The suspense surrounding the final airdrop of the year came to an end last night (December 30th). Perp DEX (decentralized perpetual contract exchange) Lighter announced the completion of its airdrop, distributing a total of $675 million to early participants, bringing a glimmer of hope to the bleak market at the end of 2025.

While the winter market is somewhat bleak, competition for liquidity and trading experience on the Perp DEX arena is intensifying. The industry is witnessing the gradual replacement of early Automated Market Makers (AMMs) by high-performance centralized limit order books (CLOBs). Lighter, based on zk-rollup, has quickly emerged as a leader, attempting to redefine the standards of on-chain derivatives trading with its zero-fee strategy and customized ZK circuitry.

Airdrops have always been a double-edged sword, and Lighter undoubtedly faces the same problems that other airdrop projects have encountered: dissatisfaction with airdrops and user retention in the post-airdrop era.

The airdrop response was polarized, and the token distribution sparked controversy.

Lighter completed its TGE yesterday, and its protocol token LIT exhibited significant volatility in the initial launch period. In pre-market trading on several centralized exchanges, LIT briefly reached a high of $3.9. After the TGE officially began, the price surged to $7.8 in a short period before falling back and stabilizing in the $2.6 to $3 range.

According to Bubblemaps monitoring, the total amount of LIT tokens airdropped to early participants on its first day of launch reached $675 million. Since the airdrop began, approximately $30 million has flowed out of Lighter.

Lighter's airdrop was relatively generous, but community opinions were polarized. Supporters argued that the initial airdrop, representing 25% of the total supply, amounted to approximately $690 million directly distributed to Season 1 and Season 2 token holders, with no lock-up restrictions—a stark contrast to the lower token allocations of many other projects' TGE tokens. Opponents, however, argued that the conversion rate between Season 1 and Season 2 tokens was approximately 20 to 28 LIT tokens per token. For some users with high trading frequency, this was roughly equivalent to the transaction fees they paid, failing to deliver the expected substantial returns.

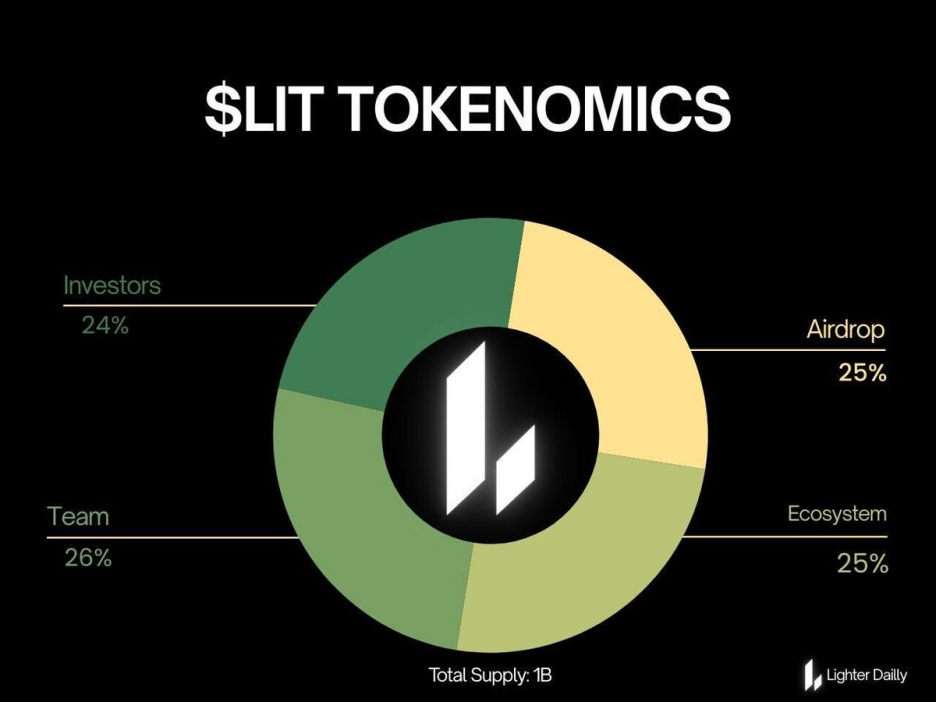

The biggest controversy surrounding this TGE lies in Lighter's token economics. The total token supply is 1 billion, with 50% allocated to the ecosystem and the remaining 50% to the team and investors, with a 3-year linear vesting period. This plan has been criticized by the community as "team-driven": while investor lock-up is strict, the overall proportion is too high, potentially diluting community interests. The 25% unlocked airdrop of tokens may create short-term selling pressure, while the 50% lock-up share could lead to potential long-term selling pressure, hindering the steady growth of LIT's market capitalization.

