Institutional finance has historically required a payment layer to transfer money between organizations. For decades, this layer has been correspondent banking: bank to bank, taking one to three days, excluding weekends.

In 2025 alone, stablecoins processed $33 trillion in transactions – nearly double the total value of Visa's payments in a single year. JP Morgan paid off its debt with USDC on Solana. Visa processed $3.5 billion in USDC through US banks.

PayPal has also launched its own stablecoin in 70 markets. This payment class has truly revolutionized the industry. This article will look back at how stablecoin infrastructure has replaced traditional methods, and who built the "railway" that institutional finance now relies on.

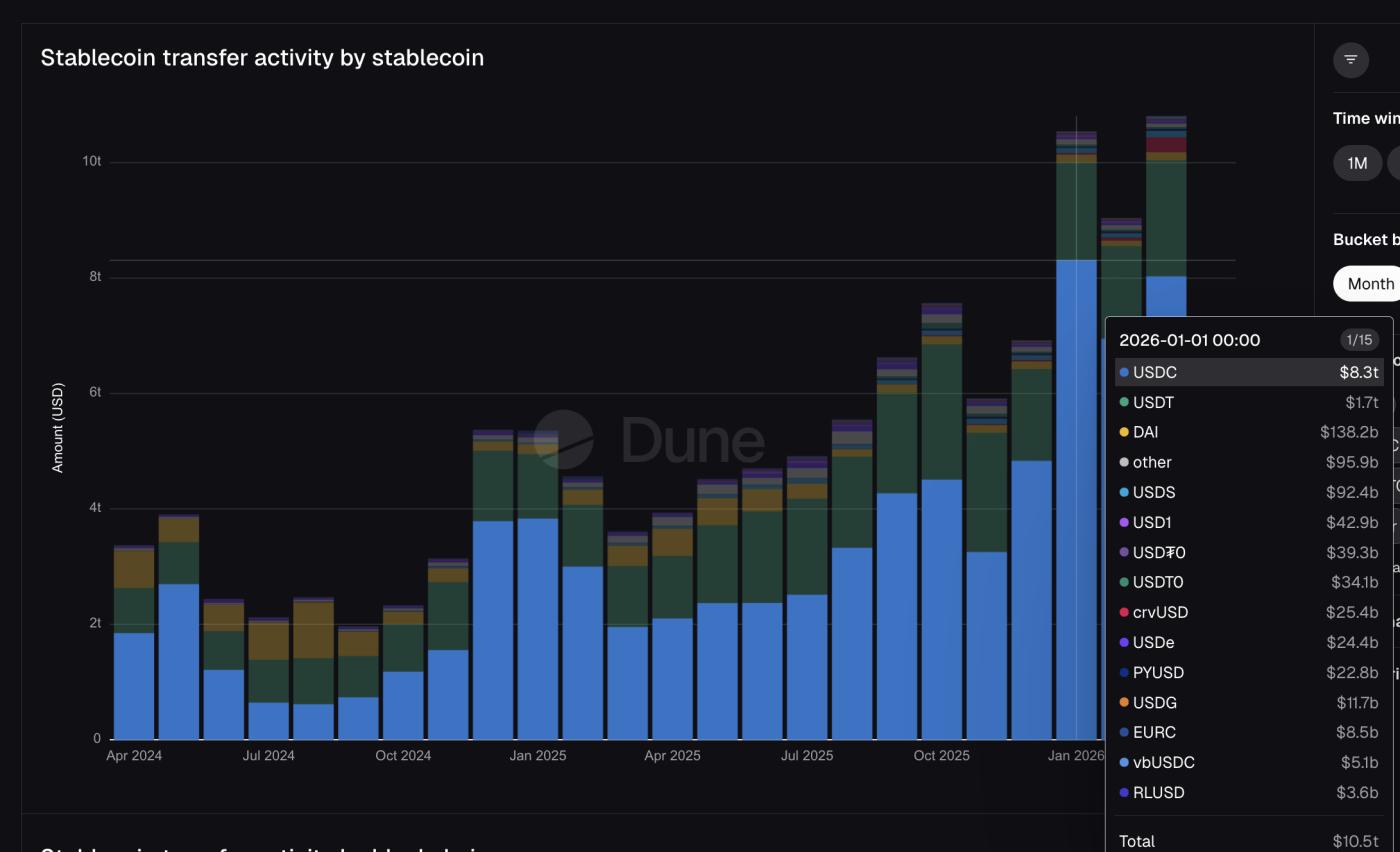

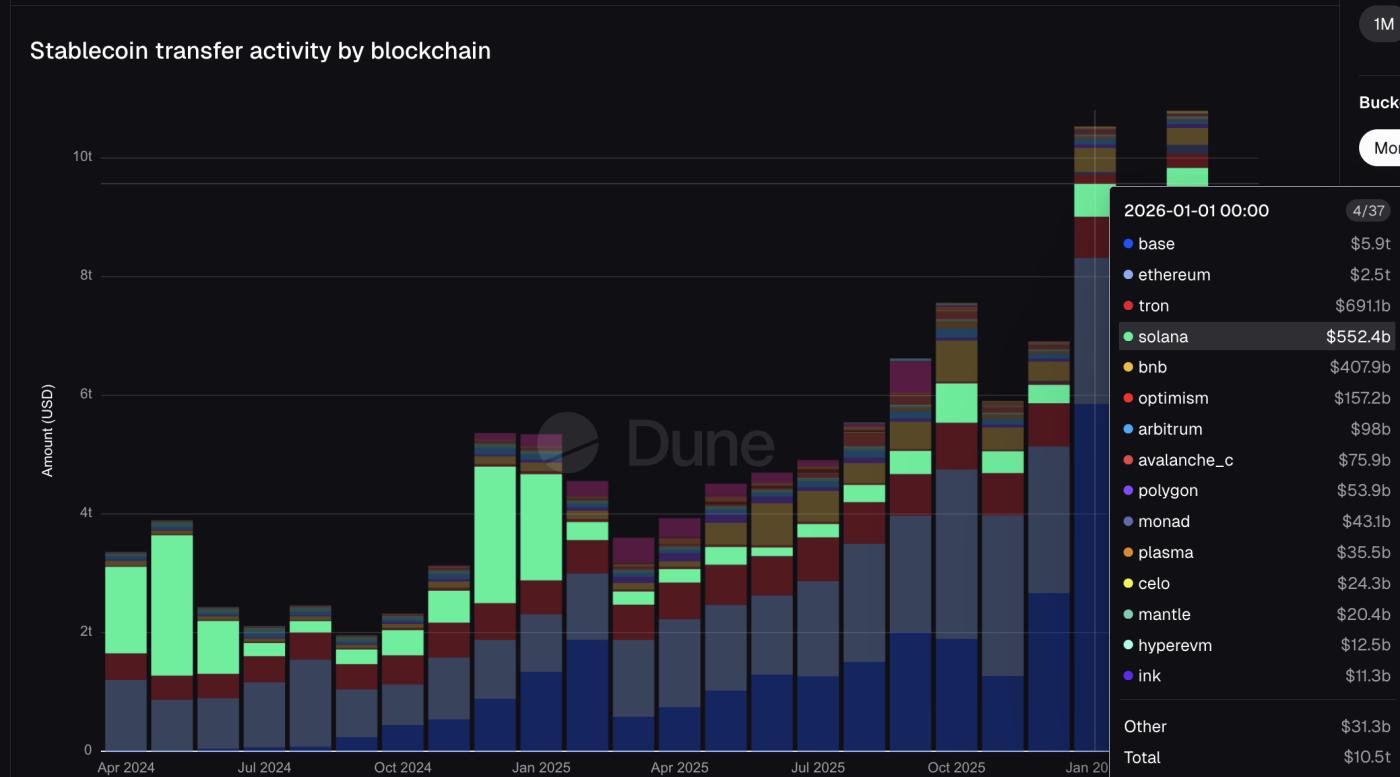

$10.5 trillion in just one month – institutions leading the game.

