Introduction

The cryptocurrency market is in turmoil. On March 9th, Bitcoin - the bellwether of the crypto world - plummeted 7%, with prices retreating from their highs, triggering widespread panic in the market. According to The Block data, the spot trading volume of centralized exchanges (CEXs) reached $1.77 trillion in February, a new low for the year, down 23.7% from $2.32 trillion in January, indicating a significant contraction in market activity. At the same time, crypto analyst Miles Deutscher pointed out on social media that only 12 of the top 100 cryptocurrencies by market cap have seen positive returns in the past 90 days. For example, BERA surged 579.63%, TRUMP rose 85.61%, while Bitcoin fell 13.47% and LINK plummeted 40%. This dramatic divergence and the decline in trading volume together paint a picture of extreme market panic. Does this mean that a bear market has quietly arrived?

Market Sentiment and Fear Index

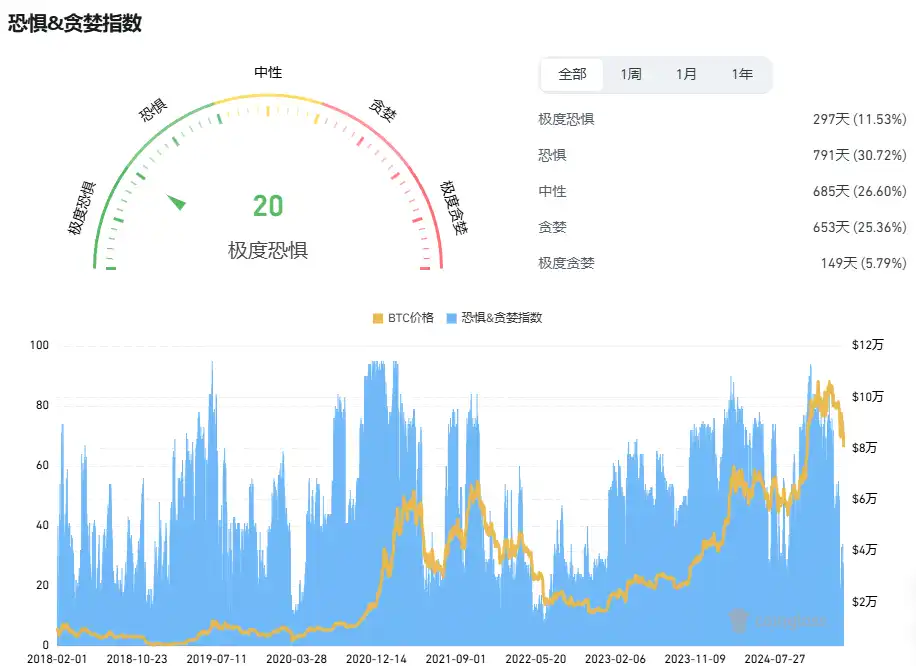

Market sentiment is one of the important indicators for judging trends, and liquidation data, as a direct reflection of market sentiment, provides a key supplement to this analysis. Currently, the Cryptocurrency Fear & Greed Index has fallen to 35, in the "Fear" zone, a significant drop from the "Extreme Greed" level of 70 a month ago. This index comprehensively reflects factors such as volatility (25%), market trading volume (25%), social media sentiment (15%), survey questionnaires (15%), Bitcoin dominance (10%), and trends (10%), clearly showing the rapid deterioration of investor confidence. Glassnode's Net Unrealized Profit/Loss (NUPL) indicator further confirms this trend, dropping from 0.6 (high greed) to 0.2, approaching the level of the early stages of a historical bear market. When this value falls below 0, it typically signals that the market has entered a capitulation phase, and the current value indicates that although the market has not yet completely collapsed, the panic sentiment is approaching a critical point.

CryptoQuant data shows that the demand growth in the Bitcoin spot market is slowing down, and the proportion of short positions in the futures market's Open Interest has risen significantly. As of March 9th, short positions on CME Bitcoin futures accounted for 45% of the total open interest, up 15 percentage points from 30% in early February. This trend of short dominance has exacerbated the market's panic sentiment, and investors' expectations of price declines have increased, with some even discussing the possibility of Bitcoin falling below the $60,000 psychological barrier.

