The stablecoin market is approaching its all-time high of $300 billion, but growth is showing signs of plateauing, with the traditional expansion logic driven by human transaction needs reaching its limit. The article points out that new growth will come from two main directions: first, on-chain yield-generating stablecoins (such as those pegged to RWA or government bonds); and second, automated on-chain payment scenarios driven by AI agents. Traditional payment giants such as Visa, Stripe, and Mastercard are accelerating their deployment of stablecoin infrastructure, and the industry focus is shifting from 'who issues stablecoins' to 'who builds a functional stablecoin network'.

Article author: imToken

Article source: Mars Finance

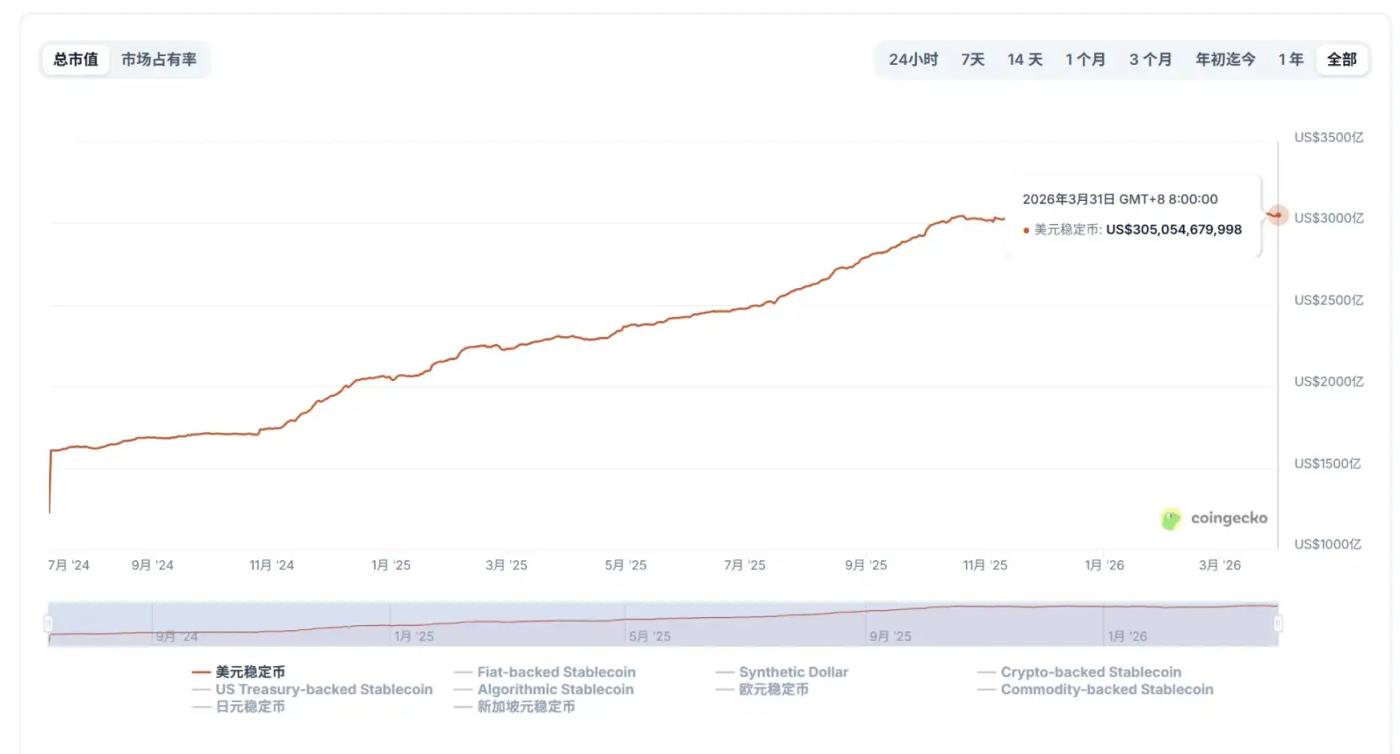

Stablecoins have been hovering around the all-time high of $300 billion for some time now.

