Authors: TaxDAO, WolfDAO

Original link: https://mp.weixin.qq.com/s/Sp5CKlFiC5W3aWQePwwWUQ

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objection to the reprint format, please contact us and we will modify it according to the author's request. This reprint is for information sharing only and does not constitute any investment advice, nor does it represent Wu Blockchain views or positions.

As more and more traditional financial institutions and even non-financial institutions begin to engage in private crypto fund business and allocate crypto-related assets, the compliant operation of private crypto funds has become increasingly important. This article will summarize the types and characteristics of crypto funds with different strategy attributes, trading methods, and funding sources, as well as the macro-regulatory situation of private crypto funds. Using compliant fund operation case studies, it will introduce the operational process of private crypto fund business and the key elements for compliant operation of private crypto funds.

1. Definition and Classification of Private Crypto Funds

1.1 What is a private crypto fund?

1.1.1 Definition and Characteristics of Private Crypto Funds

In a broad sense, a fund refers to a certain amount of capital established for a specific purpose. This mainly includes trust investment funds, provident funds, insurance funds, retirement funds, and funds from various foundations. A common characteristic is that they are centrally managed by specialized asset managers to generate higher investment returns. These funds can be invested in the primary market (venture capital, private equity) and the secondary market.

A private crypto fund is a non-publicly offered investment fund primarily targeting institutional and individual investors with sufficient wealth and risk tolerance. It focuses on investing in crypto assets and related projects, and its holdings may include crypto assets, crypto options and futures, crypto company stocks, RWA assets, etc. This fund combines the characteristics of private equity funds with the unique features of crypto assets, and its distinguishing features from other private equity funds can be summarized as follows:

① Specific investment scope: Private crypto funds focus on the crypto asset market, including digital currencies, blockchain projects, decentralized finance (DeFi) applications, etc.

② High Value Volatility: The value volatility of crypto assets far exceeds that of traditional financial assets. The valuation of unsecured crypto assets (such as most cryptocurrencies) is primarily based on speculative demand, resulting in extremely high price fluctuations. This high volatility presents investors with potential for high returns, but it also increases investment risk.

③ Significant Differences in Regulatory Attitudes Across Countries: Different countries exhibit substantial differences in their regulatory attitudes towards crypto assets. For example, the US regulatory policy on cryptocurrencies is relatively vague and constantly evolving, while Japan legalized Bitcoin and brought it under its regulatory purview earlier. Private equity crypto fund managers need to closely monitor changes in regulatory policies in various countries to adjust their investment strategies and mitigate compliance risks.

④ Low transparency: Private equity funds inherently possess low transparency, and the anonymity and decentralization of the crypto asset market further exacerbate this lack of transparency. Therefore, private crypto funds need to establish sound information disclosure systems and investor protection mechanisms.

1.1.2 Differences between private crypto funds and traditional private funds

Private crypto funds and regular private funds are similar in many ways, but there are some key differences due to their different investment targets and market environments.

(1) Investment target

Private crypto funds: These focus on cryptocurrencies, blockchain technology, and related digital assets. They may invest directly in cryptocurrencies (such as Bitcoin and Ethereum), or in blockchain startups, tokenized assets, and other projects related to the blockchain ecosystem.

Typical private equity funds typically invest in assets in traditional financial markets, such as stocks, bonds, real estate, private equity, or other traditional asset classes. While their investment targets are more diversified, they are all based on the traditional economic system.

(2) Risk and volatility

Private Crypto Funds: The cryptocurrency market is highly volatile and faces significant risks, including market volatility, technological risks (such as hacking), regulatory risks (different countries have vastly different attitudes toward regulation and policies may change constantly), and liquidity risks (some tokens or crypto assets may be difficult to liquidate quickly).

Traditional private equity funds: While still facing market volatility, changes in the economic environment, and specific industry risks, these risks are generally more manageable and have more abundant historical data. The investment targets of traditional private equity funds typically have a longer market history and a clearer regulatory framework.

(3) Regulatory environment

Private crypto funds: Limited by the regulatory environment of the cryptocurrency market, they may face greater uncertainty. Different countries have different regulatory policies regarding cryptocurrencies and related assets, which could affect the fund's operations and investment strategies.

Typical private equity funds are generally subject to strict financial regulation and laws and regulations, with clear compliance requirements. Their investment targets are usually located in a more mature and regulated market.

(4) Investor type

Private crypto funds typically attract investors with a strong interest in cryptocurrencies and blockchain technology, who may be more willing to embrace opportunities presented by high volatility and innovative technologies.

Ordinary private equity funds: The investor base is broader, typically including high-net-worth individuals and institutional investors seeking relatively stable returns, as well as pension funds, endowment funds, etc.

(5) Technological dependence

Private crypto funds: These are highly dependent on technology and require management teams to have an understanding and application of cutting-edge technologies such as blockchain, smart contracts, and decentralized finance (DeFi).

Typical private equity funds rely more on traditional financial analysis, market research, and portfolio management skills, and are relatively less dependent on technology.

(6) Liquidity

Private crypto funds: The cryptocurrency market can be highly liquid, but it can also be subject to liquidity risk due to insufficient market depth or the nature of certain assets, especially during periods of high market volatility, when this liquidity risk can be significantly amplified.

Typical private equity funds typically invest in assets with relatively certain liquidity arrangements, although they may still face liquidity constraints, especially when investing in long-term assets such as private companies or real estate.

These differences indicate that, although the two are similar in fund structure, they differ significantly in terms of investment targets, risk tolerance, regulatory environment, and market technical requirements.

1.2 Classification of Private Crypto Funds

Private crypto funds, as investment funds focused on the crypto asset market, can be categorized according to different criteria. Below are some common ways to classify private crypto funds based on their investment targets, operating methods, etc.:

(1) Classification by investment target

① Direct Investment Funds: These funds primarily invest directly in cryptocurrencies, blockchain projects, or NFTs (non-fungible tokens). They purchase and hold these assets in hopes of profiting from their appreciation.

② Indirect Investment Funds: Indirect investment funds may participate in the crypto asset market indirectly by investing in equity, fund units, or derivatives of crypto asset-related companies. For example, investing in equity in cryptocurrency exchanges, blockchain technology companies, or crypto asset mining companies.

(2) Classification by operating method

① Closed-end funds: Closed-end funds have a fixed size at the time of establishment and do not accept new investments for a certain period. These funds typically have a fixed term and are liquidated or transformed upon maturity. In private equity crypto funds, closed-end funds ensure that fund managers have a stable amount of capital over a period of time, which is conducive to their long-term investment strategy.