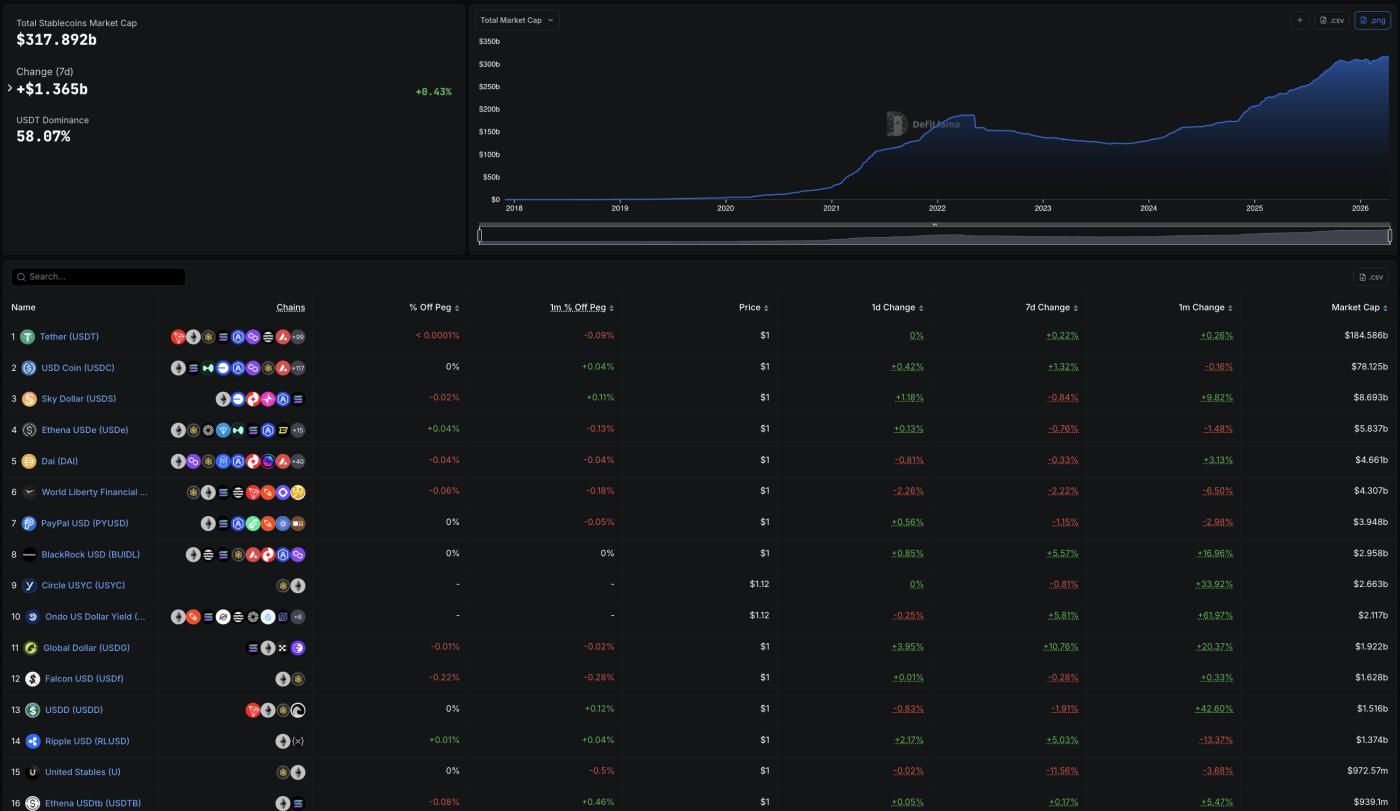

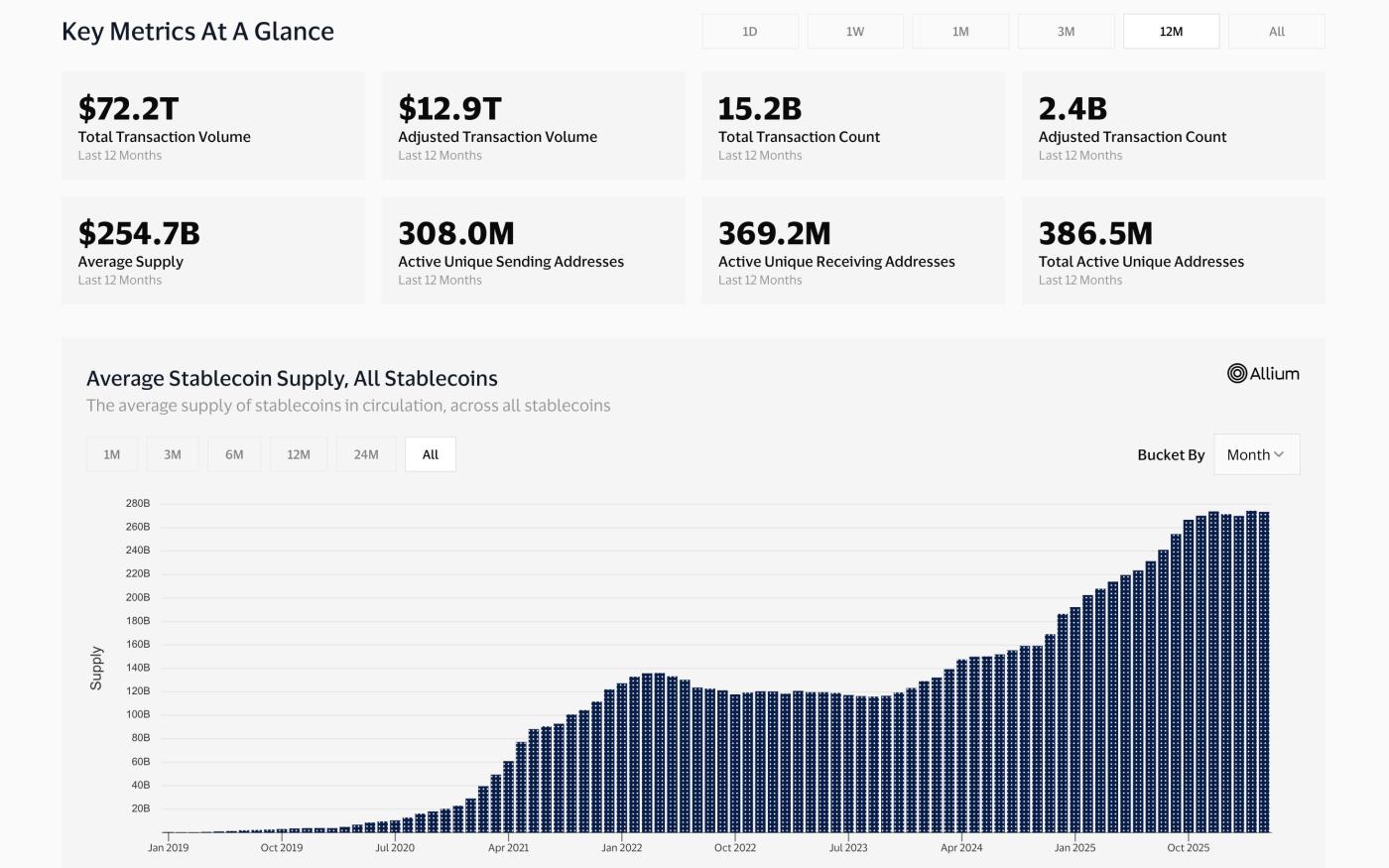

The total market Capital of stablecoins reached $317.89 billion in April 2026, a significant increase from approximately $125 billion at the beginning of 2024.

The GENIUS Act, signed into law in mid-2025, created a federal legal framework for payment-related stablecoins, giving large institutions more confidence to enter the market. Since then, stablecoin growth has been "vertical."

defillama market Capital : defillama

defillama market Capital : defillamaAccording to data from Dune Analytics, stablecoins transferred $10.5 trillion in January 2026 alone. To put this into perspective, Visa processed a total of $16.7 trillion in fiscal year 2025 through its fiat payment system.

Mastercard processed $10.6 trillion during the same period. Thus, in just one month, the volume of stablecoin transfers on the public blockchain nearly equaled the volume Mastercard processed in fiat currency in an entire year.

