Original author: Cosmo Jiang

Compiled by: Ken, Chaincatcher

AI agents are becoming economic participants. But what kind of financial mechanisms do they need to conduct transactions without human intervention?

The viral success of OpenClaw (formerly Clawdbot) marks a generational leap in autonomy. As these AI agents begin to interact with each other—and in some cases even negotiate and transact—the future of intelligent agents transforms from science fiction into an actionable reality.

OpenClaw is just one step in this accelerated process. Trillions of dollars are being poured into building an AI-powered world. By 2026, U.S. hyperscale cloud providers alone are projected to spend over $650 billion on AI, roughly ten times the inflation-adjusted cost of the Apollo program.

What began as simple chatbots are now evolving into intelligent, fully autonomous systems. These AI agents not only generate content but also become economic participants; they can reason, act, trade, coordinate, and debate—all without real-time human oversight.

Some forecasts suggest that by 2030, AI agents could facilitate $3 trillion to $5 trillion in global consumer business transactions. Even if only 10% of these transactions occur between agents, this would still represent hundreds of billions of dollars in machine-native settlement funds annually.

This naturally raises the question: what kind of financial and coordination framework is suitable for the native business of AI agents?

Today's business systems are built for humans, involving personal identity verification, banking intermediaries, legal contracts, settlement cycles, and human oversight. Autonomous software cannot walk into bank branches, sign paper documents, or wait days to complete ACH (Automated Clearing House) clearing. Intelligent agents require an infrastructure that is programmable by default, always online, globally accessible, permissionless, and machine-verifiable.

Blockchain can meet these constraints, and we are already seeing this dynamic emerging.

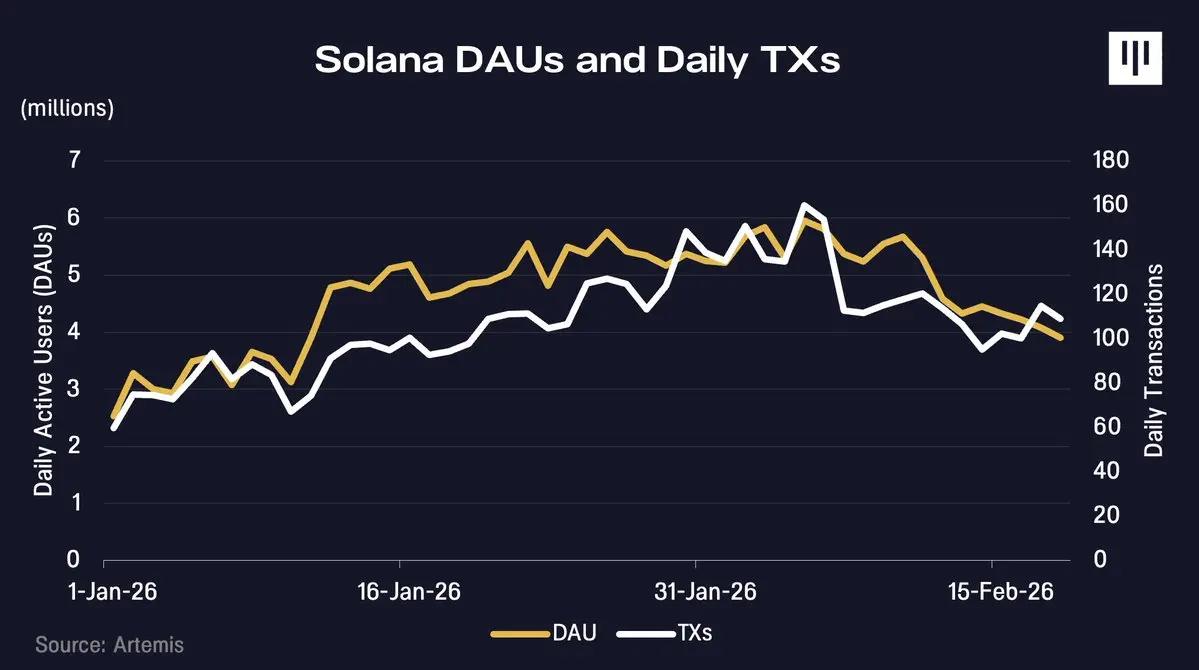

Coinciding with OpenClaw's rapid rise in popularity in January, Solana's transaction volume and number of active addresses have also begun to climb. Indices on Moltbook, the social network where its AI agents reside, suggest that they may have driven this growth.

