Author: Insights4vc. Translator: Shan Ouba, Jinse Finance

Public cryptocurrency investment vehicles (PCVs) are publicly traded companies that raise funds primarily for the purpose of buying cryptocurrencies and holding them on their balance sheets. In effect, they act as quasi-ETFs : They allow stock market investors to invest in digital assets — initially Bitcoin, and more recently Ethereum, Solana, Ripple, and others — without adopting the formal structure of an exchange-traded fund (ETF).

This report reviews the development of the PCV field, from MicroStrategy's first transaction to the current broader group of issuers; sorts out the participants, financing timelines and operating models; compares indicators such as net asset value (NAV) premium, leverage level and trading liquidity; and outlines the relevant regulatory, accounting and risk frameworks. In addition, the report provides forward-looking scenario analysis and reference for institutional investors.

Core Observation PCV has raised tens of billions of dollars (mainly through zero-coupon convertible bonds and PIPE private placements) to purchase crypto assets. MicroStrategy (now renamed "Strategy") alone holds more than 580,000 BTC , with a market value of approximately $60 billion, funded by multiple rounds of debt and equity financing.

Since 2024, more PCVs are no longer limited to Bitcoin and have begun to diversify their layout. Some companies have combined crypto asset allocation with income-oriented activities (such as staking, lending, and arbitrage).

In bull markets, PCVs often trade at premiums to their underlying NAVs (trading at a premium) due to their convenience as a regulated alternative to holding cash; whereas in risk-off phases of the market, these premiums can turn into discounts, especially when companies are highly leveraged or have a concentrated governance structure.

There are differences in regulatory treatment . In the United States, PCVs follow general securities rules and there is no dedicated system; while countries such as Canada take a more relaxed regulatory stance. There are also differences in crypto-asset accounting standards in different markets.

PCVs face unique risks, including shareholder dilution, leverage downside risk, liquidity constraints when exiting large positions, and operational challenges in custody and auditing. Nevertheless, PCVs may still exist as a form of "permanent capital" that connects equity markets and crypto assets, providing opportunities for arbitrage or asset allocation diversification.

In general, PCV is located at the intersection of corporate finance and digital asset markets , providing a "quasi-ETF" path for investors who want to participate in crypto assets through regulated channels. To evaluate any PCV, it is necessary to carefully analyze its structure, asset portfolio and regulatory background. This report provides detailed data and analytical support for this.

Market Map and Classification Method Public Cryptocurrency Investment Vehicles (PCVs) carve out a unique market space at the intersection of corporate finance and crypto investing. They are publicly traded entities with a core objective of holding crypto assets, typically financed through equity or debt. Unlike the approximately 78 publicly traded companies around the world that hold Bitcoin as a “secondary treasury asset,” PCVs explicitly set crypto asset accumulation as a primary strategy. The following is an overview of the PCV universe and its classification framework.

By asset classification: PCVs are first categorized based on their primary crypto asset . The largest and oldest group is BTC-centric , represented by Michael Saylor’s Strategy (formerly MicroStrategy), which explicitly targets Bitcoin as an asset under management. The ETH-centric group focuses on Ether and related staking yield opportunities, leveraging Ethereum’s unique yield potential. An emerging SOL-centric category has emerged, betting on the growth of Solana as a Layer-1 blockchain asset. In addition, hybrid or multi-asset asset managers hold diversified crypto portfolios, and we finally identify a group of in-the-works and rumored PCVs that have announced but not yet completed their crypto asset acquisitions.

Segmentation by strategy and structure:

PCVs are also categorized by their strategies for creating value for investors. Some act as passive holders , mirroring the performance of the underlying crypto assets (e.g., Strategy’s Bitcoin holdings actually operate as a Bitcoin ETF). Others employ active strategies , such as ETH-centric vehicles staking assets for yield or participating in distressed crypto debt purchases and structured products. Capital structures vary widely, from leveraged vehicles that issue large amounts of debt to purchase crypto (MicroStrategy’s model) to newer, unleveraged entities formed solely through equity capital (e.g., SPAC- or PIPE-funded companies). PCVs also vary in their operating roles, from existing businesses that add crypto to their balance sheets (like GameStop) to pure investment vehicles established simply to hold crypto.

