The spotlight in Washington is blazing on a year-end drama: who will succeed Jerome Powell as head of the Federal Reserve?

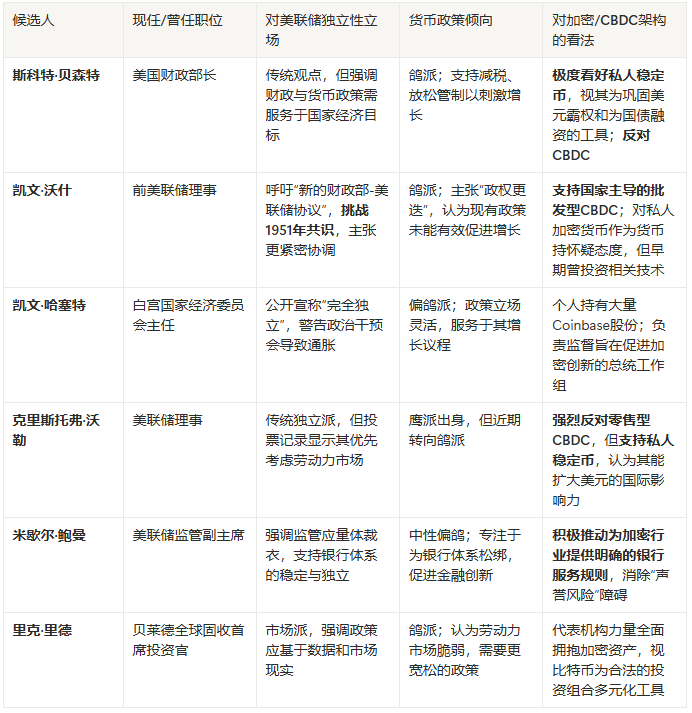

The shortlist is laid out: Waller, Bowman, Hassett, Warsh, and Reid. The media is meticulously analyzing their every word and phrase about interest rates and inflation. The entire Wall Street is holding its breath, speculating how this personnel change will shake the markets.

But what if the real core of this competition has nothing to do with the word "inflation"?

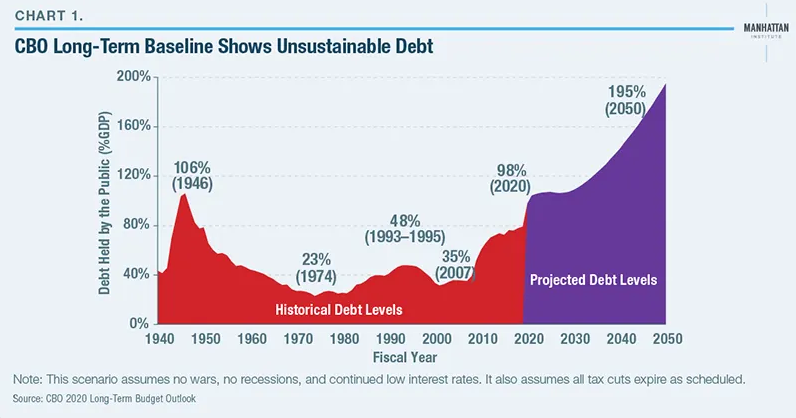

Behind the curtain of this political drama lurks a far larger and more urgent specter: the United States' staggering $35 trillion national debt. According to grim projections from the Congressional Budget Office (CBO), by 2035, the federal debt-to-GDP ratio will climb to 118%. This is the real "elephant in the room," a beast that no traditional monetary policy can tame.

When traditional tools fail, an "unconventional" solution emerges.

According to Bitcoinist, a revelation made by Trump at a private party has revealed the crux of the matter. He stated that cryptocurrency has a "bright future" and hinted at a startling possibility: using cryptocurrency to solve the $35 trillion debt problem.

“I would write on a little piece of paper: $35 trillion in cryptocurrency, we have no debt, that’s what I like to do.”

This wasn’t an impromptu joke, nor was it the first time Trump had publicly stated many times before that Bitcoin could be used to “save America.”

Putting all of this together, the true portrait of the next Federal Reserve Chairman becomes extremely clear.