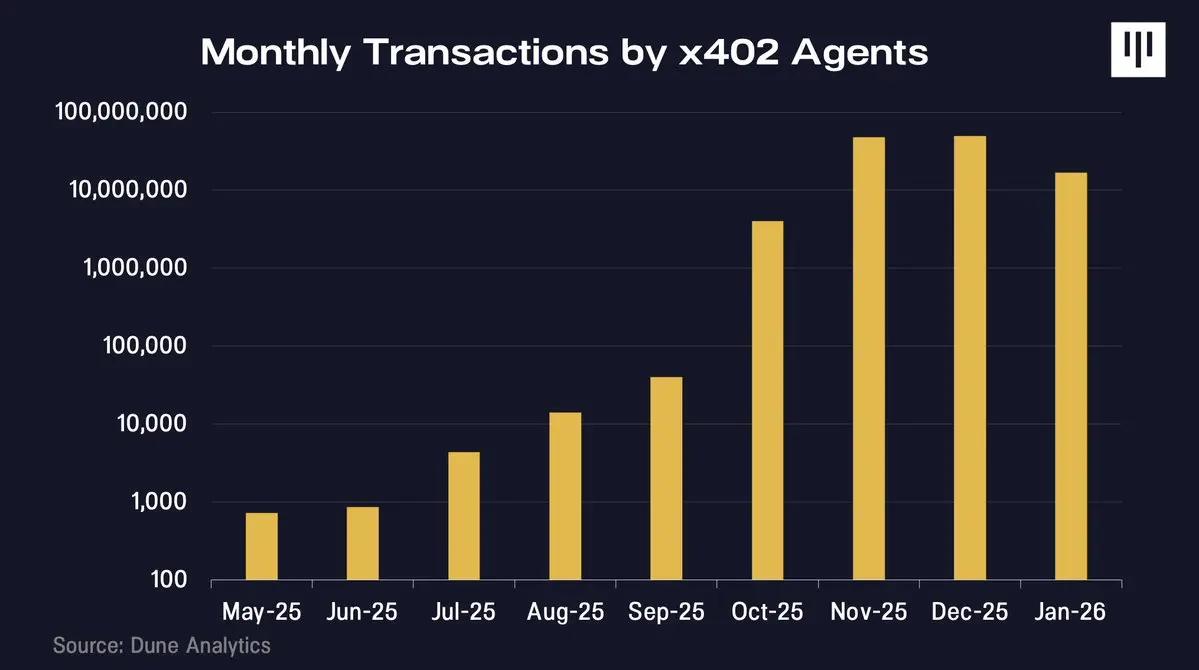

The x402 payment protocol, developed by Coinbase, enables smart agents to pay for digital resources in real time without an account or complex authentication. Its usage has steadily increased since its launch.

It is still in its early stages, and existing examples are more directional than decisive. However, if investors are excited about AI innovation, it would be an oversight to ignore "why the blockchain track could be the cornerstone for unlocking fully autonomous intelligent agents."

