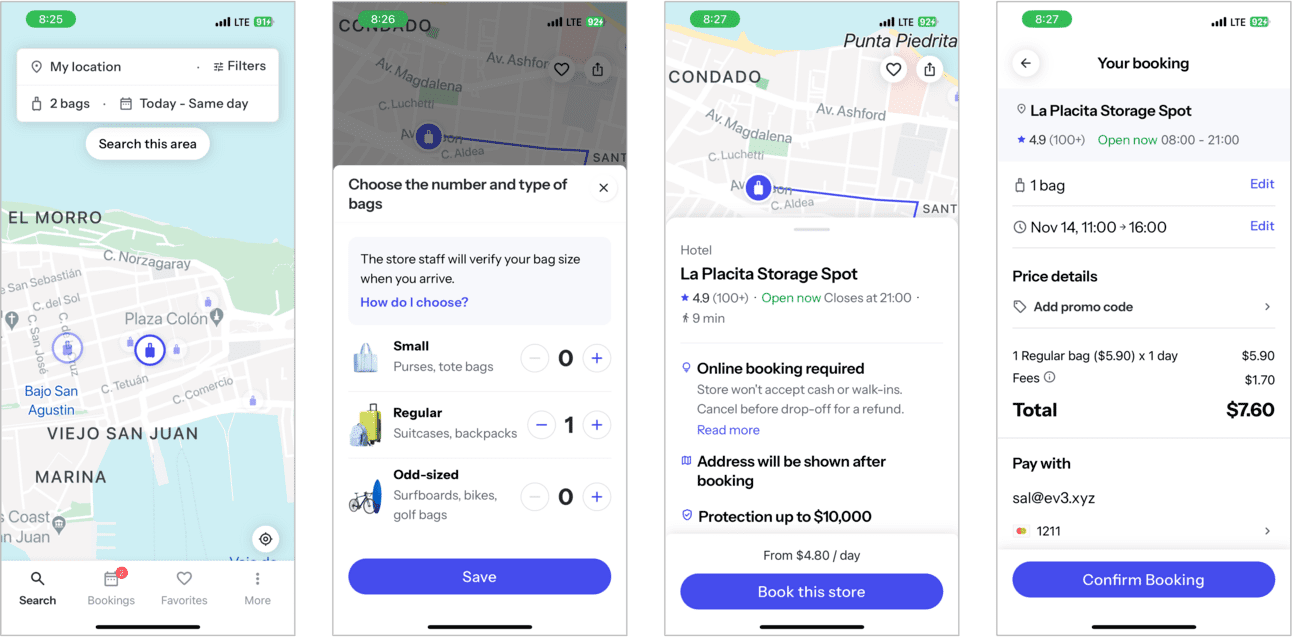

Booking storage space in San Juan via Bounce’s mobile app

The value proposition for Bounce is obvious: for travelers, Bounce provides the comfort and peace of mind of storing your luggage safely nearby for the day. For businesses, it creates a new revenue stream - storage fees - and drives foot traffic from travelers who are likely to spend more in-store. However, the investment case isn’t as clear—as a venture investor in Bounce, three things keep you up at night:

Profitability: Bounce has insurtech-like unit economics, earning $5/day in gross premiums to insure luggage against theft/loss/damage up to $10k. Assuming an average payout of $1k, Bounce can afford to pay claims on only 0.5% of its bookings to make an underwriting profit. The comparable claims frequency for auto/home insurers is an order of magnitude higher at 5-6%.

Addressable market: there are ~10m flight passengers globally each day. Assuming 10% of these travelers have short-term luggage storage needs implies a $1-2B annual gross revenue pool at Bounce’s current pricing—a large market, but not large enough to support a venture-scale outcome.

Tail risks: Bounce’s true liability is not capped at $10k, but by the total legal and reputational damage that its users might cause on its network; for example, criminals can use Bounce to smuggle illicit goods—or worse. A single bad incident can jeapordize their ability to operate in certain markets.

So why have VCs like a16z and General Catalyst invested >$30m into the company? The bull case for Bounce is:

Not your average insurtech. Bounce says they keep 99.99% of bags safe, implying a claims frequency several orders of magnitude lower than the typical insurtech. Since daily storage is such a high-velocity insurance product, Bounce can act quickly to kick businesses of its network if they cause damage/theft and lower their claims frequency asymptotically towards zero over time. At a <1% claims frequency, Bounce can generate very healthy underwriting margins.

Bigger than just luggage. Earlier this year, Bounce launched their second product - package delivery - for users to pick up their packages at local businesses. This expands Bounce into the market for package delivery which is several orders of magnitude bigger than luggage storage. Longer-term, Bounce has ambitions to expand into adjacent markets like peer-to-peer rentals.

Closing the trust deficit. Gig-economy companies like Uber/Airbnb face the same heart attack risk as Bounce. While it hasn’t always been a smooth ride, these businesses have thrived despite some of these risks materializing. Over the past decade, going inside a stranger’s car/home has gone from completely unthinkable to entirely commonplace—it’s not difficult to imagine that storing a stranger’s belongings follows a similar evolution.

Given Bounce’s success with their web2 strategy, why do we think there’s an opportunity for a better, crypto-enabled version of Bounce’s network?

Speed & scale. Bounce grew to 13k+ global locations in its first five years. While this is incredibly impressive, it’s still well under 1% of hotels, restaurants and shops globally. Token incentives are (arguably, after religion) the most powerful coordination known to man. We’ve seen networks like Helium IoT grow multiples bigger than its centralized counterparts in a fraction of the time. Could a decentralized Bounce reach millions of local businesses in a few years?

Risk capital. Based on public information, Bounce appears to write luggage protection guarantees off its own balance sheet, holding the risk of losses directly rather than selling it off to a risk capital provider (i.e., reinsurer). That said, Bounce’s $10k protection offering is not a regulated insurance product, and therefore doesn’t have the same formal capital requirements. Could a decentralized Bounce offload its risk to an onchain pool of risk capital?

Localization. As Bounce expands to new markets, it must localize its product to match the demands of local economies—not just the language of the app, but also the payments, mapping, and customer support infrastructure that makes the entire system run smoothly. Could a decentralized protocol enable local entrepreneurs around the world to build highly-localized versions of Bounce?

Thanks for reading Reaching Escape Velocity! Subscribe for free to receive new posts and support my work.