Geographic and Regulatory Classification:

Most high-profile PCVs are listed in the U.S., but the model is global. Canada pioneered the creation of crypto fund management entities, such as Ether Capital Corp’s early public holdings of ETH. Regulatory jurisdiction dictates their structure: U.S. PCVs are registered as standard corporations, following GAAP (typically accounting for intangible assets, with a recent shift to fair value). Other markets use structures similar to investment trusts , or comply with regional securities laws (e.g., Japan and the European Union require strict disclosures for crypto funds).

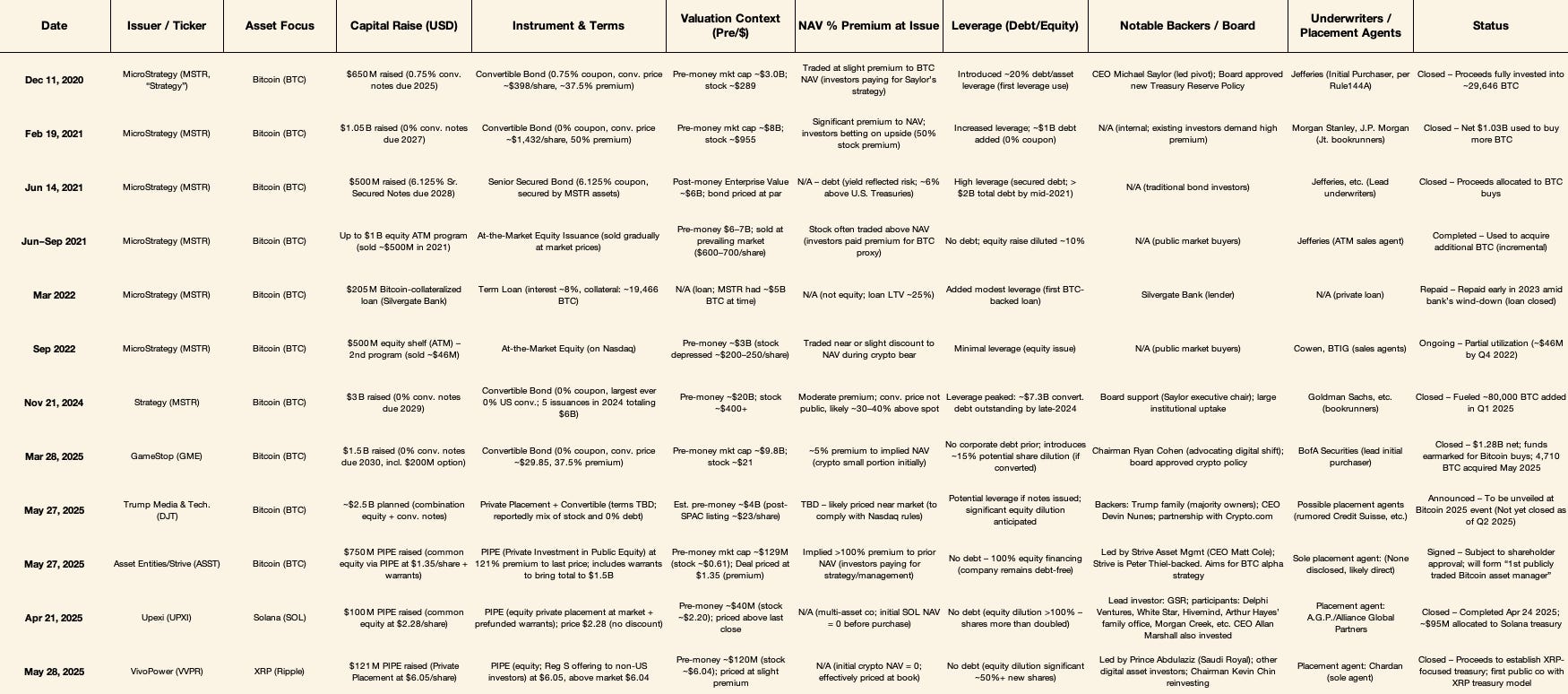

Transaction timeline and financing structure The timeline of PCV transactions shows a rapid evolution from isolated actions to structured strategies. Below is an interactive table detailing major PCV financings with analysis. Transactions range from MicroStrategy’s groundbreaking 2020 bond issuance to numerous 2025 cryptocurrency-focused transactions.