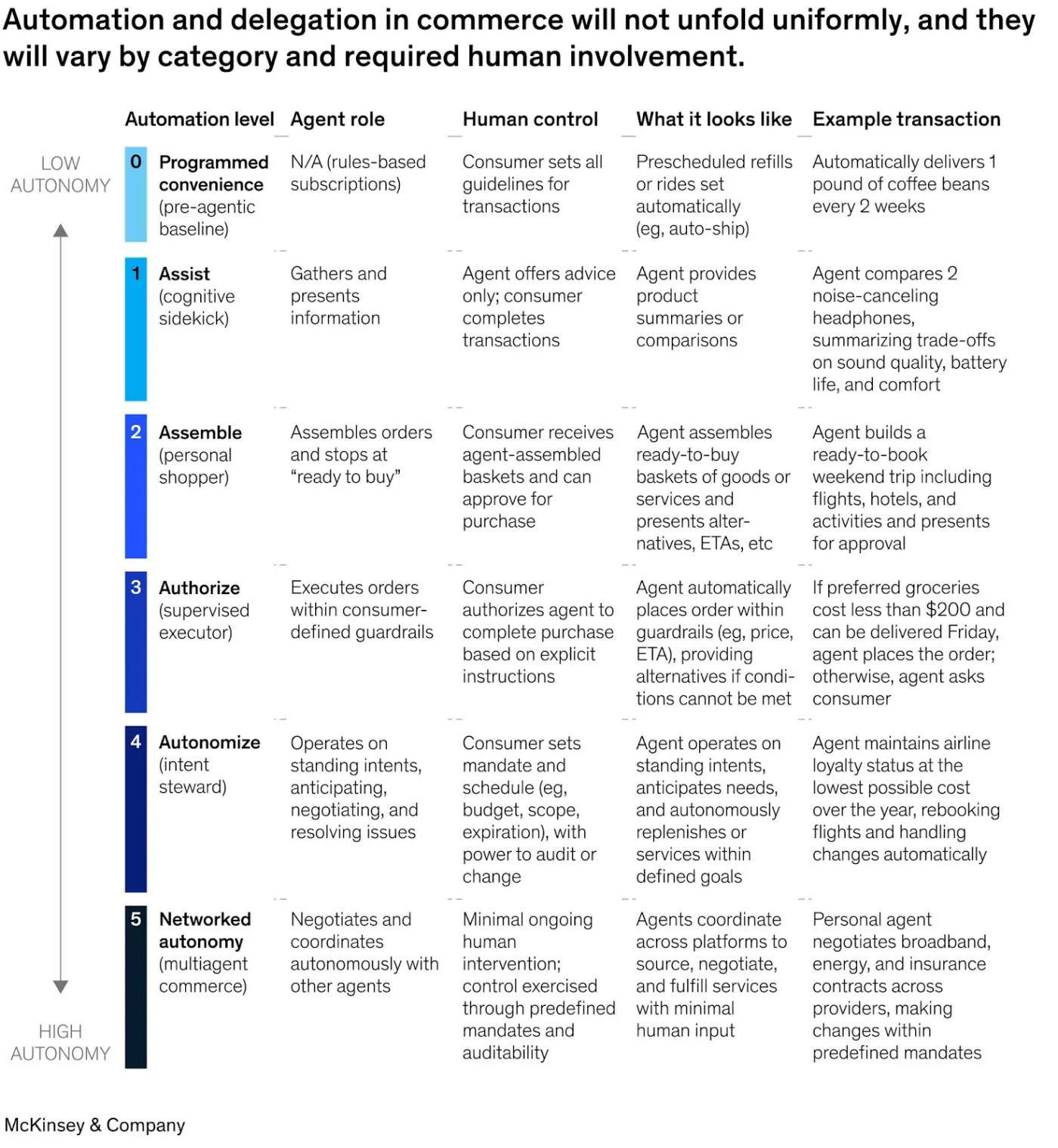

Autonomy level

Many would correctly point out that today's AI agents do not need blockchain. This is true, but it is short-sighted.

McKinsey outlines six levels of automation for AI-driven business, ranging from basic assistance (Level 0) to fully autonomous agent-to-agent business (Level 5). Levels 0-4 operate within existing financial frameworks because transactions are still backed by human identities. Human users have already authenticated themselves and linked their credit cards on platforms like ChatGPT, Amazon, or Perplexity. The agent simply acts as an intermediary, inheriting the human's identity, payment credentials, and legal status.

The infrastructure for this model—shared payment tokens, chargeback systems, fraud detection—already exists through Visa or Stripe and works well.

At level 5, the blockchain track becomes crucial: agents can transact directly with other agents without human instructions; no human identity can be inherited; payments must be programmatic, conditional, and settled within milliseconds; and the reputation of agents must be portable across different platforms.

As long as humans remain involved and take responsibility, the traditional path is sufficient. However, once intelligent agents become economically independent participants, the constraints will fundamentally change.

Intelligent Finance

To understand where value will converge and why blockchain is important, we must envision the ultimate logical form of intelligent agent AI. Some agents will be created by companies or individuals. Others will be generated autonomously by agents, forming increasingly independent systems capable of reasoning, capital allocation, and transactions without real-time human supervision.

