Original author: ChandlerZ, Foresight News

During the Qingming Festival holiday, A-shares and Hong Kong stocks are closed, but Bitcoin's trading never stops.

Starting April 6th, BTC rose from a low of $67,400 in the early Asian session, reaching a high of over $70,300 during the session, a new high since March 26th, representing a gain of over 4% from the daily low. Ethereum rose from around $2,050 to $2,170 during the same period, a gain of approximately 6%, and remained above $2,140 at the close of the US stock market, a 24-hour increase of nearly 4%.

According to CoinGlass data, total liquidations across the network amounted to approximately $229 million in the past 24 hours, including $127 million in short positions and $102 million in long positions. When BTC broke through $69,000, approximately $136 million in short positions were concentrated around $69,863, and the surge directly triggered a large-scale short liquidation.

Holiday market trends are dominated by the Middle East situation.

The macroeconomic logic driving this round of price increases remains Iran, but the circumstances have changed.

On March 21, Trump gave Iran a 48-hour deadline to reopen the Strait of Hormuz, but then extended it by more than a week, instead announcing the start of diplomatic negotiations. In the following weeks, he oscillated between "reopening the Strait with an agreement" and "reopening the Strait without an agreement," with markets fluctuating wildly with each headline. April 7 at 8 p.m. was his second final deadline, this time with escalated rhetoric: if no agreement was reached by then, Iran would "live in hell," and he threatened to strike energy infrastructure and civilian targets.

Meanwhile, U.S. Defense Secretary Hergsays announced at a press conference on April 7 that the largest airstrikes since the start of the Iranian operations would be launched that week. However, at the same press conference, Trump stated that Iran had active and willing negotiators and revealed that the U.S. and Iran were discussing a two-phase plan: first, a 45-day temporary ceasefire, followed by negotiations on a comprehensive agreement. Iran, however, publicly rejected the temporary ceasefire, insisting on a permanent end to the war, leading to a stalemate in the negotiations.

When asked if he was gradually ending the war, Trump replied, "I don't know, I can't say for sure. It depends on their (Iran's) actions."

Affected by this macroeconomic environment, the international market has also experienced fluctuations.

WTI crude oil futures for May delivery closed at $112.41 per barrel, marking a new high since June 2022 for the second consecutive trading day; Brent futures settled at $109.77 per barrel. Crude oil prices fluctuated repeatedly after briefly touching $115.48 in Asian trading, reflecting significant market disagreement regarding the continued navigability of the Strait of Hormuz.

In the US stock market, the S&P 500 closed up 0.44% and the Nasdaq closed up 0.54%, both hitting at least two-week highs. The chip stock index rose more than 1%, with Micron and SanDisk rising more than 3%. The VIX closed at 24.15, a slight increase from the previous day.

This seemingly contradictory combination of rising oil, stock, and currency prices is logically consistent. The market's pricing that day wasn't in an escalation of the war, but rather in the averting of the worst-case scenario. The news of a 45-day temporary ceasefire temporarily averted the tail risk of a systemic collapse, leading to a collective recovery in risk appetite and a synchronized rebound across all three asset classes. Oil prices remained high because the Strait of Hormuz hadn't yet reopened to navigation, but the price increase was no longer accelerating; in other words, the market had found a temporary equilibrium point where things wouldn't get worse, but a better one hadn't yet emerged.

Interactive Brokers Chief Strategist Steve Sosnick commented, "The market sees both the carrot and the stick; on one hand, there are ceasefire negotiations, and on the other hand, there is continued bombing. Aside from the brief fluctuations in the initial period after Trump's speech, investors clearly still hope that hostilities will not escalate rapidly."

