As the market enters a downtrend, skepticism about the crypto market is growing. Are we entering a crypto winter?

Key Takeaways

Crypto Winter is a series of major incidents, a collapse in trust, and an exodus of talent.

In the past, winter was an internal issue in the industry, but now, both the rise and fall are driven by external factors, so it is neither winter nor spring.

After regulation, the market is divided into three tiers: regulated, non-regulated, and shared infrastructure, and the trickle-down effect of altcoins rising when Bitcoin rises, as in the past, is gone.

ETF funds remain in Bitcoin and do not flow outside of regulatory boundaries.

The next surge will require killer use cases and a conducive macroeconomic environment.

1. How did Crypto Winter come about?

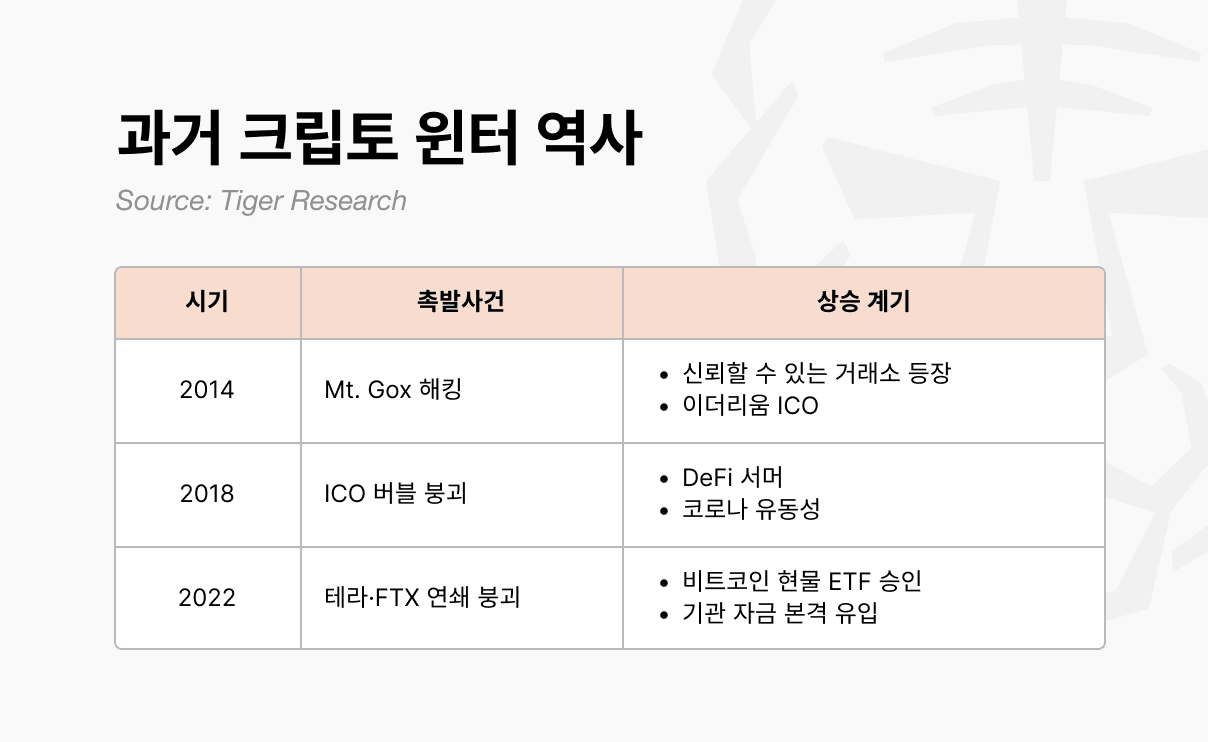

The first winter came in 2014. Mt. Gox, then an exchange handling 70% of global Bitcoin trading volume, was hacked, losing approximately 850,000 BTC, eroding market confidence. New exchanges with internal controls and auditing capabilities emerged, rebuilding trust. Ethereum's initial coin offering (ICO) also opened up new possibilities for visionary and fundraising methods.

This ICO sparked the next wave of volatility. Anyone could issue tokens and raise funds, fueling a frenzy in 2017. Projects raised hundreds of billions of won with a single white paper, but most lacked substance. The bubble burst in 2018 as South Korea, China, and the United States imposed a barrage of regulations, ushering in a second winter. This winter didn't end until 2020. The post-COVID liquidity surge, and DeFi protocols like Uniswap, Compound, and Aave gained traction, leading to a resurgence of funds.

The third winter was the most severe. Following the collapse of Terra-Luna in 2022, Celsius, Three Arrows Capital, and FTX went bankrupt in quick succession. This wasn't simply a price drop; the very structure of the industry was shaken. In January 2024, the US SEC approved a Bitcoin spot ETF, followed by the Bitcoin halving and Trump's pro-crypto policies, leading to a renewed influx of funds.