From a valuation perspective, Lighter's pricing directly mirrors that of Hyperliquid and Aster. Although its trading volume once surpassed these two competitors, the market still has doubts about the rationality of its valuation.

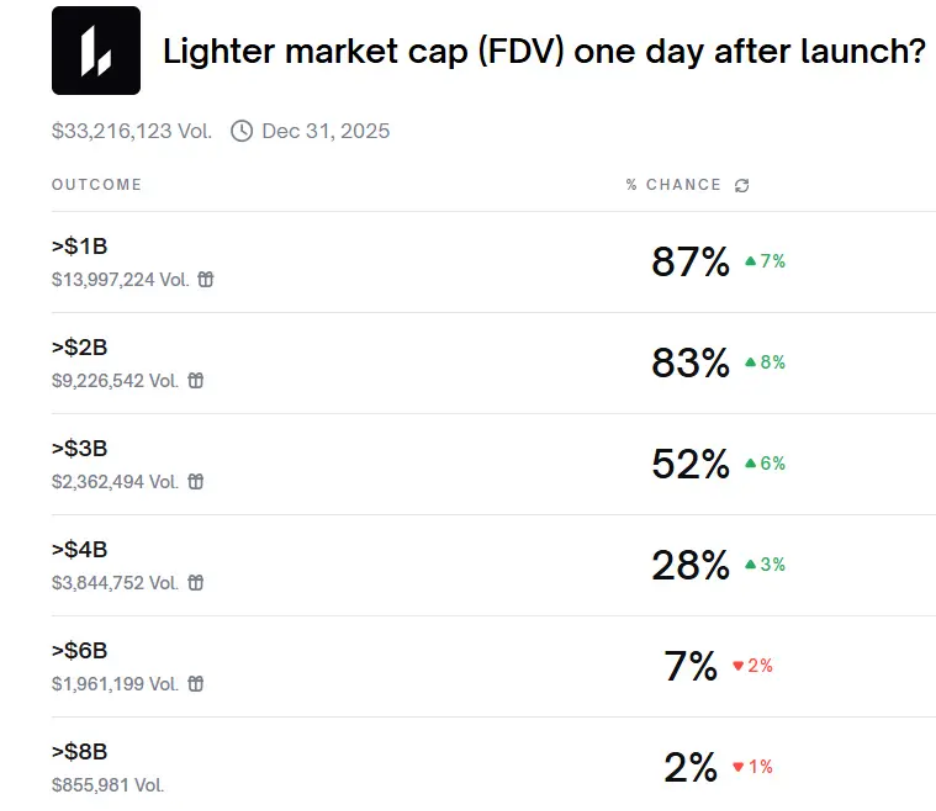

According to CoinGecko data, Lighter currently has a market capitalization of approximately $680 million and a fully diluted FDV (valued at $2.7 billion). A week ago, Polymarket predicted an 83% probability that Lighter's market capitalization would exceed $2 billion on its second day of listing.

Lighter CEO Vladimir Novakovski stated in a podcast interview that tokens don't usually skyrocket upon launch; the realistic expectation is for them to start from a relatively healthy position. Andy, founder of The Rollup, also tweeted that he would buy LIT if its FDV was around $2 billion.

Overall, Lighter's TGE performance was largely in line with expectations, but there were no surprises. Coupled with the overall market downturn, the community's overall response to the protocol was not significant.

Top-tier capital bets on Harvard geniuses to create Lighter

Lighter's story begins with its founder, Vladimir Novakovski, a typical blend of "perfect child" and Wall Street elite. He entered Harvard at 16 and graduated early, subsequently being personally recruited by Ken Griffin, founder of global market-making giant Citadel. This experience at a top quantitative fund gave him a deep understanding of the microstructure of traditional financial markets and the essence of liquidity management.

However, this genius's ambitions did not stop at Wall Street. He had previously successfully founded Lunchclub, an AI social platform valued at over $100 million on Web2. In 2023, he astutely recognized the gap in on-chain financial infrastructure and led 80% of his team to shift their focus to cryptocurrency, dedicating themselves fully to the research and development of Lighter.

"The main reason we invested in Lighter is because of Vladimir and his team's engineering capabilities." This statement by Joey Krug, a partner at Founders Fund, a top Wall Street VC firm, reveals the underlying logic of capital investment: in an extremely complex technology sector, the density of top talent is the main competitive advantage.

In November 2025, Lighter announced the completion of a $68 million funding round, bringing its post-money valuation to $1.5 billion.

The participation of renowned brokerage firm Robinhood in the investment may send an important signal: traditional financial giants are looking for Perp DEX infrastructure capable of truly supporting institutional-level trading volumes. This will not only bring funding to Lighter but also allow it to access a potential user base from traditional financial institutions.

ZK empowers Lighter to achieve 15K+ TPS while maintaining verifiability.