The numbers are impressive, but a closer look reveals another side—over the past six months, the growth of stablecoins has begun to show signs of plateauing. This doesn't mean the market has lost its potential, but rather that the logic that supported the expansion of the past few years is quietly approaching its limits.

This means that stablecoins need a new story, not just a new scenario, but a deeper change in attributes: when payment scenarios are no longer just transactions, and even when the initiators are not just humans, what role will stablecoins play?

I. The Stuck Ceiling: Change and Constancy

This isn't the first time stablecoins have faced such a critical juncture.

From USDT to USDC, and then to various new stablecoins, the past rounds of expansion have almost always been accompanied by a few familiar scenarios: larger market trading volume, higher DeFi activity, stronger cross-chain liquidity, and broader global transfer demand.

On the surface, the growth of stablecoins comes from the expansion of the supply side, and this is not the first time stablecoins have reached such a juncture.

In the past few years, these core needs have almost entirely stemmed from human behavior. Whether it's the matching and buying/selling on exchanges, collateralized lending in DeFi protocols, cross-border transfers and arbitrage opportunities, or the short-term stopover of safe-haven funds, they all essentially revolve around the central theme of "trading." Ultimately, the growth of stablecoins in the previous phase was driven by "human trading needs."

The problem today is that these demands haven't disappeared, but they're getting closer to their "predictable ceiling." After all, the exchange landscape remains vast, but the competitive landscape has stabilized; DeFi is still important, but it's unlikely to create explosive growth on its own like it did in the early days; cross-border payments and arbitrage are still expanding, but it's more of a slow, gradual process than a new story that can reshape valuation expectations in the short term.

This is why there is a clear growing interest in the "next stablecoin system with an incremental growth story".

Currently, the new growth is mainly concentrated in two directions.

- One is on-chain yield-generating stablecoins, which combine stablecoins with structures such as government bonds, RWA, and protocol yields, and repackage their appeal by offering "holding and earning returns," similar to the interest-generating stablecoin path that has been repeatedly discussed in the market in recent years.

- Another area that has become significantly hotter recently is the on-chain business of AI Agents, and the demand for stablecoin payments and settlements surrounding them.

In comparison, on-chain payments and stablecoins are more in line with the characteristics of these new demands because stablecoins naturally possess several conditions that are difficult for traditional payment systems to match: 24/7 operation, globally unified settlement, programmability, support for high-frequency micro-payments, and no need for complex intermediaries and layer-by-layer authorization.

In other words, stablecoins may not only be competing for the existing cross-border payment market, but more likely for a larger incremental payment market in the future—especially when the initiators of payments are no longer just humans.

II. From Revenue-Driven to AI-Driven: Exploring New Growth Paths

Recently, traditional giants are clearly increasing their investment in this new direction.

Visa Crypto Labs, for example, launched its first experimental product, Visa CLI, attempting to enable AI agents to securely complete payment requests when writing code and calling services. Looking at this in a broader context, its significance lies not merely in adding another tool, but in the fact that the subject of payment is, for the first time, shifting from "humans" to "programs."

In traditional payment systems, all transactions implicitly require a human to initiate them. Whether it's a bank card, e-wallet, or mobile payment, they all rely on KYC (Know Your Customer) and manual authorization, with the final fund transfer completed by the bank's account system.

Ultimately, the design of this system is essentially built around "human behavior".

But AI does not belong to this system.

To complete a task, an AI agent may need to automatically subscribe to data services, pay API fees based on the number of calls, purchase computing resources across different platforms, and even execute automated transactions according to strategies. For such behaviors, waiting for manual human confirmation at each step is neither realistic nor suitable for its high-frequency, real-time operating rhythm. Furthermore, the traditional banking account system was not built for this kind of native machine-to-machine interaction.

This is precisely where the advantage of on-chain payments lies. Stablecoins like USDT and USDC are, in a sense, currencies inherently designed for AI. They are borderless, programmable, and capable of instant settlement, perfectly matching AI's ultimate pursuit of "high speed, low cost, and frictionless" transactions. This also means that the combination of stablecoins and wallets gives this type of payment true programmability for the first time.