Liquidation data further reveals the market dynamics. In the past 1 hour, the BTC liquidation amount reached $4.707 million, and ETH was $1.306 million, with a total of $11.548 million. Among them, long liquidations were $8.2925 million, and short liquidations were $24.3301 million, with short liquidations far exceeding long liquidations, which may trigger a "short squeeze" leading to a short-term rebound. In the past 24 hours, the total liquidation amount reached $616 million, with long liquidations of $540 million and short liquidations of $76.3075 million. The dominance of long liquidations reflects the persistent pressure of the bear market, which is consistent with the deterioration of NUPL and the rise in short positions. Short-term volatility and long-term risks coexist, and investors need to be vigilant about the complexity, focus on the opportunity of short squeeze, and guard against the downside risk of the bear market.

Technical Analysis: Key Support and Resistance

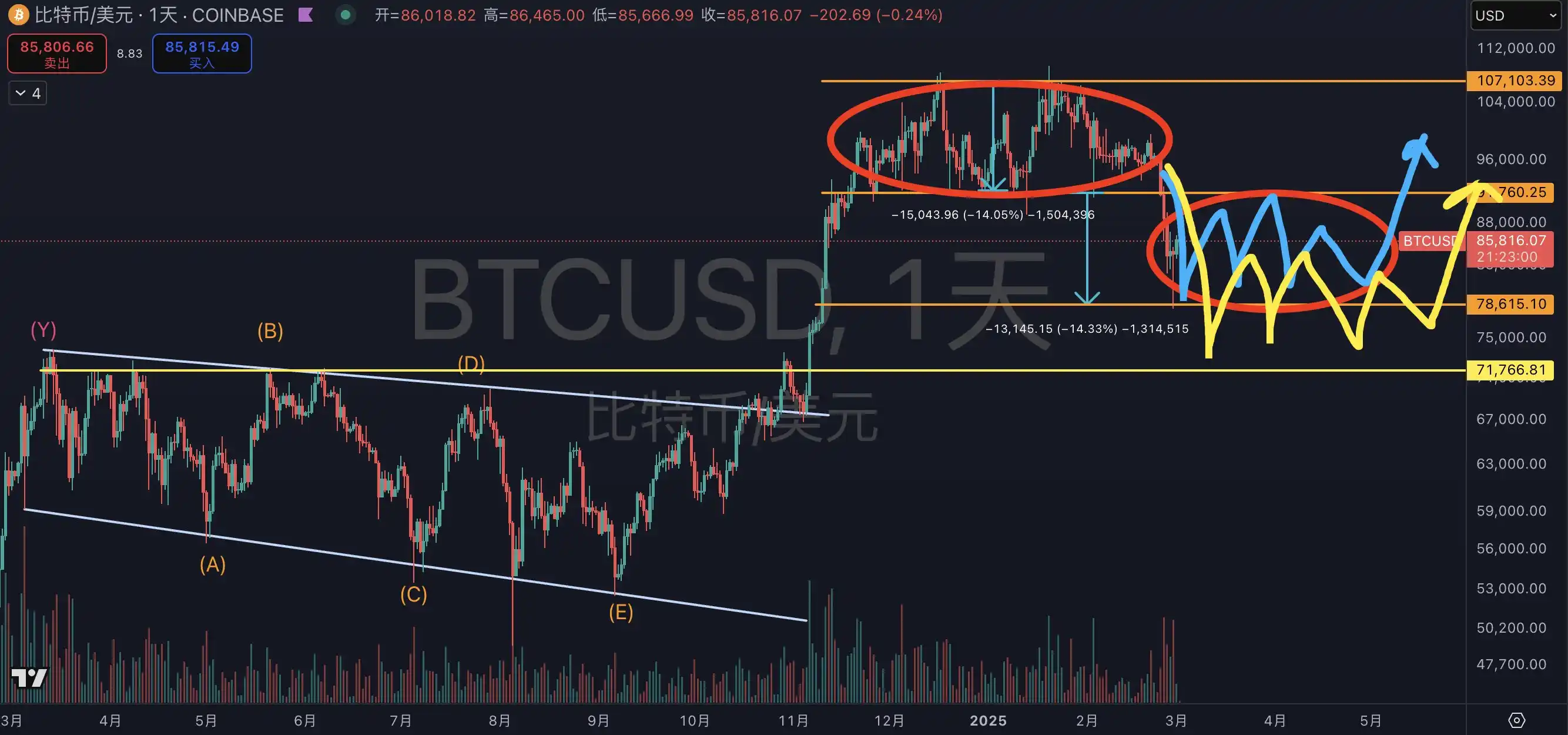

From a technical perspective, the Bitcoin price is at a critical juncture. After the high-volatility range from November 20, 2024 to February 24, 2025, the price has formed a potential Double Top pattern - a typical bearish signal. After the neckline of the Double Top was broken, the price retreated from the high of $82,000 to around $76,000, with the amplitude already close to the expected target (about 10%), but the time dimension has not yet been fully digested.

Analysts generally believe that the market may face two paths:

· Path One: Time for Space If $78,000 becomes the bottom, bulls and bears need to wait patiently for two to three months to confirm the trend. Currently, the range between the 50-day moving average (around $77,500) and the 200-day moving average (around $72,000) has become the focus of short-term tug-of-war. If the price can hold above $78,000, it may form a W-bottom pattern, laying the foundation for a subsequent rebound.

· Path Two: Further Downside If the bears are dominant, the price may fall to the left trading-dense area of $70,000-$72,000. This area is not only the support level of the 200-day moving average, but also an important retracement level after the rebound from the August 2024 low. Trader Eugene Ng Ah Sio said in a Telegram group: "I'm not in a hurry to participate in the current price, $75,000 is the only level I'm interested in." This cautious attitude reflects the uncertainty in the market.