This selection process isn't about finding an "inflation fighter." It's about finding a "chief financing officer" willing to break convention, even at the expense of central bank independence. Trump's true mission: Whoever can fully integrate the digital asset ecosystem (especially stablecoins) into the national fiscal apparatus and find new, substantial buyers for the massive U.S. national debt will be Powell's successor.

A long-planned "regime change"

To understand this selection process, one must look beyond the surface of "personnel change" and grasp its core of "system change." Trump's years-long attacks on Powell—the chairman he personally nominated but quickly turned against—had already foreshadowed all of this.

From calling Powell "not smart at all" and "a fool" to publicly pressuring him to cut interest rates to crisis levels, Trump's anger has never been directed solely at Powell personally, but at the cornerstone of central bank independence he represents, established since the Treasury-Federal Reserve Agreement in 1951. What Trump needs is a "compliant" central bank, an instrument willing to use monetary policy to serve his "pro-growth, high-debt" fiscal agenda.

Therefore, this unconventional selection timetable has become an extremely ingenious political move.

Trump plans to finalize his nominee by the end of 2025, while Powell's term doesn't end until May 2026. This is not superfluous. As Nick Timiraos of "The New Fed Watch" analyzes, the real killer move of this arrangement is that the new chairman will first be nominated to fill the seat of current governor Stephen Miran, which expires next January.

This means that in March and April, when Powell remains in office, the chairman-elect will serve as a formal member of the FOMC and have full voting rights on interest rates.

This was a politically astute move. We only need to recall Milan himself – he participated in the FOMC vote on his second day in office and became the only hawkish "traitor" to vote for a 50 basis point rate cut (rather than a 25 basis point cut) at the September meeting.

Trump is replicating and escalating this strategy. He intends to install an unwaveringly loyal and (most likely) extremely dovish shadow chairman into the core of policymaking during Powell's caretaker period, imposing his agenda two months in advance. This is far from a smooth transition; it's a carefully orchestrated internal coup aimed at preemptively seizing control of monetary policy.

The debate over two paths to the digitalization of the US dollar

Once it was understood that the fundamental purpose of this coup was to serve fiscal needs (i.e., debt financing), the policy spectrum of the five candidates instantly became clear. The media is still debating who is more "dovish," but that's no longer the point.

The real battleground is this: Will the future hegemony of the US dollar rely on innovation in the private sector or on the monopoly of the state apparatus? This is not a simple policy disagreement, but a profound philosophical debate about the future monetary architecture.

Route 1: Public-Private Partnership – Turning Privately Owned Stablecoins into Government Bond Purchasing Machines

This is the most likely path, and the one that will most directly benefit the crypto market. It represents a strategic vision of public-private partnership, the core of which is to leverage the vitality of the private sector to feed back into the U.S. fiscal system. This "alliance" boasts a truly impressive lineup.

The architect of this strategy is Scott Bessent . The former chief investment officer of the Soros Fund, he's not just interested in cryptocurrency. His proposed "3-3-3 policy" (3% deficit, 3% growth, and a 3 million barrel increase in oil production) is a comprehensive supply-side reform agenda. But his real highlight is his prediction that the stablecoin market will grow 20-fold to $2.8 trillion and become a major buyer of US Treasury bonds.

When even Trump himself started talking about using cryptocurrency to "zero out" the $35 trillion debt, Bessant's proposal ceased to be radical rhetoric and instead became a blueprint for translating the president's intentions into actionable policy. It's a perfect closed loop: the government loosens regulations, the private sector (like Circle and Tether) issues stablecoins, and the reserves of these stablecoins (cash and US Treasury bonds) in turn finance the US fiscal deficit.

Internal executors are current Board members Christopher Waller and Michelle Bowman. Their presence suggests this approach has a solid foundation within the Federal Reserve. Waller is a staunch opponent of CBDCs, known for his famous sarcasm that "CBDCs are a solution in search of a problem." However, he is also a staunch supporter of private stablecoins, believing they can "maintain and expand the international role of the dollar."

Bowman, as the Fed's Vice Chair for Supervision, plays the role of "bomb disposal expert." She is working to eliminate the obstacles that prevent banks from refusing to serve crypto companies due to "reputational risk" (i.e., political pressure, such as Operation Chokehold 2.0). Simply put: Waller is responsible for giving the green light to private stablecoins at the macro level, while Bowman is responsible for removing obstacles to crypto companies' access to the banking system at the micro level.