2025 marked a watershed moment for the Perp DEX sector. While early protocols like dYdX and GMX validated the feasibility of on-chain derivatives trading, they consistently lagged behind CEXs (centralized exchanges) in terms of execution speed, slippage control, oracle latency, and liquidity depth. Lighter, however, achieved sub-second execution times and higher capital efficiency by employing the CLOB model and a high-performance Layer 2 architecture.

The core logic behind this evolution is that verification equals trust. Lighter does not require users to trust the matching engine. Instead, it uses a customized ZK circuit to generate verifiable cryptographic proofs for every order matching, every risk assessment, and every liquidation activity. This architecture ensures that even if the sorter attempts to act maliciously or is attacked, the underlying Ethereum mainnet contracts can still guarantee asset security.

Lighter's technological moat is built on a seemingly contradictory combination: decentralized trust (ZK) and centralized efficiency (CLOB). Its architecture not only pursues high performance but also emphasizes transparency and non-custodial nature, which gives it a strong "Ethereum native" attribute in its technological narrative.

Unlike many general-purpose ZK virtual machine protocols, Lighter has chosen a more challenging path: customizing ZK circuits (zkLighter) for trading logic. This allows the protocol to generate proofs with extremely high efficiency, achieving a throughput of up to 15,000+ TPS (transactions per second) and soft finality of less than 10 milliseconds, which is sufficient to meet the demanding requirements of high-frequency traders.

It is worth mentioning that Lighter's underlying data structure adopts a "supertree" architecture to ensure that even when the system is in a state of extremely high concurrency, the transaction price of each order will be the optimal one at that time.

To mitigate the extreme risks of the sorter going offline or failing to provide service, Lighter also features an "escape pod" mode. Since all account balances and position data are published on Ethereum as Blob data, users can generate their own account value proofs based on publicly available data history and withdraw funds directly from the mainnet without authorization from the sorter. This mechanism also gives Lighter superior censorship resistance and asset sovereignty compared to the self-built L1 consensus Perp DEX protocol.

Zero-fee model reshapes customer acquisition logic through agreements

The reason Lighter has attracted such a high level of capital and user attention is not only because of its high performance and verifiability, but also because of its triple innovation in fee structure, capital efficiency and liquidation logic.

In a context where Perp DEX generally relies on transaction fees for profit, Lighter dropped a bombshell on the market with its "zero transaction fees".

The agreement designs a clever two-tiered account model to balance business sustainability.

- Retail Account (Standard): All Maker and Taker fees are waived for regular users. While this results in a slight latency of around 300ms, the cost savings are very attractive for most infrequent users.

- Premium Account: Designed for institutional and high-frequency traders, offering zero-latency access but with extremely low transaction fees (Maker 0.002%, Taker 0.02%).

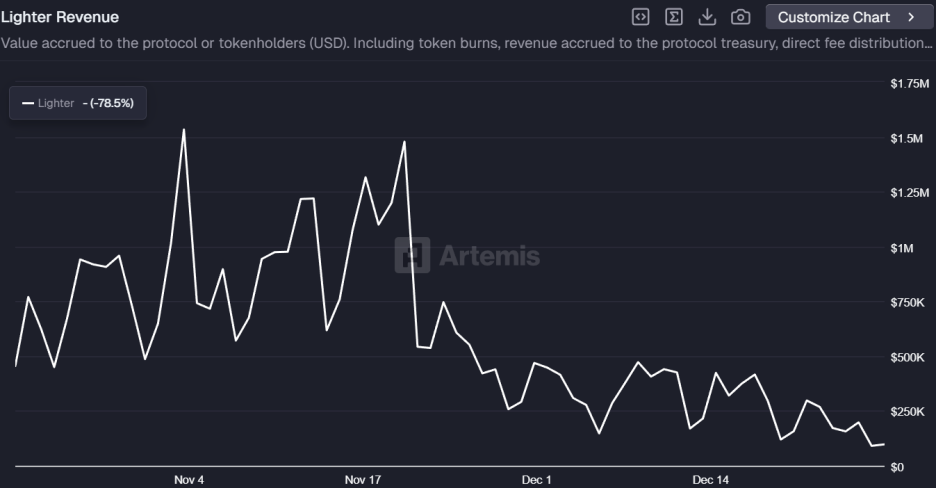

Currently, Lighter's revenue mainly comes from premium account fees and clearing fees, with an average daily revenue of approximately $200,000, which initially validates the feasibility of its customer acquisition model.

However, Lighter's revenue has declined in the past week, possibly due to the market downturn. The token airdrop expectation has been realized, and the protocol's true revenue-generating ability remains to be seen.

If zero fees are the hook for attracting users, then Cross Margin Margin (UCM) is the killer app for retaining professional funds.