In the absence of human-designated transaction channels (such as going to a bank, using Stripe, or creating a blockchain wallet), intelligent agents will rationally choose the path that maximizes speed, reliability, and global reach while minimizing friction and dependency. When the alternative is to open a bank account and wait for ACH settlement during limited bank hours, the agent will naturally choose the permissionless, 24/7 blockchain path.

We have identified three structural constraints that will drive agents toward the blockchain track.

Identity and Access Permissions

Before an agent can conduct a transaction, the counterparty must know who it is dealing with or what it is dealing with.

Traditional identity verification systems are designed for humans, relying on government IDs, physical signatures, and legal personhood. Autonomous AI agents lack any of these.

Tying AI agents to human bank accounts immediately raises questions: How can anti-money laundering (AML) checks be performed on the software? Who is the debtor? How can permissions be independently granted to multiple AI agents? How can misconduct be isolated without freezing the entire account?

In simple cases, agents can inherit credentials from their owners (e.g., ChatGPT Checkout). However, this model breaks down with widespread adoption. Agents need their own verifiable identities, not borrowed human identities.

Blockchain-based identity authentication allows agents to prove their authorization without revealing sensitive information. You can think of it as a digital authorization certificate that anyone, anywhere, can verify instantly without calling a lawyer or querying a database.

Emerging standards such as Ethereum's ERC-8004 introduce on-chain registries where agents can establish verifiable credentials and accumulate transaction history and reputation over time. An agent with thousands of undisputed transaction records is fundamentally different from a completely new agent, and this reputation is portable across different platforms.

Trust is a prerequisite for business. In an economy driven by intelligent agents, the core issue will shift from "intercepting bots" to "identifying which bots are trustworthy".

Programmable money and micropayments

Traditional payment systems are designed for human-scale transactions. Credit card fee structures make micropayments of less than a cent uneconomical. Anti-fraud systems also flag high-frequency machine activity as suspicious.

Commercial activities between agents operate on vastly different scales. One agent, writing code, might execute thousands of API calls in a single workflow. Another might compare prices across hundreds of data providers. Payments must occur within milliseconds, and the amounts are typically only a fraction of a cent.

On-chain transactions can be divided into extremely small units, and settlement costs are very low. More importantly, they are programmable. Payments can be conditional: payment is made only when the data is valid, funds are released upon completion of the task, or rewards are streamed in real time as the service is consumed. Agents can cryptographically prove their solvency without needing to pre-fund their accounts, thus greatly improving capital efficiency.

Blockchain enables financial infrastructure that matches the way intelligent agents operate: autonomous, high-frequency, conditional, and capital-efficient.

Deterministic execution

Traditional commerce relies on intermediaries for trust. Banks guarantee settlements. Payment processors manage chargebacks. Courts adjudicate disputes. Ultimately, contracts depend on the human legal system.

This framework comes under immense strain when billions of low-value transactions occur across different jurisdictions. Non-human actors may not share jurisdictions, legal remedies, or enforceable contracts. Cross-border enforcement is often slow, costly, and fraught with uncertainty.

Blockchain encodes enforcement directly into smart contracts, reducing reliance on centralized systems or legal remedies. Settlement is deterministic, unaffected by subjective interpretation. Rules are transparent and verifiable in advance. This is what blockchain enthusiasts call "trustless enforcement."

For large-scale autonomous agents, minimizing reliance on centralized intermediaries reduces friction and increases predictability. Lower friction also expands the boundaries of viable economic activity. Agent-driven commerce powered by blockchain technology has the potential to accelerate global GDP growth.

This is just the beginning.

The question is not whether intelligent agents will become commercially viable, but rather what kind of infrastructure they will operate on.

As AI agents become autonomous economic participants, the number of participants in the global economy will grow exponentially. These agents will require a digitally native financial framework, a technology stack capable of handling programmatic settlements, massive micropayments, permissionless coordination, and trust-minimized identities. These principles are central to the design of blockchain.

We believe the rapid proliferation of AI agents is a strong long-term structural positive driving blockchain activity. Preliminary evidence suggests this is already happening, and we believe it represents a value creation opportunity that is being underestimated by most investors.