Author: Decentralised.Co Translated by: Block unicorn

This article is inspired by a series of conversations with Ganesh Swami, covering the seasonality of revenue, the evolution of business models, and whether token buybacks are the best use of protocol capital. This is a supplement to my previous article on the stagnation of cryptocurrencies.

Private capital markets like venture capital oscillate between excess liquidity and scarcity. When these assets become liquid and external capital flows in, market frenzy drives up prices. Think of newly launched IPOs or token offerings. The newfound liquidity allows investors to take on more risk, which in turn spawns a new generation of companies. Last year, $22.1 billion was spent on purchasing Bitcoin. But last year's Bitcoin price surge did not translate into a rebound in the long tail of Altcoins.

We are witnessing an era where capital allocators are liquidity-constrained, attention is scattered across thousands of assets, while founders who have toiled for years on tokens struggle to find meaning. When the launch of Meme assets can generate more financial OpenSea's revenue has seasonality. In the NFT summer, the market cycle lasted two quarters, while social finance speculation lasted only two months. If the scale of revenue is large enough and consistent with product intent, speculative revenue from products is meaningful. Many Meme trading platforms have joined the $100 million+ revenue club. The scale of this number is what most founders could hope to achieve at best through tokens or acquisitions. But for most founders, this level of success is rare. They are not building consumer apps; they are focused on infrastructure, where revenue dynamics are different.

Between 2018 and 2021, VCs heavily funded developer tools, hoping developers would attract large user bases. But by 2024, two major shifts have occurred in the ecosystem. First, smart contracts have enabled limitless scaling with limited human intervention. Uniswap or OpenSea do not need to scale their teams proportionally to transaction volume. Second, advancements in LLM and AI have reduced the investment demand for crypto developer tools. As a category, it is now in a moment of reckoning.

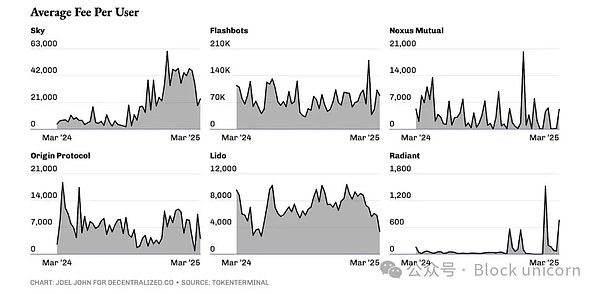

In Web2, the API-based subscription model worked because of the massive online user base. However, Web3 is a smaller niche market, with few applications scaling to millions of users. Our advantage is the high revenue metrics per user. Crypto users tend to spend more money more frequently, as blockchains enable this - they make money flow possible. Therefore, over the next 18 months, most businesses will have to redesign their business models to directly extract revenue from users in the form of transaction fees.

This is not a new concept. Stripe initially charged per API call, Shopify charged a fixed subscription fee, and both later shifted to revenue-share models. For infrastructure providers, this transition is quite direct in Web3. They will compete on API pricing to eat into the market - potentially even offering products for free up to a certain transaction volume, then negotiating revenue share. This is the ideal hypothetical scenario.

What would this look like in practice? One example is Polymarket. Currently, the UMA protocol's tokens are used for dispute resolution, with the tokens tied to the disputes. The more markets, the higher the probability of disputes occurring. This drives demand for UMA tokens. In the trading model, the required margin can be a small fraction of the total bet, say 0.10%. For example, a $1 billion bet on the US presidential election outcome would generate $1 million in revenue for UMA. In the hypothetical case, UMA could use this revenue to buy back and burn their tokens. This approach has its benefits and challenges, which we will see soon.

Another participant doing this is MetaMask. The transaction volume processed through its embedded exchange feature is around $36 billion. The exchange revenue alone exceeds $300 million. A similar model applies to staking providers like Luganode, where fees are based on the amount of assets staked.

But in a market where API call costs are increasingly declining, why would developers choose one infrastructure provider over another? If revenue sharing is required, why choose one oracle over another? The answer lies in network effects. Data providers that support multiple blockchains, provide unparalleled data granularity, and can index new chains faster will become the preferred choice for new products. The same logic applies to transaction categories like intent or Gas-less exchanges. The more chains supported, the lower the profit margins, the faster the speed, the more likely to attract new products, as this marginal efficiency helps retain users.

Full Burn

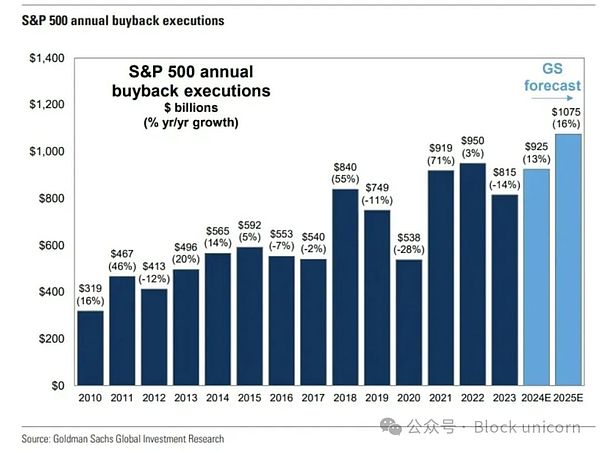

The shift of tying token value to protocol revenue is not new. In recent weeks, several teams have announced mechanisms to buy back or burn tokens proportional to revenue. Notable among them are SkyEcosystem, Ronin Network, Jito SOL, Kaito AI, and Gearbox Protocol. Token buybacks are similar to stock buybacks in the US equity market - essentially a way to return value to shareholders (or in this case, token holders) without violating securities laws. In 2024, the US market alone had around $790 billion in stock buybacks, up from $170 billion in 2000. Whether these trends will continue remains to be seen, but we are seeing a clear bifurcation in the market - one side with cash flows and willing to invest in their own value, and the other without either.

For most early-stage protocols or dApps, using revenue to buy back their own tokens may not be the best use of capital. One way to execute such operations is to allocate sufficient capital to offset the dilution from new token issuances. This is how the Kaito founders recently explained their token buyback approach. Kaito is a centralized company that uses tokens to incentivize its user base. The company generates centralized cash flows from its enterprise clients. They use a portion of this cash flow to execute buybacks through market makers. The quantity purchased is double the amount of new tokens issued, effectively making the network deflationary.

Ronin, on the other hand, has taken a different approach. The blockchain adjusts fees based on the number of transactions per block. During peak usage periods, a portion of the network fees goes into Ronin's treasury. This is a way to control the asset supply without necessarily buying back the tokens themselves. In both cases, the founders have designed mechanisms to tie value to network economic activity.

In future articles, we will delve deeper into how these operations impact the price and on-chain behavior of the tokens involved. But for now, it is evident that - as valuations are suppressed and the amount of venture capital flowing into cryptocurrencies decreases, more teams will have to compete for the marginal dollars flowing into our ecosystem. Since blockchains are essentially money rails, most teams will shift to revenue-share models based on transaction volume. When this happens, if they are tokenized, they will have an incentive to issue buyback and burn models. The teams that do this well will become the winners in the liquidity markets.

Of course, one day, all this talk about prices, yields, and revenues will become irrelevant. We will go back to spending money on dog pictures and buying monkey NFTs. But looking at the current state of the market, most survival-concerned founders have already started discussing revenue and burning.