Stable transfer activity: Dune

Stable transfer activity: Dunedefillama 's ranking clearly shows the influence of large institutions. PayPal's PYUSD holds the 7th position with a supply of $3.95 billion. BlackRock's BUIDL ranks 8th with $2.96 billion.

USDG – a stablecoin partnered with Mastercard – ranks 11th with $1.92 billion. These are not purely crypto Token – they are all stablecoins issued or affiliated with traditional financial giants, ranking alongside familiar ones like USDT and USDC .

USDC transferred $8.3 trillion in January alone, nearly five times more than USDT $1.7 trillion, despite having a supply 2.7 times smaller. USDT dominates in terms of holdings, while USDC leads in volume.

This distinction is significant because USDC is the stablecoin Visa chooses for payments , JP Morgan uses for Galaxy debt transactions , and Stripe's infrastructure also utilizes it . The entire institutional payments layer now largely runs on a single Token issued by Circle .

In addition, PayPal's PYUSD traded $22.8 billion, while Mastercard's USDG reached $11.7 billion. The major traditional stablecoins are now clearly visible on the trading volume charts, and they all share a common link to just two issuers.

Two publishers, one "track," and completely bypassing the banking system.

Circle and Paxos are the two main issuers. Circle issues USDC – a Token that transferred $8.3 trillion in January alone. Paxos is responsible for PayPal's PYUSD and USDG for the Mastercard-backed Global Dollar Network, along with partners such as Robinhood, Kraken , and DBS Bank. Most major traditional stablecoin integrations connect to either Circle or Paxos.