② Open-ended funds: Open-ended funds allow investors to subscribe to or redeem fund units at any time during the fund's term. These funds typically offer greater flexibility and can be adjusted according to market demand and investor preferences. However, in situations of high volatility in the crypto asset market, open-ended funds may face significant liquidity pressures.

(3) Classified by investment strategy

Depending on their investment strategies, private crypto funds can be categorized into active, passive, neutral, and fixed-income types.

① Passive strategies generate profits from rising coin prices. In the crypto asset field, this mainly involves tracking the overall performance of several highly liquid cryptocurrencies (such as Bitcoin and Ethereum) and passively profiting from their price increases.

② Neutral strategies hedge against market volatility (Delta) by using long and short positions and tools such as derivatives, keeping the overall long-term risk exposure around 0 and pursuing absolute returns unrelated to the rise and fall of coin prices. Common arbitrage and market-making strategies are all neutral strategies.

③ Active strategy refers to a strategy where the fund manager believes there is a target price based on a certain analytical model or prediction, and trades around the target price. If the current price is lower than the target price, the fund manager long; if the current price is higher than the target price, the fund manager short. The fund manager adjusts the position based on the difference between the current price and the target price. The returns come from both market conditions (Beta) and the excess returns (Alpha) generated by subjective judgment.

④ Fixed-income funds primarily generate returns through "bonds." Although there are no standard bonds in the crypto asset space, there is a large amount of off-exchange lending, i.e., non-standard bonds. These funds can earn returns by lending money or by profiting from the interest rate spread in lending, similar to traditional fixed-income funds. Returns are relatively stable, but strong risk control capabilities (such as collateral management) are required in actual operation. DeFi, on the other hand, is financial activity based on smart contracts on the blockchain and has certain fixed-income characteristics.

(4) Other classification methods

In addition, private crypto funds can also be classified according to other factors such as the source of funds and the investment stage. For example, based on the source of funds, they can be divided into private equity funds and private securities funds; based on the investment stage, they can be divided into angel funds, venture capital funds, etc.

2. Current Status of Global Private Equity Crypto Funds

2.1 Size of Crypto Funds

In recent years, the total market capitalization of cryptocurrencies has generally shown a fluctuating growth pattern, exceeding $2.3 trillion as of this writing. Data from Crypto Fund Research shows that although crypto funds represent a small percentage of the total fund size, nearly 900 crypto funds had been established globally by the end of 2023, encompassing various types such as hedge funds, venture capital funds, and index funds. Furthermore, according to a report by Galaxy, crypto asset funds performed strongly in 2023, with assets under management reaching $33 billion, with Bitcoin dominating the market and becoming the most popular investment target for funds.

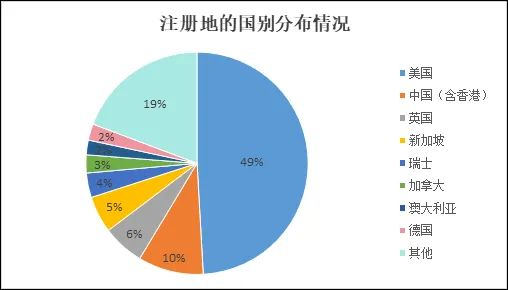

2.2 Major Registration Locations of Crypto Funds

Regarding the distribution of registration locations, although we cannot yet obtain the registration locations of private crypto funds, we can still get a general overview of the overall distribution of crypto fund registration locations in the form of charts based on data from Crypto Fund Research.

In terms of country of origin, the United States is favored by nearly half of all crypto funds, making it the primary location for crypto fund registration. It's also worth noting that although the Chinese government, particularly the mainland government, adopts a relatively conservative attitude towards crypto assets, the sheer size of its economy and the resulting investment demand mean that crypto funds registered in China still constitute a significant proportion.

2.3 Brief Introduction of Well-known Private Equity Crypto Funds

2.3.1 Pantera Capital

Pantera Capital is a private equity firm founded in 2003 and headquartered in California, USA. It is the world's first investment fund focused solely on blockchain technology and digital currencies, managing assets across multiple funds and portfolios focused on Bitcoin, ICOs (Initial Coin Offerings), and decentralized finance (DeFi). According to its website, Pantera Capital manages $4.8 billion in blockchain-related assets.

2.3.2 a16z Crypto

Headquartered in California, USA, a16z Crypto is a venture capital fund under the renowned venture capital firm Andreessen Horowitz, focusing on Crypto and Web3 startups. a16z Crypto's portfolio is broad, covering blockchain infrastructure, decentralized applications (dApps), payment systems, and more. According to its website, a16z Crypto manages over $7.6 billion in assets across four funds, wielding significant influence within the industry.

2.3.3 Galaxy Digital

Founded in 2018 and headquartered in New York, USA, Galaxy Digital is an investment management company focused on digital assets and blockchain technology, founded by former hedge fund manager Mike Novogratz. Galaxy Digital offers a variety of cryptocurrency-related investment products, including hedge funds, venture capital funds, and asset management services. According to its website, Galaxy Digital currently manages approximately $2.1 billion in assets, holding a significant position in the cryptocurrency industry and frequently appearing in industry news.

2.3.4 AnB Investment

AnB Investment is an Independent Portfolio Company (SPC) registered in the Cayman Islands. It operates two funds: a quantitative multi-strategy fund and a neutral strategy fund, primarily investing in crypto assets and DeFi, aiming to generate alpha returns from market volatility. The total assets under management (AUM) are $50 million, with a minimum investment of $100,000 per transaction. Both funds are open for monthly subscriptions and redemptions. Revenue is generated through management fees and performance-based compensation. According to AnB Investment's promotional materials, the management fee is 2.4%, and the performance-based compensation is 20% using the high-water mark method. The main expenses for operating the funds are related to strategy, trading, auditing, operations, risk control, and legal systems and personnel.

2.3.5 HashKey Digital Investment Fund

The fund will officially accept investor subscriptions starting September 1, 2023. Approved by the Hong Kong Securities and Futures Commission and managed by HashKey Capital Limited, the fund's portfolio is 100% composed of virtual assets. HashKey Capital is launching a compliant secondary liquidity fund. The fund will allocate less than 50% of its investments to Bitcoin and Ethereum, the two largest cryptocurrencies, while also diversifying its portfolio by investing in other cryptocurrencies.

