Original title: a16z: The Power Brokers

Original source: Not Boring

Original translation by: Saoirse, Foresight News

Editor's Note: This article focuses on venture capital giant a16z, taking advantage of its newly raised $15 billion fund to delve into the core of its "unconventional venture capital" approach—planning for the future with an engineer's mindset and betting on potential companies (such as Databricks) with unwavering conviction. The article interweaves performance data and classic case studies to dissect its evolution from a startup to managing over $90 billion in assets. To understand how this "tech believer" is reshaping industry rules, delve into the article.

When a16z announced its massive $15 billion fundraising, the entire venture capital world was once again shaken – some dug up years of doubts about its business model, while others wondered where the money would go.

To understand this controversial institution, I talked to its GP (General Partner) and LP (Limited Partner), had in-depth conversations with the founders of its portfolio companies valued at over $200 billion, and also reviewed its fund return data since its inception.

However, rather than dwelling on "where a16z went wrong", I'd like to ask: what are those smart people who have always made the right judgments in the past aiming at now? Of course, I have to admit that I was once a crypto consultant for a16z and was listed on the shareholder list alongside key figures, so I can't be considered a completely objective observer.

But I don't want to judge whether this 15 billion is worth investing in—institutional LPs have already voted with their hard-earned money, and the answer won't be revealed for another ten years. What I want to show you is: why has a16z become the "best storyteller" in the venture capital world? What unconventional ambitions does its vision for the future hold?

"I live in the future, the present is already the past; my existence itself is a gift, if you disagree, then leave."

——Kanye West, "Monster"

"Too flamboyant." "In politics, one should talk less and do more." "I disagree with one or two of its recent investment projects." "Quoting the Pope on social media is extremely inappropriate." "With such a large fund size, it's impossible for it to provide reasonable returns to its LPs."

a16z has been listening to these sounds for almost 20 years.

For example, in 2015, New Yorker reporter Tad Friend had breakfast with Marc Andreessen (co-founder and general partner of a16z) to write an article titled "Future Pioneers". Prior to this, Friend had just heard a question from a fellow venture capitalist: a16z's fund size was too large, but its shareholding ratio was too low[1]. To achieve a total return of 5-10 times for the first four funds, the total valuation of its portfolio would have to reach $240-480 billion.

In the article, Friend wrote, "When I tried to check this data with Andreessen, he made a dismissive gesture and said, 'Nonsense. We have the whole model—we're here to catch elephants, to chase big fish!'"

Please remember this image, because you may have similar questions later, and Andreesse will most likely react the same way.

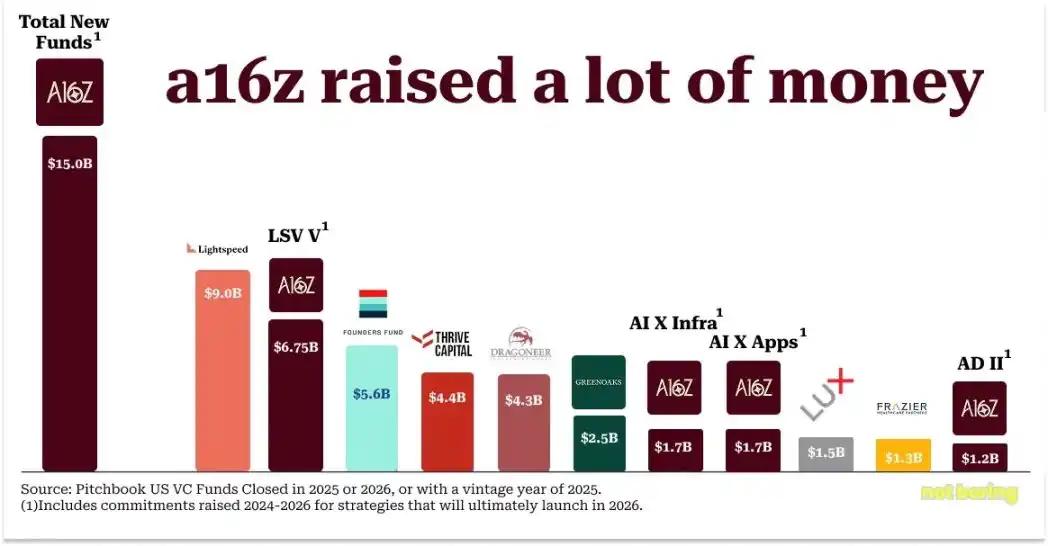

Today, a16z announced that it has raised a total of $15 billion across all its investment strategies, bringing its total assets under management (RAUM) to over $90 billion.

a16z's fund strategies and corresponding fund sizes raised in 2025

In 2025, the venture capital fundraising market was dominated by a few leading institutions, and a16z raised more than the combined fundraising amount of Lightspeed ($9 billion) and Founders Fund ($5.6 billion), which ranked second and third respectively.[2]

In the worst venture capital fundraising environment in the past five years, a16z raised more than 18% of the total venture capital fundraising in the United States in 2025[3]. It usually takes an average of 16 months for a venture capital fund to complete fundraising, while a16z took only three months from start to finish.

If we break it down, four of a16z's funds could be among the "Top 10 Fundraising Funds in the Industry in 2025": LSV V, a late-stage venture capital fund, ranked second; AI Infrastructure Fund X and AI Application Fund X tied for seventh; and AD II, the "US Vitality Fund," ranked tenth.

Comparison of fundraising scale of US venture capital firms in 2025-2026

Some might argue that with so much money, venture capital firms simply can't allocate it effectively to achieve excess returns. But I suspect a16z's response would be: "Nonsense." After all, they're always "hunting elephants, chasing big fish!"

Today, a16z’s portfolio includes 10 of the “Top 15 private companies by valuation”: OpenAI, SpaceX, xAI, Databricks, Stripe, Revolut, Waymo, Wiz, SSI and Anduril [4].

Over the past decade, a16z has invested in 56 unicorn companies through its funds[5], more than any other institution in the industry.

Its AI portfolio covers 44% of the total valuation of unicorn companies in the industry[6], which is also the highest.

From 2009 to 2025, a16z led early-stage investments in 31 companies with an eventual valuation of over $5 billion, which is 50% more than the combined total of the second and third ranked institutions.

They not only have a complete model, but now they also have solid performance backing.

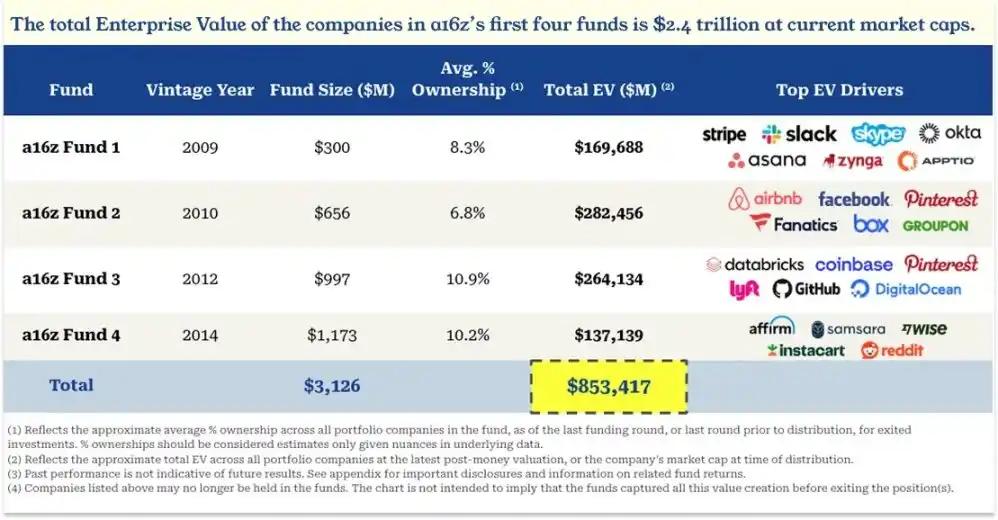

As mentioned earlier, peers have questioned whether the combined valuation of the first four a16z funds needs to reach $240 billion to meet the target. In fact, the total combined valuation of a16z funds 1-4 (calculated based on the valuation at the time of exit or the latest post-investment valuation) has reached $853 billion[7].