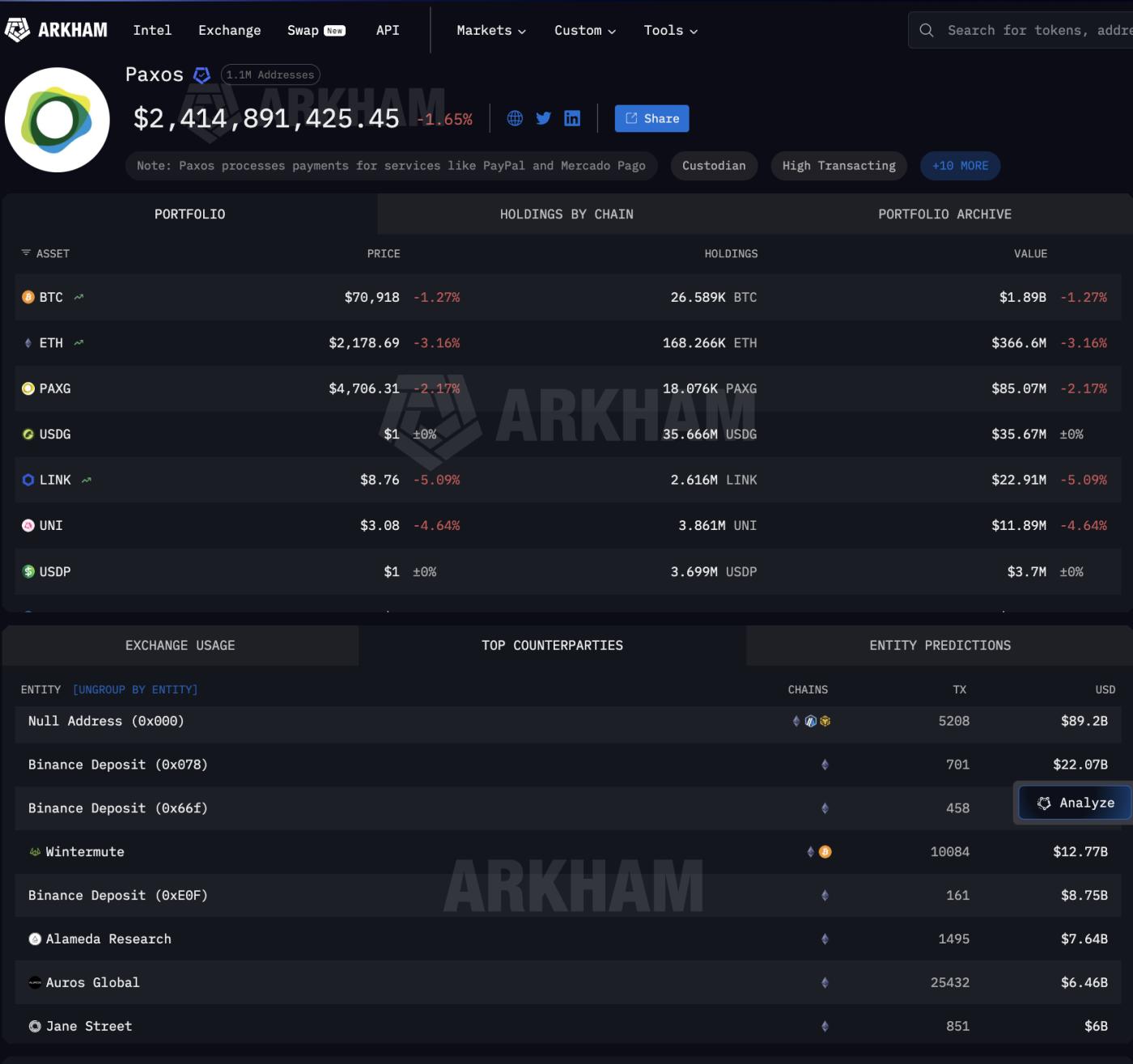

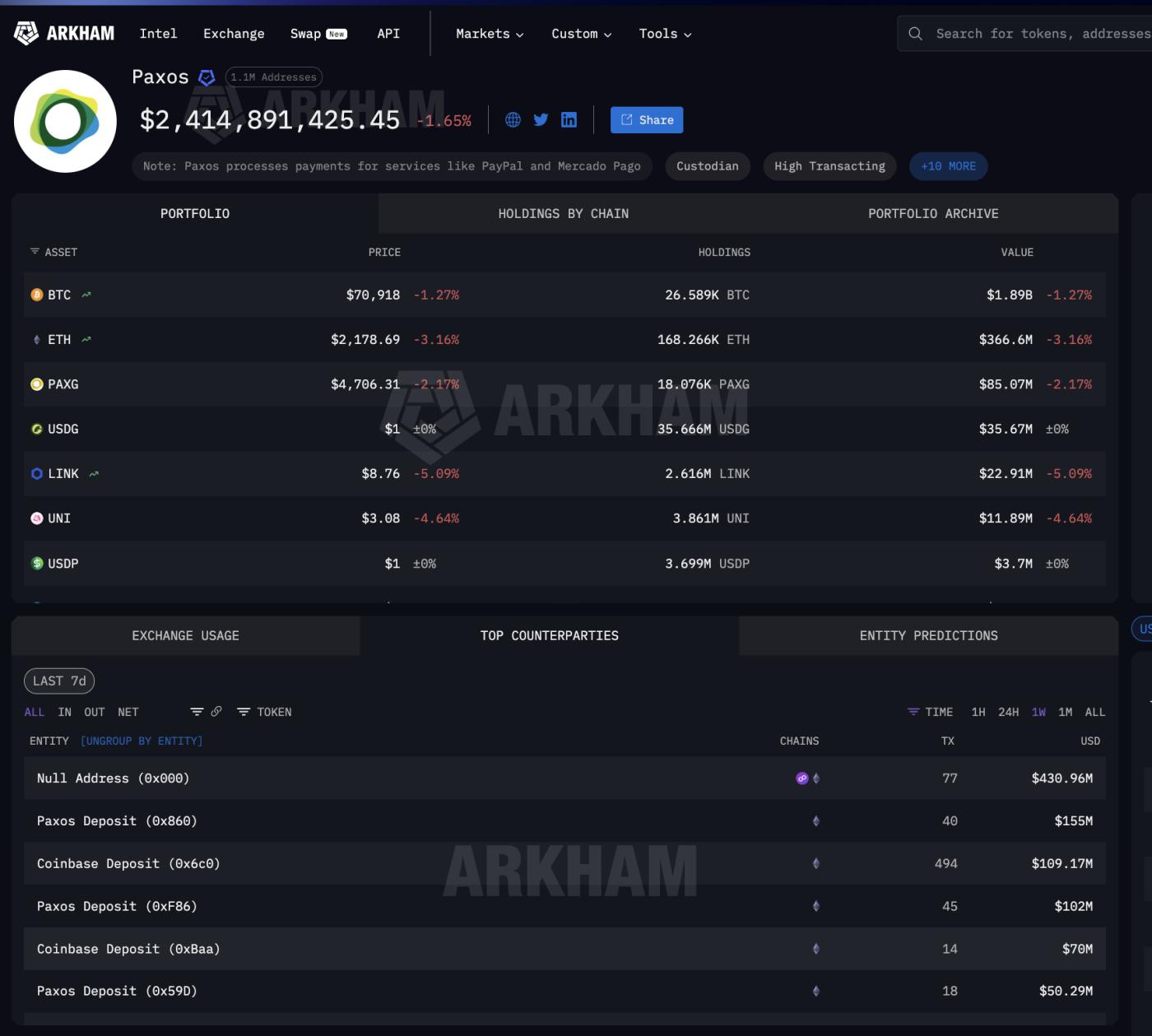

Data from Arkham Intelligence reveals what happens after the issuance. Paxos has moved out $89.2 billion through 5,208 Token issuance and burning transactions. The recipients of the funds are not banks.

These include Binance ($22 billion), Wintermute ($12.77 billion), Jane Street ($6 billion), Coinbase ($2 billion), and other major players.

These are Wall Street's leading market makers and crypto-based trading desks – not the old-fashioned correspondent banking chain .