Key details provided include deal size, instrument type, valuation context, asset value premium, leverage, key backers and status, and are primarily sourced from official filings (e.g., SEC 8-Ks) to ensure accuracy.

Featured PCV Offers (2020–2025): We recommend opening this table on your desktop

The idea of explicitly raising public capital to purchase cryptocurrencies began with MicroStrategy’s bold move in 2020. In August 2020, CEO Michael Saylor announced Bitcoin as the company’s primary asset , initially funded in cash. The turning point was in December 2020 , when MicroStrategy issued $650 million of 0.75% convertible bonds due in 2025 , immediately investing $634.9 million in approximately 29,600 Bitcoins (BTC) , becoming a leveraged Bitcoin holding company overnight.

Then, the market went wild: In February 2021 , MicroStrategy raised $1.05 billion through 0% convertible bonds due in 2027 , increasing the amount from $600 million to $1.05 billion due to strong demand, and issued $500 million of senior secured notes in June 2021. Investors eagerly accepted the 50% conversion premium and zero interest rate , reflecting the strong demand for indirect exposure to Bitcoin. Throughout 2021, MicroStrategy also sold shares through market plans, profiting from the premium of shares relative to Bitcoin holdings. By early 2022, MicroStrategy further utilized Bitcoin through a $205 million Silvergate bank loan , repaid in 2023 after Silvergate's collapse.

After the market downturn, MicroStrategy accelerated again in 2024 with a series of new 0% convertible bonds, including a $3 billion convertible bond issued in November 2024 , the largest of its kind in a decade. The five convertible bonds in 2024 raised a total of more than $6 billion, raising an additional ~80,000 BTC in the first quarter of 2025 alone . By May 2025, MicroStrategy held approximately 568,000 to 580,000 BTC , leveraging more than $7 billion in debt and significant equity dilution (the number of shares has nearly doubled since 2020). This unprecedented approach— repeatedly issuing equity and debt to purchase Bitcoin —set a template that has been widely adopted by other companies.

The “Saylor 2.0” strategy extends to companies like GameStop , which raised $1.5 billion in 0% convertible bonds in April 2025 to purchase 4,710 bitcoins (about $513 million) , marking its cryptocurrency debut. Trump Media & Technology Group announced plans to raise $2.5 to $3 billion in equity and convertible bonds explicitly for the purchase of bitcoin, a plan directly inspired by MicroStrategy.

Beyond Bitcoin, in April 2025 , Upexi raised $100 million in a PIPE at market price to increase its stake in Solana (SOL) , backed by a prominent cryptocurrency venture capital firm, demonstrating public market confidence in Altcoin centric strategies. Similarly, VivoPower raised $121 million in a private placement at market price , pioneering an XRP-centric funding strategy backed by Saudi royal family investors. Both transactions significantly diluted existing shareholders, but were designed to leverage the popularity of cryptocurrencies to justify valuations.

Another notable case is Asset Entities’ $750 million PIPE with Strive Asset Management at a 121% premium , which aims to create the first publicly traded Bitcoin asset management company with an alpha-generating strategy. This debt-free, equity-centric strategy emphasizes prudent structuring and is different from the purely passive cryptocurrency fund management model.

Overall, PCVs evolve from simple convertible bond issuances (2020-2021) to a diverse range of financing approaches by 2025, including PIPE, equity ATM, and hybrid models. Commonalities include: investor interest in cryptocurrency investments that do not offer discounts or high interest rates, significant shareholder dilution balanced by valuation premiums, diverse leverage approaches, and a hybrid narrative that aligns cryptocurrency investments with broader corporate strategies. These evolving models reflect the maturation and diversification of public market cryptocurrency investment strategies and lay the foundation for subsequent detailed cohort analysis.

1. Bitcoin-centric PCV

The "Saylor 2.0" group includes some public companies that are explicitly focused on Bitcoin accumulation and are inspired by the MicroStrategy model. These companies position themselves as Bitcoin proxies - mainly by raising funds to buy and hold BTC as a strategic reserve. Notable players include Strategy (formerly MicroStrategy), GameStop, and Trump Media's proposed Bitcoin reserve plan.