Total portfolio value of the first four funds of a16z

And this is just the valuation at the time of exit—Facebook alone has since added another $1.5 trillion to its market value!

This scenario plays out repeatedly: a16z makes what seems like a crazy bet on the future, which industry insiders call "stupid," but years later it turns out it wasn't stupid at all!

Following the 2009 global financial crisis, a16z raised $300 million in its first fund and proposed the concept of "providing an operational support platform for founders." Ben Horowitz (co-founder and general partner of a16z) recalled, "We talked to many venture capitalists, and most of them said it was a stupid idea, advised us not to do it, and said that this model had been tried before and simply didn't work." Today, almost all top venture capital firms have similar platform teams.

In 2009, a16z took $65 million from this fund and, together with Silver Lake and other institutions, acquired Skype from eBay for $2.7 billion. At the time, "everyone said the deal wouldn't go through because the intellectual property risks were too great"—after all, eBay was in litigation with Skype's founders over the ownership of the technology at the time of the deal. Less than two years later, Microsoft acquired Skype for $8.5 billion, and Ben recalled the doubts at the time in a blog post.[8]

In September 2010, Marc and Ben raised $650 million in Fund II, subsequently making large-scale late-stage investments in companies such as Facebook ($50 million, post-money valuation of $34 billion), Groupon ($40 million, post-money valuation of $5 billion), and Twitter ($48 million, post-money valuation of $4 billion), betting on the imminent opening of the IPO window. The Wall Street Journal, in an article titled "Venture Capital Newcomers Shake Silicon Valley," wrote that peers were quite dissatisfied, believing that "private equity transactions are simply not what venture capitalists are supposed to do" (at the time, this now common practice was still novel and not even labeled "secondary transactions"). Benchmark partner Matt Cohler famously stated, "You can make money trading pork futures and oil futures, but that's not what we're supposed to do." And what happened? In November 2011, Groupon went public with a valuation of $17.8 billion; in May 2012, Facebook went public with a valuation of $104 billion; and in November 2013, Twitter's valuation reached $31 billion on its first day of trading.

In January 2012, Marc and Ben raised $1 billion in Fund III and $540 million in parallel opportunity funds. The initial skepticism shifted to what is now commonly perceived as "too big": a16z's fundraising accounted for 7.5% of total US venture capital funding that year, while the venture capital industry as a whole was struggling. A 2014 Harvard Business School case study on a16z cited a 2012 report from the Kaufman Foundation, which stated, "For over a decade, venture capital returns have been terrible." Cambridge Associates data showed that the average venture capital return in 2012 was only 8.9%, far below the S&P 500's 20.6%. Legendary venture capitalist Bill Draper famously said, "The consensus in Silicon Valley's venture capital industry is that too many funds are chasing too few truly good companies." This statement remains relevant today.

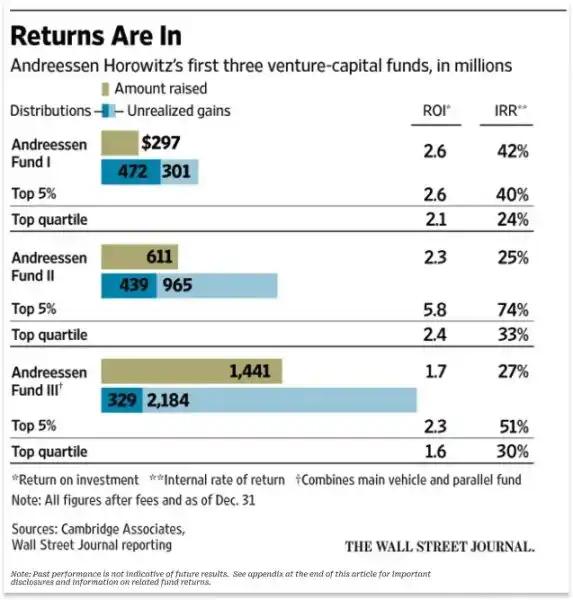

In 2016, The Wall Street Journal published an article that David Rosenthal of the Acquired podcast called "clearly a smear campaign orchestrated by fellow venture capitalists," titled "Andreessen Horowitz (a16z) Funds Lag Behind Venture Capital Elite." At the time, a16z's three funds had been established for 7, 6, and 4 years, respectively. The article claimed that while Fund 1 was among the top 5% in the industry, Fund 2 was only in the top 25%, and Fund 3 didn't even make the top 25.

The performance of the top 3 a16z funds and a comparison with industry leaders.

Looking back now, this Fund No. 3 can be described as "legendary": as of September 30, 2025, its net TVPI (total value of invested capital) after deducting fees reached 11.3 times; if parallel funds are included, the net TVPI is 9.1 times.

Fund 3's portfolio includes Coinbase (which has generated $7 billion in distributions for a16z LPs), Databricks, Pinterest, GitHub, and Lyft (though it missed out on Uber, this one oversight ultimately outweighs its numerous successful investments). I believe this fund is one of the most successful large-scale venture capital funds in history. After Q3 2025, Databricks (currently a16z's largest holding) is valued at $134 billion, meaning Fund 3's performance is still climbing (assuming other holdings don't depreciate). From Fund 3 and its parallel funds alone, a16z has already net distributed $7 billion to LPs, with nearly an equal amount of unrealized gains yet to be realized.

A significant portion of these unrealized gains comes from Databricks. When the Wall Street Journal issued a negative report on a16z in 2016, the big data company was still small, its valuation several months shy of $500 million. Today, Databricks accounts for 23% of a16z's total net asset value (NAV).

Anyone who has interacted with people at a16z will frequently hear the name "Databricks". It is not only a16z's largest holding (and perhaps one of the top three holdings in the entire venture capital industry), but its development history is also a vivid example of a16z's "best operating model".

The operating formulas of Databricks and a16z

Before discussing Databricks, there are a few key points about a16z that need to be understood first.

First, a16z was founded and is run by engineers—not just founders, but "founders with engineering backgrounds." This influenced the organization's design logic (pursuing economies of scale and network effects) and determined their criteria for choosing markets and companies.

Secondly, at a16z, "being second in the investment industry" might be the biggest "original sin" of investing. If you miss out on the winner early on, you can still make up for it later; but if you invest in the second-place winner, you will completely lose the opportunity to invest in the winner—even if the winner has not yet emerged at that time.

Third, once a16z determines that a company is the "winner in its field," their classic tactic is to "invest far more money than the company expected." This approach is often ridiculed in the industry, but they persist in it.

These three points have remained unchanged since the early days of a16z.

In the early 2010s, just a few years after a16z was founded, "big data" was the hottest topic, and the mainstream big data framework in the industry was Hadoop. Hadoop uses Google's MapReduce programming model, distributing computing tasks to inexpensive, general-purpose server clusters instead of expensive dedicated hardware, making it a driving force behind the "democratization of big data." Subsequently, a number of companies surrounding Hadoop emerged, and the industry's investment boom peaked in 2014: Cloudera, founded in 2008, raised $900 million, and the total funding for Hadoop-related companies that year increased fivefold to $1.28 billion; Hortonworks, spun off from Yahoo, also went public that year.

Big data is booming and attracting a flood of funds, but a16z remains inactive.

The "z" in a16z—Ben Horowitz—is fundamentally skeptical of Hadoop. Before becoming CEO of LoudCloud/OpsWare, he had a computer science background and believed Hadoop would never become a mainstream architecture: "It's complex to program, difficult to manage, and doesn't meet future needs—every step of the MapReduce computation requires writing intermediate results to disk, which is infuriatingly slow for iterative computational tasks like machine learning."