3. Overview of key international regulatory rules for private crypto funds

Currently, some international organizations and some countries have made relevant regulations on the supervision of private cryptocurrency funds. Some of them are listed below:

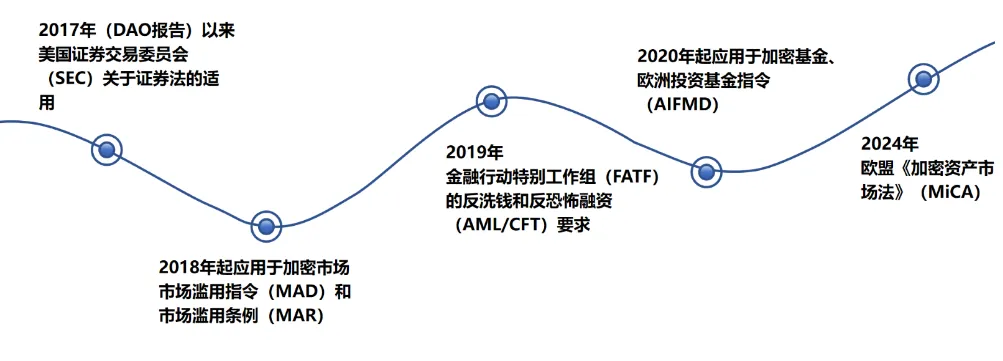

3.1 U.S. Securities and Exchange Commission (SEC) on the application of securities laws

In 2017, the U.S. Securities and Exchange Commission (SEC) released the well-known "The DAO Investigation Report." The report stated that certain cryptocurrencies and Initial Coin Offerings (ICOs) may meet the definition of "securities" under the Securities Act of 1933 and the Securities Exchange Act of 1934. Therefore, these crypto assets need to comply with the relevant securities regulations, including registration, disclosure, and fraud protection. This regulation is particularly relevant to crypto projects and token issuances that raise funds and promise future profits or returns. For example, if tokens raise funds through an ICO and grant holders corresponding rights, dividends, or other economic benefits, they may be considered securities. For these assets, issuers must register with the SEC or apply for an exemption, and must also regularly disclose financial and other material information to ensure adequate investor protection.

Subsequently, the SEC tightened its oversight of cryptocurrency funds, requiring them to comply with existing securities laws. For example, cryptocurrency funds must register or obtain exemptions when dealing with security tokens or other similar products. Furthermore, fund managers must ensure that the fund's operations comply with "accredited investor" requirements and meet relevant anti-money laundering, anti-fraud, and other compliance requirements.

The SEC's increased regulatory scrutiny of crypto assets reflects its emphasis on investor protection and market stability. In 2020, the SEC released the Crypto Asset Framework, further clarifying the criteria for classifying crypto assets as securities. This framework focuses on assessing factors such as whether token purchasers expect to profit from the efforts of others, whether the project team plays a central role in the development and marketing of the asset, and whether the project possesses decentralized characteristics. Of course, if the Financial Innovation and Technology for the 21st Century Act (FIT21) is ultimately passed, the SEC's standards may need to be adjusted.

3.2 EU Market Abuse Directive (MAD) and Market Abuse Regulation (MAR)

The Market Abuse Directive (MAD) and the Market Abuse Regulation (MAR), implemented in 2018, are a comprehensive framework developed by the European Union to prevent market manipulation, insider trading, and illegal disclosure of inside information. These regulations aim to prevent illegal activities such as market manipulation and insider trading. Since 2018, the MAR has explicitly applied to financial instruments in the cryptocurrency market. For example, if crypto assets are considered "financial instruments" (such as security tokens), they must comply with the MAR, including preventing insider trading, market manipulation, and improper disclosure of information. Furthermore, traders involved in crypto assets, particularly those trading in regulated markets or whose actions could potentially influence market prices, are subject to the Market Abuse Regulation. This aims to ensure investors have fair information and prevent market distortion due to illegal activities.

3.3 Financial Action Task Force (FATF) Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT) Requirements

The Financial Action Task Force (FATF) is an international body that sets global standards for anti-money laundering and counter-terrorist financing. In 2019, FATF released guidance on virtual assets and virtual asset service providers (VASPs), clearly defining anti-money laundering and counter-terrorist financing requirements for the crypto asset sector for the first time. This guidance imposes stringent AML/CFT requirements on VASPs, including: requiring VASPs to conduct customer due diligence (CDD), including collecting and verifying customer identity information; requiring VASPs to report suspicious activity to relevant authorities for transactions exceeding a certain amount; and monitoring cross-border transactions. When institutions directly participate in the custody, management, transfer, or trading of virtual assets, they are considered VASPs and must comply with FATF's AML and CFT requirements. Currently, countries worldwide are gradually incorporating FATF guidance into their national laws, requiring crypto funds to adhere to these AML/CFT standards.

3.4 European Investment Funds Directive (AIFMD)

The AIFMD (Alternative Investment Management Act) was initially adopted in 2011 to strengthen the regulation of alternative investment funds in Europe. With the rise of crypto funds, the scope of the AIFMD expanded to include crypto asset funds in 2020, requiring fund managers to ensure appropriate disclosure and risk management to protect investors' interests. Specific rules include: fund managers must regularly disclose the fund's investment strategy, asset allocation, and risks to investors; they must have sufficient compliance measures to avoid conflicts of interest; and they must ensure informed consent from investors. As a result, crypto funds in Europe are subject to strict regulation, thereby ensuring the protection of investors' rights.

3.5 EU Crypto-Asset Markets Act (MiCA)

To establish a unified regulatory framework for the crypto asset market, the European Union enacted Regulation 2023/1114—the Crypto Asset Market Regulation (MiCA)—in 2023. It was formally passed by the European Parliament on April 20, 2023, and came into effect on June 30, 2023, with a transition period ending on June 30, 2026. As part of the EU's comprehensive digital finance strategy, MiCA covers the registration, operation, and investor protection requirements for crypto funds. It clarifies the scope of application, the classification of crypto assets, regulatory bodies and corresponding information reporting systems, business restrictions, and conduct regulations. It is the most comprehensive digital asset regulatory framework to date, affecting all 27 EU member states and the other three countries in the European Economic Area (EEA) (Norway, Iceland, and Liechtenstein). It will provide a clear legal framework for crypto assets and achieve regulatory consistency across the EU.

4. Overview of Global Tax Policies for Private Crypto Funds

Many countries are actively developing or improving tax policies to ensure that the income and transaction gains of cryptocurrency funds can be accurately declared and taxed in accordance with the law. The taxes covered include capital gains tax, goods and services tax, and value-added tax.