This has given rise to a new form: the "Agent Wallet"—wallets are gradually evolving into asset interfaces and execution terminals for AI, and in practice, they are exhibiting several typical models (further reading: "From 'Collective Intelligence' to 'Super Individual': How AI Reshapes the DAO and Ethereum Ecosystem?").

- Non-custodial authorization: You can create an independent, restricted sub-wallet for your AI Agent, which can trade autonomously within the limits you set (e.g., no more than 500 USDC per transaction) without you having to manually confirm each time. The master key is always in your hands, and the AI is just your authorized agent.

- Cross-chain asset management: AI can query your assets on more than 100 chains in real time and rebalance, stake or arbitrage according to your set strategy, freeing you from tedious daily monitoring and allowing you to focus on higher-level strategic decision-making.

- Human-machine collaboration: This isn't about complete hands-off management, but rather supports flexible confirmation mechanisms—such as automatic small-amount transactions and alerts for large-amount transactions. AI is responsible for identifying opportunities and structuring trades, while you handle the final button press. This model perfectly combines human judgment with AI's execution efficiency.

III. From "Who issues stablecoins" to "Who organizes the network"

If Visa's experiment represents a change in demand, then Tempo, a blockchain project backed by Stripe and Paradigm, announcing the launch of its stablecoin mainnet, is more like an upgrade on the supply side.

Its importance lies not only in the fact that another stablecoin project has been added to the market, but also in reminding everyone that the focus of industry competition is no longer "who can issue stablecoins", but "who can truly organize stablecoins into a working network".

In the past few years, the first issue the stablecoin industry has addressed is issuance.

Major stablecoins such as USDT and USDC have completed the large-scale supply of on-chain US dollars, making "digital dollars" an asset class that can be used globally for the first time. However, as the supply gradually matures, what is truly scarce is no longer the stablecoin itself, but the ability to connect on-chain accounts, merchant payments, corporate payments, and fiat currency clearing networks.

This also explains why, from Stripe to Mastercard, and then to Visa and PayPal, traditional payment giants have been making intensive investments in stablecoins over the past two years, and even native crypto platforms have begun to penetrate TradFi:

- In October 2024, Stripe acquired Bridge, a stablecoin API service provider, for $1.1 billion, setting a new record for the largest merger and acquisition in the crypto payments sector at the time.

- In March of this year, Mastercard acquired stablecoin service provider BVNK for $1.8 billion, breaking this record.

- At the same time, Visa is also continuing to expand its partnership with Bridge to bring stablecoin-linked cards to a wider market;

- Looking further back, PayPal launched PYUSD even earlier, which clearly signaled its strategic intentions.

- In the Hong Kong market, licensed and compliant exchange OSL announced its transformation into a stablecoin payment and settlement infrastructure last year. In January of this year, it completed the acquisition of Web3 payment service provider Banxa. In February, it launched USDGO, an enterprise-grade USD stablecoin that complies with US federal regulations and can be compliantly distributed in Hong Kong.

Overall, Crypto and the broader payment industry have long since shifted their attitude towards stablecoins from "wait and see" to "positioning themselves."

This is why projects like Bridge, BVNK, OSL/USDGO, and today's Tempo, which attempt to build stablecoin network layers, suddenly seem so scarce. Their greatest value lies precisely in their position: connecting on-chain assets and wallets on one end, and merchants, businesses, payment service providers, and real-world clearing networks on the other.

The industry has moved beyond the initial stage of "who issues stablecoins" and entered the second half of the game: "who can make stablecoins truly take off".

In conclusion

The new high for stablecoins is not just a refresh of the scale figure; it is also like a watershed moment.

If the past few years have seen stablecoins address the question of "how people can make payments on the blockchain," then the next challenge they face is: how to network, scale, and automate the influence of stablecoins?

When AI can autonomously access wallets, when payments are embedded in programs, and when stablecoins become the default settlement currency in global trade, the upper limit of stablecoins will no longer depend solely on today's market trading volume, nor solely on the rate of replacement of existing cross-border payments. Instead, it may correspond to a much larger new variable.

Therefore, what truly matters for stablecoins in the next round is not just whether their supply will continue to reach new highs, but whether they can further evolve into a "global settlement interface".

This may be the real driver behind stablecoins breaking through new highs and reaching new plateaus.