Strategy (MicroStrategy) - Prototype: Strategy holds the world's largest corporate Bitcoin vault, approximately 568,000 to 580,000 Bitcoins (BTC), valued at over $60 billion by 2025. Its financing channels include $7.3 billion in convertible bonds and equity issuances, effectively building a structure similar to a leveraged Bitcoin ETF. Due to the scarcity of regulated Bitcoin investment vehicles, Strategy's stock price is highly correlated with BTC and trades at a premium during bull markets. This premium also reflects the leverage brought by debt financing, which has greater upside (and downside risk) than directly holding BTC. With Bitcoin reaching approximately $107,000 in early 2025, Strategy's early bet (average purchase price of approximately $70,000) has been validated. Key success factors include Saylor's leadership, first-mover advantage, and savvy capital market execution. Current risks include asset management complexity, regulatory scrutiny, and debt refinancing challenges.

GameStop – Meme Stock vs Bitcoin Balance Sheet: GameStop’s 2025 BTC funding plan marks its foray into the cryptocurrency space as part of its turnaround strategy. By issuing $1.5 billion in 0% convertible bonds, GameStop acquired approximately $512 million in BTC without depleting its cash reserves. Initially, investors reacted positively, believing that the BTC purchases strengthened GameStop’s digital narrative. However, GameStop took a more conservative stance than Strategy, with BTC accounting for approximately 10% of its total assets, indicating its cautious and gradual consolidation. GameStop’s retail investor base and limited cryptocurrency experience differ from Strategy, but the move legitimizes the consumer-focused company’s strategy of holding Bitcoin.

Trump Media & Technology Group (TMTG) – Ambitious Bitcoin Reserve: TMTG plans to raise $2.5-3 billion specifically to build a massive Bitcoin reserve that could rival the size of the Strategic Fund. TMTG’s combination of equity and convertible debt positions Bitcoin as a strategic protection against currency debasement, consistent with a politically charged narrative and broader cryptocurrency integration plans. However, the ambitious fundraising raised concerns about equity dilution and sparked initial skepticism in the market, highlighting the risks associated with large-scale, politically relevant cryptocurrency reserves.

Asset Entities/Strive - Active BTC Strategy: The merger of Strive and Asset Entities introduces a more active Bitcoin strategy that involves trading and opportunistic investing in addition to simple BTC accumulation. This hybrid strategy - "Bitcoin+" - combines long-term BTC belief with active alpha generation. It may be challenging to execute this strategy transparently in the open market, but if successful, it may redefine the potential of public cryptocurrency investment vehicles.

Metrics and Market Perception: The premium to NAV of Bitcoin-centric investment vehicles varies, with Strategy historically trading at up to 20% above NAV. GameStop's valuation far exceeds its Bitcoin holdings, indicating that the market still views it as primarily a retail investor. Debt usage also varies widely, from Strategy's high leverage to GameStop's zero-interest convertible bonds, highlighting the different risk profiles of this group. The adoption of fair value accounting from 2025 will increase transparency and may further align stock performance with crypto asset valuations.

Outlook: BTC-centric PCVs are likely to remain important due to their unique appeal - leveraged BTC exposure, corporate governance, and regulatory compliance. Unless these investment vehicles can evolve by offering Bitcoin dividends, divesting non-core businesses, or exploring innovative fund management strategies, potential competition from spot ETFs could erode their premiums and appeal.

ETH-centric PCV accumulates ETH as primary reserves, taking advantage of ETH's appreciation and yields generated through staking. Major pioneers include Ether Capital and BTCS, which provide efficient crypto asset exposure that is different from Bitcoin. Staking income introduces cash flow, which enhances financial status compared to non-yielding BTC holdings, although these tools face unique custody, regulatory, and technical risks.

Emerging SOL-centric PCVs such as Upexi have accumulated large SOL reserves in an effort to capture institutional demand and foster growth in the Solana ecosystem. Upexi’s transformation demonstrates a new way to integrate crypto assets into traditional corporate structures, tests public market appetite for Altcoin centric investment vehicles, and could pave the way for similar initiatives.

Companies such as VivoPower are exploring hybrid treasuries that focus on alternative digital assets such as XRP. Diversified treasuries that combine mainstream and Altcoin holdings can reduce volatility and strategically align with broader cryptocurrency trends. While these multi-asset experiments bring management complexity and regulatory considerations, they may also bring broader market upside.

