Amazon stock’s bullish momentum is picking up real steam right now, with Barclays planting its flag firmly in the bull camp. The bank has put Amazon at the top of its mega-cap picks, citing a wave of new disclosures that make the Amazon stock forecast look stronger than ever. For anyone still trying to decide whether Amazon stock is bullish or bearish heading into the rest of 2026 — Barclays, and also most of Wall Street, have a pretty clear answer.

Also Read: Tesla Q1 Earnings Beat Forecasts as Tailwinds Lift Auto Growth

Amazon Stock Bullish Outlook Backed By Barclays And AWS Growth

AWS And AI: The Numbers That Convinced Barclays

Amazon Web Services sits at the core of the Amazon stock bullish argument, and the latest data makes it easy to see why. AWS rents computing power, storage, and software tools to businesses of all sizes — and it also happens to be where Amazon makes its biggest AI bets. Companies running large-scale AI workloads need massive infrastructure, and AWS has that at a scale very few can match.

The fresh disclosures from Amazon’s shareholder letter put some striking figures on the table. AWS AI revenue hit a $15 billion annualized run rate (ARR) in Q1 2026, and Barclays sees that number “ascending rapidly.” For context, CEO Andy Jassy reported in February that AWS grew 24% year-over-year in Q4 2025 — its fastest growth in 13 quarters — making it a $142 billion ARR business. Barclays noted that while Amazon’s AI position has long been “one of the more highly debated” topics among investors, the new data provides “additional confidence around AWS upside from AI over coming years.”

Amazon’s Chip Unit: A $50 Billion Business Hiding In Plain Sight

Most investors barely think about Amazon’s custom chip division, and Barclays thinks that’s a mistake. The Trainium and Graviton processors now run at $20 billion in annual revenue. Barclays flagged that if Amazon sold this chip business as a standalone operation to outside customers, it “would be ~$50 billion” — a number that rarely comes up in analyst conversations about AMZN stock.

Jassy made clear in Amazon’s Q4 earnings call that Trainium2 already powers the majority of the company’s Bedrock AI service. The newer Trainium3 chip delivers 40% better cost efficiency than its predecessor, and Amazon expects “nearly all Trainium3 supply of chips […] to be committed by mid-2026.” On top of that, Barclays highlighted Amazon’s plan to add more than 1 million Nvidia GPUs across 2026 and 2027 — capacity the bank estimates could support roughly $100 billion in annual AWS revenue, which puts the current AMZN stock price target in a very different light.

Grocery, Retail Engagement, And What The Street Thinks

The Amazon stock bullish case also extends well beyond cloud. Barclays called out Amazon’s grocery segment, which crossed $150 billion in U.S. gross sales in 2025 — making Amazon the country’s second-largest grocer. Jassy noted that everyday essentials now account for one in three units sold by Amazon in the U.S., and customers who buy perishables shop with Amazon “twice as often as customers who don’t.” That level of daily engagement points to a retail moat most people still underestimate.

Also Read: Strategy (MSTR) Stock Soars 10%, BTC Rally and Latest $2B Buy

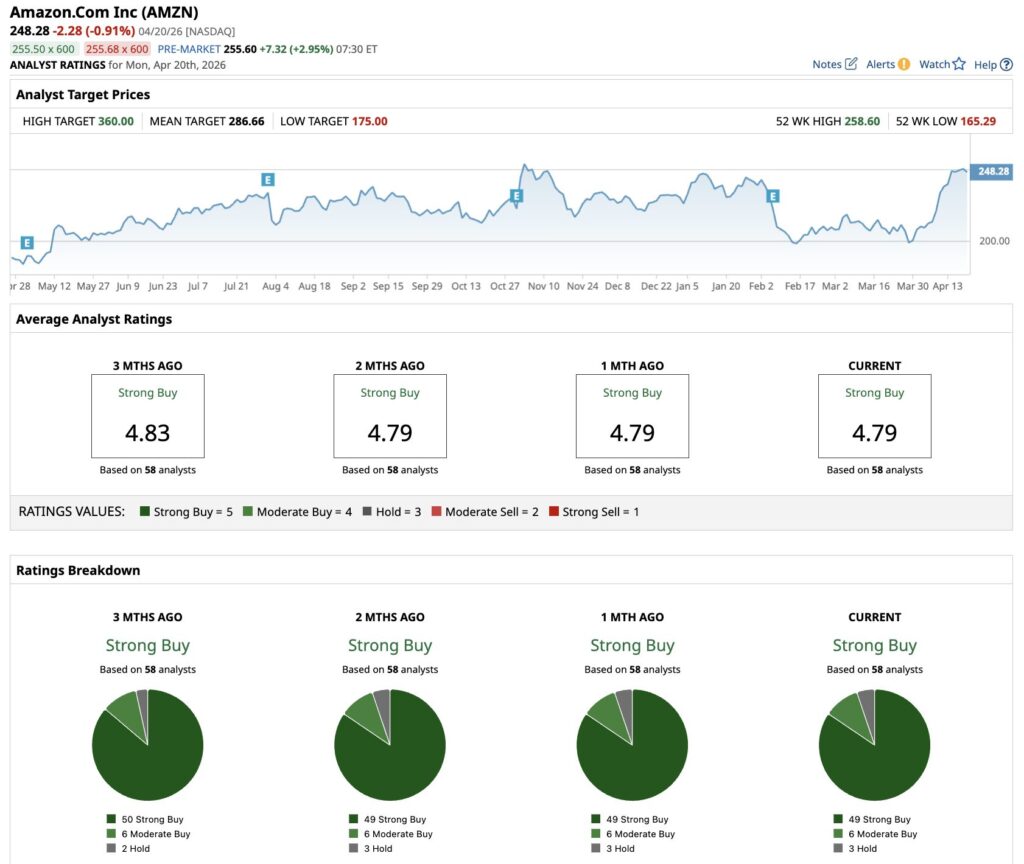

The broader analyst community backs this Amazon stock bullish read too. At the time of writing, 58 analysts cover AMZN stock, and 49 of them rate it a “Strong Buy,” with six more at “Moderate Buy” and just three at “Hold.” The mean AMZN stock price target sits at $286.66 — with a high target of $360 — against a current price around $248. Longer term, the Amazon stock forecast calls for adjusted EPS to grow from $7.17 in 2025 to $16.34 by 2030. Barclays’ position, and also the broader Street consensus, points to one conclusion: AMZN stock has serious room to run.