Paxos' receiving partner page (page 1): Arkham Intelligence

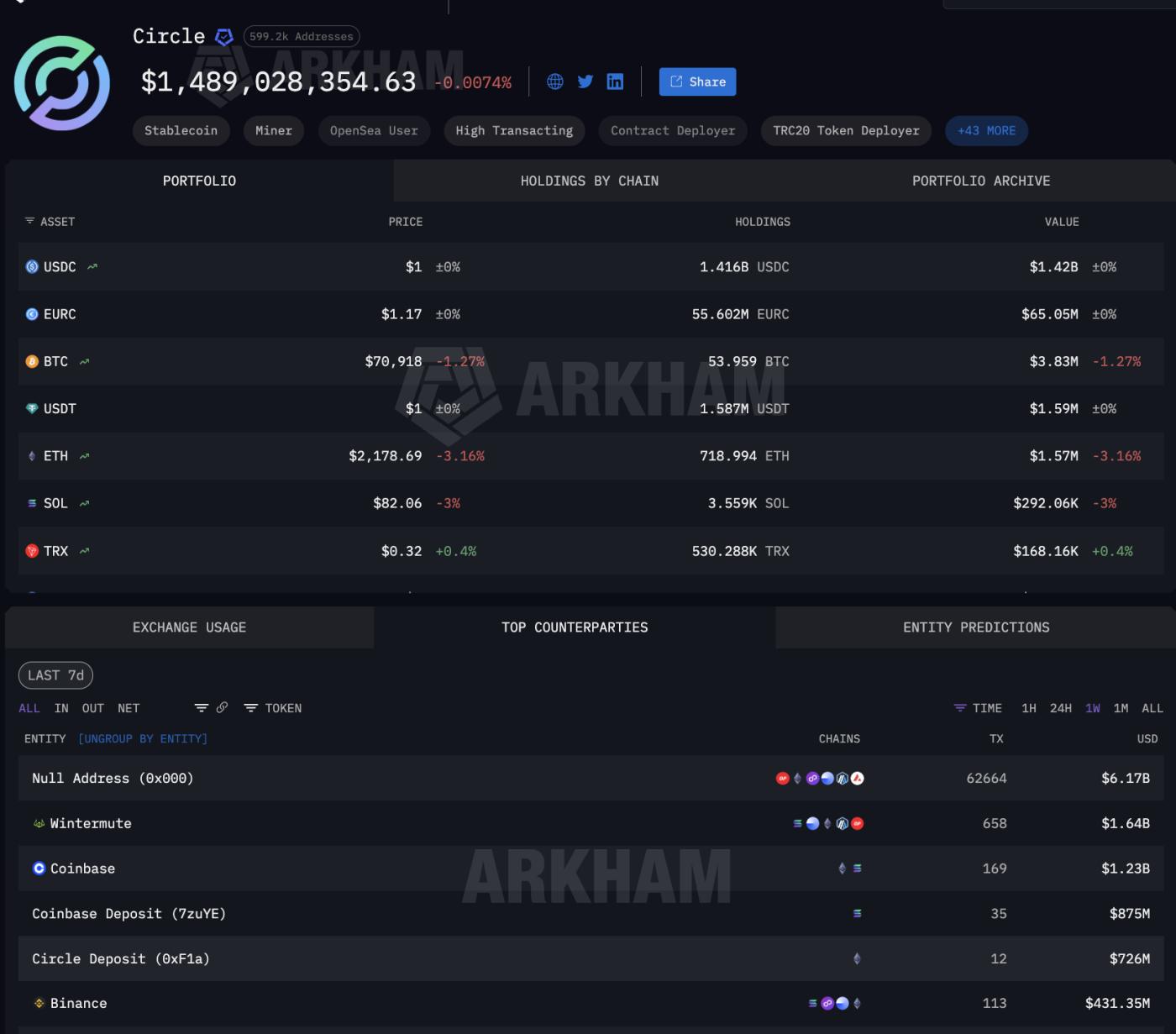

Paxos' receiving partner page (page 1): Arkham IntelligenceCircle 's partner data also shows the same pattern: $6.17 billion through Token issuance and burning transactions. Wintermute received $1.64 billion. Coinbase received a total of $2.1 billion across various deposit addresses.

Coinbase emerged as the largest partner for both issuers, being the only distributor involved on both sides of the traditional payments market (TradFi).

Circle's partners: Arkham Intelligence

Circle's partners: Arkham IntelligenceThe outflow of funds from Paxos and Circle primarily comes from Token minting and burning, a mechanism by which stablecoin issuers create new Token when customers need them or burn them when customers redeem them. The size of the partners will indicate the position of large payment transactions within the financial institution.

When large companies receive billions of dollars from Paxos, it's typically in the form of newly minted stablecoins for purposes such as paying PayPal merchants, fulfilling obligations to Mastercard recipients, or providing liquidation to Visa's banking partners. These stablecoins are created solely for payment purposes and are redeemed shortly thereafter.

Such instantaneous processes don't exist in the correspondent banking model. That's why stablecoin infrastructure is becoming the new payment network. So where do stablecoins sit between being minted and awaiting destruction?

Between minting and burning, stablecoin infrastructure relies on digital asset custody.

Therefore, the stablecoin infrastructure serving financial institutions depends not only on who mints the Token, but also on where these Token are stored while awaiting use or exchange. USDC is used by millions of people, making it difficult to pinpoint exactly which holdings belong to large institutional transactions.

However, USDG is different. This Token serves only one purpose: to serve the Global Dollar Network, where Mastercard, Robinhood, Kraken , and DBS Bank are core partners. Therefore, every major USDG holder is directly tied to this network.

