September 9, 2024

Sol Strategies, then still operating under its original name, Cypherpunk Holdings, had not yet undergone the rebranding process.

It still trades on the Canadian Securities Exchange, a market typically reserved for small and micro-cap companies. Just a few months ago, the company hired Leah Wald, the former CEO of Valkyrie, as its new CEO. At that time, Cypherpunk was still relatively unknown and received little investor attention.

Meanwhile, Upexi focused on driving consumer product sales for DTC brands, targeting Amazon niches like pet care and energy solutions, and vying for traffic amid fierce competition. DeFi Development Corp (DFDV, then still using its old name, Janover) was preparing to launch a platform connecting real estate syndicators with investors. Sharps Technology, on the other hand, produced specialized medical syringes—an extremely niche medical technology target that struggled to attract investors.

These companies, at the time, were small – both in size and ambition. Collectively, they held less than $50 million worth of Solana (SOL).

Fast forward a year and things have changed dramatically.

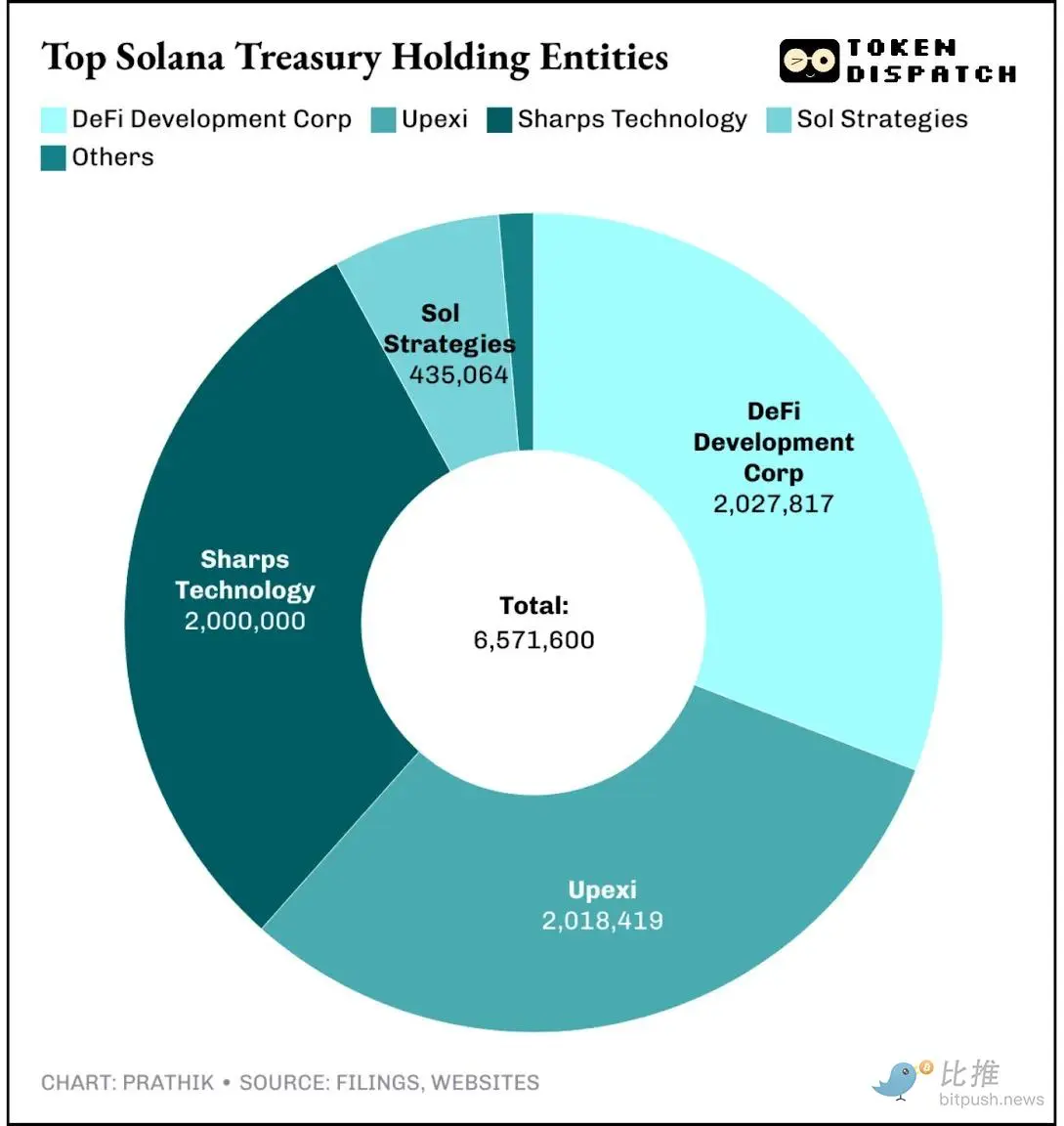

Today, they proudly stand on Nasdaq – the world’s second-largest stock exchange – holding over 6 million SOL tokens and a valuation of $1.5 billion. The value of Solana’s holdings alone has skyrocketed 30-fold in a year.