4.1 United States

Income Tax: In the United States, private crypto funds can be organized as limited partnerships (LPs), limited liability companies (LLCs), or corporations (specifically classified as C-type and S-type corporations), each subject to different tax policies. LPs directly bear losses, share profits, and pay income tax; LLCs offer flexibility in choosing their tax structure, choosing to be taxed as a sole proprietorship, partnership, S-corporation, or C-corporation; corporations, however, face double taxation, as profits earned by corporations are subject to corporate income tax, and if profits are distributed as dividends to shareholders, the shareholders are also subject to personal income tax. Therefore, considering the high return potential of crypto assets, adopting a corporation structure may not be conducive to reducing the overall tax burden of private crypto funds and their investors.

Capital gains tax: In the United States, capital gains tax is divided into two types: short-term capital gains tax and long-term capital gains tax. Short-term capital gains refer to gains generated from assets held for no more than one year, while long-term capital gains refer to gains generated from assets held for more than one year. The tax rate for short-term capital gains is the same as the taxpayer's ordinary income tax rate; the tax rate for long-term capital gains is usually lower than that for short-term capital gains, and is divided into three brackets based on the taxpayer's total annual income and tax status: 0%, 15%, and 20%.

The IRS issued Notice 2014-21 regarding virtual currency transactions back in 2014, explaining how virtual currencies are treated for federal income tax. In this notice, all crypto assets are considered property, not currency, and therefore subject to the general tax principles for property transactions. This means that most crypto asset transactions are subject to capital gains tax. When conducting crypto asset transactions involving capital gains tax, investors need to subtract their cost basis from the selling price to calculate the capital gain or loss and pay the corresponding capital gains tax. The duration of holding the crypto asset (in one-year increments) determines the capital gains tax rate. If the crypto asset is held for more than one year, the investor is subject to long-term capital gains tax, which is generally lower than short-term capital gains tax, applicable to holdings of less than one year.

4.2 European Union

Value Added Tax (VAT): The EU's taxation policies for cryptocurrencies vary. Some countries levy VAT on crypto asset transactions, while others exempt them. For example, countries like Ireland and Germany do not levy VAT on Bitcoin transactions, but in Italy and Spain, these transactions may be subject to VAT.

MiCA (Crypto Asset Markets Law): The introduction of MiCA aims to provide a legal framework for crypto assets not covered by existing EU financial services legislation; to support innovation and promote the development and wider use of distributed ledger technology (DLT) by establishing a sound and transparent legal framework; to ensure appropriate consumer and investor protection and market integrity; and to further enhance financial stability, given the potential for widespread acceptance of some crypto assets.

4.3 United Kingdom

Due to common law tradition and the flexibility of crypto assets, the UK government has not opted for a comprehensive crypto asset tax law. Instead, it incorporates crypto assets into the existing tax framework based on their nature and purpose, primarily levying income tax and capital gains tax. These two taxes are collected in the same way as other types of income and assets. Taxpayers need to calculate their income and profits from crypto assets for each financial year and declare them on the corresponding tax return. The UK also offers several tax exemptions or relief measures, such as personal allowances, Individual Savings Account (ISA) allowances, and annual exemptions.

4.4 Singapore

(1) Income Tax: Singapore does not tax capital gains, making it a very favorable jurisdiction for private crypto funds. However, if cryptocurrency transactions are considered business income, income tax is payable.

(2) Goods and Services Tax (GST): Singapore originally planned to levy a Goods and Services Tax on cryptocurrency transactions, but as of January 1, 2020, it no longer levies GST on payment cryptocurrency (DPT) transactions.

5. OECD Regulatory and Tax Compliance Framework

The OECD, one of the most influential international organizations, has long focused on the regulation and taxation of crypto assets. In recent years, the OECD has developed several important policies and frameworks regarding the regulation and tax compliance of crypto assets and related funds, through expanding the scope of existing regulations and formulating new policies. These aim to regulate the operation of private crypto funds and ensure their tax transparency and compliance globally. Therefore, it is necessary to specifically focus on and summarize the OECD's regulatory and tax compliance framework.

5.1 Crypto-Asset Reporting Framework (CARF)

With the increasing prevalence of crypto assets, the OECD recognized that existing tax information exchange standards (such as the Common Reporting Standard (CRS)) could not fully cover the specific needs of crypto assets. Therefore, the OECD proposed CARF in 2022 to enhance the exchange and transparency of tax information related to crypto assets.

CARF requires crypto asset service providers (such as private crypto funds) to report their clients' crypto asset transactions to the tax authorities of their respective countries. The reports include client identification information, transaction amounts, and asset classes. It provides a globally unified standard, enabling tax authorities in different countries to effectively exchange information related to crypto assets, thereby preventing tax evasion.

5.2 Common Reporting Standard (CRS)

CRS is a global standard launched by the OECD in 2014, designed to combat cross-border tax evasion through the automatic exchange of information. Although CRS was initially applied primarily to traditional financial assets, in recent years, countries have gradually included crypto assets in its scope.

The CRS requires financial institutions (including crypto funds) to collect and report their clients' tax information. This information includes account holder identity, account balance, interest income, etc., and the relevant information is automatically exchanged between tax authorities in different countries.

At the 2024 G20 summit in Brazil, participating countries decided to extend the Automatic Exchange of Information (AEOI) mechanism, centered on CRS, to the crypto asset sector. This would require Crypto Asset Service Providers (RCASPs) to report crypto asset information of their non-resident clients and automatically exchange this information with the tax authorities of the clients' countries, thereby improving tax transparency in the crypto asset sector and preventing tax evasion and avoidance.

5.3 Action Plan on Base Erosion and Profit Shifting

The Base Erosion and Profit Shifting (BEPS) initiative is a global initiative jointly launched by the OECD and G20 to address the risks of base erosion and profit shifting by strengthening international tax rules. With the rise of crypto assets, some of BEPS' action plans (such as Items 1 and 13) are also beginning to apply to crypto assets and private crypto funds.

Its main contents include:

(1) Tax Challenges of the Digital Economy: BEPS Action Plan 1 explores how to address the tax challenges posed by the digital economy, including crypto assets. The plan encourages countries to implement measures to ensure tax fairness for crypto assets.

(2) Country-by-Country Reporting (CbCR): BEPS Action Plan 13 requires multinational corporations, including private crypto funds, to submit country-by-country reports to tax authorities, disclosing information such as their income, pre-tax profits, and taxes paid in each country. This helps countries identify and combat profit shifting.

References

[1].Rock'n'Bock. (2024b, May 7). 50 Blockchain & Crypto VC Funds List in 2024. Rocknblock.io; Rock'n'Block.

