The S&P 500 has risen 28% over the past 12 months, and Nvidia has risen 73%. However, these gains still pale in comparison to the storage sector. SanDisk, which was $34.61 a year ago, is now at $1,406.32, a staggering 39-fold increase.

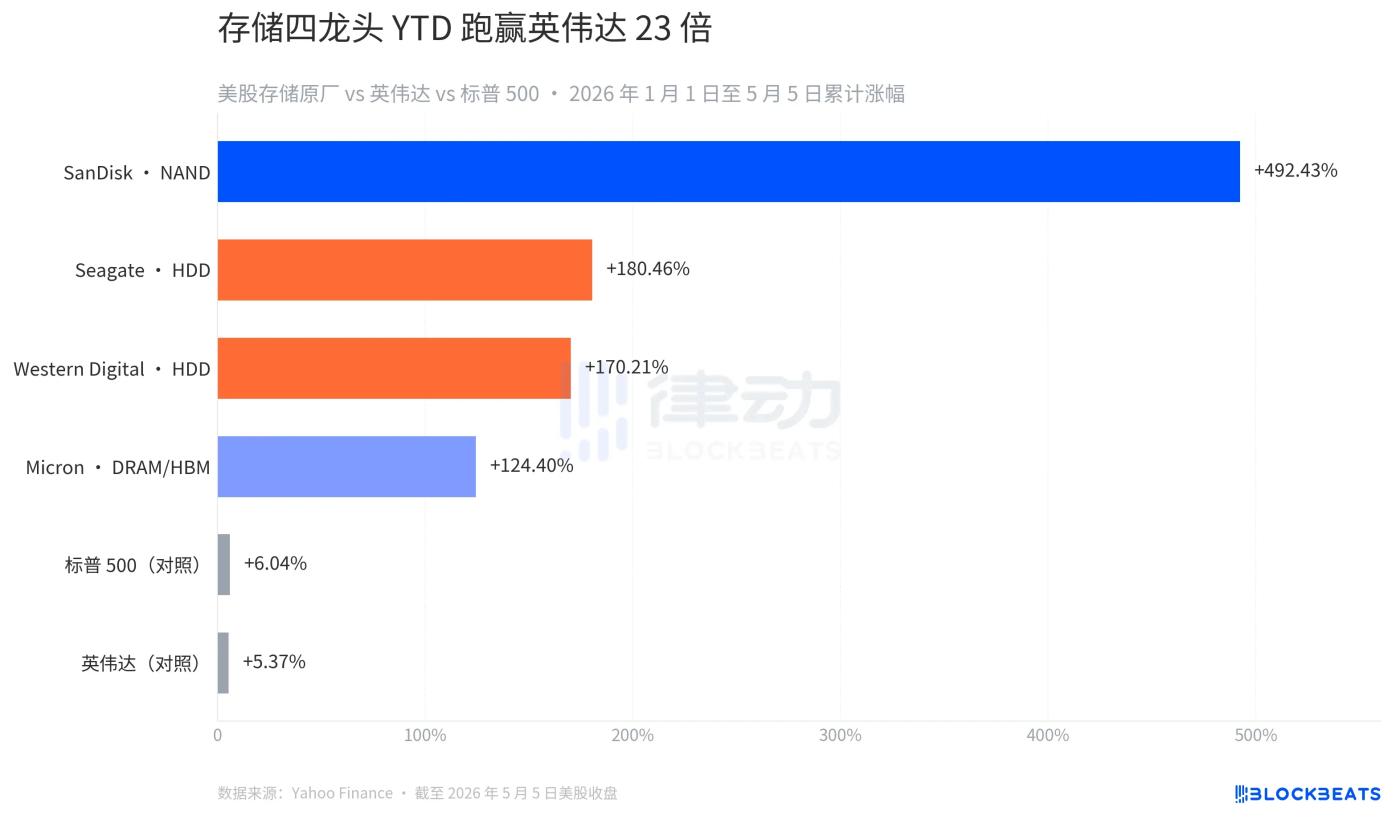

This NAND flash memory manufacturer, spun off from Western Digital just 14.5 months ago, is the best-performing stock on the US stock market so far in 2026, surging 492% year-to-date. The four major US memory manufacturers behind it—Micron, Seagate, and Western Digital—have seen year-to-date (YTD) gains ranging from 124% to 492%, with even the lowest-performing one outperforming Nvidia by 23 times. The label of "shovel seller" in the AI revolution is shifting from the GPU side to the memory side.

The most notable day was May 5th. SanDisk rose 11.98%, Micron rose 11.06%, Western Digital rose 5.18%, and Seagate rose 4.38%. Among the four US-listed memory manufacturers, three hit new 52-week highs.