From Margin to Center: Nasdaq's Recognition

This Tuesday, the opening bell of the Nasdaq in New York not only marked the official listing of Sol Strategies, but also resonated on-chain: users can send Solana transactions through stke.community to participate in the "virtual bell ringing", permanently recording this historic moment.

For Sol Strategies, which previously traded on the Canadian Securities Exchange (symbol HODL) and the OTCQB market (symbol CYFRF), this was a true graduation gift. Admission to the Nasdaq Global Select Market is no small feat. The market, renowned for its stringent standards and typically admitting only blue-chip companies, secured Sol Strategies the legitimacy most crypto companies crave.

This is why Sol Strategies’ listing is significant, even though institutions seeking exposure to Solana on Wall Street can already invest in Upexi and DeFi Development Corp.

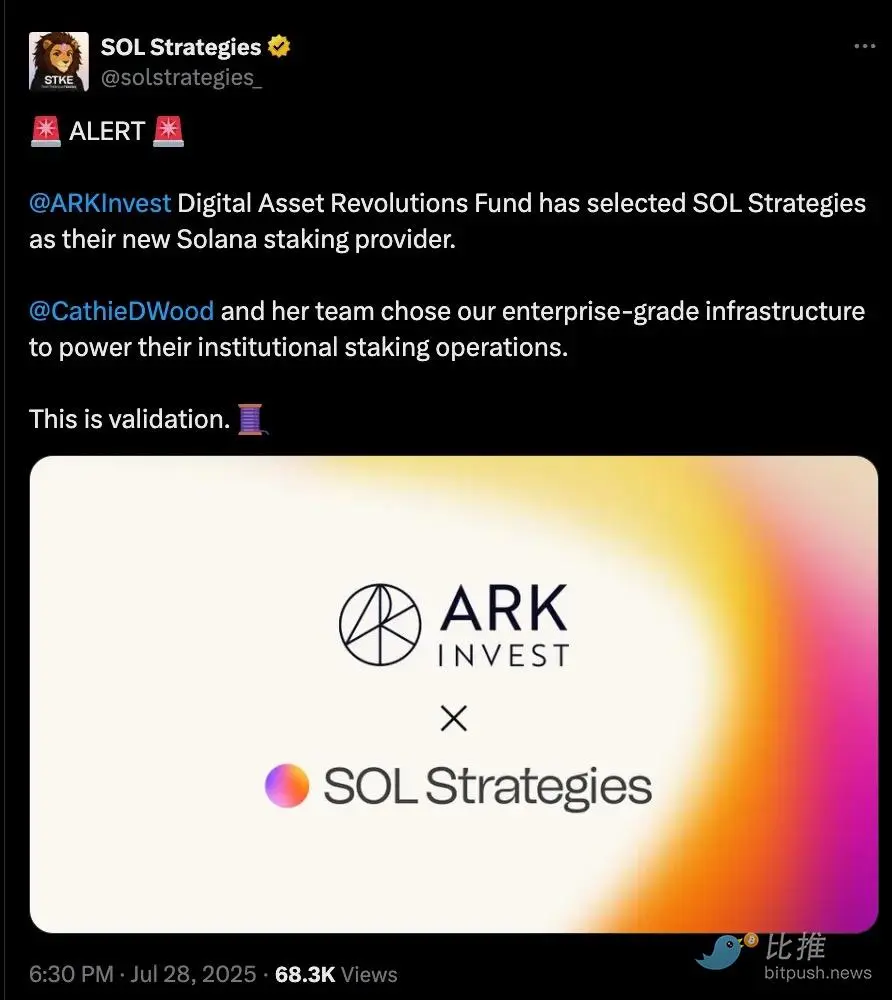

Unlike Upexi and DeFi Dev Corp, both of which were already public companies before transitioning to the Solana treasury, each holding over 2 million SOL, Sol Strategies took the slow route. It established a validator operation, secured institutional mandates like ARK’s 3.6 million SOL, passed a SOC 2 audit, and strategically positioned itself on the Nasdaq Global Select Market, the exchange’s top-tier market.

While other firms simply hold SOL, Sol Strategies is actively running the infrastructure that supports it, turning these holdings into viable businesses.