The ultimate market adopter is Rick Rieder. As BlackRock's Chief Investment Officer for Global Fixed Income, he represents the ultimate institutionalization of Wall Street. His firm has already demonstrated its power through its Bitcoin ETF. Rieder's entry into the market signals the full embrace of digital assets by traditional finance as a legitimate store of value and diversification tool.

Route 2: National Monopoly – Establishing a Digital Track Controlled by the Federal Reserve

Another frontrunner, Kevin Warsh , represents a completely opposite approach.

Warsh's credentials are impeccable, having served on the Federal Reserve Board during the 2008 financial crisis. His core pitch is for "regime change," even calling for a "new Treasury-Federal Reserve agreement." This is a highly disruptive proposal that essentially challenges the core principle established since 1951 to free the central bank from the obligation to finance government spending.

Warsh's attitude toward digital assets is extremely complex. On the one hand, he is an angel investor in crypto startups (such as the algorithmic stablecoin Basis) and is well aware of the technology's potential; on the other hand, he is highly skeptical of private cryptocurrencies that are "disguised as currencies."

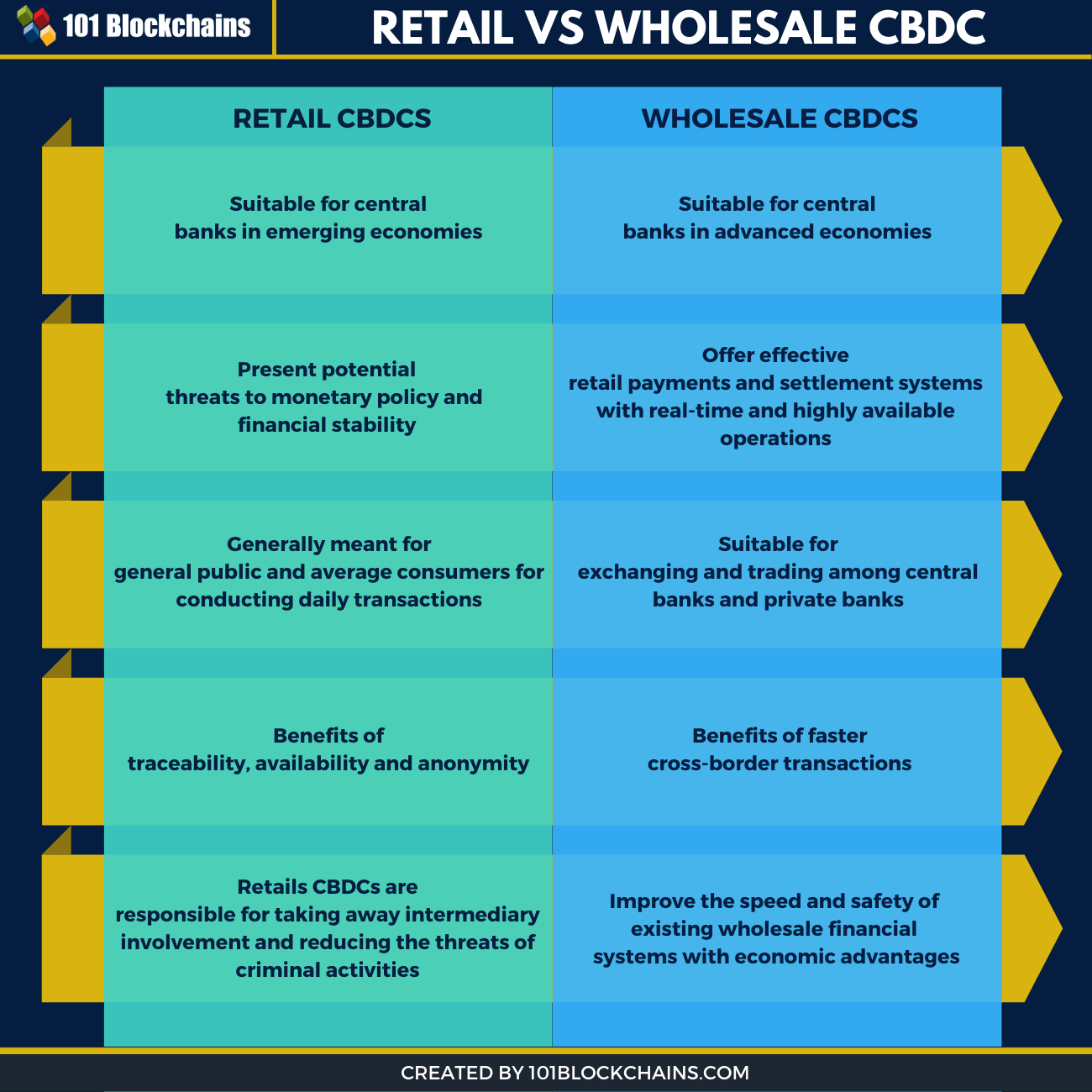

What he really supports is the state-led " wholesale CBDC" .

To help readers understand, this is not a "digital yuan" or "digital dollar" (i.e., a retail CBDC) for ordinary people, but a super settlement network operated by the Federal Reserve and used exclusively by banks and other financial institutions. It aims to make large interbank transfers instant, efficient, and near-zero cost.

This poses a potentially significant threat to the crypto industry. A highly efficient, state-controlled interbank digital dollar system could fundamentally marginalize private stablecoin issuers. In Warsh's vision, the future of currency must be state-led, and any private innovation could be seen as a target for regulatory suppression.

The next Federal Reserve chairman? A comparison of the top candidates

Cryptocurrency at a crossroads: a booster or a shackle?

The new Federal Reserve's dovish shift is almost certain. But for the crypto industry, this is by no means the whole story. The liquidity frenzy brought about by interest rate cuts is certainly tempting, but hidden behind the loose policy are two completely different regulatory paths: one is a booster of integration, and the other is a strict constraint imposed by the national team.