[2]. Home. (nd-b). Galaxy.

[3]. Home. (nd-c). Pantera.

[4]. Enriques, L., & Zetzsche, DA (2019). Corporate Technologies and the Tech Nirvana Fallacy. SSRN Electronic Journal.

[5].Rubinstein, F., & Vettori, GG (2018). Taxation of Investments in Bitcoins and Other Virtual Currencies: International Trends and the Brazilian Approach. SSRN Electronic Journal.

[6].Bossu, W., Itatani, M., Margulis, C., Rossi, ADP, Weenink, H., & Yoshinaga, A. (2020). Legal Aspects of Central Bank Digital Currency. IMF Working Papers, 20(254).

[7].Crypto Fund Research. (2024) 2023 Q4 Crypto Fund Report, Crypto Fund Research.

[8].Crypto Fund Research. (2024) Cryptocurrency Investment Fund Industry Graphs and Charts.

Original link: https://mp.weixin.qq.com/s/Sp5CKlFiC5W3aWQePwwWUQ

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objection to the reprint format, please contact us and we will modify it according to the author's request. This reprint is for information sharing only and does not constitute any investment advice, nor does it represent Wu Blockchain views or positions.

As more and more traditional financial institutions and even non-financial institutions begin to engage in private crypto fund business and allocate crypto-related assets, the compliant operation of private crypto funds has become increasingly important. This article will summarize the types and characteristics of crypto funds with different strategy attributes, trading methods, and funding sources, as well as the macro-regulatory situation of private crypto funds. Using compliant fund operation case studies, it will introduce the operational process of private crypto fund business and the key elements for compliant operation of private crypto funds.

1. Definition and Classification of Private Crypto Funds

1.1 What is a private crypto fund?

1.1.1 Definition and Characteristics of Private Crypto Funds

In a broad sense, a fund refers to a certain amount of capital established for a specific purpose. This mainly includes trust investment funds, provident funds, insurance funds, retirement funds, and funds from various foundations. A common characteristic is that they are centrally managed by specialized asset managers to generate higher investment returns. These funds can be invested in the primary market (venture capital, private equity) and the secondary market.

A private crypto fund is a non-publicly offered investment fund primarily targeting institutional and individual investors with sufficient wealth and risk tolerance. It focuses on investing in crypto assets and related projects, and its holdings may include crypto assets, crypto options and futures, crypto company stocks, RWA assets, etc. This fund combines the characteristics of private equity funds with the unique features of crypto assets, and its distinguishing features from other private equity funds can be summarized as follows:

① Specific investment scope: Private crypto funds focus on the crypto asset market, including digital currencies, blockchain projects, decentralized finance (DeFi) applications, etc.

② High Value Volatility: The value volatility of crypto assets far exceeds that of traditional financial assets. The valuation of unsecured crypto assets (such as most cryptocurrencies) is primarily based on speculative demand, resulting in extremely high price fluctuations. This high volatility presents investors with potential for high returns, but it also increases investment risk.

③ Significant Differences in Regulatory Attitudes Across Countries: Different countries exhibit substantial differences in their regulatory attitudes towards crypto assets. For example, the US regulatory policy on cryptocurrencies is relatively vague and constantly evolving, while Japan legalized Bitcoin and brought it under its regulatory purview earlier. Private equity crypto fund managers need to closely monitor changes in regulatory policies in various countries to adjust their investment strategies and mitigate compliance risks.

④ Low transparency: Private equity funds inherently possess low transparency, and the anonymity and decentralization of the crypto asset market further exacerbate this lack of transparency. Therefore, private crypto funds need to establish sound information disclosure systems and investor protection mechanisms.

1.1.2 Differences between private crypto funds and traditional private funds

Private crypto funds and regular private funds are similar in many ways, but there are some key differences due to their different investment targets and market environments.

(1) Investment target

Private crypto funds: These focus on cryptocurrencies, blockchain technology, and related digital assets. They may invest directly in cryptocurrencies (such as Bitcoin and Ethereum), or in blockchain startups, tokenized assets, and other projects related to the blockchain ecosystem.

Typical private equity funds typically invest in assets in traditional financial markets, such as stocks, bonds, real estate, private equity, or other traditional asset classes. While their investment targets are more diversified, they are all based on the traditional economic system.

(2) Risk and volatility

Private Crypto Funds: The cryptocurrency market is highly volatile and faces significant risks, including market volatility, technological risks (such as hacking), regulatory risks (different countries have vastly different attitudes toward regulation and policies may change constantly), and liquidity risks (some tokens or crypto assets may be difficult to liquidate quickly).

Traditional private equity funds: While still facing market volatility, changes in the economic environment, and specific industry risks, these risks are generally more manageable and have more abundant historical data. The investment targets of traditional private equity funds typically have a longer market history and a clearer regulatory framework.

(3) Regulatory environment

Private crypto funds: Limited by the regulatory environment of the cryptocurrency market, they may face greater uncertainty. Different countries have different regulatory policies regarding cryptocurrencies and related assets, which could affect the fund's operations and investment strategies.

Typical private equity funds are generally subject to strict financial regulation and laws and regulations, with clear compliance requirements. Their investment targets are usually located in a more mature and regulated market.

(4) Investor type

Private crypto funds typically attract investors with a strong interest in cryptocurrencies and blockchain technology, who may be more willing to embrace opportunities presented by high volatility and innovative technologies.

Ordinary private equity funds: The investor base is broader, typically including high-net-worth individuals and institutional investors seeking relatively stable returns, as well as pension funds, endowment funds, etc.

(5) Technological dependence

Private crypto funds: These are highly dependent on technology and require management teams to have an understanding and application of cutting-edge technologies such as blockchain, smart contracts, and decentralized finance (DeFi).

Typical private equity funds rely more on traditional financial analysis, market research, and portfolio management skills, and are relatively less dependent on technology.

(6) Liquidity

Private crypto funds: The cryptocurrency market can be highly liquid, but it can also be subject to liquidity risk due to insufficient market depth or the nature of certain assets, especially during periods of high market volatility, when this liquidity risk can be significantly amplified.

Typical private equity funds typically invest in assets with relatively certain liquidity arrangements, although they may still face liquidity constraints, especially when investing in long-term assets such as private companies or real estate.

These differences indicate that, although the two are similar in fund structure, they differ significantly in terms of investment targets, risk tolerance, regulatory environment, and market technical requirements.