In addition, the Relative Strength Index (RSI) is currently at 42, having fallen from the overbought zone (above 70) to a neutral-to-low level, indicating that the selling pressure has eased somewhat, but it has not yet entered the oversold zone (below 30). Technical analysis suggests that investors should remain cautious, avoid blind chasing or buy the dips, and wait for the trend to become clearer.

Macroeconomic Background: Exhaustion of Positive News and Uncertainty

Macroeconomic factors cannot be ignored in their impact on the cryptocurrency market. First, changes in the global interest rate environment are putting pressure on high-risk assets. The yield on the 10-year US Treasury bond has recently risen to 4.2%, up 40 basis points from 3.8% at the beginning of the year, attracting capital to flow back from the crypto market to traditional safe-haven assets. At the same time, inflation expectations remain high, and the Federal Reserve may delay rate cuts, further diminishing the appeal of Bitcoin as a "digital gold".

On the legislative front, the weakening of positive news has also exacerbated market pressure. For example, the Bitcoin bill in Utah, which was passed by the state Senate on March 7th with 19 votes in favor and 7 against, and is about to be signed into law by the governor. However, its core provision - allowing Utah to hold Bitcoin as a reserve asset - was deleted in the final review. The original provision would have authorized the state treasurer to invest in Bitcoin, with a cap of 5% of its market value (about $25 billion). Now, the bill only retains basic rights such as custody protection and Bitcoin mining/node operation, significantly reducing its impact.

The exhaustion of macroeconomic positives has undermined market confidence, and external uncertainties (such as potential changes in crypto policy under a Trump administration) are also adding variables to the market. Bloomberg analysts predict that if Trump is re-elected, his tax cuts and deregulation policies may provide a short-term boost to the crypto market, but the long-term effects remain to be observed.

