"That 90-minute crash wiped out the investments of 1.66 million investors. The money went into the exchange's pocket."

First, the collapse you see is not the truth of the matter.

In the early hours of October 11, 2025, if you happen to be trading all night, you will witness the largest liquidation in cryptocurrency history: Bitcoin will be dumped starting from nearly $100,000, and Altcoin will generally drop by more than 40%. You want to close your position, click confirm, it spins, then times out; try again, still times out. The app freezes, the system crashes.

You might think this is a technical accident compounded by market panic and a stampede of unfortunate investors, but what you're seeing isn't the whole story.

The harsh truth behind it all is that while your order placement channel is blocked, someone else's channel remains open, and they're waiting there specifically. That person is the exchange itself.

II. Deliberately Compressed Numbers

Following the incident, the crypto data platform CoinGlass released its total liquidation data: $19.1 billion, involving approximately 1.66 million accounts. This figure was cited verbatim by almost all media outlets, becoming the official narrative anchor for the 10/11 attacks.

Common sense tells us that a $19.1 billion liquidation could not possibly have caused such a severe blow to the cryptocurrency market; it simply doesn't make sense. Therefore, there's only one truth:

This number is fake.

It's not a minor deviation in statistical methods, but a systemic, order-of-magnitude fraud.

▍Restore the true data

Hyperliquid is a blockchain-based decentralized exchange where data is completely public and tamper-proof. On October 11th, its liquidation volume was $10.31 billion, and its open interest (OI) was approximately $13.8 billion, resulting in a liquidation/OI ratio of about 75%—which is considered normal within the industry (50%–80%) during extreme flash crashes.

Applying the same logic to centralized exchanges:

Binance's online investment (OI) before the incident: approximately $120 billion (number one globally)

OKX's online inventory (OI) before the incident: approximately $43 billion (third largest globally).

Based on an extreme market condition with a 70% liquidation rate → Binance's actual liquidation volume: $84 billion; OKX: approximately $30 billion

According to CoinGlass, Binance's official liquidation amount was $2.41 billion, while OKX did not disclose the full figures.

This means that Binance underreported the value by a full 35 times.

This is not a typo, not a bug, it's a design flaw.

CoinGlass later admitted that when exchanges reported liquidation data to it, they only pushed one record per second, not the full amount. In extreme market conditions, the actual liquidation trigger frequency could reach hundreds of records per second. By controlling the push speed, exchanges could compress publicly available data to a fraction of its true size within the compliance framework. This mechanism is known in the industry as "bulk aggregation reporting"—in layman's terms: push only as much as you want the outside world to know.

Cathie Wood, founder of ARK Invest, believes the true deleveraging in 2011 was $28 billion; K33 Research gives a range of $35 billion to $40 billion; and Evgeny Gaevoy, CEO of market-making giant Windemute, publicly stated that the actual figure is "at least between $25 billion and $30 billion." No institution agrees with the figure of $19.1 billion.

III. How were the $22 billion and $3 billion earned?

When Binance announced a total of $680 million in compensation for affected accounts, no one could have predicted that they would profit immensely from this industry disaster. Their revenue breakdown is as follows:

The first type: liquidation discount profit

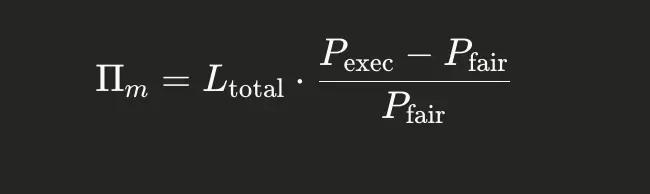

A former head of contract products at a leading exchange provided us with a formula:

in:

· — Manipulating profits

· — Nominal total amount of liquidated positions

· — Actual purchase price on the exchange

• — Fair market value

The latter part of this formula is a very important coefficient. It determines when and how the exchange will intervene to support the market in extreme cases, such as when a liquidity vacuum occurs. Specifically, it determines the price at which the liquidation engine will liquidate a user's position when it reaches the liquidation threshold.

