Cryptocurrencies have always given the impression of high volatility, with tokens easily surging and plummeting, seemingly having little to do with "stability." However, most stablecoins are pegged to the US dollar, and can not only be used as chips to exchange for other tokens, but also serve payment functions. This sector has a total market capitalization of over $200 billion, making it a relatively mature sector in the crypto market.

However, the most common USDT and USDC on the market are both issued by centralized institutions, and the combined market share of the two accounts for nearly 90%. Other projects also want to grab a slice of this big 'BTC'. For example, the Web 2.0 payment giant PayPal is launching its own stablecoin pyUSD in 2023 to stake a claim; recently, Ripple, the parent company of XRP, has also issued RLUSD in an attempt to challenge the stablecoin market.

The above two cases are more about the payment business use of stablecoins, with the backing assets mostly being US dollars or short-term government bonds, while decentralized stablecoins emphasize more on yield, anchoring mechanism, and composability with DeFi.

The market's desire for decentralized stablecoins has never diminished. From DAI to UST, from the types of collateral assets to the anchoring mechanism, the development of decentralized stablecoins has gone through several iterations. Ethena's creation of the USDe stablecoin, which uses spot-futures arbitrage + staking to generate yield, has opened up users' imagination for yield-bearing stablecoins. The market cap of USDe has reached $5.9 billion, ranking third in the entire market. Recently, Ethena has collaborated with BlackRock to launch the USDtb stablecoin, which is backed by real-world assets (RWA) to provide yield, avoiding the risk of negative funding rates and being able to provide stable income in both bull and bear markets, rounding out their product line and making Ethena a focus of market attention.

Given Ethena's successful case, the market has also seen more and more yield-bearing stablecoin related protocols emerging, such as: Usual, which recently announced a partnership with Ethena; Anzen, built in the Base ecosystem; and Resolv, which uses ETH as collateral. What are the anchoring mechanisms of these three protocols? Where do the yields come from? Let's take a look with WOO X Research.

Source: Ethena Labs

USUAL: Strong team background, token design has Ponzi-like attributes

USUAL is an RWA yield-bearing stablecoin, with short-term government bonds as the underlying yield-generating assets. The stablecoin is USD0, and by staking USD0, users can obtain USD0++, with $USUAL as the staking reward. They believe that current stablecoin issuers are too centralized, like traditional banks, and rarely distribute value to users. USUAL will make users co-owners of the project, with 90% of the value generated returned to users.

In terms of the project team, CEO Pierre Person was a member of the French National Assembly and a political advisor to French President Emmanuel Macron. The Asia-Pacific executive Yoko was the fundraising manager for the French presidential election. The project has strong political and business connections in France, and the key to the success of the RWA project is the transfer of physical assets to the chain, where the support and regulation of the government is crucial. It is clear that USUAL has good political and business connections, which is a strong moat for the project.

Regarding the project mechanism itself, the USUAL token economics has Ponzi-like attributes. It is not only a mining token, but also has no fixed issuance. The issuance of USUAL is linked to the TVL of the staked USD0 (USD0++), following an inflationary model. However, the issuance will vary according to the "revenue growth" of the protocol, strictly ensuring that the inflation rate is less than the protocol growth rate.

Whenever new USD0++ bond tokens are minted, a corresponding proportion of $USUAL will be generated and distributed to the participants. The Minting Rate, which determines this conversion ratio, will be highest at the start of the TGE and then gradually decline in an exponential curve, with the aim of rewarding early participants and creating token scarcity to drive up the intrinsic value of the token.

In simple terms, the higher the TVL, the less USUAL will be issued, and the higher the value of a single USUAL token.

The higher the USUAL price -> the more incentive to stake USD0 -> the higher the TVL -> the less USUAL issued -> the higher the USUAL price