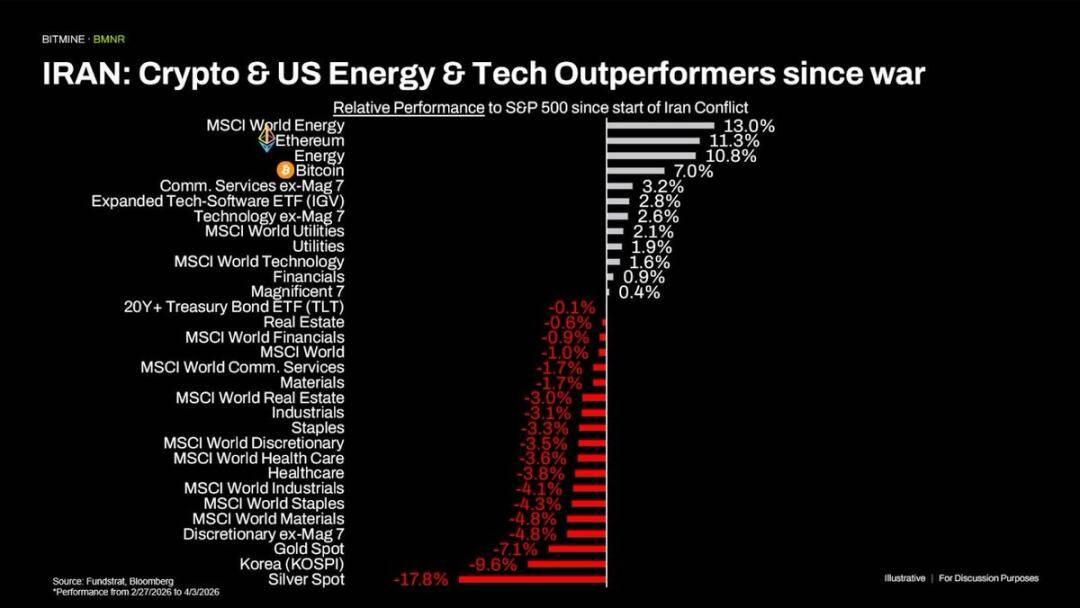

It is worth noting that this pattern has held true since the outbreak of the war in Iran. From February 27, when the war began, to April 3, the top four performers relative to the S&P 500 in terms of excess returns were MSCI World Energy (+13.0%), Ethereum (+11.3%), U.S. Energy Sector (+10.8%), and Bitcoin (+7.0%).

Conversely, the performance of traditional safe-haven assets was surprising. Gold fell 7.1% relative to the S&P 500, and silver fell 17.8%, completely contrary to the market inertia of "buying gold as a safe haven" in previous rounds of geopolitical conflicts.

The on-chain structure has improved, but new funding has not yet followed.

The Glassnode report indicates that the internal structure of this rebound is beginning to show signs of repair, momentum is strengthening, spot demand is stabilizing, and overall market losses have significantly decreased.

The spot market reflected early signs of a demand recovery, with the Spot CVD turning from -$47.8 million to +$27.9 million, shifting from net selling pressure to net buying pressure. The Relative Strength Index (RSI) rebounded strongly, and the Spot CVD turned positive, indicating a renewed buying interest. However, declining trading volume suggests that market participation remains relatively low, indicating that while the recovery momentum is good, it is not yet fully confirmed.

The adjustment in derivatives market positions was not significant, with a decrease in open interest and a cooling of long positions, indicating lower leverage and a more balanced market environment. Perpetual CVD contracts rebounded sharply from -$412 million to $461 million, demonstrating a clear directional bias in the futures market. Open interest fell from $30.3 billion to $29.7 billion, indicating that excessive leverage was not observed.