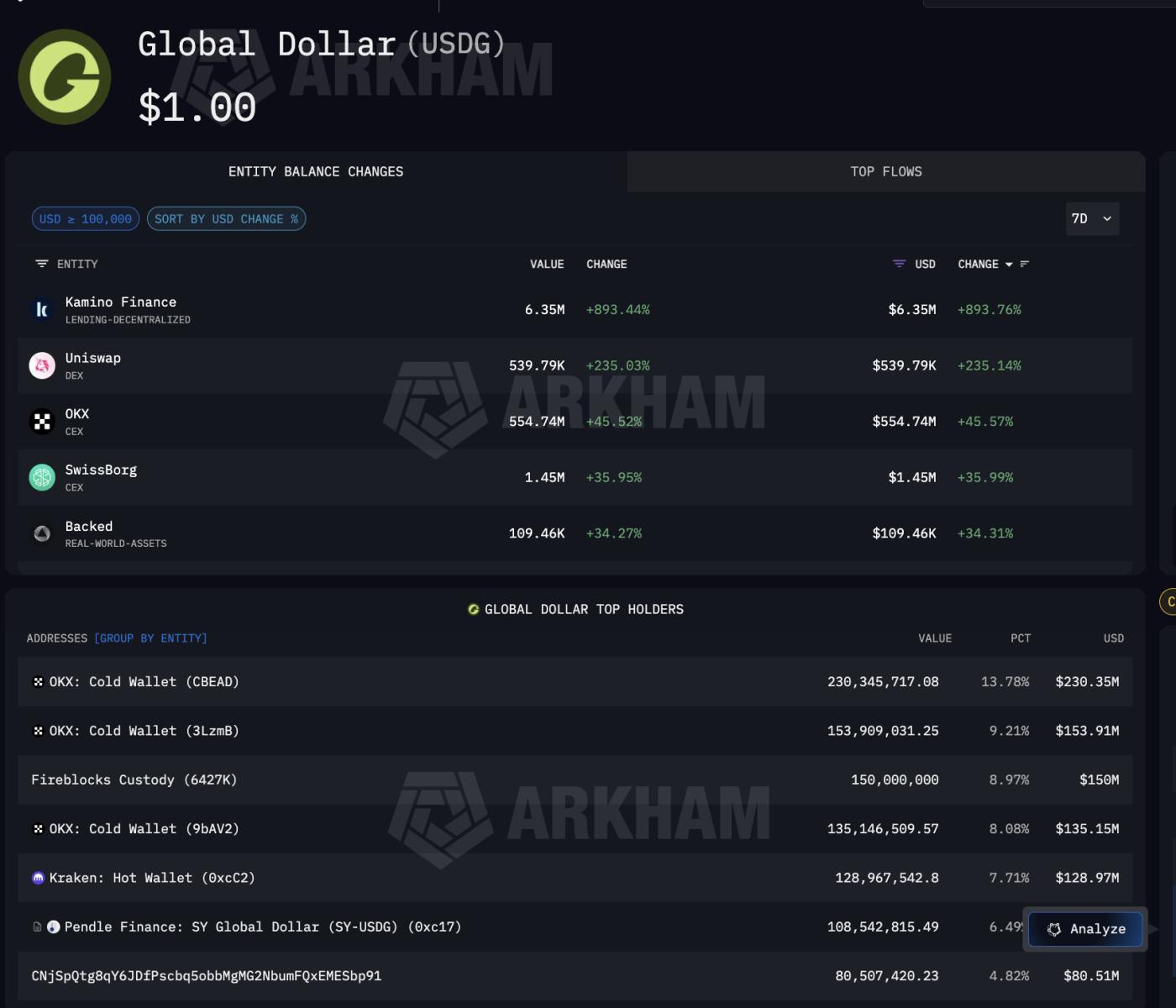

Data from Arkham on USDG reveals where institutional stablecoins typically "sit idle." The largest holder is Fireblocks Custody with $150 million, accounting for 8.97% of the total supply.

The largest holder of USDG: Arkham Intelligence

The largest holder of USDG: Arkham IntelligenceBesides Fireblocks, OKX 's Cold Storage holds $519 million Chia across three addresses, while Kraken – the public partner of the Global Dollar Network – holds nearly $128.97 million. Even Pendle Finance holds USDG, suggesting that the USDG Token is also entering DeFi yield-generating strategies.

Other USDG holder : Arkham Intelligence

Other USDG holder : Arkham IntelligenceWhat makes Fireblocks particularly important is that it also serves as the custodial platform that many banks use to operate USDC, including on the Solana blockchain – where Visa processes payments. In other words, this single custodial entity Vai as an intermediary for both Mastercard payments (via USDG) and the Visa network (via USDC).

Thus, the stablecoin infrastructure chain has a clear path forward.

Circle and Paxos handle Token minting. Coinbase, Wintermute , and Jane Street are the distributors. Fireblocks, as well as Cold Storage on exchanges, are the storage locations. This system serves not only token networks.

Arkham 's analytics page for Paxos confirms that Paxos also processes payments for Mercado Pago, the largest fintech platform in Latin America, meaning its Token minting infrastructure serves Mastercard, PayPal, and emerging markets.

Paxos processes payments for PayPal and Mercado Pago: Arkham Intelligence

Paxos processes payments for PayPal and Mercado Pago: Arkham IntelligenceAt every step between minting and burning, the operations of financial institutions depend on the same group of centralized stablecoin infrastructure providers.

Four TradeFi strategies, all sharing a common stablecoin platform.

After gaining a clear understanding of how the payment infrastructure operates, the question arises as to how traditional financial institutions will participate. Each major player chooses a different strategy, but they all connect to the same underlying stablecoin platform.

Visa is the strongest participant. As of December 2025, the company is paying $3.5 billion annually through USDC on Solana, via Cross River Bank and Lead Bank.

Visa has expanded to four stablecoins across four chain : USDC, PYUSD, USDG, and EURC on Solana, Ethereum, Stellar , and Avalanche. The stablecoin-linked card via Stripe's Bridge is currently operational in 18 countries, with plans to expand to over 100 countries .

Visa also built its own on-chain data analytics dashboard with Allium Labs, tracking up to $12.9 trillion in adjusted stablecoin volume, considering on-chain data a core business asset.