1.2 Classification of Private Crypto Funds

Private crypto funds, as investment funds focused on the crypto asset market, can be categorized according to different criteria. Below are some common ways to classify private crypto funds based on their investment targets, operating methods, etc.:

(1) Classification by investment target

① Direct Investment Funds: These funds primarily invest directly in cryptocurrencies, blockchain projects, or NFTs (non-fungible tokens). They purchase and hold these assets in hopes of profiting from their appreciation.

② Indirect Investment Funds: Indirect investment funds may participate in the crypto asset market indirectly by investing in equity, fund units, or derivatives of crypto asset-related companies. For example, investing in equity in cryptocurrency exchanges, blockchain technology companies, or crypto asset mining companies.

(2) Classification by operating method

① Closed-end funds: Closed-end funds have a fixed size at the time of establishment and do not accept new investments for a certain period. These funds typically have a fixed term and are liquidated or transformed upon maturity. In private equity crypto funds, closed-end funds ensure that fund managers have a stable amount of capital over a period of time, which is conducive to their long-term investment strategy.

② Open-ended funds: Open-ended funds allow investors to subscribe to or redeem fund units at any time during the fund's term. These funds typically offer greater flexibility and can be adjusted according to market demand and investor preferences. However, in situations of high volatility in the crypto asset market, open-ended funds may face significant liquidity pressures.

(3) Classified by investment strategy

Depending on their investment strategies, private crypto funds can be categorized into active, passive, neutral, and fixed-income types.

① Passive strategies generate profits from rising coin prices. In the crypto asset field, this mainly involves tracking the overall performance of several highly liquid cryptocurrencies (such as Bitcoin and Ethereum) and passively profiting from their price increases.

② Neutral strategies hedge against market volatility (Delta) by using long and short positions and tools such as derivatives, keeping the overall long-term risk exposure around 0 and pursuing absolute returns unrelated to the rise and fall of coin prices. Common arbitrage and market-making strategies are all neutral strategies.

③ Active strategy refers to a strategy where the fund manager believes there is a target price based on a certain analytical model or prediction, and trades around the target price. If the current price is lower than the target price, the fund manager long; if the current price is higher than the target price, the fund manager short. The fund manager adjusts the position based on the difference between the current price and the target price. The returns come from both market conditions (Beta) and the excess returns (Alpha) generated by subjective judgment.

④ Fixed-income funds primarily generate returns through "bonds." Although there are no standard bonds in the crypto asset space, there is a large amount of off-exchange lending, i.e., non-standard bonds. These funds can earn returns by lending money or by profiting from the interest rate spread in lending, similar to traditional fixed-income funds. Returns are relatively stable, but strong risk control capabilities (such as collateral management) are required in actual operation. DeFi, on the other hand, is financial activity based on smart contracts on the blockchain and has certain fixed-income characteristics.

(4) Other classification methods

In addition, private crypto funds can also be classified according to other factors such as the source of funds and the investment stage. For example, based on the source of funds, they can be divided into private equity funds and private securities funds; based on the investment stage, they can be divided into angel funds, venture capital funds, etc.

2. Current Status of Global Private Equity Crypto Funds

2.1 Size of Crypto Funds

In recent years, the total market capitalization of cryptocurrencies has generally shown a fluctuating growth pattern, exceeding $2.3 trillion as of this writing. Data from Crypto Fund Research shows that although crypto funds represent a small percentage of the total fund size, nearly 900 crypto funds had been established globally by the end of 2023, encompassing various types such as hedge funds, venture capital funds, and index funds. Furthermore, according to a report by Galaxy, crypto asset funds performed strongly in 2023, with assets under management reaching $33 billion, with Bitcoin dominating the market and becoming the most popular investment target for funds.

2.2 Major Registration Locations of Crypto Funds

Regarding the distribution of registration locations, although we cannot yet obtain the registration locations of private crypto funds, we can still get a general overview of the overall distribution of crypto fund registration locations in the form of charts based on data from Crypto Fund Research.

In terms of country of origin, the United States is favored by nearly half of all crypto funds, making it the primary location for crypto fund registration. It's also worth noting that although the Chinese government, particularly the mainland government, adopts a relatively conservative attitude towards crypto assets, the sheer size of its economy and the resulting investment demand mean that crypto funds registered in China still constitute a significant proportion.

2.3 Brief Introduction of Well-known Private Equity Crypto Funds

2.3.1 Pantera Capital

Pantera Capital is a private equity firm founded in 2003 and headquartered in California, USA. It is the world's first investment fund focused solely on blockchain technology and digital currencies, managing assets across multiple funds and portfolios focused on Bitcoin, ICOs (Initial Coin Offerings), and decentralized finance (DeFi). According to its website, Pantera Capital manages $4.8 billion in blockchain-related assets.

2.3.2 a16z Crypto

Headquartered in California, USA, a16z Crypto is a venture capital fund under the renowned venture capital firm Andreessen Horowitz, focusing on Crypto and Web3 startups. a16z Crypto's portfolio is broad, covering blockchain infrastructure, decentralized applications (dApps), payment systems, and more. According to its website, a16z Crypto manages over $7.6 billion in assets across four funds, wielding significant influence within the industry.

2.3.3 Galaxy Digital

Founded in 2018 and headquartered in New York, USA, Galaxy Digital is an investment management company focused on digital assets and blockchain technology, founded by former hedge fund manager Mike Novogratz. Galaxy Digital offers a variety of cryptocurrency-related investment products, including hedge funds, venture capital funds, and asset management services. According to its website, Galaxy Digital currently manages approximately $2.1 billion in assets, holding a significant position in the cryptocurrency industry and frequently appearing in industry news.

2.3.4 AnB Investment

AnB Investment is an Independent Portfolio Company (SPC) registered in the Cayman Islands. It operates two funds: a quantitative multi-strategy fund and a neutral strategy fund, primarily investing in crypto assets and DeFi, aiming to generate alpha returns from market volatility. The total assets under management (AUM) are $50 million, with a minimum investment of $100,000 per transaction. Both funds are open for monthly subscriptions and redemptions. Revenue is generated through management fees and performance-based compensation. According to AnB Investment's promotional materials, the management fee is 2.4%, and the performance-based compensation is 20% using the high-water mark method. The main expenses for operating the funds are related to strategy, trading, auditing, operations, risk control, and legal systems and personnel.

2.3.5 HashKey Digital Investment Fund

The fund will officially accept investor subscriptions starting September 1, 2023. Approved by the Hong Kong Securities and Futures Commission and managed by HashKey Capital Limited, the fund's portfolio is 100% composed of virtual assets. HashKey Capital is launching a compliant secondary liquidity fund. The fund will allocate less than 50% of its investments to Bitcoin and Ethereum, the two largest cryptocurrencies, while also diversifying its portfolio by investing in other cryptocurrencies.