Future PCVs may emerge through SPACs, mid-sized technology companies, and geographically diversified markets. The approval of a Bitcoin ETF could dampen or stimulate further corporate adoption of cryptocurrencies, thus affecting the development of PCVs. Potential investment vehicles could further diversify into Metaverse tokens, NFTs, or other themed cryptocurrency baskets, which would be affected by macroeconomic and regulatory developments.

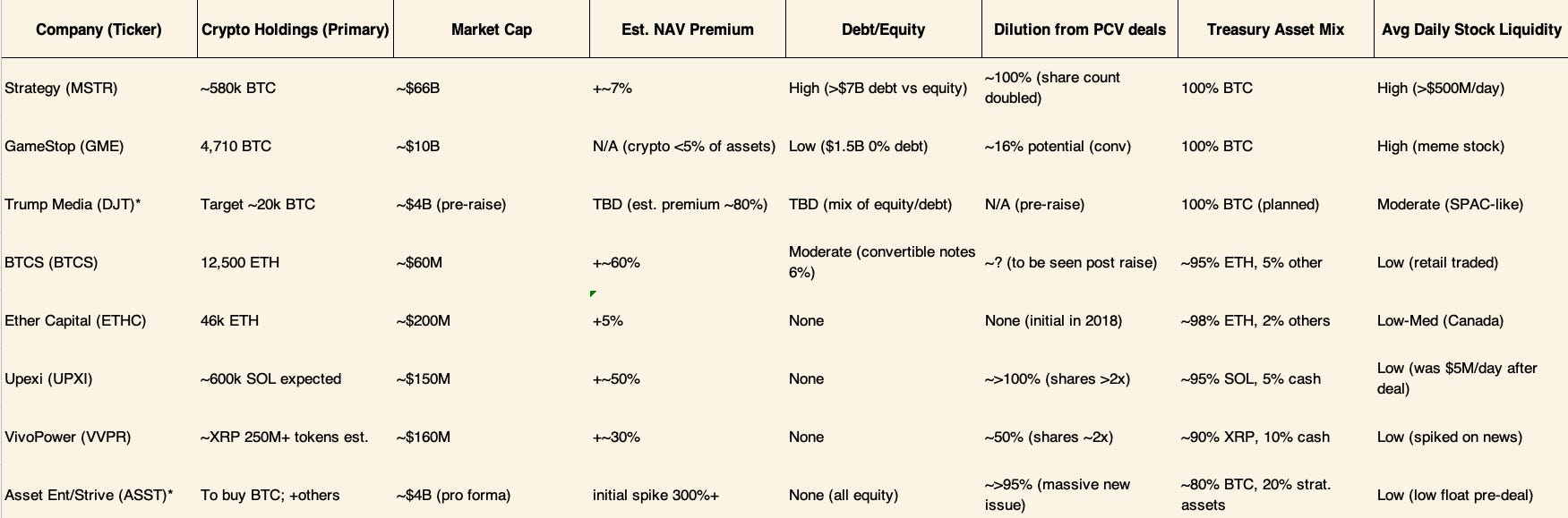

In this section, we summarize the current PCV comparative metrics, focusing on NAV premium/discount , leverage, dilution impact, liquidity considerations, and fund composition. These metrics illustrate how the market assesses the valuation of each investment vehicle relative to the asset, revealing structural advantages or risks. The bar chart shows the NAV premium/discount of the major PCVs and highlights the relative valuations.

NAV Premium/Discount: Measures the ratio of stock market capitalization to the value of the crypto asset (plus net assets). Positive percentages indicate a premium (reflecting perceived management value or strategic optionality), while negative percentages indicate a discount due to arbitrage constraints or management concerns. As of mid-2025:

The MSTR strategy (MSTR) trades at a premium of approximately 5-10% to its Bitcoin NAV, reflecting the market's confidence in Saylor's management and leverage potential. Historically, premiums have reached over 40% during peak market sentiment, but have fallen as BTC holdings have increased. A modest premium makes equity issuance accretive, thereby incentivizing equity issuance.

GameStop (GME) currently holds a large premium because its crypto exposure ($513 million in BTC) is lower than its overall business. GameStop has a market cap of $10 billion, and its crypto-specific premium (~1,900%) reflects retail investors and earnings expectations rather than pure crypto investment. Adding BTC holdings could significantly reduce the premium, providing a clearer valuation.