So Ben chose to avoid the Hadoop craze. Jen Kha told me that Marc even "criticized" Ben for this at the time.

"We've definitely missed a chance! We've completely messed up and made a huge mistake!" Marc was frantic at the time.

But Ben said, "I don't think this is the direction the next architectural change will take."

Then Databricks came along, and Ben said, "This might be the right thing to do." And then, of course, he bet everything.

The birth of Databricks was timely, and it was located near the University of California, Berkeley.

During the Iranian Revolution in 1984, Ali Ghodsi and his family fled Iran and moved to Sweden. His parents bought Ali a Commodore 64 computer, which he used to teach himself programming. His skill level was so high that he even received an invitation to be a visiting scholar at the University of California, Berkeley.

At Berkeley, Ali joined the AMPLab lab, where he worked with eight researchers, including his advisor Scott Shenker and Ion Stoica, to bring to life the ideas in doctoral student Matei Zaharia's dissertation and develop Spark—an open-source big data processing engine.

Spark's design philosophy is to "reproduce the functionality that tech giants have achieved with neural networks without complex interfaces." It once set a world record for data sorting speed, and Zaharia's paper won "Best Computer Science Paper of the Year." However, following academic practice, after they made the code free and open source, almost no one uses it.

Starting in 2012, these eight people met several times for discussions and ultimately decided to form a company around Spark, named Databricks. Seven of them became co-founders, and Shenker served as an advisor.

Databricks co-founder Ali Ghodsi sat in the front center seat, according to Forbes.

The team initially felt they "needed some money, but not too much." Ben recalled in an interview with Lenny Rachitsky:

"When I met with them, they said, 'We need to raise $200,000.' At that time, I knew that they had Spark, and their competitors were Hadoop companies that already had large amounts of funding. Moreover, Spark is open source, and time was of the essence."

Ben also realized that, as academics, the team was "easily content with small goals." He told Lenny, "Generally speaking, if a professor's startup can achieve a valuation of $50 million, they're already considered a 'hero' on campus."

So Ben gave the team some bad news: "I can't write a check for $200,000."

Then came the "good news": "I can write a check for $10 million."

His reasoning was: "If you want to start a business, you have to do it seriously and give it your all. Otherwise, you might as well stay in school."

The team decided to drop out of school. Further investment was made, with a16z leading Databricks' Series A funding round, valuing the company at $44 million post-investment, and a16z acquiring a 24.9% stake.

This initial encounter—Databricks asking for 200,000 and a16z investing 10 million—set the tone for their cooperation: once a16z invests in you, they will "completely trust you" and push you to "aim at bigger goals."

When I asked Ali about the impact of a16z, his attitude was very clear: "I think without a16z—especially without Ben—Databricks wouldn't exist today. I don't think we would have survived this long. They genuinely believed in us."

In the company's third year, revenue was only $1.5 million. "At the time, there was absolutely no certainty that we could succeed," Ali recalled. "The only person who truly believed that this company would be incredibly valuable in the future was Ben Horowitz. His confidence was stronger than all of ours, frankly, even much stronger than my own. He deserves high praise for that."

Having a belief is a great thing, but its value increases when you have the ability to make that belief self-fulfilling.

For example, in 2016, Ali was trying to reach a partnership with Microsoft. In his view, the market demand for "integrating Databricks into the Azure cloud platform" was extremely urgent, and this partnership should have been a natural progression. He asked several venture capital partners to help make connections, hoping to get in touch with Microsoft CEO Satya Nadella—they did help, but these connections ultimately "got lost in the president's assistant's process and came to nothing."

Subsequently, Ben personally facilitated a formal communication channel between Ali and Satya. "I received an email from Satya saying, 'We are very interested in establishing a deep partnership,'" Ali recalled. "He also copied his deputy and his deputy's subordinates. Within just a few hours, I received 20 emails from Microsoft employees I had previously tried to contact without success, all asking, 'When can we meet to discuss this further?' At that moment, I realized, 'This is different; this collaboration is definitely going to happen.'"

For example, in 2017, Ali was trying to recruit a senior sales executive to accelerate the company's business growth. This executive proposed to include a "change of control clause" in the contract—essentially, that if the company were acquired, his shares would be cashed out more quickly.

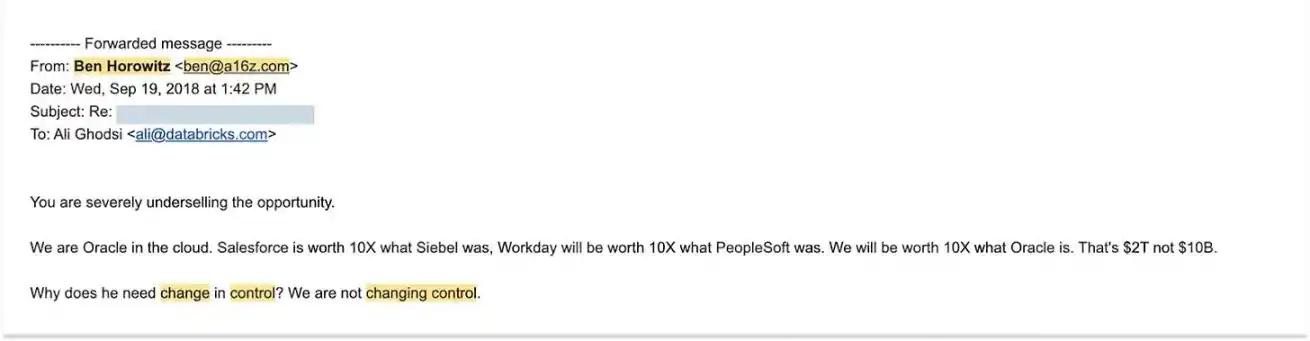

This became a bottleneck in the negotiations, so Ali asked Ben to help persuade the manager that Databricks' valuation "could reach at least $10 billion." After communicating with the manager, Ben sent Ali the following email:

An email from Ben Horowitz to Ali Ghodsi, dated September 19, 2018, provided by Ali Ghodsi.

"You have seriously underestimated the value of this opportunity."

We will become the Oracle of cloud computing. Salesforce is valued at 10 times that of Siebel, Workday at 10 times that of PeopleSoft, and we will be valued at 10 times that of Oracle—meaning our target is $2 trillion, not $10 billion.

Why would he need a "change of control clause"? There will be no change of control at all.

This is probably one of the most impactful corporate emails ever, especially considering that at the time, Databricks had a revenue run rate (annualized revenue) of $100 million and a valuation of only $1 billion; now, the company's revenue run rate has exceeded $480 million and its valuation has reached $134 billion.

“They can see the full potential of something,” Ali told me. “When you’re in the thick of it, dealing with day-to-day operations, surrounded by challenges—deals falling through, being outmaneuvered by competitors, running out of cash, nobody knowing your company, employees constantly leaving—it’s hard to see things that far ahead. But they’ll show up at board meetings and tell you: ‘You will conquer the world.’”

Their judgment was correct, and this conviction brought them substantial returns. In short, a16z participated in all 12 rounds of Databricks' financing, leading four of them. It was precisely because of investment targets like Databricks that a16z's initial AH No. 3 fund performed so well; simultaneously, Databricks was also one of the core drivers of the revenue growth of the larger "late-stage venture capital funds No. 1, 2, and 4".

"First and foremost, they truly care about the company's mission," Ali commented. "I don't think Ben and Marc see this primarily as an investment seeking returns; return on investment is secondary. They are believers in technology and want to change the world through technology."

If you can't understand Ali's assessment of Marc and Ben, you'll never truly understand a16z.

