In discussions about stablecoins, a common assessment is that as stablecoins are increasingly used in transfers and settlements, the importance of traditional payment tools will gradually decline.

However, in its recent report, "Stablecoin Payments at Scale: How Cards Bridge Digital Assets and Global Commerce," Artemis offers a more pragmatic observation on the actual use of stablecoins: while stablecoins have been widely adopted in asset storage and value transfer, their implementation in real-world consumption still heavily relies on existing payment networks.

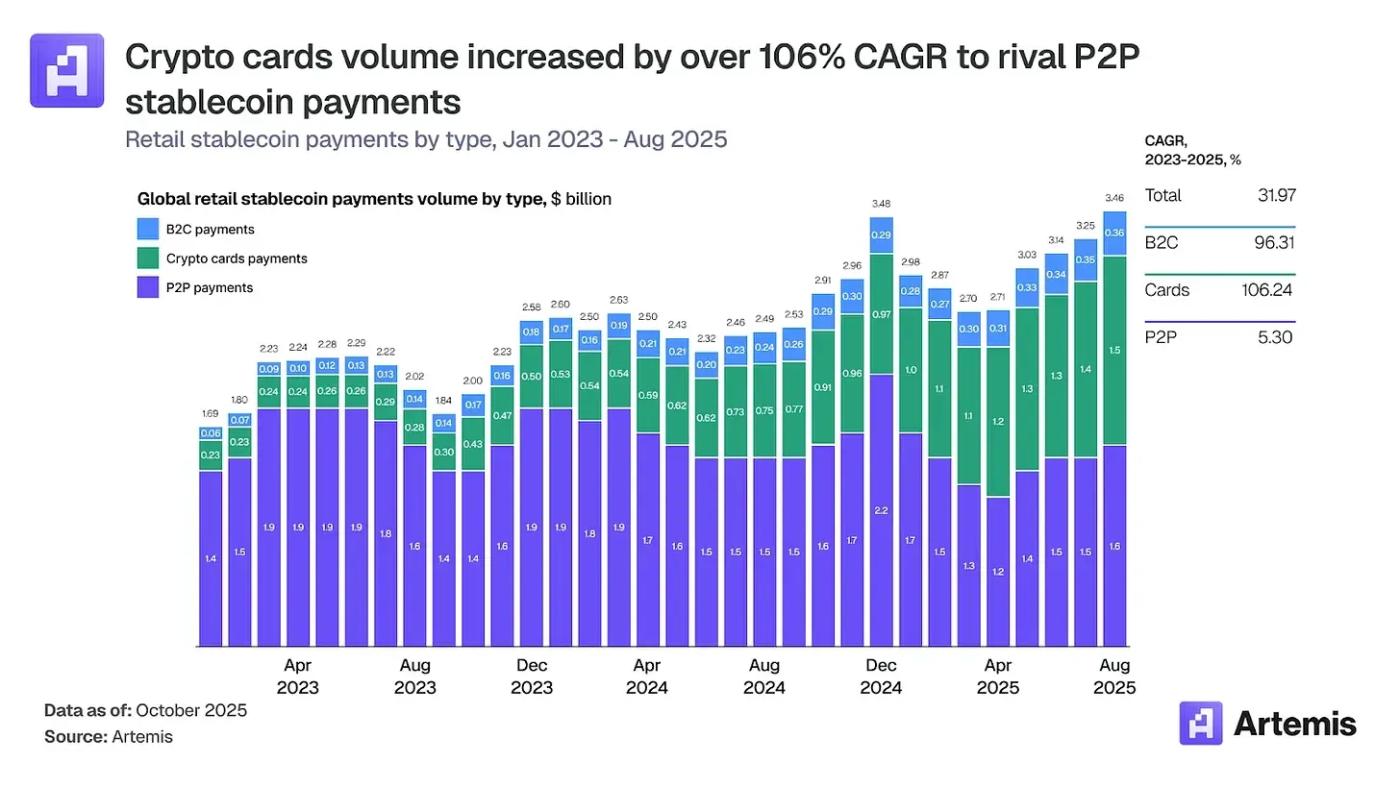

Data shows that the crypto card market has jumped from the fringes at the beginning of 2023 to a behemoth with an annualized value of $18 billion, and monthly transaction volume has increased 15 times in just two years.

This means that stablecoins have solved the problem of how funds can move efficiently, but a viable connection is still needed regarding how these funds can be accepted in the real world. Under current industry conditions, crypto cards are one of the most mature and scalable carriers of this connection.

