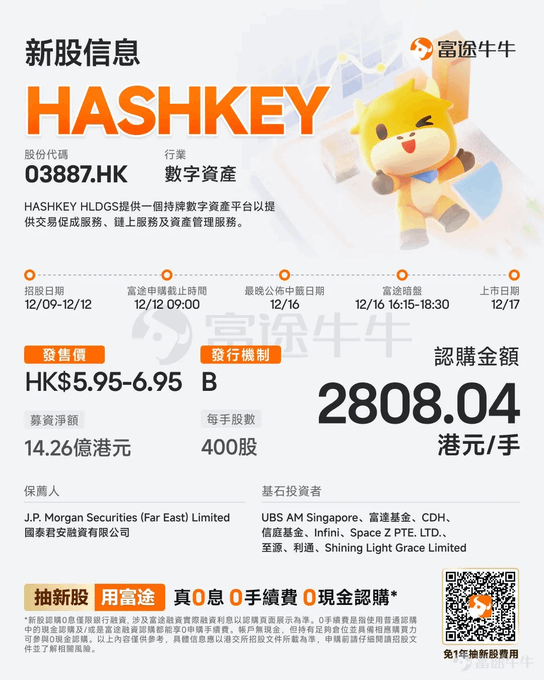

Frankly, I've seen too many #Web3 projects telling "stories" in the past two years, but in Asia, there's practically only one that has managed to integrate that story into the regulatory framework, its prospectus, and the mainstream capital system—#HashKey (@HashKeyGroup). Now, it has officially passed the Hong Kong Stock Exchange's listing hearing and will be listed on December 17th. It has also attracted three top-tier cornerstone investors from the financial sector: UBS, Fidelity, and CDH Investments. This lineup is quite impressive; it's not just simple "support," but a vote of real money. Foreign investors are attracted to its compliance approach, and CDH Investments understands the value of its platform. As a seasoned investor, this is the first time I've felt that Hong Kong has gone from "experimenting" to "getting serious," and #HashKey's listing is the starting gun. 1️⃣HashKey's Core Value—Systemic Compliance Capability Most exchanges start by "listing new coins and boosting trading volume," but HashKey goes against the grain, starting with a "comprehensive top-down regulatory compliance framework," setting a high bar from the outset. These two development paths lead to drastically different outcomes: trading volume can be artificially inflated, tokens can be listed, and retail advertising can be implemented. However, compliance capabilities, institutional-level risk control frameworks, asset management capabilities, and on-chain infrastructure are entirely inimitable and require significant time for development and accumulation. This path, while starting slowly, has become increasingly stable: ▸ 2018–2021: While others were frantically pursuing trading volume, they were building infrastructure. Knowledge verification, risk control, custody, and compliance internal controls may sound low-profile, but these are the "underlying operating system" for obtaining licenses. ▸ 2022 Obtaining Licenses: A Watershed Moment and a Barrier to Entry Becoming one of the first virtual asset exchanges to obtain Class 1/7 licenses is not just a "permit"; it essentially means being able to serve clients using traditional financial institution standards. This isn't just a simple certificate; it's HashKey securing its ticket to partnerships with banks, financial institutions, and funds. ▸ 2023 to Present: The HashKey Ecosystem is Basically Formed • Exchange: Expanding from professional investors to retail • Custody, OTC, and Staking Services: A Complete Chain • HashKey Capital: One of Asia's Largest Blockchain VCs and Secondary Fund Managers • HashKey Chain: Building the Underlying Network for RWA and Institutional On-Chain Assets Many people think HashKey is an "exchange." But if you look closely at its structure, you'll find that it's building a compliant foundation for the Hong Kong digital asset market, comparable to Coinbase in the US stock market. 2️⃣ Not Relying on "Transaction Fees" to Survive, But "Helping Institutions Make Money" Many people think HashKey is just an exchange. Wrong! Its core is actually a three-in-one system of "asset management + infrastructure + investment." Managing HK$7.8 billion (as of September 2025), it is one of the largest licensed digital asset management institutions in Asia; its fund returns exceed 10 times, twice the industry average (data from Frost & Sullivan); it has invested in over 400 projects, covering the entire chain from early-stage VC to the secondary market. It has also developed its own blockchain—HashKey Chain—not for issuing tokens to speculate on virtual assets, but specifically for legally putting "real-world assets" such as bonds, real estate, and fund shares onto the blockchain. This is precisely the next step in the currently booming "RWA tokenization" trend, which global financial giants are scrambling to establish. Therefore, HashKey is not just an "exchange," but a forward-thinking player that "invests in projects, invests in sectors, and invests in the future." This "ecosystem + asset management" growth model is something that no one in Hong Kong's virtual asset industry has been able to replicate to date. 3️⃣ Financials: Reasonable "Turning-off Fluctuations" Behind the Rapid Growth Seeing three consecutive years of losses in the financial reports (a loss of nearly HK$1.2 billion in 2024), most people might frown. However, a closer examination reveals that these losses are not operational, but rather strategic investments. HashKey's gross profit margin has consistently been above 70% (73.9% in 2024), indicating that its business model is inherently profitable. The losses primarily stem from: technology R&D (such as HashKey Chain), licensing and compliance, global team building, and early-stage investments. Currently, it has HK$1.657 billion in cash and HK$592 million in digital assets, demonstrating extremely healthy cash flow. This is similar to Tesla's losses in 2019, yet no one questioned its technological barriers and ecosystem ambitions. HashKey is now doing something similar—using high investment to build a long-term competitive advantage. Finally, on December 17th, #HashKey will be listed on the Hong Kong Stock Exchange. Seeing that Futu is also supporting IPO subscriptions today, I must support the "first Hong Kong crypto stock." If Coinbase represents the "American model"—first build a large user base, then seek compliance; then HashKey represents the "Hong Kong model"—first achieve compliance, then serve institutions, and finally drive the ecosystem. In the context of Chinese capital markets, HashKey's path will be more stable and sustainable. I believe that international institutions looking to enter the Asian market will see HashKey as a "compliance gateway." If it succeeds, a number of similar companies will follow suit, forming a "digital finance Hong Kong stock market sector," creating a cluster effect. Asia's Coinbase is setting sail; let's wait and see! 🧐 @siyahashkey

This article is machine translated

Show original

Sector:

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content