Trump Media (DJT) valuation remains speculative before the deal. The company has a market cap of approximately $4-5 billion, minimal liquid assets, and pricing includes an estimated $2.5 billion in BTC purchases (estimated purchase of 20,000 BTC at $110,000 each). The ~80% premium suggests it has both meme status and political appeal.

BTCS (market cap ~$50-60m, ETH ~$32m) continues to trade at a premium of ~50-80% due to staking returns and growth prospects through additional ETH acquisitions.

Ether Capital (ETHC) typically trades around NAV, exhibiting a slight (<10%) premium in bull markets, similar to a closed-end fund.

After the Solana transaction, Upexi (UPXI) traded at a 50% premium to its initial trading price before the raised funds were deployed ($95 million invested in SOL). This reflects investors' expectations of the SOL acquisition and optimism about the Solana market. The stability of the premium depends largely on SOL's performance.

VivoPower (VVPR) is trading at a premium of about 32% to XRP, thanks to investor interest in XRP and support from prominent backers. Liquidity constraints on XRP trading, especially in the U.S., have pushed up the premium, but eventual arbitrage could narrow it.

Asset Entities/Strive (ASST) has experienced extreme short-term volatility (~1,000% initial premium). Given the significant dilution that is imminent ($750M raised at $1.35/share), the premium is temporary and reflects speculative misperceptions. Ultimately, the combined stock price should be closely tied to NAV.

Leverage: Strategy is moderately leveraged (~12% debt to assets), historically high but somewhat mitigated by the appreciation of Bitcoin. GameStop’s debt ($1.5 billion vs. $10 billion equity) remains low risk due to zero interest rates. Trump Media expects moderate leverage (~40% debt in capital structure). Newer alternative investment companies (ASST, Upexi, VivoPower) are funded with equity, reflecting their limited access to high-quality debt markets.

Dilution (%): PCV financings come with significant dilution of ownership. The strategy doubles the number of shares (dilution of ~100%); GameStop's potential dilution is ~16%. Trump Media's dilution could be substantial, depending on the structure. ASST faces extreme dilution (less than 5% existing ownership after the transaction), but this is offset somewhat by the premium valuation. Upexi (~72% dilution) and VivoPower (~50% dilution) similarly trade ownership for asset growth, which is acceptable in the case of premium execution.

Liquidity — Days to Exit: Analyzes liquidity by comparing cryptocurrency vault size to stock and cryptocurrency trading volume:

Stock liquidity varies widely; major PCVs (MSTR, GME) trade strongly, and micro-caps exhibit less predictable liquidity due to float dynamics.

Public cryptocurrency vehicles (PCVs) operate in a complex environment, with regulatory and accounting environments that vary across jurisdictions. This overview explores key considerations in the United States, Canada, Japan, the European Union, and other major markets, as well as evolving digital asset accounting standards that directly impact financial reporting and investor perceptions.

United States: US PCVs are regulated like regular public companies and subject to SEC disclosure rules, but special care is needed to avoid classification under the Investment Company Act of 1940. Generally, companies holding commodities such as Bitcoin can avoid classification issues, while Altcoin centric PCVs face complications due to potential securitization (e.g. XRP, SOL). Mandatory disclosure of cryptocurrency risks (volatility, custody, regulatory uncertainty), often requiring timely filing of Form 8-K for significant transactions. New FASB rules requiring fair value accounting for crypto assets, effective in 2025, will significantly increase transparency and reduce prior impairment asymmetries. US corporate tax applies only to realized gains, allowing for strategic tax loss harvesting given the current ambiguity around wash sale rules.

Canada: Canada is friendly to cryptocurrencies, allowing easy listings on the Canadian Stock Exchange (CSE), NEO or TSX Venture. International Financial Reporting Standards (IFRS) have historically considered cryptocurrencies as intangible assets, but potential changes are yet to be determined. Canadian regulators familiar with cryptocurrency ETFs are positive about holding cryptocurrencies directly. Companies are generally classified as operating entities rather than investment entities, provide internal management, and do not have redemption mechanisms. Canadian regulatory guidelines strongly encourage qualified custody arrangements.

Japan: In Japan, corporate holdings of cryptocurrencies are permitted, with conservative accounting standards (lower of cost and market, with limited markups). The regulatory framework classifies crypto assets similarly to commodities under the Payment Services Act to avoid securities disputes. Companies that primarily hold cryptocurrencies as inventory assets typically avoid registering as exchanges or financial instruments. However, unclear rules on the taxation of unrealized gains by companies create uncertainty that could hinder large-scale PCV activity until the situation becomes fully clear.