Financial report in-depth analysis: Pledge is income, cash flow has turned positive

I dug into Sol Strategies' balance sheet to understand the story behind the numbers.

In the quarter ending June 30th, Sol Strategies reported revenue of $2.53 million Canadian dollars (approximately $1.83 million USD). While this figure on its own may seem modest, the real story lies in the fine print. This revenue came entirely from staking approximately 400,000 SOL and operating validators securing the Solana network—not from selling traditional products. Upexi is weighed down by a non-crypto re-commerce business, while DFDV relies heavily on ongoing fundraising to fuel growth and still derives 40% of its revenue from its non-crypto real estate business.

Sol Strategies has opened up a new revenue stream from its Solana Treasury business by offering validators as a service. This approach provides recurring income without the burden of growing debt or traditional overhead costs.

Sol Strategies delegates SOL on behalf of its institutional clients, including 3.6 million SOL delegated in July from Cathie Wood's ARK Invest. The commissions from these delegations generate a steady stream of revenue. Call it income, call it fees, but in accounting terms, it's revenue—something many crypto treasuries can't show.

A typical Solana validator charges a commission of approximately 5%–7% on staking rewards. With the base staking yield hovering around 7%, these delegated tokens generate approximately 0.35%–0.5% of their notional value per year for the validator.

At 3.6 million SOL (over $850 million at current prices), this translates to over $3 million in annualized fee income, even without any price appreciation or gains in Sol Strategies’ own treasury. This is effectively an additional revenue stream, more than half of the staking income from its own 400,000 SOL holdings, generated entirely by external capital.

Sol Strategies’ bottom line for the third quarter, however, showed a net loss of $8.2 million Canadian dollars (about $5.9 million USD). But if you strip out one-time expenses such as amortization of acquired validator IP, share-based compensation, and listing costs, the operation itself is cash flow positive.

Core Advantages

What truly sets Sol Strategies apart from its competitors is how it views Solana.

For the firm, the product isn't just the Solana token; it's the Solana ecosystem. This unique perspective is both innovative and strategic, setting Sol Strategies apart from its peers in the space.

As more delegators join, the network becomes more secure, and the reputation of nodes improves, further attracting more delegations – creating a flywheel effect. Every user who delegates SOL to Sol Strategies becomes both a customer and a co-creator of its revenue, transforming community participation into a measurable driver of shareholder value.

This model gives it an advantage over competitors who hold far more SOL than it currently does. Currently, at least seven listed companies control a total of 6.5 million SOL (worth $1.56 billion), accounting for 1.2% of the total SOL supply.

In the race for the Solana treasury, each company is striving to become the first choice for proxy investors to gain exposure to Solana.

Each company is slightly different: Upexi is acquiring SOL at a discount, DFDV is betting on global expansion, while Sol Strategies is betting on a diversified war chest.

The game is the same: accumulate SOL, pledge it, and sell a wrapper to Wall Street.

Bitcoin’s path to Wall Street adoption was paved by companies like MicroStrategy, which transitioned from a software business to a leveraged BTC treasury, and through a highly successful spot ETF. Ethereum has followed a similar path, with companies like BitMine Immersion, Joe Lubin’s SharpLink Technologies, and most recently, a spot ETF.

For Solana, I foresee adoption occurring primarily through operating companies within the network. These businesses not only hold assets but also run validators, earning fees and staking rewards, and publishing quarterly returns. This model is closer to active managers than to ETFs.

It’s this combination of net asset value (NAV) appreciation and real cash flow that may well convince investors to invest via this route. If Sol Strategies can make this all work, it could become the BlackRock of the Solana space.

Risk Warning: Challenges in the New Stage

The future hints at a closer relationship between Wall Street and Solana.

Sol Strategies is exploring the possibility of tokenizing its equity and issuing it on-chain. Imagine STKE shares not only existing on Nasdaq but also becoming a Solana token, exchangeable in DeFi pools and instantly settled with USDC. This "listed equity + on-chain trading" bridge is something ETFs cannot bridge. While still speculative, this trend is blurring the lines between public equity and crypto assets.

However, it was not easy. Listing on Nasdaq introduced new challenges, including greater responsibilities for Sol Strategies.

- Validator operational errors or governance mistakes may trigger immediate feedback from investors

- Betting on the Solana ecosystem (not just the token) means higher risk and reward

- The SOL network itself still faces the risk of interruption and competition from new public chains.

- If the stock price is too far below NAV, arbitrageurs may sell regardless of fundamentals.

Despite this, Sol Strategies' IPO represents Solana's best chance to secure a front-row seat on Wall Street. Can it package its on-chain treasury into a packaged investment product and integrate it into Nasdaq? Sol Strategies has already taken on the responsibility of doing so.