Onchain analytics dashboard: Visaonchainanalytics.com

Onchain analytics dashboard: Visaonchainanalytics.comIn January 2026 alone, Solana recorded a total stablecoin transaction value of $552 billion (ranking in the top 4), and it is also the blockchain chosen by Visa and PayPal with PYUSD for transactions.

Amount of stablecoins on the chain : Dune

Amount of stablecoins on the chain : DuneMastercard took a different approach, supporting four stablecoins on its network: USDC, PYUSD, USDG, and FIUSD . Mastercard also joined the Paxos Dollar Global Network with the USDG stablecoin, which is also the stablecoin that Fireblocks Custody is holding in custody for, valued at up to $150 million, as mentioned above.

Stripe acquired the active infrastructure , taking over Bridge for $1.1 billion. Bridge now operates both Stripe's stablecoin-linked Visa cards and stablecoin financial accounts in 101 countries, using USDC issued by Circle .

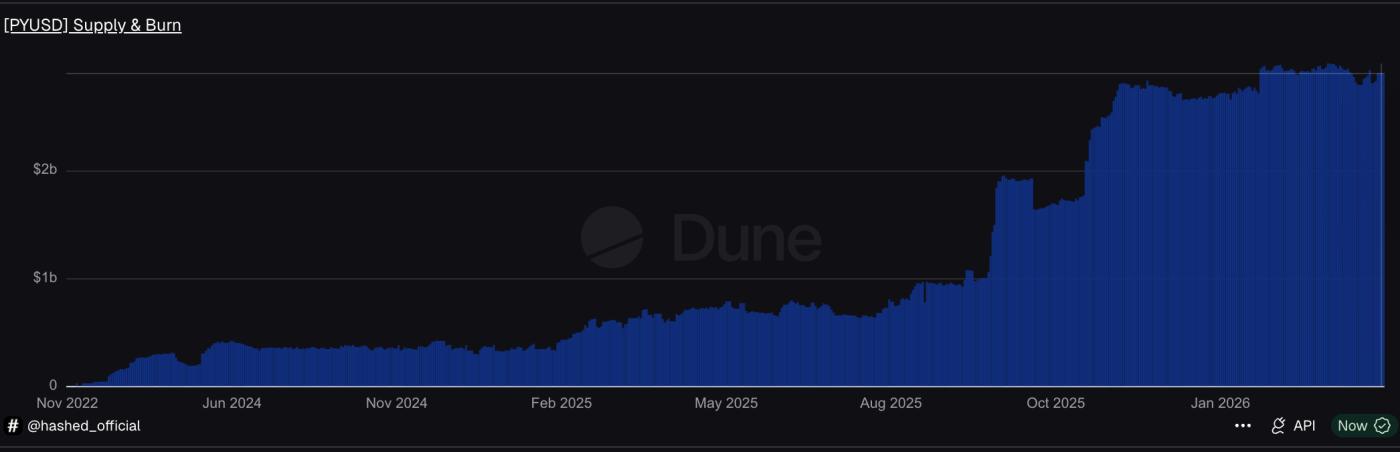

PayPal has built its own stablecoin. PYUSD, Mint by Paxos , currently has a supply of $3.95 billion across 70 markets (according to data from defillama) .

PYUSD supply shown on the chain: Dune

PYUSD supply shown on the chain: DuneOn Solana, PYUSD has a daily transaction speed of 0.6x , four times higher than on Ethereum, which is also Visa's blockchain.

Four strategies utilize the same underlying stablecoin infrastructure: Circle or Paxos Mint stablecoin, Coinbase distribution, and Fireblocks custody. But everything still needs to be more tightly integrated.

Stablecoin infrastructure is currently the foundation for institutional financial transactions.

The data presented in this article all point to one clear common point: Stablecoin infrastructure has now become the final transaction layer for institutional finance, not because large institutions are automatically "playing" crypto. The reason is that only a few entities have already built platforms that offer extremely fast, low-cost, 24/7 connectivity, and all the major players simply need to "connect" instead of building from scratch.

The entire platform has four layers, each of which focuses on a very small number of units.

At the supply layer, Circle and Paxos are the two main stablecoin issuers that institutional finance relies on. Circle 's USDC recorded $8.3 trillion in transfers in just one month. Paxos Mint its stablecoin for PayPal, Mastercard, and Mercado Pago, all through this single business.

At the distribution layer, data from Arkham shows that issuers distribute stablecoins through the same major partners: Coinbase and Wintermute. This trading channel completely bypasses traditional intermediary banks.

In the custody layer, Fireblocks holds up to $150 million USDG – making it the largest custodian of this stablecoin, and also stores USDC on Solana, serving both card-based transaction systems.

At the integration layer, Visa trades $3.5 billion annually while overseeing stablecoin flows as part of its core business data. Mastercard supports four stablecoins. Stripe acquired Bridge for $1.1 billion. PayPal launched PYUSD in 70 markets. JP Morgan even pays off debt with USDC on Solana. None of them needed to build their infrastructure from scratch.

This model is similar to what we previously analyzed regarding institutional crypto custody, where only seven entities across four tiers control all crypto assets.

This time, centralization also controls how an organization's money moves. The Vai are different, but the results are the same: institutional finance is now thriving on stablecoins built and maintained by a small group of providers. The pipeline is already in place. The question now is: will the next wave diversify this dependence or further centralize it?