What exactly is a16z?

a16z is not a venture capital fund in the traditional sense. This is obvious on the surface: the fundraising it has completed is the largest venture capital fundraising across all strategies since SoftBank's $98 billion Vision Fund in 2017 and Vision Fund II in 2019[8]. This is completely contrary to the characteristics of traditional venture capital. But even so, SoftBank's Vision Fund is essentially just a "fund", while a16z is not.

Of course, now that a16z has raised capital, it needs to generate returns for its investors. It must excel in this area, and so far, its performance has been outstanding. Not Boring has compiled return data for a16z's funds to date, which we will share below.

But first, we need to clarify: what exactly is a16z?

a16z is a “technology faith community.” Everything it does is aimed at driving the creation of more advanced technologies to build a better future. The company firmly believes[9] that “technology is the glory of human ambition and achievement, the vanguard of progress, and the means of realizing human potential.” All its actions stem from this core belief. It has unwavering confidence in the future and stakes the entire company’s resources on this belief.

a16z is an "institution." It's a business, a company built to achieve scalability and continuously improve itself in the process. I believe that an "institution" possesses many qualities that traditional "funds" lack, which I will explain below. I believe this "institution > fund" positioning precisely resolves the most contradictory point in the venture capital industry's self-perception: this industry provides the most scalable products (funding) to companies with the greatest potential for scalability (tech startups), yet the industry itself is perceived as "not scalable."

This distinction between "institutional investors > funds" originates from David Haber, the general partner (GP) of a16z. He is the most "East Coast financially savvy" member of the team and describes himself as a "learner who studies the business models of investment institutions." He explains, "The objective function (core goal) of a fund is to generate the most incidental returns with the fewest people in the shortest amount of time; while the goal of an institution is to create outstanding returns and build a competitive advantage that generates a compounding effect. Our question is: how can we make the company stronger, not weaker, as it scales?"

a16z is run by engineers and entrepreneurs. The typical approach of traditional asset management managers is to compete for a larger share of a fixed "pie"; while engineers and entrepreneurs make the "pie" itself bigger by building more complete systems and promoting the scaling of those systems.

a16z is a "master of the time domain," an "institution born for the future." In moments of greater ambition, this institution sees itself as equal to the world's top financial institutions and governments. It has stated its goal is to become "the (first) JPMorgan Chase of the information age," but in my view, this statement underestimates its true ambition. If governments serve a "specific spatial scope," then a16z serves "the vast time dimension of the future." Venture capital is simply one way it has found to exert the greatest influence on the future, and this business model best aligns with the logic of "profiting from driving the future."

a16z creates and "sells" influence. It builds its influence through scaling, culture building, networking, organizational structure, and past successes; then it bestows this influence upon the tech startups in its portfolio—primarily through sales support, marketing, recruitment, and government relations. However, in the words of its founders, a16z will "do everything it can to help," and it seems it can do much more than that.

If you were to design an organization that firmly believes that "technology is penetrating markets far beyond the boundaries of traditional technology industries" and that "all fields will eventually become technologized" [10], then what you would ultimately create would be an enterprise that sells "winning capabilities" to thousands of companies that "may form the core of the economy in the future." And I think the organization you would ultimately create would be very similar to a16z.

Because the companies that may form the core of the economy in the future are often small and weak in their early stages. They are initially scattered across various sectors, each with different goals and competitors, and often even competing with each other; at the same time, they also have to face giants who dominate the current market and are unwilling to concede to new entrants. A startup, no matter how bright its prospects, may not be able to recruit top recruiters (and thus fail to attract the best engineers and executives); may not be able to advocate for a level playing field for itself through policy advocacy; may not have enough audience to make its ideas heard; and may lack enough credibility to sell its products to government departments and large corporations that are overwhelmed by sales pitches promising to "bring the next big thing."

It would be illogical for any startup to invest billions of dollars in building these capabilities only to serve itself; however, if these capabilities could be distributed among "all these startups," covering "a future market worth trillions of dollars," then these small companies could suddenly possess the resources of large corporations. Their success or failure would depend solely on the quality of their products, and they could, in a way, drive the future forward.

What would happen if we combined the agility and innovation of a startup with the influence and power of the "time-based rulers"?

This is exactly what a16z has been trying to do—since it was a startup.

Why did Marc and Ben found a16z?

In June 2007, Marc wrote a blog post titled "The Only Thing That Matters"[11], which was part of Pmarca's Startup Guide[12]. On the surface, the article was advice for tech startups, but in retrospect, it was more like an "operation manual for starting a16z". The article answered a question at its core: Of the three core elements of a startup—team, product, and market—which is the most important?

Entrepreneurs and venture capitalists often say "the team is the most important"; engineers, on the other hand, often say "the product is the most important".

"Personally, I support the third view," Marc wrote. "I believe the market is the most important factor in determining the success or failure of a startup."

Why? He explained in the article:

"In a high-quality market—that is, a market with a large number of real potential customers—the market will 'drive' startups to launch products..."

Conversely, in a bad market, even if you have the best product in the world and the most outstanding team, it won't help—you're destined to fail...

In tribute to Andy Rachleff, former partner at Benchmark Capital, I propose the "Rachleff Rules for Startup Success":

The primary reason for the company's failure was the lack of a quality market.

Andy described it this way:

When a top-tier team encounters a terrible market, the market wins.

A bad team encountering a good market, the market wins;

Exceptional achievements are born when top-tier teams encounter high-quality markets.

I think what Marc and Ben saw in the venture capital industry was a “high-quality market” (and nobody realized how high-quality it was at the time), and that the market was full of “bad teams” (and nobody realized how bad they were).

Between 2007 and 2009, Ben and Marc were thinking about what to do next. They were already very successful tech entrepreneurs—despite their success, they still had a burning desire; and it was precisely because of this success that they had the capital to "not have to depend on others" and could take risks without any scruples.

But what exactly needs to be done?

Whether as entrepreneurs or later as angel investors, Marc and Ben have dealt with many unprofessional venture capitalists, and they think, "It might be interesting to compete with these people."

"In my opinion, Marc never did this for the money," David Haber told me. "He was already very wealthy when he was around 20 years old. Initially, he probably did it more to 'show Benchmark or Sequoia Capital what's what.'"

Another characteristic of the venture capital industry, which was almost unnoticed during the worst of the economic recession triggered by the Global Financial Crisis (GFC), is that it may be the best market in the world. And this is crucial for Marc.

Of course, not all venture capital firms are bad. The two firms Marc wanted to "teach a lesson to"—Sequoia Capital and Benchmark—were actually quite excellent (Marc even quoted Andy Rachleff!), but they had a tendency to "remove founders." For founders who wanted to retain control, Peter Thiel founded Founders Fund back in 2005, during the investment period of "Fund 2007 II (FF II)"—as Mario wrote, this fund ultimately achieved a return of $18.60 in cash (DPI, dividend yield on invested capital) for every $1 invested.

However, compared to today, the venture capital industry at that time was still a "lazy, closed, and manual industry".

Marc often tells a story: In 2009, when he and Ben were considering founding a16z, they met with a GP from a top venture capital firm. The GP likened investing in startups to "taking sushi from a conveyor belt." According to Marc, this GP told him:

"The venture capital business is like going to a conveyor belt sushi restaurant. You just sit on Sand Hill Road (the heart of Silicon Valley's venture capital scene), and startups will naturally come to you. Even if you miss one, it doesn't matter, because the next sushi will be served soon. You just sit there, watch the 'sushi' go by, and occasionally reach out and grab a piece."

Marc explained to Jack Altman on the Uncapped podcast, "If the goal is simply to 'maintain the good life,' this approach is viable as long as the industry's ambitions are limited."

But Marc and Ben's ambitions extend far beyond that. For their soon-to-be-founded company, "missing out on a great project"—that is, failing to invest in a great company—would be the biggest mistake. This is no small matter, because they clearly see that as the market expands, the size of those large tech companies will far exceed expectations.