ETF Outflows: Waning Institutional Enthusiasm

Institutional demand was an important driver of the Bitcoin price surge in 2024, but the recent outflows from spot ETFs are a cause for concern. According to sosovalue data, since March, the net outflow from US Bitcoin spot ETFs has exceeded $500 million, with the outflow from Grayscale's GBTC being particularly significant. CryptoQuant research chief Julio Moreno pointed out: "The growth in Bitcoin spot demand is contracting, while short positions in the futures market are dominating, directly leading to the price decline."

According to WhaleWire founder Jacob King, "the Bitcoin bear market has arrived. ETF capital outflows have hit record levels, the institutional demand narrative has collapsed, and Bitcoin is heading towards multi-year lows." Although this view is rather extreme, the outflow of ETFs does reflect a decline in institutional enthusiasm. In early 2024, the daily net inflow of ETFs reached as high as $200 million, but has now turned into a net outflow, indicating that institutional investors are reassessing the risk-reward ratio of crypto assets. This change further undermines market confidence.

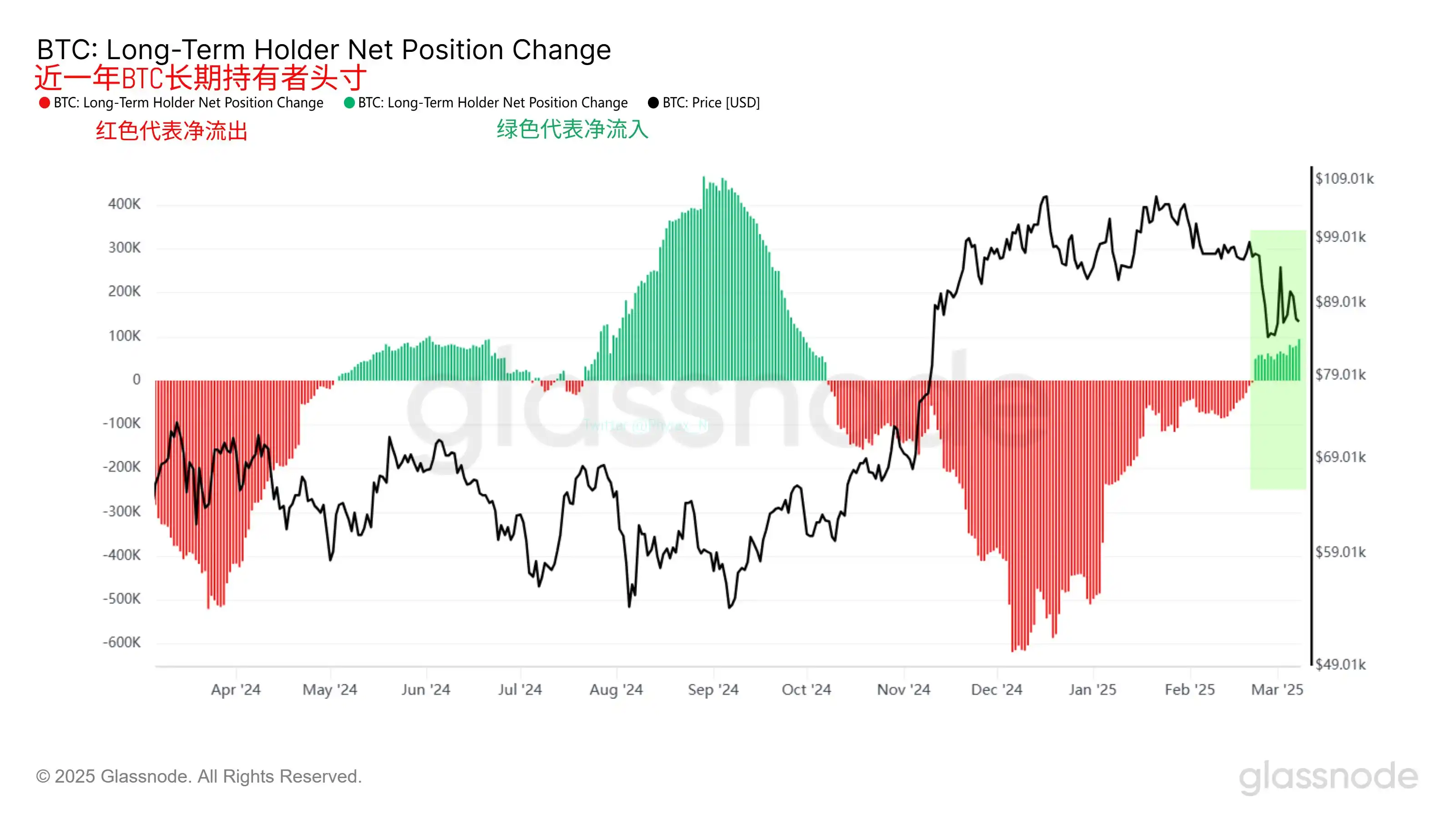

On-chain data: hope and uncertainty coexist

On-chain data provides a glimmer of hope for the market. According to Glassnode's analysis, the behavior of long-term holders (investors holding for more than a year) is undergoing a transformation, shifting from the distribution phase to the accumulation phase. As of March 9, the net position change of long-term holders has turned positive, with a daily average inflow of around 5,000 Bitcoins. Historically, this trend reversal has often been a reliable signal of the market transitioning from the top to the bottom, such as the bottom formation periods in early 2019 and March 2020.

However, the current situation differs from previous cycles. First, the price decline may be slow and sustained, and a relative bottom may only be reached when long-term holder holdings reach a new high (e.g., exceeding 700,000 Bitcoins). Second, the rise of spot ETFs has changed the holder structure. Arkham Intelligence data shows that ETF holders currently control about 4% of the circulating Bitcoin supply (around 840,000 Bitcoins), while the proportion of traditional on-chain long-term holders has declined from 65% in 2023 to 60%. This may weaken the predictive power of traditional on-chain indicators.

