Author: @BlazingKevin_, Blockbooster Researcher

The integration of Web3 and AI is moving beyond its early stages. Market scrutiny of the AI crypto space is shifting from early "hype" to "fundamentals and technological implementation." In this shift, projects demonstrating remarkable resilience and technological breakthroughs are reshaping market valuations.

1. Bittensor firmly establishes its leading position.

The current total market capitalization of the AI cryptocurrency sector is approximately $17.46 billion, with a 24-hour trading volume of nearly $1.94 billion. Within this sector, Bittensor (TAO) firmly holds the top position with a market capitalization of approximately $3.43 billion. It accounts for nearly 19.6% of the entire AI cryptocurrency market share, establishing its absolute leading position.

A direct comparison with core competitors reveals its niche:

| competitors | Tokens | Market capitalization (USD billion) | Core positioning | Differentiation from TAO |

|---|---|---|---|---|

| Bittensor | TAO | 34.3 | Decentralized AI Incentive Network | |

| NEAR Protocol | NEAR | 14.9 | High-performance L1 public chain | General-purpose public blockchains, with AI as part of their ecosystem. |

| Render Network | RENDER | 8.64 | Decentralized GPU rendering/computing | Pure computing infrastructure, without AI quality incentives |

| Fetch.ai (ASI) | FET | 5.33 | Autonomous AI Agent Network | Focus on AI application layer, not underlying model training |

| Akash Network | AKT | 1.26 | Decentralized cloud computing market | The general computing power market lacks complex AI consensus mechanisms. |

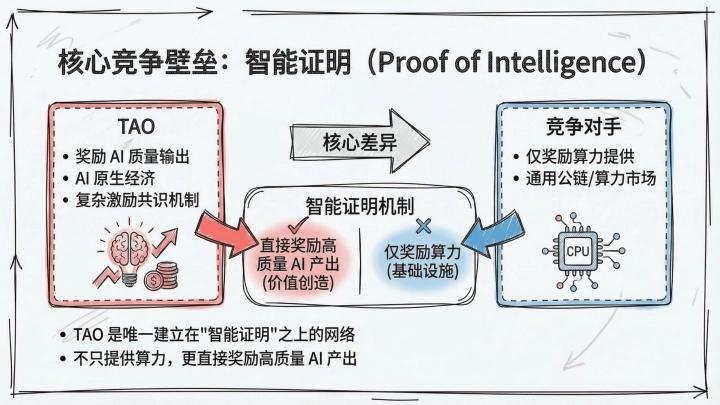

Core competitive barriers

Bittensor's core competitive advantage lies in its unique "Proof of Intelligence" network. It transcends the framework of simply providing computing power. The network introduces a complex incentive mechanism that directly rewards the production of high-quality AI models. This unique positioning makes it extremely difficult to replicate among competitors.

2. Verification of Real "Self-Growth" Capability and Reshaping of Valuation Logic

Leaving aside grand technological visions, the key to testing the Web3 protocol's ability to weather market fluctuations lies in its actual commercial expansion and revenue generation capabilities.

In the crypto market, Bittensor has demonstrated a rare ability to generate real revenue. According to data from the first quarter of 2026, the Bittensor network generated approximately $43 million in revenue from genuine AI clients (non-token-incentivized fake transactions). This figure surpasses the annual revenue of many traditional Web3 protocols.

Key valuation metrics (as of March 29, 2026):

| index | numerical values | illustrate |

|---|---|---|

| Circulating market capitalization | ~$3.42 billion | Based on a circulation of approximately 10.78M |

| Fully diluted valuation | ~$6.68 billion | Based on a total supply of 21M |

| Q1 2026 Real Income | ~$43 million | Non-token incentives, real AI customer payments |

| Annualized income calculation | ~$172 million | Linear extrapolation based on Q1 data |

| Price-to-Sales Ratio (P/S) | ~20x | Based on circulating market capitalization/annualized revenue |

| FDV/Annualized Income | ~39x | Based on FDV/Annualized Revenue |

| Total market value of subnet ecosystem | ~$1.47 billion | Total market capitalization of dTAO Alpha tokens |

Traditional centralized AI infrastructure companies typically enjoy forward revenue valuations of 15-25x in the private market. Bittensor possesses high liquidity premiums, network effects, and scarcity narratives. Its current P/S multiple of approximately 20x is within a reasonable or even undervalued range. The total market capitalization of its subnet tokens within its ecosystem has reached $1.47 billion. This ecosystem structure, in turn, contributes to the value capture of the mainnet TAO.

3 SN3 Breakthrough

Financial data established the lower limit of the protocol's valuation. Technological breakthroughs in decentralized training have completely opened up the potential for its market capitalization.

The core driving force behind TAO's recent surge against the market trend is by no means simply speculative trading. A historic breakthrough has been achieved in its underlying technology. Its valuation logic has undergone a fundamental shift from "narrative-driven" to "product-driven."