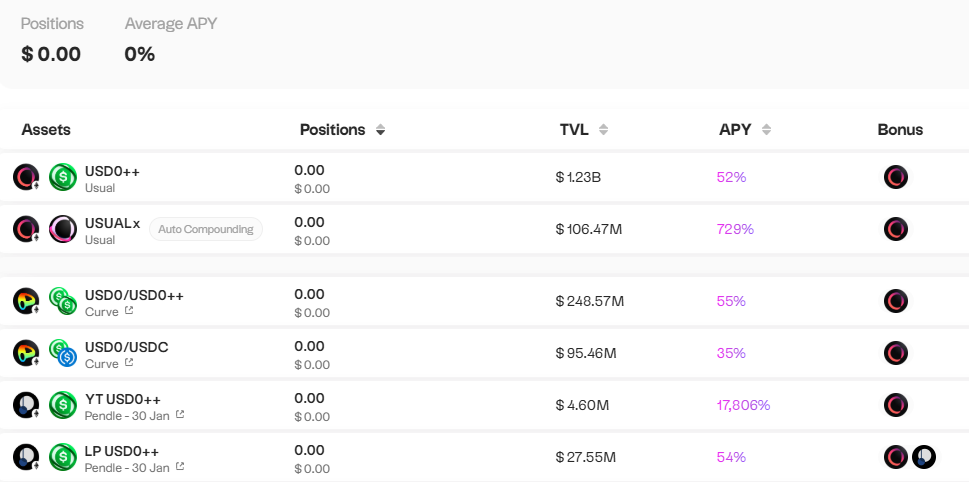

The market cap of USD0 has increased by 66% in the past week, reaching $1.4 billion, surpassing PyUSD. The APY of USD0++ is also as high as 50%.

Recently, Usual has also partnered with Ethena, accepting USDtb as collateral, and will subsequently migrate some of the supporting assets of the USD0 stablecoin to USDtb. In the next few months, Usual will become one of the largest minters and holders of the USD0 stablecoin.

As part of this collaboration, Usual will set up a sUSDe vault for holders of the bond product USD0++, allowing Usual users to receive sUSDe rewards while maintaining their basic exposure to Usual. This will allow Usual users to leverage Ethena's rewards while increasing Ethena's TVL. Finally, Usual will incentivize and enable the swapping of USDtb-USD0 and USDtb-sUSDe, increasing the liquidity between core assets.

They have also recently opened USUAL staking, with the rewards coming from 10% of the total USUAL supply, currently offering an APY of up to 730%.

USUAL:

Current price: $1.04

Market cap rank: 197

Circulating market cap: $488,979,186

TVL: $1,404,764,184

TVL/MC: 2,865

Source: usual.money

Anzen: Securitization of credit assets

Anzen's issued stablecoin is USDz, currently supporting five chains including ETH, ARB, MANTA, BASE, and BLAST. The underlying assets are a portfolio of private credit assets, and by staking USDz, users can obtain sUSDz and earn RWA yields.

The underlying assets are in collaboration with the licensed US broker-dealer Percent, with the risk exposure mainly in the US market, and no single asset exceeding 15% of the portfolio, which is diversified across 6-7 assets. The current APY is around 10%.

The partners are also well-known in traditional finance, including BlackRock, JP Morgan, Goldman Sachs, Moody's Ratings, and UBS.

Source: Anzen

In terms of financing, Anzen has raised $4 million in seed funding from Mechanism Capital, Circle Ventures, Frax, Arca, Infinity Ventures, Cherubic Ventures, Palm Drive Ventures, M31 Capital, and Kraynos Capital. They have also successfully raised $3 million through a public offering using Fjord.

