US wholesale prices rose in January, with food and energy costs rising. According to data on the PPI and CPI for January 2025 released by the Bureau of Labor Statistics last week, the PPI rose 0.4% month-on-month, lower than the revised previous value of 0.5% but higher than the expected 0.3%, and the year-on-year growth rate rose to 3.5%, higher than the market expectation of 3.2%, the largest increase since February 2023. Core PPI rose 0.3% month-on-month and 3.6% year-on-year; CPI rose 3.0% year-on-year, compared to the previous value of 2.9% and the market expectation of 2.9%, while core CPI rose 3.3% year-on-year, compared to the previous value of 3.2% and the market expectation of 3.1%.

Both CPI and PPI rebounded more than expected, with food prices rising faster and energy prices rising more slowly. CPI has now rebounded for four consecutive months, and the risk of a continued rebound in inflation remains high. The additional tariffs imposed by Trump have brought a second round of inflationary risks, so it can be considered that before seeing a easing of inflationary pressures, a slower pace and intensity of rate cuts during the year is a high probability event.

How to interpret the recent CPI and PPI data?

According to the monetary policy report submitted by Powell to Congress, the Fed mainly focuses on the PCE indicator in assessing the inflation outlook, mainly considering: core goods, housing services, and core non-housing services. Powell's speech on February 11 clearly stated the Fed's pace of interest rate adjustments, "If the economy remains strong and inflation does not return to 2% on a sustained basis, we may need to maintain the current policy restrictions for a longer period."

The high inflation data on February 12 has basically laid the foundation for this. From an inflation perspective, rate cuts before the middle of this year do not need to be considered. According to the detailed data, the decline in core goods has widened, inflationary pressures have eased, and the stubborn point of inflation remains in core non-housing services.

Wall Street-related traders have currently pushed the expectation of the next rate cut to December of this year. One point to note is that the Los Angeles wildfire incident that occurred in January may affect market pricing of inflation, as a large part of the current market's concerns about the rebound in inflation are due to the four consecutive months of rebound, and the CPI rise caused by the wildfire is to some extent a systemic risk event. Excluding the wildfire condition, the conclusion of four consecutive months of rebound may not be obtained. From the perspective of the Trump administration's efforts to end the Russia-Ukraine war as soon as possible, if the Russia-Ukraine war ends quickly, it may lead to a decline in construction materials, energy prices, and agricultural product prices, thereby reducing inflation. It is very likely that new data will gradually rescue the pessimistic expectations and increase the expectations for the number and intensity of rate cuts.