Traditional Perp DEXs typically require users to deposit stablecoins such as USDC as margin, resulting in low capital efficiency. To address this, Lighter introduced the UCM system, which allows traders to directly use interest-bearing assets stored on Ethereum L1 (such as stETH, LP tokens, or even Aave deposit positions) as collateral for L2 leveraged trading.

The ingenuity of this design lies in the fact that users' collateralized assets do not need to be moved across chains, but are instead mapped to L2 via ZK proofs. This means that users can earn L1 staking rewards while simultaneously opening orders on L2.

In the event of liquidation, the system generates a cryptographic proof and submits it to the L1 contract, automatically deducting the corresponding assets. This "asset immobilization, credit extension" model significantly improves capital efficiency and eliminates the difficult choice users face between yield assets and transaction funds.

The liquidation mechanism has always been the most contentious aspect of Perp DEX. Lighter uses ZK circuits to ensure that liquidation actions are fully verifiable, reducing the likelihood of malicious manipulation or forced liquidation on the platform.

In addition, Lighter has launched risk-tiered liquidity pools:

- LLP (Lighter Liquidity Provider): This is the main protocol pool, acting as both a counterparty and a clearing executor. It not only profits from losing trades but also captures funding rates and clearing fees. Currently, LLP's annualized yield remains around 30%.

- XLP (Experimental Liquidity Provider): An isolated pool specifically designed for experimental assets (such as pre-market tokens, RWA, and low-liquidity Altcoin). XLP does not participate in forced liquidation, and its risk exposure is isolated from the main protocol, making it suitable for liquidity providers with a higher risk appetite.

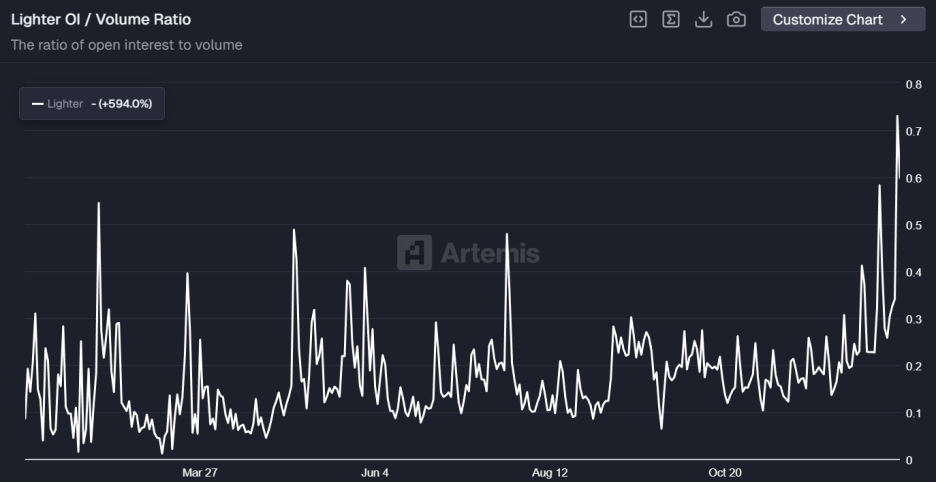

The OI/Vol ratio has been hovering around 0.2 for a long time, and the data may be significantly dehydrated after the data drop.

Lighter, running at high speed, is not without shadows.

The protocol's exaggerated OI/Vol (Open Interest/Volume) ratio has sparked widespread skepticism in the market. Although the ratio has recently rebounded, Lighter had long maintained a ratio around 0.2, meaning that on average, every $1 of open interest was traded approximately 5 times within 24 hours. This significantly deviates from a healthy organic open interest model (OI/Vol < 0.33) and exhibits clear characteristics of wash trading.

This phenomenon mainly stems from Lighter's aggressive points-based incentive program. Although the protocol has taken measures such as scarcity of invitation codes and weighted holding periods to defend against this, the TGE (token generation event) has ended, and the fate of these high-frequency transactions will also affect Lighter's actual market share.

Lighter's frequent outages have exposed its system instability. On October 9th, the protocol experienced a 4.5-hour outage. On December 30th, Lighter encountered a problem where the proof generator stalled, preventing users from withdrawing funds. For a derivatives platform handling billions of dollars in funds, stability is its lifeline.

The emergence of Lighter represents a new stage in the evolution of Perp DEX: from decentralization to verifiable high performance. The protocol solves the trust problem through the security of the Ethereum mainnet and ZK technology, and enters the Perp DEX arena with a zero-fee strategy.

However, the competition in the Perp DEX sector is no longer a simple contest of technology, but a comprehensive battle involving liquidity, community ecosystem, and product quality. Whether Lighter can grow from a technological dark horse to a leader in the sector depends on its ability to continuously attract and retain genuine trading demand in the post-airdrop era.