EU: EU regulations under MiCA focus on crypto service providers rather than corporate financial holdings, and typical PCVs are not affected unless tokens are actively issued. International Financial Reporting Standards (IFRS) are currently still based on intangible assets and are awaiting an update. The corporate environment varies from country to country, with Switzerland and the UK being particularly supportive. Corporate governance frameworks across the EU occasionally require shareholder approval for significant crypto asset allocations. Emerging interest could lead to more companies listing in jurisdictions such as Frankfurt or Euronext.

Emerging Markets: El Salvador is actively involved in the Bitcoin market at the government level, and rumors of some unstable economies (such as Africa and Latin America) have also highlighted the phenomenon of local companies using cryptocurrencies for hedging. The UAE's supportive stance suggests that private securities companies (PCVs) may be listed in Dubai. Hong Kong is exploring a cryptocurrency-friendly framework to provide a possible listing path for private securities companies serving regional investors.

Audit and Custody: Custody transparency and audit standards (such as the US Public Company Accounting Oversight Board (PCAOB) guidance) have evolved significantly, and the Big Four accounting firms are now well-versed in cryptocurrency audits. While simple assets like Bitcoin rarely raise issues, complex DeFi or alternative asset strategies can significantly increase the complexity, cost, and disclosure requirements of audits.

Securities Regulation and Market Manipulation: Regulators closely monitor personal investable securities (PCVs) to ensure that they do not operate like unregulated ETFs. Currently, comprehensive information disclosure is sufficient to meet regulators' requirements, but the sharp increase in passive cryptocurrency holdings may prompt regulators to introduce stricter investor protection measures. Companies must strictly ensure full compliance to avoid losses or hacker attacks.

Jurisdiction Summary:

Overall, PCVs follow existing regulatory frameworks that primarily treat them as operational or quasi-investment entities. Recent accounting reforms have significantly increased transparency, which is expected to increase corporate adoption of crypto assets.

Investing in or operating a public cryptocurrency investment vehicle (PCV) carries a number of risks, ranging from macroeconomic factors to cryptocurrency-specific pitfalls. This section outlines the following key risk factors: macro market risk, liquidity and volatility risk, custody and operational security risk, accounting and audit risk, and counterparty/credit risk (particularly relevant to yield-generating strategies).

Macro & Market Risks: PCV’s inherent concentration of crypto exposure makes it vulnerable to crypto market cycles and macroeconomic downturns. In a bear market, the value of the underlying asset declines and stocks typically trade at a discount, amplifying losses. During the 2022 crypto downturn, MicroStrategy’s stock price fell more than Bitcoin due to concerns about compounding leverage. There is a risk that a prolonged crypto winter could lead to significantly discounted valuations, making equity financing or debt repayment more complicated. Rising interest rates increase the opportunity cost of non-yielding crypto assets, making PCV less attractive unless it can provide a yield (which ETH staking tools have certain advantages). Regulatory crackdowns pose a serious risk; forced asset liquidations during price downturns could severely damage value.

Liquidity and Volatility: Cryptocurrency assets are extremely volatile, with Bitcoin’s daily volatility typically as high as 5-10%, which exacerbates the volatility of PCV shares. High volatility may discourage institutional investors from investing. Liquidity risks include:

Custody and security risks: Risks unique to cryptocurrencies include irreversible asset loss due to compromised private keys. Professional custodians can mitigate single point failure risks (the custodian is hacked or bankrupt). Multi-signature wallets increase operational complexity and risk (e.g., key loss, internal collusion). Auditors need to provide strong proof of control over cryptocurrencies; failure to prove control (e.g., key loss or long-term stake lockup) may delay audits and undermine investor confidence. Technical risks such as blockchain forks or network outages (e.g., Solana outage) can hinder asset management, highlighting the need for strong internal expertise.

Accounting and Valuation Risks: Fair value accounting can lead to earnings volatility. PCV’s profits and losses are subject to large GAAP fluctuations due to cryptocurrency price fluctuations, which complicates traditional valuation metrics and can mislead investors. Auditors closely scrutinize cryptocurrency’s internal controls; negative audit opinions or significant deficiencies could severely damage stock prices and investor confidence.