1. Why an encrypted card, instead of native encrypted payment?

On the surface, stablecoins seem to possess all the technological requirements for a means of payment—on-chain settlement, programmability, and high efficiency. However, in the real world, payment is not merely a technological act; it also involves:

Merchant-side acquiring and clearing system

Compliance, responsibility and risk control boundaries

Compatibility with existing acquiring and clearing systems

This is why, in Artemis' analysis of stablecoin use cases, a structural characteristic can be clearly seen: the large-scale use of stablecoins is mainly concentrated in the transfer and settlement layer, rather than the consumption layer directly facing merchants.

This structural distribution does not mean that stablecoins cannot be used for consumption, but rather reflects that for stablecoins to enter real-world consumption scenarios, they must rely on mature, compliant, and scalable crypto payment infrastructure as a prerequisite.

Meanwhile, the market is actively seeking feasible paths to integrate stablecoins into real-world consumption scenarios. Crypto cards, with their scalability and flexibility, have become an effective way to connect traditional and digital payment systems. They can support payment pathways for digital assets such as stablecoins, as well as fiat currency-based consumption and settlement capabilities. Market acceptance is reflected in the data: crypto card transaction volume grew from approximately $100 million per month in early 2023 to over $1.5 billion by the end of 2025.

II. The True Role of Encrypted Cards: Embedded in the Existing Payment System

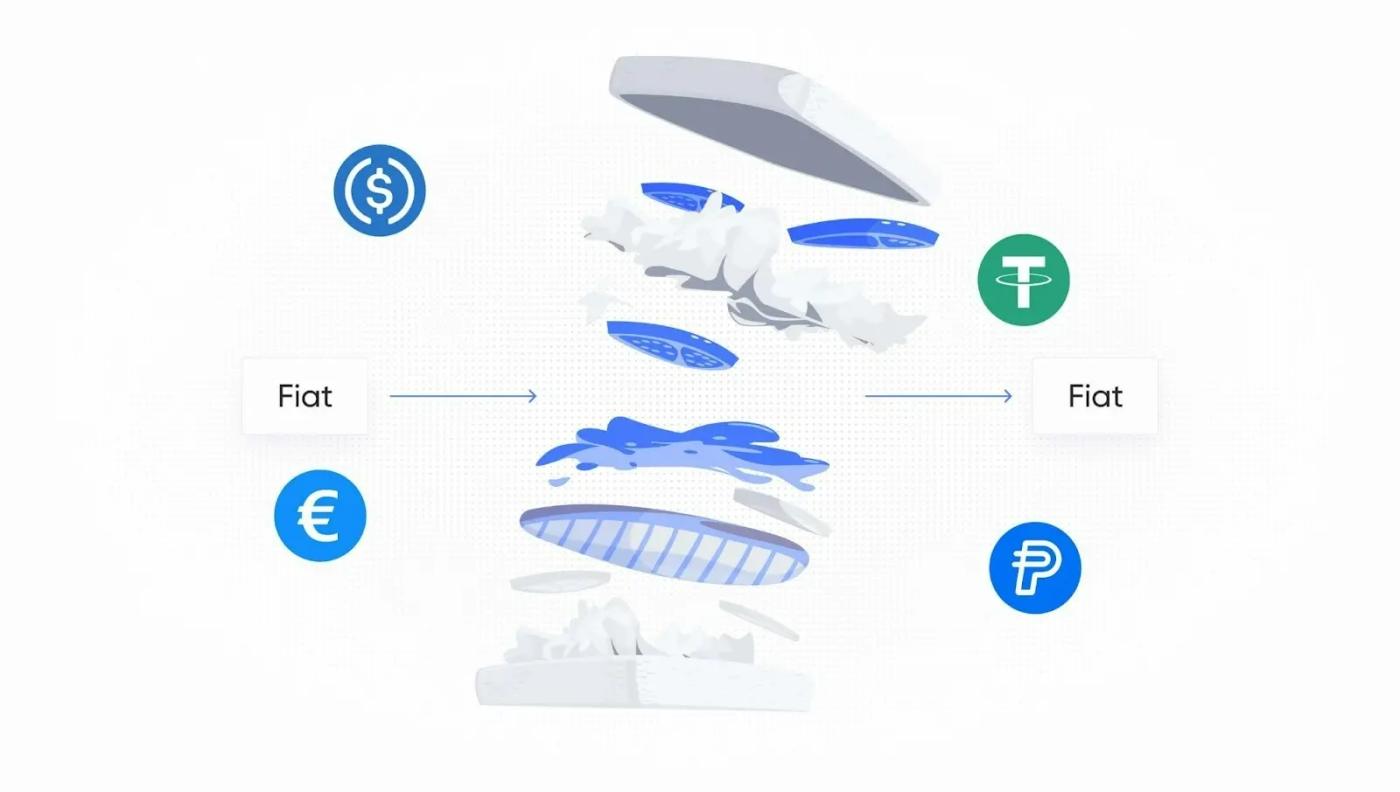

Crypto cards, serving as a bridge between crypto assets and fiat currency, can be understood using a "sandwich structure":

The upper and lower layers remain the fiat currency system and existing payment networks.

Stablecoins occupy the middle, playing a role in value transfer and settlement.

Users and merchants may not be directly aware of the existence of stablecoins.

In this structure, the consumer side needs an interface that is widely accepted in the real world, and the crypto card is a key component that plays this role. Under this structure, the crypto card is not a replacement for stablecoins, but rather an interface layer design:

Internally, it connects stablecoin liquidity pools with corporate accounts.

Externally, it connects to established payment networks such as Visa and Mastercard.

The middle layer is constrained by compliance, risk control, and clearing systems.

This allows stablecoins to be used for real-world consumption and spending without changing merchants' payment methods or requiring users to understand on-chain details. From this perspective, the value of crypto cards lies not in whether the payment experience is native enough, but in whether it closely resembles the operating logic of real-world payment systems .

III. In enterprise scenarios, the demand for encryption cards is becoming clearer.

Before being widely adopted in consumer scenarios, stablecoins were already more readily accepted by businesses due to their efficient settlement and low-friction characteristics. Examples include using stablecoins to pay for overseas advertising, cloud services, and software subscriptions; settling payments with global suppliers or partners; and managing expenses across teams and regions. A common example is a SaaS company that accepts stablecoin subscription fees but still uses traditional payment tools to pay for Google Ads and AWS.