Typically, a reputable trading platform will maintain a discount rate between 0.5% and 2% to avoid the industry-criticized phenomenon of price spikes, uphold the image expected of a leading exchange, and fulfill the basic responsibility of an industry leader. Previously, a well-regarded trading platform set a KPI of 1.375% for its contract trading team.

However, in an extreme flash crash like the one in 1011, where liquidity instantly dried up and market makers withdrew all orders, the situation was completely different: the exchange allowed the order book depth to plummet by 99%, and a forced liquidation order that should have been executed at $80,000 might actually have been executed at $65,000. This difference—the discount—is conservatively estimated to be no less than 20%, and may even exceed 30%.

More importantly, on centralized exchanges, this discount gain goes 100% to the exchange. No external arbitrageurs can intervene because the entire system is down; only the exchange can operate it.

Binance liquidation discount profit (conservative estimate): 84 billion × 20% = 16.8 billion USD

The second method: Profits from ADL automatic position reduction

When the losses from a margin call exceed the insurance fund's capacity, the exchange activates the ADL (Advance Debt Management) mechanism: forcibly liquidating profitable positions and using the profits of the traders to cover the margin call shortfall. This portion of the loss never appears in any public data; it has no name, no record, and is simply quietly deducted from profitable accounts.

The third type: Delayed transaction privilege

During system downtime, users cannot place orders or deposit margin. However, the liquidation engine doesn't immediately execute a liquidation—it can "delay" it. Prices continue to fall, position losses widen, and are then wiped out at an even lower price. For users, this is no different from a normal liquidation; the difference is that the liquidation price is much lower than it should have been. Who pockets the extra price difference?

Based on these calculations, with the three types of revenue combined, Binance's final profit is estimated to be between $18 billion and $22 billion, while OKX's is estimated to be between $2.5 billion and $3.5 billion.

IV. The Caste System in the Server

To understand how money is made, you also need to understand who can place orders during downtime.

Large centralized exchanges typically consist of several independent modules: an order placement module, a market data module, a clearing engine, and a risk control system. A "system crash" refers to the crash of the order placement channel accessible to external users. However, internally, there exists a priority system that is never explicitly stated in any user agreement.

Tier 1: Exchange Proprietary Market Makers – These are written in the same code as the exchange's core system, so external outages have zero impact on them. They are the only real selling force in the market during outages.

Tier 2: Leading third-party market makers (such as Wintertermute and Jump Trading) – possess proprietary low-latency API protocols, allowing ordinary users to still perform partial operations even when their systems are down.

Level 3: Ordinary quantitative trading teams – gradually become inoperable after system congestion, but recover slightly earlier than retail investors.

Level 4: Ordinary retail investors – always at the very bottom.

"Exchange servers have strict service priorities. When everyone else is down, only proprietary market makers can place orders. They are the referees, and also the fastest runners in the race." — Xiao Daxia, former core management member of Huobi.

V. The Wintertermute Incident: The wealthy man's money was returned in full.

Wintertermute was also affected by the outage.

One of the world's largest cryptocurrency market makers, managing billions of dollars in assets, also suffered significant losses during the 10/11 crash due to a lack of transparency in its liquidation mechanism. Afterwards, CEO Evgeny Gaevoy publicly criticized Binance on social media, claiming that Binance's liquidation data was "seriously underreported, with the actual liquidation scale at least ten times the official figures"; he also criticized the priority mechanism during the outage as "extremely unfair to third-party market makers." The post was shared thousands of times, causing an uproar in the industry.

This is a rare public counterattack, coming from the group least likely to fight back—the top market makers who have long profited from this system, finally speaking out because they too have been taken advantage of.

About ten days later, he deleted the post. All related statements were withdrawn. The official statement said, "This matter has been resolved through private channels." There has been no further public criticism since.

In the cryptocurrency industry, no one was surprised by this outcome. Wintermute got its money back—possibly even more than it lost; Binance silenced the most credible dissenting voice. A private settlement in exchange for permanent silence—a win-win situation for both parties.

VI. Jane Street: A Well-Designed Smokescreen

Months after 1011, a mysterious name inexplicably resurfaced: Jane Street. Accompanying this was an astonishing statistic: Jane Street's profits in the crypto are projected to reach $130 billion by 2025.