3. Overview of key international regulatory rules for private crypto funds

Currently, some international organizations and some countries have made relevant regulations on the supervision of private cryptocurrency funds. Some of them are listed below:

3.1 U.S. Securities and Exchange Commission (SEC) on the application of securities laws

In 2017, the U.S. Securities and Exchange Commission (SEC) released the well-known "The DAO Investigation Report." The report stated that certain cryptocurrencies and Initial Coin Offerings (ICOs) may meet the definition of "securities" under the Securities Act of 1933 and the Securities Exchange Act of 1934. Therefore, these crypto assets need to comply with the relevant securities regulations, including registration, disclosure, and fraud protection. This regulation is particularly relevant to crypto projects and token issuances that raise funds and promise future profits or returns. For example, if tokens raise funds through an ICO and grant holders corresponding rights, dividends, or other economic benefits, they may be considered securities. For these assets, issuers must register with the SEC or apply for an exemption, and must also regularly disclose financial and other material information to ensure adequate investor protection.

Subsequently, the SEC tightened its oversight of cryptocurrency funds, requiring them to comply with existing securities laws. For example, cryptocurrency funds must register or obtain exemptions when dealing with security tokens or other similar products. Furthermore, fund managers must ensure that the fund's operations comply with "accredited investor" requirements and meet relevant anti-money laundering, anti-fraud, and other compliance requirements.

The SEC's increased regulatory scrutiny of crypto assets reflects its emphasis on investor protection and market stability. In 2020, the SEC released the Crypto Asset Framework, further clarifying the criteria for classifying crypto assets as securities. This framework focuses on assessing factors such as whether token purchasers expect to profit from the efforts of others, whether the project team plays a central role in the development and marketing of the asset, and whether the project possesses decentralized characteristics. Of course, if the Financial Innovation and Technology for the 21st Century Act (FIT21) is ultimately passed, the SEC's standards may need to be adjusted.

3.2 EU Market Abuse Directive (MAD) and Market Abuse Regulation (MAR)

The Market Abuse Directive (MAD) and the Market Abuse Regulation (MAR), implemented in 2018, are a comprehensive framework developed by the European Union to prevent market manipulation, insider trading, and illegal disclosure of inside information. These regulations aim to prevent illegal activities such as market manipulation and insider trading. Since 2018, the MAR has explicitly applied to financial instruments in the cryptocurrency market. For example, if crypto assets are considered "financial instruments" (such as security tokens), they must comply with the MAR, including preventing insider trading, market manipulation, and improper disclosure of information. Furthermore, traders involved in crypto assets, particularly those trading in regulated markets or whose actions could potentially influence market prices, are subject to the Market Abuse Regulation. This aims to ensure investors have fair information and prevent market distortion due to illegal activities.

3.3 Financial Action Task Force (FATF) Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT) Requirements

The Financial Action Task Force (FATF) is an international body that sets global standards for anti-money laundering and counter-terrorist financing. In 2019, FATF released guidance on virtual assets and virtual asset service providers (VASPs), clearly defining anti-money laundering and counter-terrorist financing requirements for the crypto asset sector for the first time. This guidance imposes stringent AML/CFT requirements on VASPs, including: requiring VASPs to conduct customer due diligence (CDD), including collecting and verifying customer identity information; requiring VASPs to report suspicious activity to relevant authorities for transactions exceeding a certain amount; and monitoring cross-border transactions. When institutions directly participate in the custody, management, transfer, or trading of virtual assets, they are considered VASPs and must comply with FATF's AML and CFT requirements. Currently, countries worldwide are gradually incorporating FATF guidance into their national laws, requiring crypto funds to adhere to these AML/CFT standards.

3.4 European Investment Funds Directive (AIFMD)

The AIFMD (Alternative Investment Management Act) was initially adopted in 2011 to strengthen the regulation of alternative investment funds in Europe. With the rise of crypto funds, the scope of the AIFMD expanded to include crypto asset funds in 2020, requiring fund managers to ensure appropriate disclosure and risk management to protect investors' interests. Specific rules include: fund managers must regularly disclose the fund's investment strategy, asset allocation, and risks to investors; they must have sufficient compliance measures to avoid conflicts of interest; and they must ensure informed consent from investors. As a result, crypto funds in Europe are subject to strict regulation, thereby ensuring the protection of investors' rights.

3.5 EU Crypto-Asset Markets Act (MiCA)

To establish a unified regulatory framework for the crypto asset market, the European Union enacted Regulation 2023/1114—the Crypto Asset Market Regulation (MiCA)—in 2023. It was formally passed by the European Parliament on April 20, 2023, and came into effect on June 30, 2023, with a transition period ending on June 30, 2026. As part of the EU's comprehensive digital finance strategy, MiCA covers the registration, operation, and investor protection requirements for crypto funds. It clarifies the scope of application, the classification of crypto assets, regulatory bodies and corresponding information reporting systems, business restrictions, and conduct regulations. It is the most comprehensive digital asset regulatory framework to date, affecting all 27 EU member states and the other three countries in the European Economic Area (EEA) (Norway, Iceland, and Liechtenstein). It will provide a clear legal framework for crypto assets and achieve regulatory consistency across the EU.

4. Overview of Global Tax Policies for Private Crypto Funds

Many countries are actively developing or improving tax policies to ensure that the income and transaction gains of cryptocurrency funds can be accurately declared and taxed in accordance with the law. The taxes covered include capital gains tax, goods and services tax, and value-added tax.

4.1 United States

Income Tax: In the United States, private crypto funds can be organized as limited partnerships (LPs), limited liability companies (LLCs), or corporations (specifically classified as C-type and S-type corporations), each subject to different tax policies. LPs directly bear losses, share profits, and pay income tax; LLCs offer flexibility in choosing their tax structure, choosing to be taxed as a sole proprietorship, partnership, S-corporation, or C-corporation; corporations, however, face double taxation, as profits earned by corporations are subject to corporate income tax, and if profits are distributed as dividends to shareholders, the shareholders are also subject to personal income tax. Therefore, considering the high return potential of crypto assets, adopting a corporation structure may not be conducive to reducing the overall tax burden of private crypto funds and their investors.

Capital gains tax: In the United States, capital gains tax is divided into two types: short-term capital gains tax and long-term capital gains tax. Short-term capital gains refer to gains generated from assets held for no more than one year, while long-term capital gains refer to gains generated from assets held for more than one year. The tax rate for short-term capital gains is the same as the taxpayer's ordinary income tax rate; the tax rate for long-term capital gains is usually lower than that for short-term capital gains, and is divided into three brackets based on the taxpayer's total annual income and tax status: 0%, 15%, and 20%.