These scenarios are highly standardized and heavily reliant on existing payment networks. Under these conditions, crypto cards become a viable option: they provide businesses with a compliant, low-friction, and scalable spending outlet for stablecoins .

However, in practice, the encryption card is not an isolated tool; it also needs to be connected to the company's funds and financial systems.

Taking Interlace's practice as an example, its encrypted card product, Infinity Card, more accurately assumes the role of the expenditure layer in a company's financial system. By directly connecting a company's multi-currency accounts and asset balances, it completes the conversion and settlement of encrypted assets and fiat currency in the background, enabling corporate funds to be seamlessly used in global consumption scenarios without changing the original account structure and settlement logic.

Structurally, these enterprise-oriented encrypted cards have several distinct advantages:

The card is directly linked to the corporate account, reducing the operational costs associated with repeated top-ups, manual transfers, and multi-level clearing.

It supports both fiat currency and crypto assets as sources of expenditure, with the system automatically handling the exchange and processing during consumption;

A multi-user, multi-permission expenditure management mechanism designed for internal enterprise use scenarios, supporting limit control, role differentiation, and unified management.

Another noteworthy change is that more and more enterprises are no longer satisfied with simply using a card; they want to integrate the encryption card's capabilities into their own products or platforms as part of the user experience and business processes. This has driven the gradual formation of Card as a Service (CaaS) in the encryption card field. Under the CaaS model, enterprises can:

Issue virtual or physical cards via API, embedding card issuance capabilities into your own system;

Customize card usage scenarios, transaction limits, and other rules;

The encryption card is integrated into its business, rather than being a separate third-party product.

Within Interlace's ecosystem, encrypted card CaaS capabilities are abstracted into underlying modules, including card issuance, compliance and risk control, clearing and settlement, and other components. Enterprises can build card products tailored to their specific business needs on this foundation. This shift essentially reflects a trend: encrypted cards are transforming from user-facing tools into system-facing capabilities—what we commonly refer to as the infrastructure layer.

Conclusion

From Artemis' report, we gained an important insight: the growth in the size of stablecoins does not automatically mean that they have entered every corner of the real world.

For the foreseeable future, crypto cards will remain one of the most mature and scalable ways to connect stablecoins with real-world consumer networks. Their value lies not in how native their narrative is, but in how closely they align with the operating logic of the real world—and this is precisely where payment infrastructure truly shines.