3.1 Covenant-72B Verifies the Feasibility of Decentralized Training

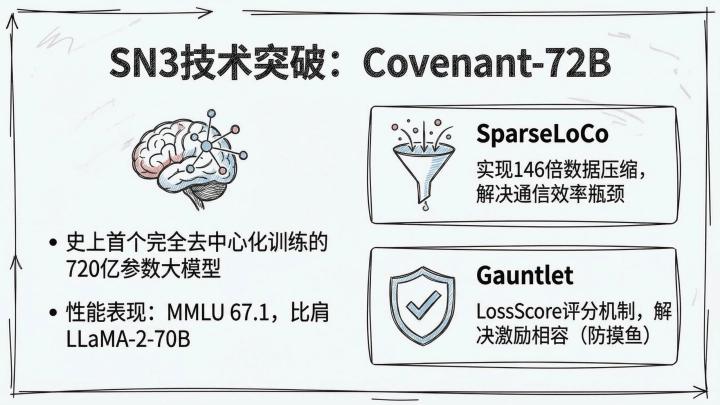

On March 10, 2026, Templar (SN3), a subnet of the Bittensor ecosystem, and the Covenant Labs team behind it released a technical report on arXiv. The team announced the successful pre-training of the Covenant-72B large language model. This is the largest-scale dense architecture model trained to date in a completely decentralized, permissionless internet environment.

This model boasts 72 billion parameters and is trained on 1.1 trillion tokens. Its MMLU score reaches 67.1, with basic performance comparable to Meta's LLaMA-2-70B. This model overcomes the communication bandwidth bottleneck of decentralized training. The introduction of the SparseLoCo algorithm played a crucial role. Nodes only need to transmit 1%-3% of the core gradient components and perform 2-bit quantization, achieving over 146 times data compression (compressing 100MB of data to less than 1MB). Under normal internet bandwidth, the computational utilization remains as high as 94.5%. This milestone demonstrates that globally distributed heterogeneous computing power can produce commercially competitive cutting-edge models. This technical solution eliminates reliance on expensive InfiniBand leased lines and centralized supercomputing clusters.

The success of Covenant-72B quickly caused a stir in the traditional AI community:

- Anthropic co-founder Jack Clark highly praised the breakthrough, citing it extensively in his research report on March 16th. He characterized it as "challenging the political economy of AI through distributed training." He noted that this is a technology worth continuing to track and predicted that future on-device AI will widely adopt such decentralized training models.

- Jensen Huang's "Folding@home" analogy: On March 20th, during the All-In VC podcast, Chamath introduced Bittensor's technological achievements to NVIDIA CEO Jensen Huang. Huang responded positively, comparing it to a "modern version of Folding@home" and affirming the necessity of coexisting open-source and distributed models.

3.2 Two core components of SN3: solving the problems of communication efficiency and excitation compatibility

Dozens of distrustful nodes with varying hardware and network quality collaboratively train the same 72B model. SN3 solves the challenges of communication bandwidth and malicious attacks through two core components:

- SparseLoCo (solves communication efficiency issues): Traditional distributed training requires synchronizing complete gradients at every step, resulting in massive amounts of data. SparseLoCo allows each node to run 30 steps of internal optimization (AdamW) locally. The nodes then compress and upload the resulting "pseudo-gradients." The system employs Top-k sparsity (retaining only 1%-3% of the core gradient components), error feedback, and 2-bit quantization. This process achieves over 146 times data compression (compressing 100 MB of data to less than 1 MB). Under normal internet conditions (110 Mbps upload, 500 Mbps download), the system maintains a computational utilization of 94.5%. Each communication round takes only 70 seconds.

- Gauntlet (solves incentive compatibility): This component runs on the Subnet 3 blockchain. It is responsible for verifying the quality of pseudo-gradients submitted by each node. The system uses a small batch of data to test the "degree of reduction in model loss after using the node's gradient" (LossScore). The system also checks whether the node is training on the allocated data (to prevent cheating). Each round of aggregation only selects the gradient from the node with the highest score. This mechanism fundamentally solves the problem of "how to prevent miners from slacking off" in decentralized scenarios.

4. The Super Leverage of Subnet Ecosystem and dTAO Mechanism

Bittensor launched the Dynamic TAO (dTAO) mechanism in 2025. This mechanism played a key "amplifier" role in this surge. dTAO allows each subnet to issue its own independent alpha token. Subnets establish liquidity pools with TAOs through an Automated Market Maker (AMM) mechanism.