The IRS issued Notice 2014-21 regarding virtual currency transactions back in 2014, explaining how virtual currencies are treated for federal income tax. In this notice, all crypto assets are considered property, not currency, and therefore subject to the general tax principles for property transactions. This means that most crypto asset transactions are subject to capital gains tax. When conducting crypto asset transactions involving capital gains tax, investors need to subtract their cost basis from the selling price to calculate the capital gain or loss and pay the corresponding capital gains tax. The duration of holding the crypto asset (in one-year increments) determines the capital gains tax rate. If the crypto asset is held for more than one year, the investor is subject to long-term capital gains tax, which is generally lower than short-term capital gains tax, applicable to holdings of less than one year.

4.2 European Union

Value Added Tax (VAT): The EU's taxation policies for cryptocurrencies vary. Some countries levy VAT on crypto asset transactions, while others exempt them. For example, countries like Ireland and Germany do not levy VAT on Bitcoin transactions, but in Italy and Spain, these transactions may be subject to VAT.

MiCA (Crypto Asset Markets Law): The introduction of MiCA aims to provide a legal framework for crypto assets not covered by existing EU financial services legislation; to support innovation and promote the development and wider use of distributed ledger technology (DLT) by establishing a sound and transparent legal framework; to ensure appropriate consumer and investor protection and market integrity; and to further enhance financial stability, given the potential for widespread acceptance of some crypto assets.

4.3 United Kingdom

Due to common law tradition and the flexibility of crypto assets, the UK government has not opted for a comprehensive crypto asset tax law. Instead, it incorporates crypto assets into the existing tax framework based on their nature and purpose, primarily levying income tax and capital gains tax. These two taxes are collected in the same way as other types of income and assets. Taxpayers need to calculate their income and profits from crypto assets for each financial year and declare them on the corresponding tax return. The UK also offers several tax exemptions or relief measures, such as personal allowances, Individual Savings Account (ISA) allowances, and annual exemptions.

4.4 Singapore

(1) Income Tax: Singapore does not tax capital gains, making it a very favorable jurisdiction for private crypto funds. However, if cryptocurrency transactions are considered business income, income tax is payable.

(2) Goods and Services Tax (GST): Singapore originally planned to levy a Goods and Services Tax on cryptocurrency transactions, but as of January 1, 2020, it no longer levies GST on payment cryptocurrency (DPT) transactions.

5. OECD Regulatory and Tax Compliance Framework

The OECD, one of the most influential international organizations, has long focused on the regulation and taxation of crypto assets. In recent years, the OECD has developed several important policies and frameworks regarding the regulation and tax compliance of crypto assets and related funds, through expanding the scope of existing regulations and formulating new policies. These aim to regulate the operation of private crypto funds and ensure their tax transparency and compliance globally. Therefore, it is necessary to specifically focus on and summarize the OECD's regulatory and tax compliance framework.

5.1 Crypto-Asset Reporting Framework (CARF)

With the increasing prevalence of crypto assets, the OECD recognized that existing tax information exchange standards (such as the Common Reporting Standard (CRS)) could not fully cover the specific needs of crypto assets. Therefore, the OECD proposed CARF in 2022 to enhance the exchange and transparency of tax information related to crypto assets.

CARF requires crypto asset service providers (such as private crypto funds) to report their clients' crypto asset transactions to the tax authorities of their respective countries. The reports include client identification information, transaction amounts, and asset classes. It provides a globally unified standard, enabling tax authorities in different countries to effectively exchange information related to crypto assets, thereby preventing tax evasion.

5.2 Common Reporting Standard (CRS)

CRS is a global standard launched by the OECD in 2014, designed to combat cross-border tax evasion through the automatic exchange of information. Although CRS was initially applied primarily to traditional financial assets, in recent years, countries have gradually included crypto assets in its scope.

The CRS requires financial institutions (including crypto funds) to collect and report their clients' tax information. This information includes account holder identity, account balance, interest income, etc., and the relevant information is automatically exchanged between tax authorities in different countries.

At the 2024 G20 summit in Brazil, participating countries decided to extend the Automatic Exchange of Information (AEOI) mechanism, centered on CRS, to the crypto asset sector. This would require Crypto Asset Service Providers (RCASPs) to report crypto asset information of their non-resident clients and automatically exchange this information with the tax authorities of the clients' countries, thereby improving tax transparency in the crypto asset sector and preventing tax evasion and avoidance.

5.3 Action Plan on Base Erosion and Profit Shifting

The Base Erosion and Profit Shifting (BEPS) initiative is a global initiative jointly launched by the OECD and G20 to address the risks of base erosion and profit shifting by strengthening international tax rules. With the rise of crypto assets, some of BEPS' action plans (such as Items 1 and 13) are also beginning to apply to crypto assets and private crypto funds.

Its main contents include:

(1) Tax Challenges of the Digital Economy: BEPS Action Plan 1 explores how to address the tax challenges posed by the digital economy, including crypto assets. The plan encourages countries to implement measures to ensure tax fairness for crypto assets.

(2) Country-by-Country Reporting (CbCR): BEPS Action Plan 13 requires multinational corporations, including private crypto funds, to submit country-by-country reports to tax authorities, disclosing information such as their income, pre-tax profits, and taxes paid in each country. This helps countries identify and combat profit shifting.

References

[1].Rock'n'Bock. (2024b, May 7). 50 Blockchain & Crypto VC Funds List in 2024. Rocknblock.io; Rock'n'Block.

[2]. Home. (nd-b). Galaxy.

[3]. Home. (nd-c). Pantera.

[4]. Enriques, L., & Zetzsche, DA (2019). Corporate Technologies and the Tech Nirvana Fallacy. SSRN Electronic Journal.

[5].Rubinstein, F., & Vettori, GG (2018). Taxation of Investments in Bitcoins and Other Virtual Currencies: International Trends and the Brazilian Approach. SSRN Electronic Journal.

[6].Bossu, W., Itatani, M., Margulis, C., Rossi, ADP, Weenink, H., & Yoshinaga, A. (2020). Legal Aspects of Central Bank Digital Currency. IMF Working Papers, 20(254).

[7].Crypto Fund Research. (2024) 2023 Q4 Crypto Fund Report, Crypto Fund Research.

[8].Crypto Fund Research. (2024) Cryptocurrency Investment Fund Industry Graphs and Charts.