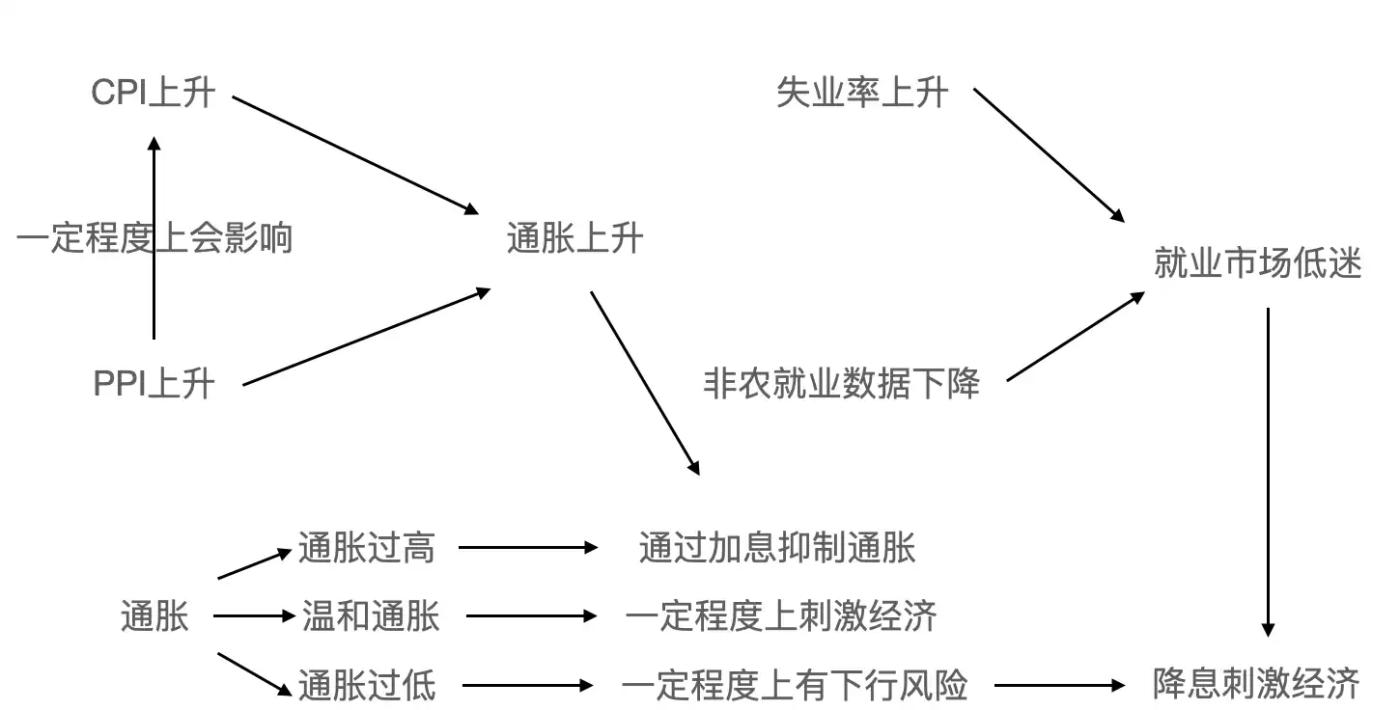

The transmission mechanism of inflation, employment and rate cuts

Powell: "Our focus on whether to cut rates should be on controlling inflation and promoting employment."

The Consumer Price Index (CPI) is a macroeconomic indicator that measures the changes in the price level of a basket of consumer goods and services. When CPI rises continuously, it means consumers need to pay more money to purchase the same amount of goods and services, which is usually seen as a signal of inflation; while the Producer Price Index (PPI) mainly measures the trend and degree of changes in the ex-factory prices of industrial products, and changes in PPI will affect CPI, as changes in producer costs will be gradually transmitted to the consumer end through the industrial chain.

In general, moderate inflation has a certain stimulating effect on the economy, but if inflation is too high, it will affect the stability of the economy and the living standards of residents. When the inflation rate is below the target level and has a downward trend, it may indicate a lack of growth momentum in the economy. In this case, rate cuts may be used to stimulate the economy, raise inflation expectations, and bring inflation back to a reasonable range. But if inflation is at a relatively high level, the central bank usually adopts a tightening monetary policy such as raising interest rates to curb inflation.

Non-farm employment data reflects the changes in the number of employed persons in industries other than agriculture. An increase in this data indicates that enterprises are expanding production or business and need to hire more labor, meaning a prosperous job market and an overall improvement in employment; while the unemployment rate is the ratio of the unemployed population to the labor force.

When the job market performs poorly, such as high unemployment rates and persistently low non-farm employment data, economic growth may be hindered. To stimulate the economy and create more job opportunities, a rate cut monetary policy may be adopted to lower the financing costs of enterprises, encourage them to expand investment and production, and thereby create more job opportunities.

Does BTC have other upward logic?

According to a report on February 13, the US federal budget deficit has expanded to a record $840 billion in the first 4 months of the fiscal year, and on February 14, Dalio also said in public that the US must reduce the budget deficit from 7.5% of GDP to 3%, otherwise it will enter a debt death spiral, and now the US is like a patient on the verge of a heart attack who needs urgent intervention.

Currently, the signs of a US debt crisis have already emerged, with a debt scale of over $36 trillion, and interest payments already accounting for 4% of annual GDP and 22% of total annual fiscal revenue, with nearly a quarter of government revenue needed to pay interest. From this perspective, if the Fed continues to maintain high interest rates, the risk of a debt crisis explosion will become greater, and it is more likely that, ignoring the turbulence of the macroeconomic environment, they will give up short-term policy opportunities and focus on the main contradiction - the debt crisis - to cut interest rates and inject liquidity.

In addition to the narrative of macro rate cuts injecting liquidity into the risk market, another very important narrative for the Crypto market is the inclusion of BTC in strategic reserves, not only at the national level but also at the state fiscal level. This means that if this reserve is approved, state finances will directly purchase BTC, with a purchasing power of around 250,000 BTC, meaning that nearly 1% of BTC's liquidity will be locked up. The resulting mood boost and supply reduction effect may once again form a flywheel upward movement in the cryptocurrency market.