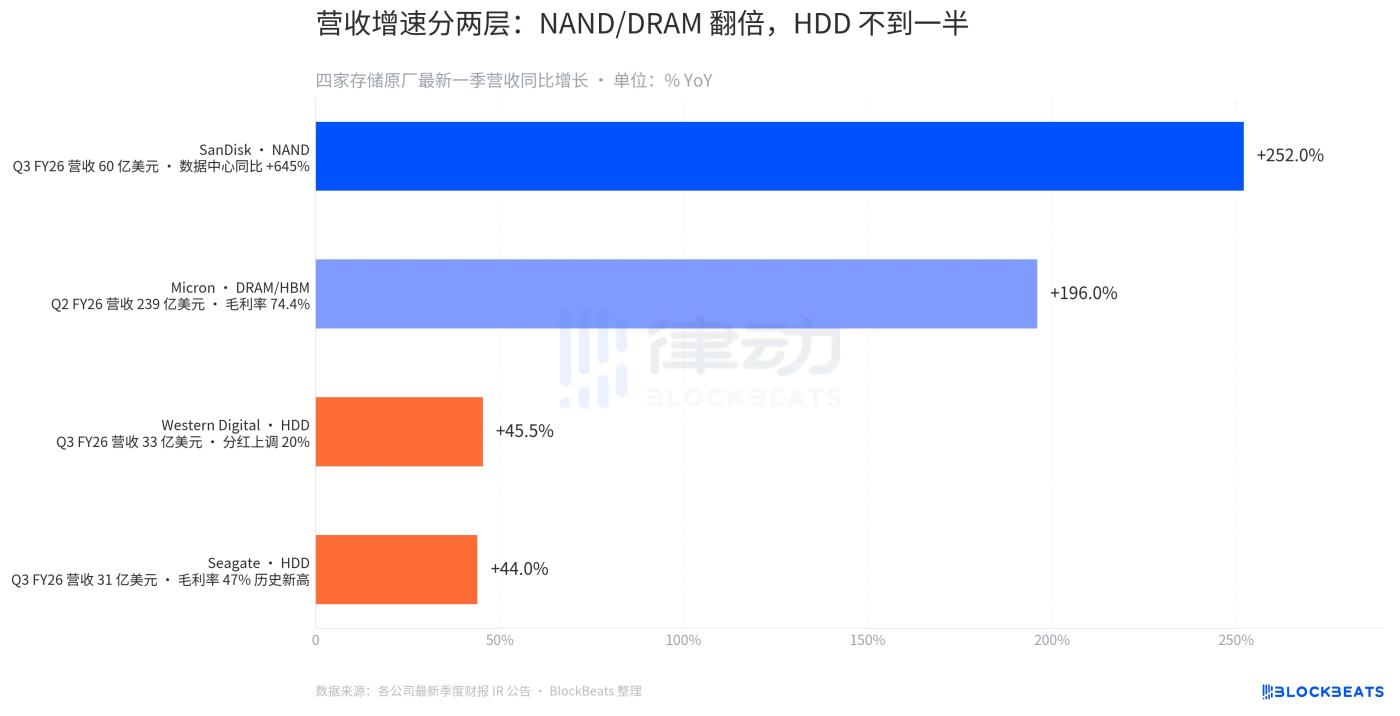

The catalysts were two financial reports and a supply story. On April 28, Seagate announced that its Q3 FY26 revenue increased by 44% year-on-year and its gross margin reached a record high of 47%. CEO Dave Mosley said in the conference call that "AI is ushering Seagate into a new era of structural growth," and that the Nearline exabyte capacity has been allocated to 2027.

Two days later, SanDisk announced Q3 FY26 revenue of $5.95 billion, a year-on-year increase of 252%, exceeding the upper limit of guidance by $1.15 billion. Data center revenue increased by 645% year-on-year and nearly doubled quarter-on-quarter. Q4 guidance is for a further year-on-year increase of 308% to 334%. Coupled with Micron receiving a credit rating upgrade from Fitch, the entire sector saw a broad-based rally on Monday.

But that's just the surface. If you break down the four stocks individually, the statement that "the entire storage sector is rising" is actually a misleading summary. They are rising based on three completely different supply stories, with vastly different price increases.

Looking at year-to-date (YTD) performance, SanDisk rose 492.43%, Seagate 180.46%, Western Digital 170.21%, and Micron 124.40%, falling into four completely different tiers. During the same period, the S&P 500 rose 6.04%, and Nvidia rose 5.37%. The latter even fell 7.82% in the past five days. The label of "primary beneficiary of AI" is shifting: the GPU story driven by large model training has completed its valuation expansion cycle over the past year, and money is starting to flow downstream, into the memory and storage needed to handle AI workloads.

This cutting is not uniform. It layers along the medium properties.

The latest quarterly financial reports clearly illustrate the tiered growth. SanDisk's NAND revenue increased by 252% year-over-year, Micron's DRAM/HBM revenue increased by 196% year-over-year, and Western Digital and Seagate's HDD revenue both increased by 44-45% year-over-year. NAND and DRAM are the sectors experiencing explosive growth in this round, while HDD is showing steady growth, with a gap of 4 to 5 times between the two.