If "Route One" (a public-private alliance) prevails, the crypto industry will usher in a period of "convergence and prosperity." This will be a "convergent" Federal Reserve, headed by figures like Bessant, Waller, or Bowman. What we will see is not only an aggressive rate-cutting cycle, but also a complete deregulation. Banks will be encouraged to provide services to the crypto industry, and institutions like BlackRock will lead a funding frenzy.

For the market, this not only means a bull market for Bitcoin, but also potentially explosive growth for stablecoins and DeFi . A $2.8 trillion stablecoin market will reshape global finance. But all this comes at a price. This is more like a co-optation: as the crypto industry gains mainstream acceptance, its ideals of decentralization and censorship resistance may be sacrificed, becoming relegated to a more efficient settlement layer for traditional finance and a tool for sustaining national finances.

Conversely, if "Route 2" (state monopoly) prevails, the industry will face competition from the national team. This represents a "reformed" Federal Reserve led by Warsh. Interest rate cuts will occur, but the iron fist of regulation will fall heavily on the private sector. The Fed will pour resources into developing its wholesale CBDC and may impose strict limits on the reserves held by private stablecoins (such as USDC and USDT), viewing them as competitors to national digital currencies.

Imagine if banks had an instant, zero-cost digital dollar settlement track backed by the Federal Reserve. How much incentive would they have to use Circle or Tether's services? This would be a future fraught with conflict and uncertainty, with markets repeatedly torn between loose monetary policy and regulatory crackdowns.

Federal Reserve Chairman – America's "Chief Financing Officer for Debt"

Trump's "joke" about Bessant was actually his most straightforward "confession".

What he needs is no longer a traditional central bank governor who worries about inflation data. What he needs is a chief financing officer who can find an "antidote" to the astronomical debt of the United States.

When Trump himself began publicly discussing using a cryptocurrency on a "little piece of paper" to "zero out" $35 trillion in debt, Bessant was the only one of the five candidates to concretely define this as a viable path (using stablecoins to purchase Treasury bonds). This selection marked the end of an era. Central bank independence was giving way to the imperatives of fiscal survival.

Cryptocurrency, a heresy born on the fringe, is being forcibly pulled into the core of the state apparatus and becoming the most critical weapon in this battle to defend finances.

For the crypto industry, this presents both an unprecedented opportunity and its most severe test of survival. We must prepare for a fundamental "regime change" in the central bank system—whether we like it or not, cryptocurrencies are destined to be pushed to the core of the future monetary system.