"Ten years ago, there were about 50 million internet users, and even fewer with broadband connections," Ben and Marc wrote in their April 2009 fundraising memo for AH Fund I. "Today, there are about 1.5 billion internet users, many of whom have broadband connections. Therefore, the most successful companies in the industry, both in terms of consumer demand and infrastructure, may have far greater potential than the most successful technology companies of the previous generation."

At the same time, the cost of starting a company has been significantly reduced and the process has become simpler—meaning that more startups will emerge in the future.

In a letter to potential limited partners (LPs), they wrote: "Over the past decade, the cost of developing a new technology product and bringing it to market, at least in beta, has dropped dramatically; today, the cost is typically between $500,000 and $1.5 million, compared to $5 million to $15 million a decade ago."

Finally, as startups transform from "tool providers" into "players directly competing with industry giants," their own ambitions continue to expand—meaning that all industries will eventually become technology industries, and the scale of all industries will become larger as a result.

That's why the "market" was so favorable at that point in time. Marc continued:

From the 1960s to around 2010, the venture capital industry had a fixed "script"... At that time, companies were essentially "tool providers," that is, "companies that sell picks and shovels"—mainframes, desktop computers, smartphones, laptops, internet access software, SaaS (Software as a Service), databases, routers, switches, disk drives, word processing software, these are all tools.

Around 2010, a permanent transformation occurred in the industry… The most successful companies in the technology sector are increasingly those that directly enter traditional industries and compete with existing giants.

In its early days, was a16z "overpricing" the company? Or was the initial pricing actually reasonable relative to its anticipated future potential?

Looking back now, it would be easy to assert that it was the latter; but what is impressive about a16z is that they held this judgment before things even happened.

As they wrote in their article: Every year, about 15 tech companies eventually achieve $100 million in annual revenue, and the market capitalization created by these companies accounts for 97% of the total market capitalization of all companies founded in the same year on the public market—this is the now widely known "Power Law." Given this, they must invest in as many companies as possible that "have the potential to become one of those 15" at all costs; then, among these companies, they must double down and double again on the winners.

To achieve this, two investment partners alone are not enough—a16z must build the company in a way that is “different from all its peers.”

Therefore, after explaining the basic investment terms of the "AH Fund I" (target fundraising size of US$250 million, of which the general partner will contribute US$15 million), Ben and Marc summarized the company's core strategy in one sentence.

AH Fund No. 1 Fundraising Memorandum

Even though the company is now much larger than the "two partners" and its ambitions are no longer limited to "entering the top five in the industry," they are still implementing this strategy.

The three development stages of a16z

Since the inception of its first fund, and throughout the company's development, I believe that a16z's extraordinary belief in the future and its asymmetrical, unwavering commitment have always been its core competitive advantages. It is this differentiated characteristic that has given rise to all other competitive advantages.

As the company's ambitions, resources, fund size, and influence continue to expand, the way it leverages this advantage and achieves differentiation is also constantly evolving.

Phase 1 (2009 - approximately 2017)

In the first phase of a16z (2009 - around 2017), its core insight was that if "software is eating the world," then the value of top software companies would far exceed everyone's valuation expectations at the time.

Based on this belief, a16z took three steps to successfully rise from a newcomer to the top 5 investment firms in the industry:

Paying the High Prices for Deals: As mentioned earlier, some of the deals made by a16z's early-stage funds were considered by many peers to be overpriced or off-track at the time. In the "Acquired" podcast, Ben Gilbert stated, "There was widespread criticism that they were 'buying fame by throwing money at the problem,' squeezing into the ranks of high-quality projects through overpriced investments." However, he also pointed out that this approach was reasonable at the time, and asked rhetorically, "Does anyone today think that any of the projects a16z invested in between 2009 and 2015 were actually overvalued? The answer is absolutely no." As Ben Horowitz explained in a 2014 Harvard Business School (HBS) case study, "Even with valuations of billions of dollars, investors may still underestimate the potential of these companies." And this "underestimation" is precisely where a16z's opportunity lies.

Building operational infrastructure that others considered "wasteful": assembling a full-service team, hiring partners, setting up an executive briefing center… To the fund managers at the time, these measures seemed like "extra expenses" that would drag down costs. But if they firmly believed that the companies in their portfolio could grow into industry benchmarks that "define their category," and that achieving this required enterprise-level strength, then these investments were justified. This move was a strategic layout for the future—in the future, startups must possess the image of "mature companies" to win contracts from Fortune 500 companies.

Viewing tech-savvy founders as a scarce resource was also a gamble—as the cost and barriers to entry for starting a company decreased, tech geniuses, even without traditional management experience, were capable of, and would inevitably be, creating more influential businesses. Therefore, a16z went to great lengths to attract and support such founders, introducing the model of the innovative talent agency CAA to the venture capital industry. Today, "founder-friendly" is a popular industry concept, but at the time, this was undoubtedly a highly innovative approach.

It's worth noting that in the first phase, a16z's core objective is to invest in "the right companies" and realize profits as these companies grow to their expected scale of success. While they will also focus on supporting founders, the essence of this phase is to capitalize on "valuation arbitrage" opportunities.

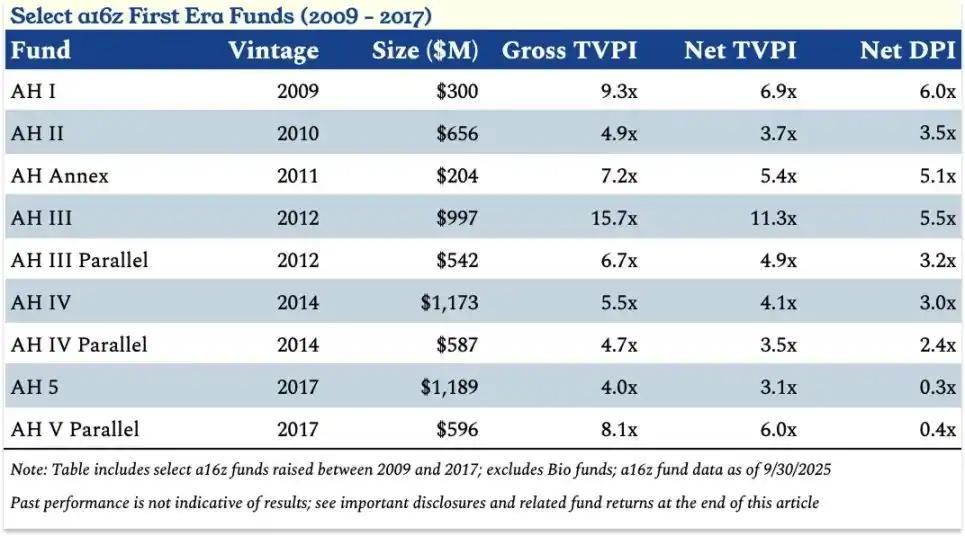

Core data of some funds from a16z during the first phase (2009-2017).

a16z Fund III (AH III) has stood out due to its investments in both Coinbase and Databricks, but its performance is more noteworthy for its "sustainability".

"As limited partners (LPs), we are pleased to see funds consistently achieve a total net value to paid-in capital ratio (TVPI) of 3x, and occasionally more than 5x (net) TVPI, and a16z has done just that," said David Clark, chief investment officer at VenCap (who has been an LP of a16z since its third fund). "a16z is one of the few companies that can consistently deliver this kind of performance on a large scale over a long period of time." This is evident in the performance data mentioned above.

If a16z's willingness to "pay a high price" and "invest across industries like investing in pork futures" at this stage is to build brand reputation and wait for long-term returns, then in the short term, the cost of this "payment" does not seem high.

Phase Two (2018-2024)

In the second phase of a16z (2018-2024), its core belief shifted to: the leading companies will be much larger than anyone expected, they will remain private for longer, and the "devouring" of technology on the industry will be more extensive than others realize.