This world's largest high-frequency market maker was accused in a widely circulated tweet of systematically suppressing Bitcoin prices, manipulating the market through ETF derivatives structures, and being the mastermind behind the crash. The narrative connects multiple events, including the Terra crash lawsuit, penalties in the Indian market, and the regular sell-off at the opening of the US stock market, with a seemingly complete logical chain and extremely strong emotional appeal.

The underlying fact is that Jane Street is one of the core authorized participants (APs) of Bitcoin ETFs. When ETFs like IBIT experience large redemptions, Jane Street needs to sell in the spot market to hedge, causing concentrated selling pressure at the opening – a normal market-making behavior determined by the mechanism. Coinbase analysts have compiled data from the past 60 days showing a high degree of consistency in the opening price movements of IBIT and QQQ; the so-called "market dumping" is essentially a linkage at the beta level of the market. Furthermore, manipulating Bitcoin prices makes no business sense for Jane Street: market makers earn bid-ask spreads and volatility premiums; directional bets only bring unnecessary one-sided risks, and reputational damage is the price they cannot afford.

So why did this narrative become popular? Because it shifted the focus. When the market was rife with the claim that "Jane Street was manipulating Bitcoin," the discussion strayed from the truth: exchanges exploited system priority and liquidation mechanism vulnerabilities to absorb hundreds of billions of dollars in liquidation losses while users were unable to recover from their outages.

After all, some people will always be curious: whose pockets did their lost assets end up in?

Jane Street is a perfect target: big enough, mysterious enough, Wall Street-esque, naturally resonating with crypto fundamentalists. Directing anger toward Jane Street is the most valuable public relations gift to Binance and OKX.

VII. The Evolution of KPIs and the Birth of the Slaughterhouse

Xiao Daxian has been involved in the cryptocurrency industry for over a decade, and previously served in Huobi's core management team, witnessing the industry's complete evolution from its early stages to its current state. He attributes everything to one thing: KPIs.

In Huobi's early days, there were only two core KPIs: no margin calls and no price spikes. No margin calls were the bottom line—it was better to let the insurance fund bear the losses than to maliciously wipe out users' positions; no price spikes were a matter of principle—price data had to be accurate, and artificially created long shadows couldn't trigger mass liquidations. In those days, brand was more valuable than profit, and there was still a group of idealists in the industry who believed in Satoshi Nakamoto's vision.

As the industry continues to expand, the influence of leading exchanges is approaching that of traditional financial giants, but the industry's ethics and bottom line are declining inversely.

When Binance's daily trading volume surpassed $100 billion, when derivatives contracts became the platform's largest source of revenue, and when the two exchanges held hundreds of billions of dollars in open interest, only one KPI remained: maximizing liquidation profits. Every extreme fluctuation presented a massive liquidation opportunity, and every liquidated user represented a precisely calculated potential income. Protecting user positions became voluntarily forgoing revenue.

"Slaughterhouses weren't created by a sudden decision to kill people; rather, slaughter was designed as a normal part of the system's operation."

8. Complaint

In December 2025, Xiao Daxia began systematically collecting victim information. As of the time of this writing, 383 victims had been registered, with total losses exceeding $303 million—and this is only a small fraction of those who actively sought redress; compared to the 1.66 million affected accounts, it's a drop in the ocean.

He hired two law firms, one in Hong Kong and one in the United States, to explore possible paths to class-action lawsuits against Binance and OKX. The road is difficult: both exchanges are registered in the Cayman Islands and Seychelles, respectively, and their user agreements contain lengthy arbitration clauses, meaning any jurisdictional dispute could drag on for years. If even former industry executives face such challenges, what about ordinary retail investors who lack resources, legal representation, and a voice?

But Master Xiao said that this battle must be fought.

Data Description

The data cited in this article comes from ARK Invest public reports, K33 Research research reports, a public statement from the CEO of Wintermute (now deleted), CoinGlass, CryptoQuant, and a Sina Finance roundtable interview. Neither Binance nor OKX has publicly responded to the data and mechanisms discussed in this article. All financial estimates are extrapolations based on publicly available data and are not audited results.