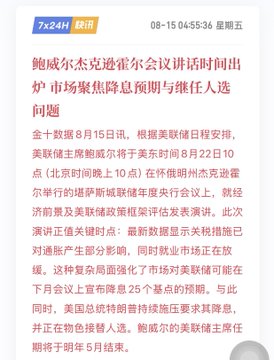

Last week, we discussed that the market is likely to fluctuate in the short term, with the key point being the global central bank annual conference this Friday. Many may not be clear about the theme of this central bank conference, "Labor Market in Transition: Population, Productivity, and Macroeconomic Policy," which can be said to be very apt for the current U.S. economic situation. The debate about immigration, domestic population, and productivity brought by artificial intelligence is almost raised in conjunction with all topics, whether it's tariffs, deficit bills, unemployment rate ineffectiveness, capital expenditure, terminal interest rates, or earnings reports from tech stocks to consumer stocks - all cannot avoid this critical issue. This is also the key focus of the current market: The medium to long-term upward momentum is clear, driven by fiscal expansion, industrial policy, large-scale AI acceleration, and the process of massive purchasing of core crypto assets. However, short-term momentum is beginning to lack, especially after last Thursday's PPI data significantly exceeded expectations, which was discussed as not being good for the market. Then last Friday's inflation expectations gradually rose. Previously, everyone thought it would necessarily move towards easing due to debt pressure, but because of data and potential inflation upside risks, this certain easing expectation has been hit, which is the underlying logic of the current oscillation and adjustment. As mentioned in the previous tweet, this will affect the inflow speed and rhythm of buy-side funds. This is also what was mentioned in the previous fiscal expansion 2.0 tweet: the medium to long-term logic is solid, but there are short-term small-scale risk impact sources. Returning to the central bank conference, now Powell's attitude can be reasonably seen as either dovish or hawkish: The dovish expectation is that the labor market is indeed slowing down, inflation is moderately rising without massive surge, and debt pressure is indeed significant. The hawkish expectation is that tariffs have not yet translated into high commodity inflation, but service industry stickiness has indeed risen again, which also implicitly involves the Fed's independence struggle. The core is still on Powell's balance between his dual mandate of employment and inflation, and which side he leans towards is crucial. Personally, I think his best attitude would be neutral, not explicitly stating a September rate cut, but instead stating that he will wait for August employment and inflation data, which is largely neutral for a market that has fully priced in a September rate cut. Powell also mentioned his new interest rate framework in the July monetary policy meeting: the current interest rate level is at least "moderately restrictive". If inflation upside risk dominates, such a policy positioning is reasonable. But if employment downside risk and inflation upside risk tend to balance, the policy rate should be lowered and move towards neutrality. So Powell's neutral stance can be considered as alleviating short-term market concerns, but we still need to see how August data will verify whether the service sector strength in July CPI and PPI is one-time or trend-based.

This article is machine translated

Show original

qinbafrank

@qinbafrank

08-15

晚上公布8月通胀预期都是起来,消费者信心指数略低于预期,又回到几个月前软数据差的状态,这个会影响到市场情绪,如昨天说短期还是会震荡。后面的关键时点应该就是下周全球央行年会鲍威尔的讲话,他怎么看待7月份服务超预期,商品通胀不及预期的状态,以及能否释放未来的利率走势的预期。 x.com/qinbafrank/sta…

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content