Although the shift of long-term holders to a buying mode is encouraging, the reversal is still in its early stages, and the possibility of a reversal has not been ruled out. Predicting the market bottom still requires the verification of additional external signals.

Historical comparison: similarities and differences in bear markets

Looking back at history, the current market has similarities with the bear markets of 2018 and 2022, but also significant differences. In 2018, Bitcoin plunged from $20,000 to $3,200, a decline of over 80%, accompanied by the bursting of the ICO bubble and a contraction in trading volume. In 2022, it fell from $69,000 to $16,000, a decline of about 76%, influenced by the FTX collapse and interest rate hikes. Currently, Bitcoin has declined about 7%-13% from its peak of $82,000, far from the historical bear market levels.

The similarities lie in the decline in trading volume and market segmentation. For example, the trading volume of CEXs declined 70% from its peak in 2018, while the current decline is only 23.7%. The differences are in the degree of institutional participation and the emergence of ETFs, which provide a new buffer mechanism for the market. Therefore, the current panic may be an adjustment period rather than a full-blown bear market, but if the ETF outflow continues to expand, the historical tragedy may repeat itself.

Whether the market has entered a bear market remains inconclusive. Technically, the risk of a correction still exists, as key support levels at $78,000 and $75,000 are being tested. Macroeconomically, positive news is limited, ETF outflows are intensifying, and the institutional narrative is weakening. While on-chain data suggests a recovery in the confidence of long-term holders, the bottom is not yet clear. The current panic may be a harbinger of a deeper adjustment, or it could be the darkness before the dawn.

For investors, caution is paramount. As Miles Deutscher said, "This is a rotational market, and holders are being punished." Rather than chasing short-term volatility, it is better to focus on the intersection of technical support, macroeconomic dynamics, and on-chain signals. Borrowing from Warren Buffett's wisdom - "Be fearful when others are greedy, and greedy when others are fearful" - in the turbulent crypto market, risk management and a long-term perspective are the keys to survival.

Welcome to join the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram discussion group: https://t.me/BlockBeats_App

Twitter official account: https://twitter.com/BlockBeatsAsia