Counterparty Risk and DeFi Risk: Participating in cryptocurrency lending or DeFi business carries significant counterparty risk and credit risk. Default events (e.g. Celsius, 3AC) have historically caused severe PCV losses or bankruptcies. Smart contract vulnerabilities and limited insurance in DeFi further exacerbate the risk. Excessive pursuit of yield can turn simple fund management strategies into complex risk exposure.

Dilution and governance risks: Repeated issuance of additional equity at discounted valuations can severely dilute shareholders, erode company value, and lead to a downward valuation spiral. Governance risks include internal decision-making that is unfavorable to minority shareholders, dual-class share structures that lead to excessive control, and potential related-party conflicts or fraud, especially in smaller, less scrutinized PCV companies.

External disruption risk: Policy intervention (e.g., central bank digital currency) or competitive market changes (e.g., ETF approval) could negatively impact demand for PCV shares or premiums, indirectly harming valuations and financing capabilities.

Contagion and correlation: Crypto assets are often highly correlated during economic downturns, limiting the benefits of diversification. Problems in other crypto areas (e.g., exchange crashes, stablecoin crises) may indirectly affect PCV through broader market declines, thereby amplifying systemic risks.

Bankruptcy/Liquidation: Debt-ridden PCVs face the risk of bankruptcy during periods of declining asset values, triggering forced liquidation. Loss of assets due to critical mismanagement (such as in the QuadrigaCX case) could lead to bankruptcy, litigation, or significant losses to investors.

Mitigation: Risks can be mitigated through reputable custodians, hedging exposures, maintaining insurance, diversified banking relationships, and a robust governance structure including independent directors and strict financial oversight.

In summary, PCV combines typical characteristics of asset managers, operating companies, and crypto-specific risks. Investors must recognize that the leveraged cryptocurrency risk they take on is compounded with additional corporate risk, which provides both significant upside potential and multiple avenues for severe losses. Effective risk management remains critical, as past failures highlight the real consequences of being unprepared.

The future of public crypto vehicles (PCVs) could present a variety of scenarios, from bull market highs to bear markets, and mild baseline scenarios in between. Below we explore the implications for investors, outline actionable signals, and offer advice on managing risk exposure.

Baseline scenario (steady growth): The cryptocurrency market experiences moderate and sustained growth; Bitcoin price fluctuates between $100,000 and $150,000, and Ethereum price rises proportionally with typical volatility. PCV gradually integrates into financial markets.

Existing PCV: Steady growth of assets, gradual capital increase if NAV premium allows. This strategy increases BTC holdings; ETH-centered PCV increases holdings and stakes ETH, thereby increasing NAV.

Valuation: NAV premiums have stabilized (5-15% for large PCVs (e.g. Strategy) and 10-20% for small PCVs), reflecting company value and liquidity. Arbitrage activity has narrowed the initial high premiums.

New Entrants: There are a limited number of new PCVs, mostly mid-sized companies or niche investment vehicles (companies focused on Polygon or Web3 games). Mass adoption of the S&P 500 remains unlikely.

Investor attitude: Institutional investor confidence has slightly improved; hedge funds are actively involved (long PCV/short cryptocurrency strategies). Cautious institutional investors prefer diversified or income-oriented PCV.

Regulation/Accounting: Fair value accounting makes earnings clearer; SEC guidelines stabilize and no longer impose any stringent new restrictions. Bitcoin ETF approval is uncertain, but may be in 2026, as its unique product (leverage, asset diversification) will complement PCV.

Risk: Controllable with moderate adjustments. Leveraged PCV actively manages or reduces debt.

Investor Takeaways: PCV will become a reliable proxy for cryptocurrencies with alpha potential. Investors should track NAV premiums, rotate accordingly, and actively participate in governance (shareholder activism, buybacks).

Bull Case (Crypto Super Cycle): Crypto markets surge dramatically; BTC price exceeds $250,000 following widespread adoption or technological breakthrough.

Bear Case (Crypto Recession/Shock): A major crash or prolonged downturn due to regulatory issues, technological flaws, or market exhaustion.

General operational points:

All in all, PCV represents a complex but rewarding component of cryptocurrency investing, suitable for strategic holdings or arbitrage opportunities. Astute investors must skillfully combine cryptocurrency market analysis, stock valuations, and regulatory awareness to effectively navigate this dynamic market.