All three winters followed the same pattern: a major incident, a breakdown in trust, and the departure of talented individuals.

It always starts with a major event: the Mt. Gox hack, ICO regulations, the Terra-Luna collapse, and the FTX bankruptcy. The scale and form of these events varied, but the outcome was the same: the entire market was shocked.

The shock soon spread to a breakdown in trust. People discussing what to build next began questioning whether crypto was truly a meaningful technology. The collaborative atmosphere among builders disappeared, and they began blaming each other for the problems.

Doubt leads to talent exodus. Builders who were creating new dynamics in blockchain, succumbing to skepticism, left for fintech and big tech in 2014, and then to institutions and AI in 2018—searching for seemingly more certain places.

Even now, we see patterns that have been seen in past crypto winters.

But it's hard to call this a crypto winter. Previous winters erupted within the industry. Mt. Gox was hacked, numerous ICO projects were exposed as frauds, and FTX collapsed. The industry itself lost trust. This time, things are different. ETF approvals triggered a bull market, while tariff policies and interest rates drove the decline. External factors drove the upswing, and external factors drove the downswing.

Builders haven't left either. RWA, perpDEX, prediction markets, InfoFi, privacy. New narratives have emerged, and are still being created. While they haven't driven the entire market like DeFi did in the past, they haven't disappeared. The industry hasn't collapsed; the external environment has changed.

Since we didn't create spring, there is no winter.