Based on this belief, a16z took three steps to rise from a "top 5 company" to an industry leader:

Raising Larger Funds: In its first phase, a16z raised $6.2 billion through nine funds; in its second phase over five years, it raised $32.9 billion through 19 funds. The traditional venture capital consensus is that "the larger the fund, the lower the return," but a16z offers the opposite perspective: if the ultimate value of leading companies becomes even higher, then more capital is needed to maintain a meaningful stake across multiple funding rounds. For venture capitalists, the worst-case scenario is "missing out on leading companies" or "under-investing in leading companies." Marc often says, "You can only lose your initial investment (i.e., a 1x loss), but the potential for returns is virtually unlimited."

Breaking away from the "single-fund" model, a16z has achieved a diversified portfolio: In its first phase, a16z primarily raised core funds, while also securing subsequent late-stage funds. Although each general partner (GP) has their own area of expertise, all GPs invest from the same pool of funds. Additionally, a16z has also raised a biotechnology fund—due to the significant differences between the biotechnology sector and other areas. This article will focus on a16z's venture capital funds outside of biotechnology and healthcare.

Entering its second phase, a16z began implementing a "decentralized" strategy: In 2018, under the leadership of Chris Dixon, a16z launched its first fund focused on the cryptocurrency sector, CNK I; in 2019, the company hired David George to lead the establishment of a dedicated Late Stage Ventures (LSV), and raised what was then its largest fund—LSV I, with a size of $2.26 billion, roughly twice the size of any of a16z's previous funds. During this period, a16z raised multiple new funds around its core sectors, cryptocurrencies, biotechnology, and LSV, and also launched a dedicated seed fund in 2021 (AH Seed I, $478 million), a dedicated games fund in 2022 (Games I, $612 million), and its first cross-strategy fund (2022 Fund, $1.4 billion)—this fund allowed LPs to invest proportionally in all funds within the same year.

Importantly, while each fund can leverage the company’s centralized resources (such as the investor relations team), each fund has also established its own dedicated platform team covering areas such as marketing, operations, finance, event planning, and policy research to meet the needs of founders in specific vertical sectors.

Extended holding periods: In the second phase of a16z's development, leading companies began to remain private for longer periods and raise more funds in the private market—including "primary market financing" for company operations and "secondary market transactions" to provide liquidity for employees and early investors. When a16z purchased late-stage secondary market shares of Facebook, Matt Cohler likened this practice to "investing in pork futures," and today, this model has become the norm in the industry—companies such as Stripe, SpaceX, WeWork, and Uber can all obtain liquidity in the private market that was previously only available in the public market.

This trend presents challenges for the industry: limited partners (LPs) face difficulties accessing liquidity, hindering capital allocation cycles. However, for institutions firmly believing in the significant expansion of tech companies (such as a16z), this presents a golden opportunity—it not only provides access to invest more in high-quality private companies but also shifts returns previously held by public market investors to the private market. I believe this shift is one of the key reasons why venture capital firms like a16z have been able to significantly expand their scale without compromising returns.

In response to this trend, a16z took two key steps: first, it became a Registered Investment Advisor (RIA), which allowed it to freely invest in cryptocurrencies, publicly traded stocks, and secondary market transactions; second, under the leadership of David George, it launched the LSV I fund mentioned earlier [9]. In the second phase, of the $32.9 billion raised by a16z, the LSV series funds contributed $14.3 billion. In addition, the cryptocurrency fund was also split up - the fourth cryptocurrency fund (CNK IV) was divided into a seed fund ($1.5 billion) and a late-stage fund ($3 billion).

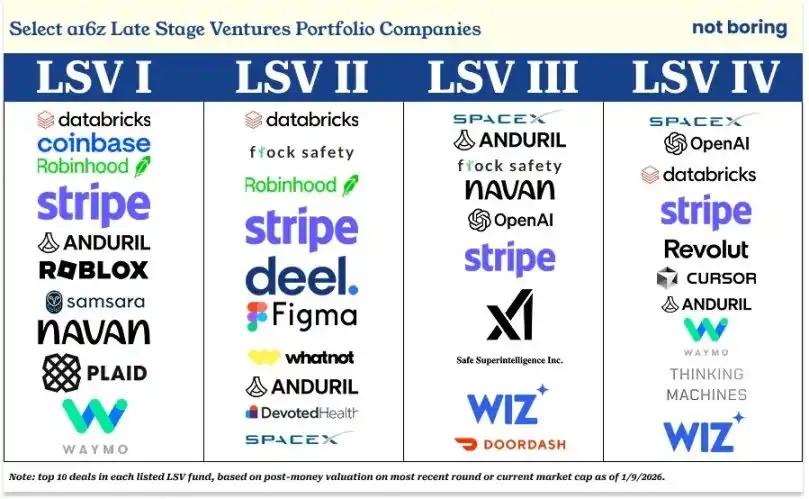

The following are the top 10 investments of each LSV fund, ranked by "valuation after the latest funding round" or "current market capitalization":

LSV I: Coinbase, Roblox, Robinhood, Anduril, Databricks, Navan, Plaid, Stripe, Waymo, Samsara

LSV II: Databricks, Flock Safety, Robinhood (exited from the public market, funds reinvested in Databricks), Stripe, Deel, Figma, WhatNot, Anduril, Devoted Health, SpaceX

LSV III: SpaceX, Anduril, Flock Safety, Navan, OpenAI, Stripe, xAI, Safe Superintelligence, Wiz, DoorDash

LSV IV: SpaceX, Databricks, OpenAI, Stripe, Revolut, Cursor, Anduril, Waymo, Thinking Machine Labs, Wiz

If, as previously accused, a16z's investments were aimed at "riding the coattails of well-known companies," then the aforementioned portfolio is undoubtedly a "high-quality list of trending companies." More importantly, according to Cambridge Academia Sinica's Q2 2025 data, LSV I ranked in the top 5% of its batch of funds, while LSV II and LSV III were both in the top 25% (i.e., the first quartile) of their respective batches.

As of September 30, 2025, LSV I's net TVPI was 3.3x; LSV II's net TVPI was 1.2x (however, this figure may have increased after Databricks and SpaceX recently completed their financing); and LSV III's net TVPI was 1.4x (in addition, reports indicate that SpaceX is about to complete a large-scale secondary market transaction with a valuation of up to $800 billion, more than double the previous valuation, so LSV III's net TVPI is likely to rise further).

Because it firmly believes that the ultimate value of these leading companies will far exceed the expectations of most people (although not everyone—for example, Founders Fund’s assessment of SpaceX and Thrive’s assessment of Stripe are consistent with a16z’s), a16z was able to invest more money in these high-quality private technology companies while they were still private.

The key point is that a16z has proven that, under the right conditions, growth funds can achieve venture capital-level returns. Specifically, according to analysis data I obtained from one of a16z's LPs, if a venture capital firm possesses strong early-stage investment capabilities, by continuously adding investments during the growth phase, it can not only achieve venture capital-level returns (multiples) but also obtain a higher internal rate of return (IRR). Of course, establishing deeper partnerships with these firms can further enhance a16z's industry influence.

In the second phase, a16z believes the most important goal is to "hold as many shares as possible in leading companies"—this goal is easier to achieve if one can gain a deep understanding of the company through early-stage investments and continue to invest with specialized late-stage funds (or make up for mistakes in early-stage investments) (although its shareholding ratio still does not reach the "controlling" level common in other asset classes).

The core of this phase remains "arbitrage," but unlike the first phase, a16z is putting more effort into helping individual portfolio companies succeed in this phase.