4.1 Leverage effect of subnet tokens

Under the dTAO mechanism, the price of a subnet's token is directly determined by the amount of TAO reserves staked in that subnet's pool. As TAO appreciates, the underlying reserve value of all subnets increases accordingly. The price of the subnet's token then passively rises. This surge in subnet token prices attracts more speculative and staked funds to buy TAO and lock it into the subnet. The system thus forms a strong positive feedback loop.

| Core subnet tokens | 30-day price increase | Core Business Positioning |

|---|---|---|

| Templar (SN3) | +444% | Distributed pre-training of large models |

| OMEGA Labs | +440% | Multimodal data collection and mining |

| Level 114 | +280% | - |

| BitQuant | +230% | - |

| Targon | +166% | Computing power and inference services |

As shown in the table above, directly stimulated by the success of Covenant-72B, the SN3 (Templar) token surged by over 440% in a single month, reaching a market capitalization of $130 million. This wealth-creating effect at the subnet level is evident. The total market capitalization of the subnet tokens reached $1.47 billion by the end of March, with daily trading volume exceeding $118 million. This effect, acting as a form of "super leverage," transmitted the enormous buying pressure back to the TAO coin.

4.2 Integration of Vertical Ecosystems

While operating SN3, Covenant Labs has also established SN39 (Basilica, focusing on computing power services) and SN81 (Grail, focusing on post-training and evaluation of reinforcement learning). This vertical integration covers the entire process from pre-training to alignment optimization. This strategy demonstrates to the market the complete decentralized AI industry chain loop that has already formed within the Bittensor ecosystem.

5. Chip Distribution

Based on the latest on-chain data from taostats and CoinMarketCap as of March 29, 2026, the health of the Bittensor network can be assessed in depth from the following dimensions:

| On-chain metrics | Data performance | Evaluation and Insight |

|---|---|---|

| Pledge ratio | 68% - 75% of the circulating volume | The extremely high pledging ratio (approximately 7.34 million TAO tokens locked) significantly reduced the actual circulating supply in the market. A strong supply-tightening effect was created, supporting the upward price spiral. |

| Subnet activity | 128 active subnets | The ecosystem is thriving. Top subnets such as Templar (SN3) and Targon (SN4) have achieved independent market capitalizations of hundreds of millions of dollars. This data demonstrates the success of subnet tokens as "leveraged bets" under the dTAO mechanism. |

| Alpha token total market capitalization | ~$1.47 billion | This data represents a more than 50-fold increase since dTAO's launch, reflecting the market's high level of acceptance of the subnet ecosystem. The mainnet TAO continues to receive strong demand support. |

| validator concentration | Head validators account for the majority of the weight. | tao.bot, Taostats, and the OpenTensor Foundation hold significant weight, indicating a degree of centralization. The deep integration of core network builders with the network is also evident. |

| Daily trading volume | Approximately $241 million | The trading volume to market capitalization ratio is approximately 7.03%. Liquidity is extremely abundant. Market trading is active. Institutional and retail investor participation is high. |

| Deploy AI agents within 90 days | 14,500 | The actual growth in network usage is reflected in this data. This is an important indicator for measuring real demand. |

Overall evaluation based on on-chain data:

Bittensor's on-chain data exhibits characteristics of an extremely healthy economy. High staking rates lock in liquidity. Real revenue supports fundamentals. The dTAO mechanism stimulates subnet innovation. Continuous supply-side tightening (including halving and high staking) combined with continuous demand-side growth (including institutional entry and AI-driven narrative enhancement) constructs a highly advantageous price dynamics model.

6. Valuation Concerns

It is important to note that the transparency of on-chain data is mainly reflected on the supply side, while the off-chain characteristics of the demand side (actual AI service call volume) remain a significant information blind spot.

Risk 1: High Token Subsidies Mask True Business Costs. Currently, most subnets' low-priced services heavily rely on TAO token inflation subsidies. Take the leading inference subnet Chutes (SN64) as an example. The ratio of issuance subsidies to external revenue on this network is as high as 22-40:1. Excluding token subsidies, its actual service pricing far exceeds that of centralized competitors. Compared to platforms like Together.ai , its service premium is 1.6 to 3.5 times. The continued progress of subsequent halving cycles will fully expose the fragility of this business model.

Risk 2: Lack of a Commercial Moat Leads to High User Attrition. The Bittensor network primarily provides open-source models and standardized APIs. This model differs fundamentally from traditional cloud giants like AWS. The ecosystem severely lacks proprietary platforms, deep enterprise integration, or data flywheels—traditional "lock-in effects." Developer migration costs are extremely low. Once token subsidies are phased out, price-sensitive B2B users will rapidly leave. Lower-cost centralized computing platforms will easily absorb this exodus.

Risk 3: Valuation Disconnect Risk After Data Deflatoring Regarding the aforementioned $43 million in Q1 revenue, some prudent institutional research has offered drastically different calculation models. Excluding related-party transactions and subsidies within the ecosystem, and only considering rigorously verified genuine external fiat currency revenue, the network's annualized revenue could plummet to between $3 million and $15 million. Using this deflated, genuine revenue base, the network's actual price-to-sales ratio (P/S) would surge to an extremely dangerous range of 175-400 times. The risk of a valuation bubble burst objectively exists.