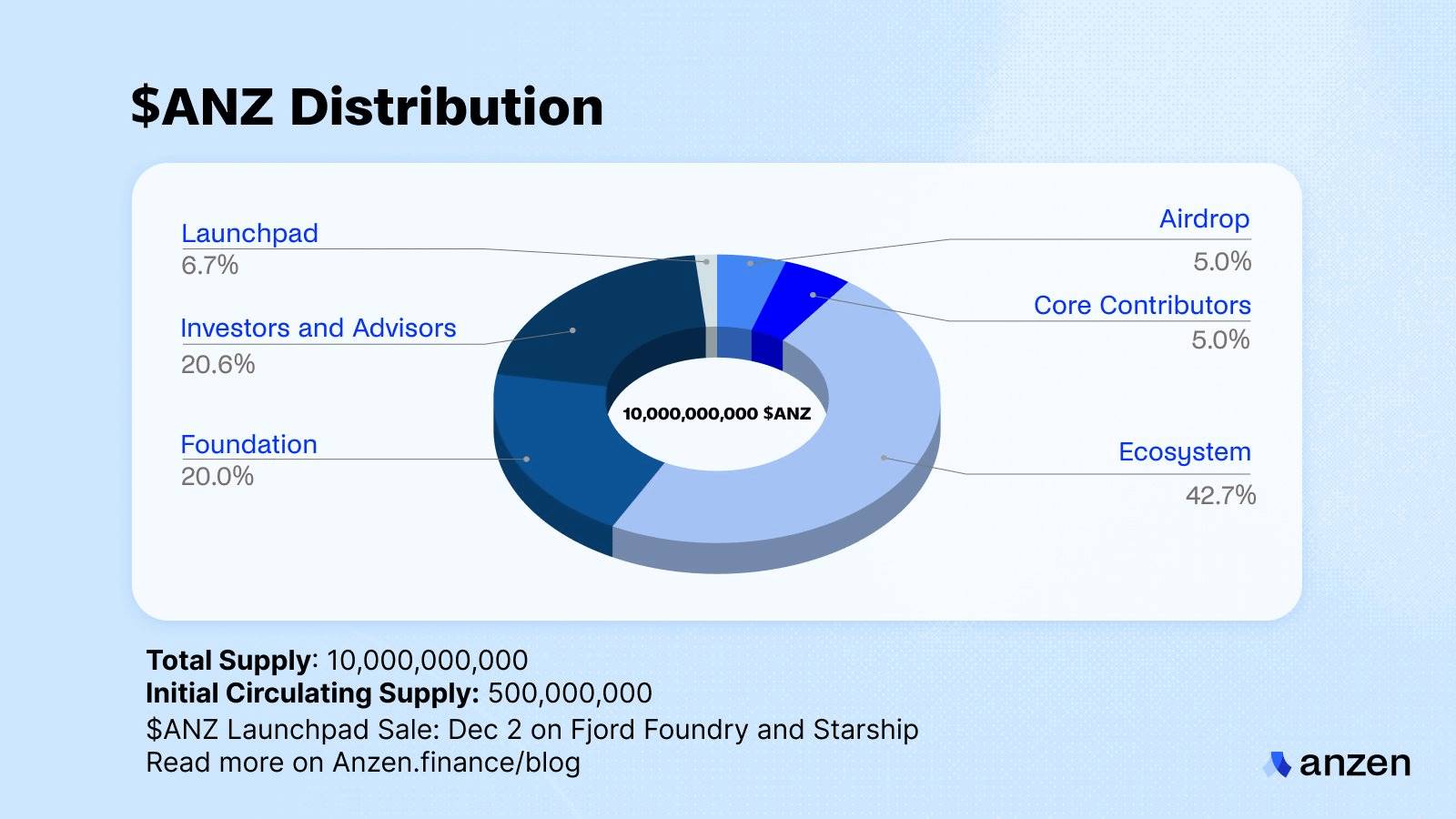

In the ANZ token design, a ve model is used, where ANZ can be locked and staked to obtain veANZ, which entitles the holder to a share of the protocol's revenue.

Source: Anzen

ANZ:

Current price: $0.02548

Market cap rank: 1,277

Circulating market cap: $21,679,860

TVL: $94,720,000

TVL/MC: 4,369

Resolv: Delta-neutral stablecoin protocol

Resolv has two products, USR and RLP:

USR: Overcollateralized stablecoin minted using ETH as collateral, with RPL providing price peg assurance. Users can stake USR to earn stUSR and receive yields.

RLP: The collateral for USR exceeds 100%, with the surplus used to back RLP. RLP is not a stablecoin, and the amount of collateral required to mint or redeem RLP is determined by the latest RLP price.

For the ETH used to generate USR, Resolv employs a delta-neutral strategy, with the majority of the collateral directly deposited and staked on-chain. A portion of the collateral is held by institutions as futures margin.

The on-chain collateral is 100% deposited in Lido, with the short position margin ranging from 20% to 30%, i.e., using 3.3 to 5 times leverage. 47% is on Binance, 21% on Deribit, and 31.3% on Hyperliquid (using Ceffu and Fireblocks as the CEX custodians).

The sources of yield are on-chain staking and funding rates:

Base rewards (70%): to stUSR and RLP holders

Risk premium (30%): to RLP

Assuming the collateral pool generates $20,000 in profit:

The basic reward calculation formula is $20,000*70%=$14,000, and it is distributed proportionally based on the TVL of stUSR and RLP.

The risk premium calculation formula is $20,000*30%=$6,000, which is allocated to RLP.

It can be seen that RLP receives a larger share of the profits, but if the funding rate is negative, the funds will be deducted from the RLP pool, and the risk of RLP is also higher.

Recently, Resolv has launched on the Base network and also launched a points activity, where holding USR or RLP can earn points, laying the groundwork for future token issuance.

Related data:

stUSR: 12.53%

RLP: 21.7%

TVL: 183M

Collateralization ratio: 126%