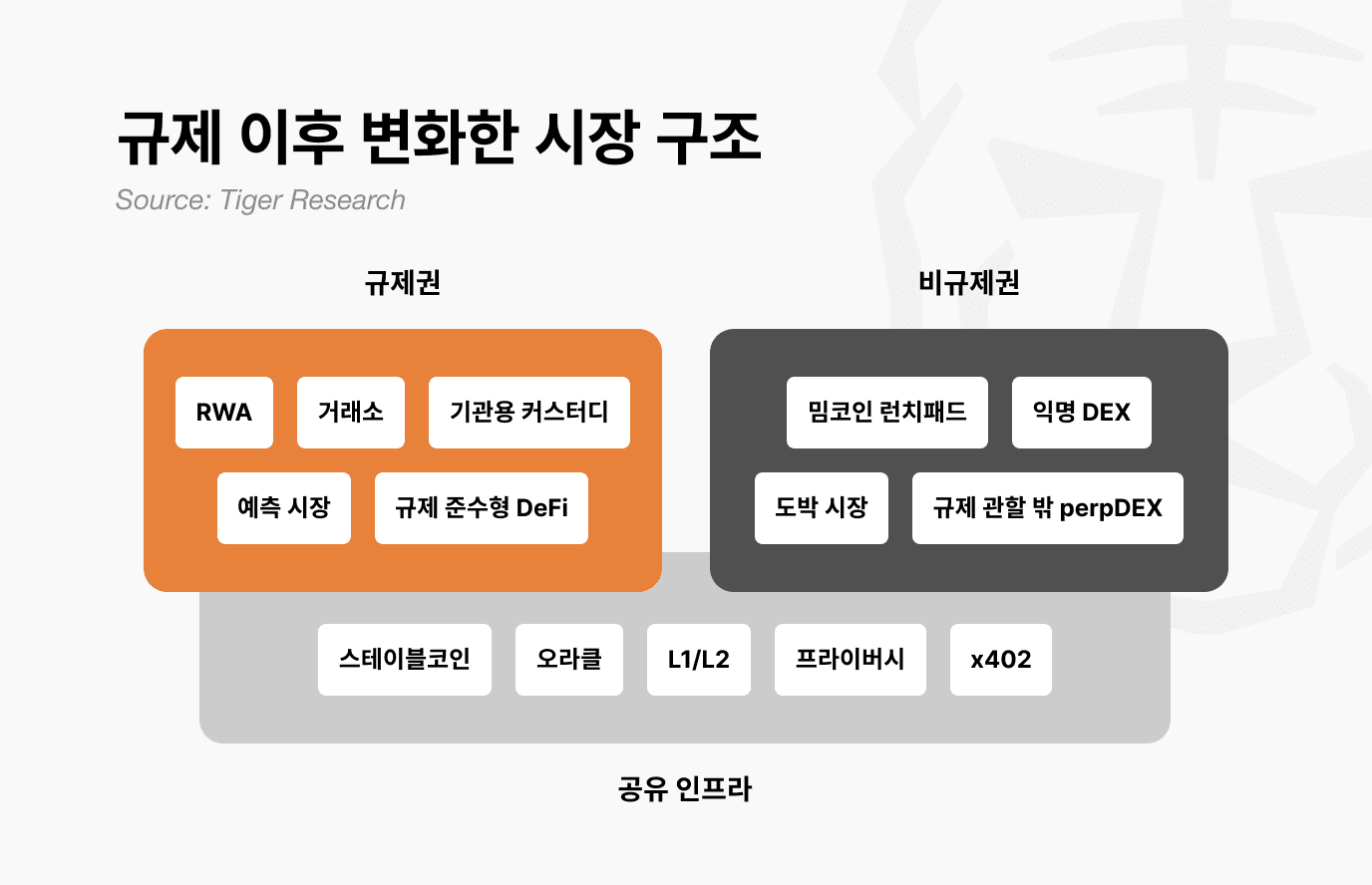

This is due to significant changes in the market structure following regulation. The market is already broadly divided into three tiers: 1) regulated, 2) non-regulated, and 3) shared infrastructure.

Regulated areas include RWA tokenization, exchanges, institutional custody, prediction markets, and regulated DeFi. These areas undergo audits, are subject to disclosure, and enjoy legal protection. Growth is slow, but the capital base is large and stable. However, once regulated, explosive growth like in the past is unlikely. Volatility is reduced, and upside is limited. However, downside is also limited.

On the other hand, the non-regulated sector will likely become more gambling-like in the future. Examples include Memecoin Launchpad, anonymous DEXs, and perpDEX, which operates outside of regulatory jurisdiction. Barriers to entry are low and speed is high. A 100x increase one day and a 90% decrease the next occur more frequently. However, this area is not insignificant. Industries that emerge in the non-regulated sector are creative and, once proven, will migrate to the regulatory sector. DeFi did this, and prediction markets are following suit. They serve as a testing ground. However, the non-regulated sector itself will increasingly become separate from regulated businesses.

Shared infrastructure includes stablecoins and oracles. They are used in both regulated and non-regulated environments. The same USDC is used for institutional RWA payments and Pump.fun transactions. Oracles also provide data for tokenized government bond verification and anonymous DEX settlement.

In other words, as markets diverged, the flow of funds also changed. In the past, a rise in Bitcoin would trickle down to altcoins. Things are different now. Institutional funds flowing into ETFs stayed in Bitcoin and ended there. Regulated funds don't flow into unregulated markets. Liquidity remains only in areas with proven value. And even Bitcoin has yet to prove its value as a safe haven asset versus risky assets.

Regulations are already being finalized, and builders are continuing to build. So, that leaves two options.

First, a new killer use case must emerge from the non-regulated space. Like the DeFi Summer of 2020, this is something that creates unprecedented value. While narratives like AI agents, InfoFi, and on-chain social are promising, they're not yet at a market-shaping scale. A new trend must emerge, with experiments in the non-regulated space being validated and transitioning to the regulated space. DeFi has done this, and prediction markets are already doing it.

Second, the macroeconomic environment. Even if regulations are streamlined, developers build, and infrastructure is built, growth will be limited if the macroeconomic environment is not supportive. The 2020 DeFi summer exploded as liquidity was released after the COVID-19 pandemic. The rise following ETF approval in 2024 also coincided with expectations of interest rate cuts. No matter how well the crypto industry performs, interest rates and liquidity cannot be controlled. For the industry's efforts to be persuasive, the macroeconomic environment must change.

The "crypto season" of the past, where everything rose together, is unlikely to return. This is because the market is fragmented. Regulatory power steadily grows, while non-regulated power experiences significant ups and downs.

The next rise is coming, but it won't come to everyone.

이번 리서치와 관련된 더 많은 자료를 읽어보세요.

Disclaimer

This report has been prepared based on reliable sources. However, we make no express or implied warranties as to the accuracy, completeness, or suitability of the information. We are not responsible for any losses resulting from the use of this report or its contents. The conclusions, recommendations, projections, estimates, forecasts, objectives, opinions, and views contained in this report are based on information current at the time of preparation and are subject to change without notice. They may also differ from or be inconsistent with the opinions of other individuals or organizations. This report has been prepared for informational purposes only and should not be construed as legal, business, investment, or tax advice. Furthermore, any reference to securities or digital assets is for illustrative purposes only and does not constitute investment advice or an offer to provide investment advisory services. This material is not intended for investors or potential investors.

Tiger Search Report Usage Guide

Tigersearch supports fair use in its reports. This principle allows for the broad use of content for public interest purposes, provided it does not affect commercial value. Under fair use rules, reports may be used without prior permission. However, when citing Tigersearch reports, 1) "Tigersearch" must be clearly cited as the source, and 2) the Tigersearch logo must be included. Reproducing and publishing materials requires separate agreement. Unauthorized use may result in legal action.