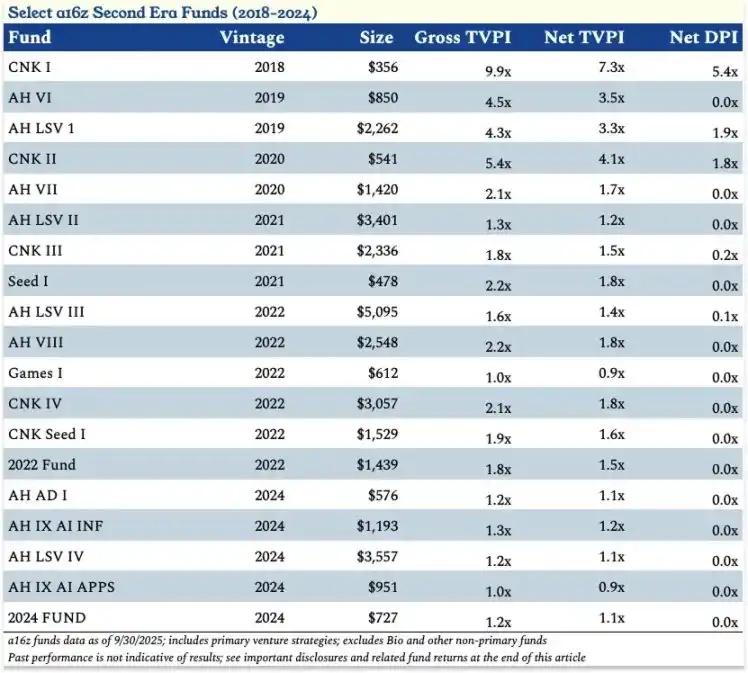

Although the return cycle of the second-stage fund has not yet fully ended, its returns are currently leading compared to the first-stage fund during the same period (when the Wall Street Journal reported its poor performance).

Investment return comparison between a16z Fund and Cambridge Association industry benchmark

Specifically: the net TVPI of funds raised in 2018 was 7.3 times; in 2019 it was 3.4 times; in 2020 it was 2.4 times; in 2021 it was 1.4 times; and in 2022 it was 1.5 times.

Core performance data of some funds from a16z during 2018-2024 (Phase II).

The most noteworthy highlight of this phase is the outstanding performance of the cryptocurrency funds (CNK 1-4 and CNK Seed 1) – CNK I has already delivered a 5.4x net distribution to paid-in capital ratio (DPI) return to LPs.

Even more surprisingly, despite some questioning whether a16z "chose the wrong time and raised too many cryptocurrency funds" in 2022, its $3 billion raised for its fourth cryptocurrency fund (CNK IV) has already achieved a net TVPI of 1.8 times.

The two core stories of the second phase—the LSV series fund and the cryptocurrency fund—perfectly embody a16z's two beliefs about the future: LSV is a response to the trend of "longer corporate privatization cycles and increased demand for private market financing"; while cryptocurrency represents a concept—innovation (and returns) may come from entirely new fields completely different from traditional investment tracks.

These two stories also highlight the need for a16z to further expand its services—both supporting portfolio companies and empowering the entire industry. For example, to help late-stage portfolio companies grow, a16z needs to replicate some of its public market advantages in the private market; and to ensure the survival of the cryptocurrency industry in the United States and to ensure that various new technology companies have a level playing field with established giants, a16z must venture into Washington (to lobby for policies).

This leads to a16z's third phase (2024 - Future). In this phase, its core belief is that, given a level playing field, new technology companies can not only reshape industries but also succeed in all industries; and a16z must lead industries and even the entire nation in the right direction.

This belief has once again shifted a16z's positioning. When a company reaches a certain threshold (the $15 billion new fund raised this time is a clear indicator), "picking winners" is no longer enough—

To create winners, you must create an environment that is conducive to their competition.

As Ben put it, "It's time to lead the industry."

a16z's third phase: It's time to lead the industry.

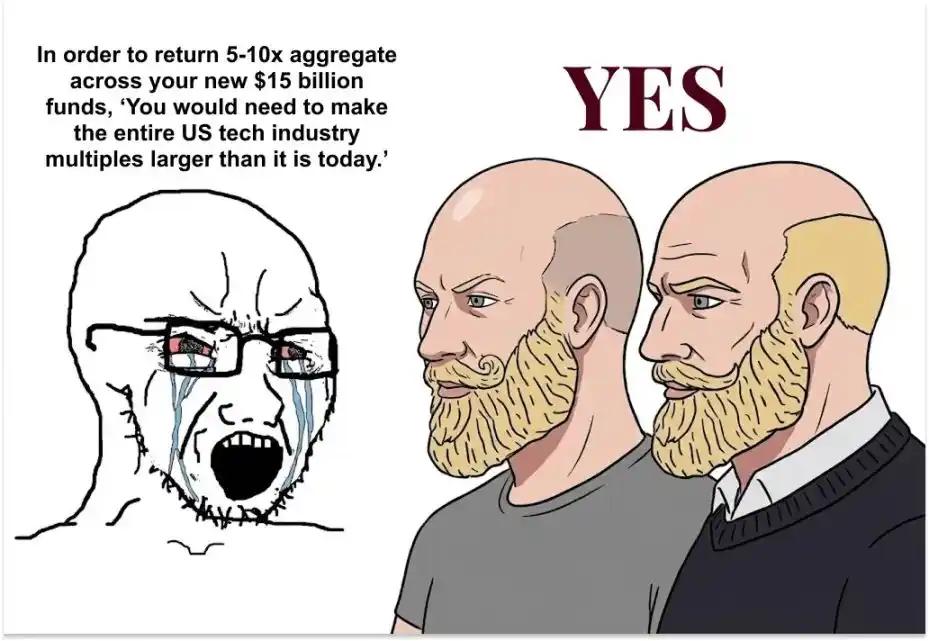

At this moment, you might imagine this scenario: an analyst from a rival venture capital firm messages journalist Tad Friend, saying, "To achieve a combined 5-10x return on these two new $15 billion funds, 'you'd have to expand the entire U.S. tech industry several times over.'"

And as you can probably guess, Marc and Ben would respond like this: Yes, that's exactly what we're planning.

This is precisely the plan explicitly proposed by a16z, and its logic is as follows:

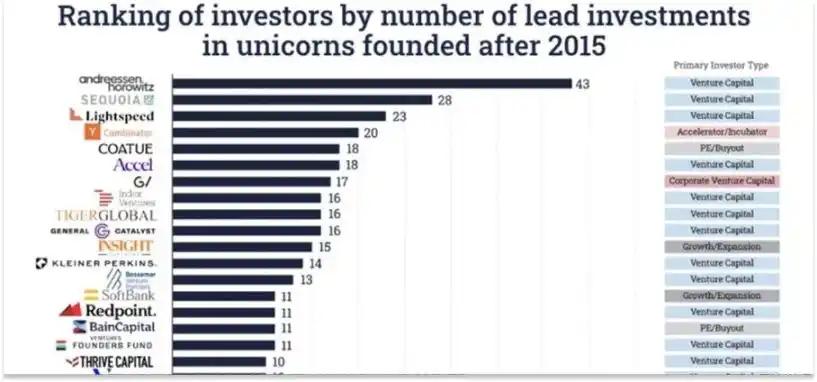

Since 2015, a16z has invested in more unicorn companies at an early stage than any other investor, and the gap between it and the second-ranked investor (Sequoia Capital) is comparable to the gap between the second and twelfth ranked investors.

Data source: Stanford University Professor Ilya Strebulaev

Clearly, the number of early-stage investments that grow into unicorns is a very specific and convenient metric for measuring the "best investors." A more common evaluation method is to consider returns—whether it's multiple returns, internal rate of return (IRR), or simply the total amount of cash distributed to limited partners (LPs). Some also focus on investment success rate or performance stability. There are many ways to rank venture capital firms, and the perspectives vary.