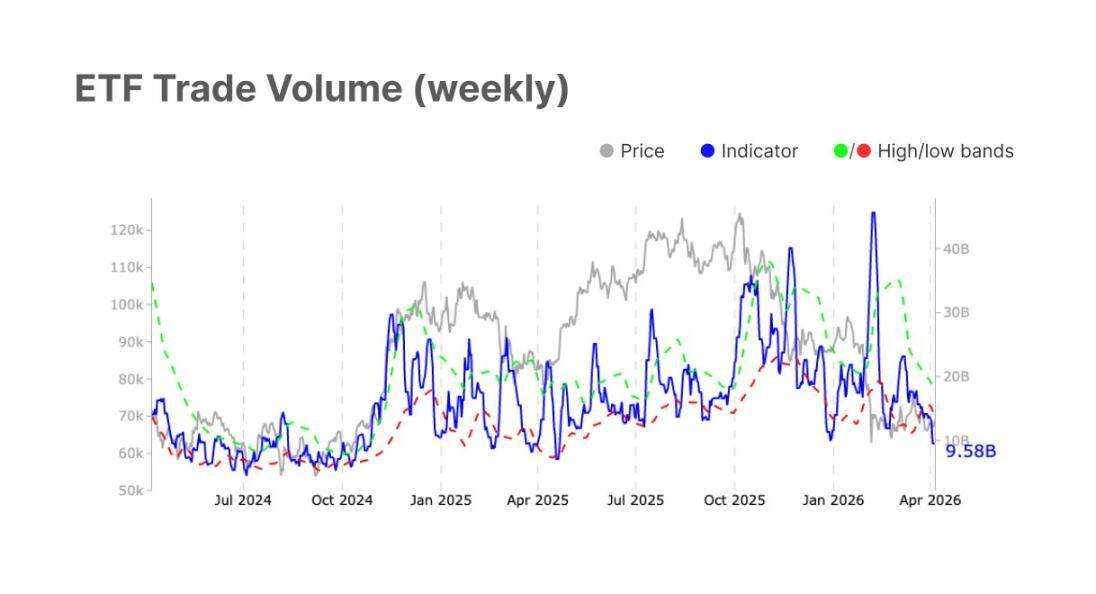

The liquidity situation of ETFs has improved significantly. The net outflow of US spot Bitcoin ETF narrowed sharply from -$405 million to -$22 million, a decrease of nearly 95%. The ETF MVRV rose from 1.10 to 1.16, and institutional holdings have increased their floating profits.

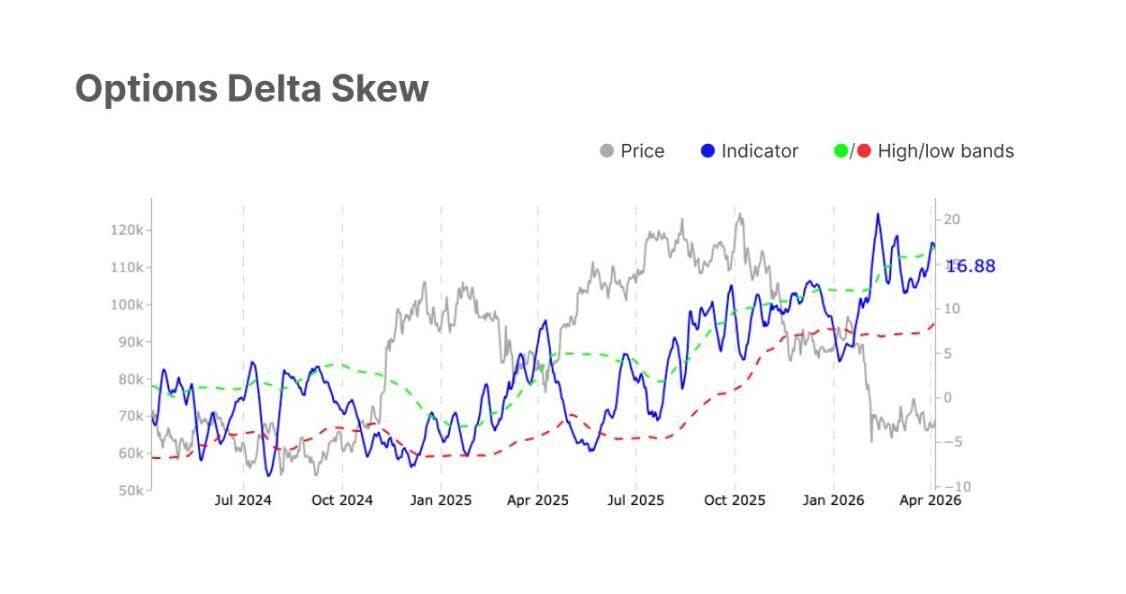

However, the recovery of on-chain fundamentals remains lagging. The realized market capitalization change further decreased from -0.6% to -0.7%, indicating that new funds have not yet flowed back in on a large scale. Hot Capital Share decreased from 21.0% to 20.1%, indicating a continued outflow of short-term speculative funds. The 25-Delta skew rose to 16.88%, indicating that the pricing of downside risk in the options market has not subsided due to the price rebound.

Crypto Market Aftermath

Can the market rally continue? Institutional opinions are divided.

CoinDesk, citing analysts, stated that unless Bitcoin can recover to $75,000, the risk of falling to lower levels remains; if the current price cannot hold above $70,000, it will face a new round of downward pressure after short-term holders lose confidence.

Glassnode's conclusion was relatively cautious, stating that the rebound momentum had improved, spot demand had stabilized, and selling pressure at a loss had significantly decreased. However, participation remained weak across exchanges, ETFs, and on-chain metrics, indicating that market confidence had not yet fully recovered. For this rally to stabilize, further increases in trading volume, capital inflows, and network activity are needed.

April 7th is the deadline set by Trump. Whether the situation deteriorates substantially after the deadline will directly determine the next direction of oil prices and risk assets, and will also be a key variable in whether Bitcoin can hold onto $70,000.