However, this evaluation criterion centered on the "number of unicorns" seems highly consistent with a16z's perspective on the industry. During discussions with the a16z cryptocurrency team, I repeatedly heard this viewpoint: if you bet on a sector simply because many excellent entrepreneurs are investing in it, even if you ultimately misjudge, it's perfectly acceptable; but if you choose the wrong investment company within a sector, or miss out on the ultimate leader for any reason, that's unacceptable. As Ben said:

"We are well aware that starting a business is extremely risky. Therefore, as long as we follow the correct procedures when investing and make reasonable risk assessments, we will not be overly concerned even if some investments ultimately fail. On the contrary, we will pay close attention if we are unable to accurately determine whether an entrepreneur is the best candidate in their field."

Choosing the wrong emerging field isn't a big problem; choosing the wrong entrepreneur is a serious issue; missing out on an excellent entrepreneur is equally problematic. Whether due to a conflict of interest or a voluntary withdrawal, missing out on a company with epochal significance has far more serious consequences than investing in the best entrepreneur in a misjudged field.

Based on a16z's own defined "core metrics," it has become a leader in the venture capital industry.

"So, what's the next step?" Ben asked. "What exactly does it mean to lead an industry?"

In a lengthy statement announcing the $15 billion funding round for Platform X, he provided the answer: "As a leader in the U.S. venture capital industry, the future of new technologies in the U.S. is, to a certain extent, in our hands. Our mission is to ensure that the U.S. wins technological dominance for the next 100 years."

It's extremely rare for a venture capital firm to say something like that.

However, if you agree with the following premises—that technology is the engine of progress, that the United States must have a technological advantage to maintain its leading position, and that A16Z is the largest and most influential investor in emerging American technology companies and has the ability and resources to provide these companies with a fair chance to compete with industry giants—then this statement is not entirely without merit.

He further pointed out that to win technological dominance over the next 100 years (which, in a16z's view, is equivalent to winning overall leadership over the next 100 years), it is necessary to master key new technological architectures—AI and cryptocurrencies—and apply these technologies to the most important areas, such as biotechnology, defense, healthcare, public safety, and education, and even integrate them into the government operating system.

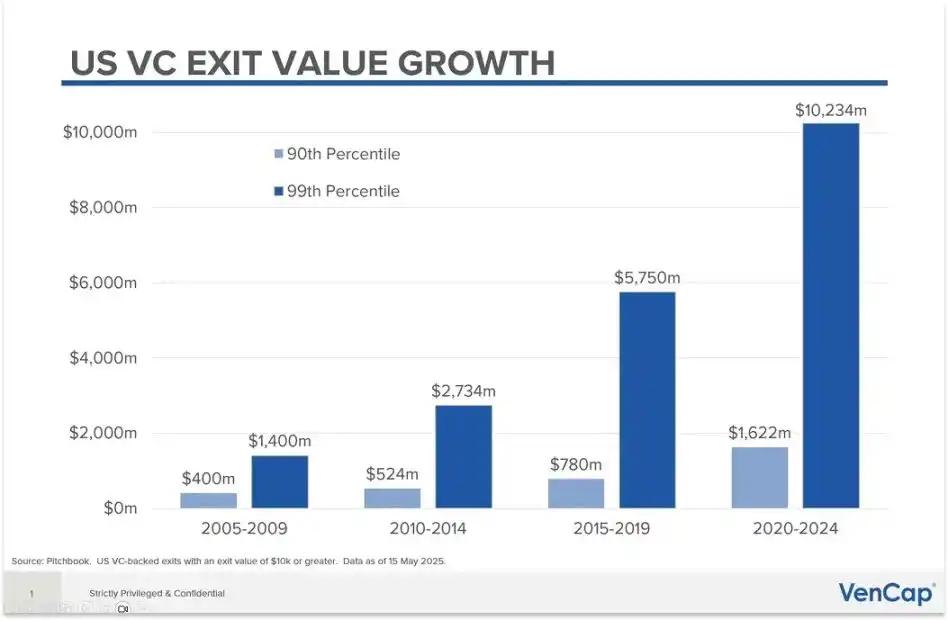

These technologies will dramatically expand the market size. As I discussed in my articles "The Tech Sector Will Expand Significantly" and "Everything Can Be Technologically Adapted," industries and tasks previously outside the scope of the tech sector are now included. This means that venture capital investable value (VCAV) will also increase significantly.

US venture capital exits are growing significantly. (Chart source: David Clark, Chief Investment Officer, VenCap)

This is a continuation of a16z's long-standing investment strategy, but with a key shift in philosophy: as long as a16z fulfills its role as a leader, these values can be realized, and the future of the United States (and even the world) can be secured.

Specifically, this means doing five things:

1. Reshape U.S. technology policy to bring it back to its former glory;

2. To fill the gap between the development of private enterprises and listed companies;

3. Drive the evolution of marketing models towards the future;

4. Embrace new business models;

5. While improving our own capabilities, we continuously shape the corporate culture.

Those seemingly perplexing measures by a16z are almost all aimed at achieving these five goals.

Most notably, a16z has become increasingly vocal in the political arena over the past two years, with Marc and Ben publicly endorsing President Trump in the last election. This move has drawn criticism from many, with some arguing that venture capital funds should not interfere in national politics.

But a16z would vehemently oppose this view. It hopes to "reshape U.S. technology policy and bring it back to its former glory."

Marc and Ben articulated their position in the "Small Technology Business Agenda," the core points of which can be summarized as follows:

Emerging technology companies are crucial to national development.

To win the future, we need a legal, policy, and regulatory system that fosters innovation, while also preventing well-funded industry giants from hindering competition through "regulatory capture."

However, the reality is quite the opposite: "We believe that poor government policies have become the number one threat facing small technology companies."

Currently, no one is speaking up for emerging technology companies at the government level or in the process of confronting industry giants: industry giants will not do this, and startups should not devote their limited resources to such matters.

Venture capital firms’ financial returns are closely linked to the success of emerging technology companies, so the venture capital industry should take the lead in this regard; and as a leader in the venture capital industry, a16z has an even greater responsibility.

a16z is "single-issue oriented" in its political stance, focusing only on the development of small technology companies and adhering to the principle of bipartisanship.

Their public stance includes: "We will not participate in political controversies that are not directly related to small tech companies" and "Our support or opposition to a politician depends solely on their attitude toward small tech companies, regardless of their political party affiliation or their stance on other issues"—based on what I've seen and heard on a16z, these are not empty slogans, but their actual code of conduct.

a16z's foray into politics isn't out of amusement (although Marc at least seems to enjoy the "excitement"; he seems passionate about many things and can find humor in the absurd—an underrated competitive advantage, but we don't have time to discuss that today). In the short term, a16z is willing to endure criticism and accusations of "seeming foolishness" simply to ensure the long-term flourishing of emerging technologies.

As Bill Gurley, a former partner at Benchmark, pointed out in his article "2581 Miles," for a long time, the tech industry could largely ignore Washington (referring to the US government), and Washington could largely ignore the tech industry. But a few years ago, things changed, partly for reasons I mentioned earlier—the tech industry's focus shifted from "building tools" to "competing with industry giants." The cryptocurrency industry is the first sector to face "life-or-death" regulatory pressure.

When a16z first ventured into Washington's political circles, "small tech companies" had not yet formed an influential group. Large tech companies had dedicated lobbying teams and government relations networks; industry giants—whether banks, defense companies, or leaders in other sectors—also had their own lobbying resources and connections. But small tech companies, including cryptocurrency firms, lacked this support. At the time, apart from Coinbase, no small tech company could afford the costs and groundwork required to establish representation in Washington (and even in state legislatures across the country).

Therefore, in October 2022, the a16z cryptocurrency team hired Collin McCune as Head of Government Affairs to lead efforts to educate U.S. politicians about cryptocurrency. Collin, Chris Dixon, Miles Jennings, General Counsel for Cryptocurrency at a16z, other team members, and entrepreneurs from a16z's portfolio and the cryptocurrency industry traveled to Washington multiple times to explain to politicians how cryptocurrencies work, their development potential, and, more importantly, the risk that