The stratification of gross margins is even more dramatic. Micron's Q2 FY26 gross margin was 74.4%. This is an extreme figure that a chip manufacturer can achieve, meaning that for every $100 of DRAM and HBM sold, $74 goes into the profit statement. Seagate's 47% gross margin, while a record high, is still an order of magnitude lower than DRAM manufacturers. This is due to differences in supply structure. HBM capacity is concentrated in the hands of three companies (SK Hynix, Samsung, and Micron), all under long-term contracts until the end of 2026. HDD capacity, on the other hand, is evenly distributed between Seagate and Western Digital, resulting in relatively dispersed price negotiation power.

The price signals the same thing.

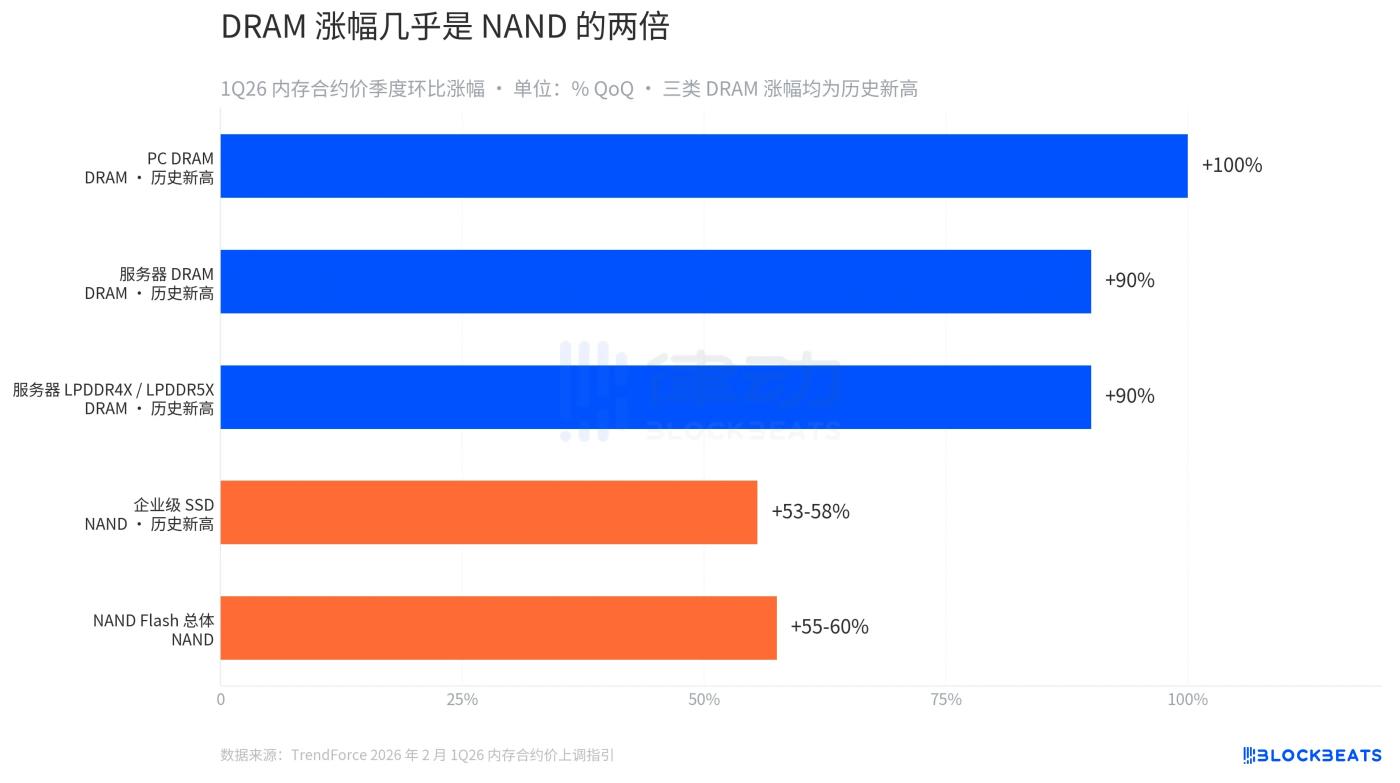

According to TrendForce's revised 1Q26 memory contract price guidance released on February 2nd, PC DRAM saw a quarter-over-quarter increase of 100%, server DRAM approximately 90%, and server LPDDR4X/5X approximately 90%, all three DRAM categories experiencing record price increases. In the NAND Flash market, enterprise-grade SSDs saw a year-over-year increase of 53% to 58%, while NAND overall increased by 55% to 60%, a rise only slightly more than half that of DRAM.

This is a scissors gap that explains everything. AI servers require both NAND and DRAM, but they need bandwidth (HBM) and capacity density (DDR5, LPDDR5X) even more. The supply-demand gap on the DRAM side is much larger than that on NAND. Micron's CEO's statement at the Q2 FY26 earnings call, "We're sold out for 2026," succinctly explained this supply story. HBM4 36GB 12H is already in mass production and shipping for Nvidia's Vera Rubin platform, and the FY26 capital expenditure was revised upward from $20 billion to $25 billion in preparation for adding another tier in 2027.

Of the four original equipment manufacturers (OEMs), SanDisk is the one most worthy of being singled out for discussion.

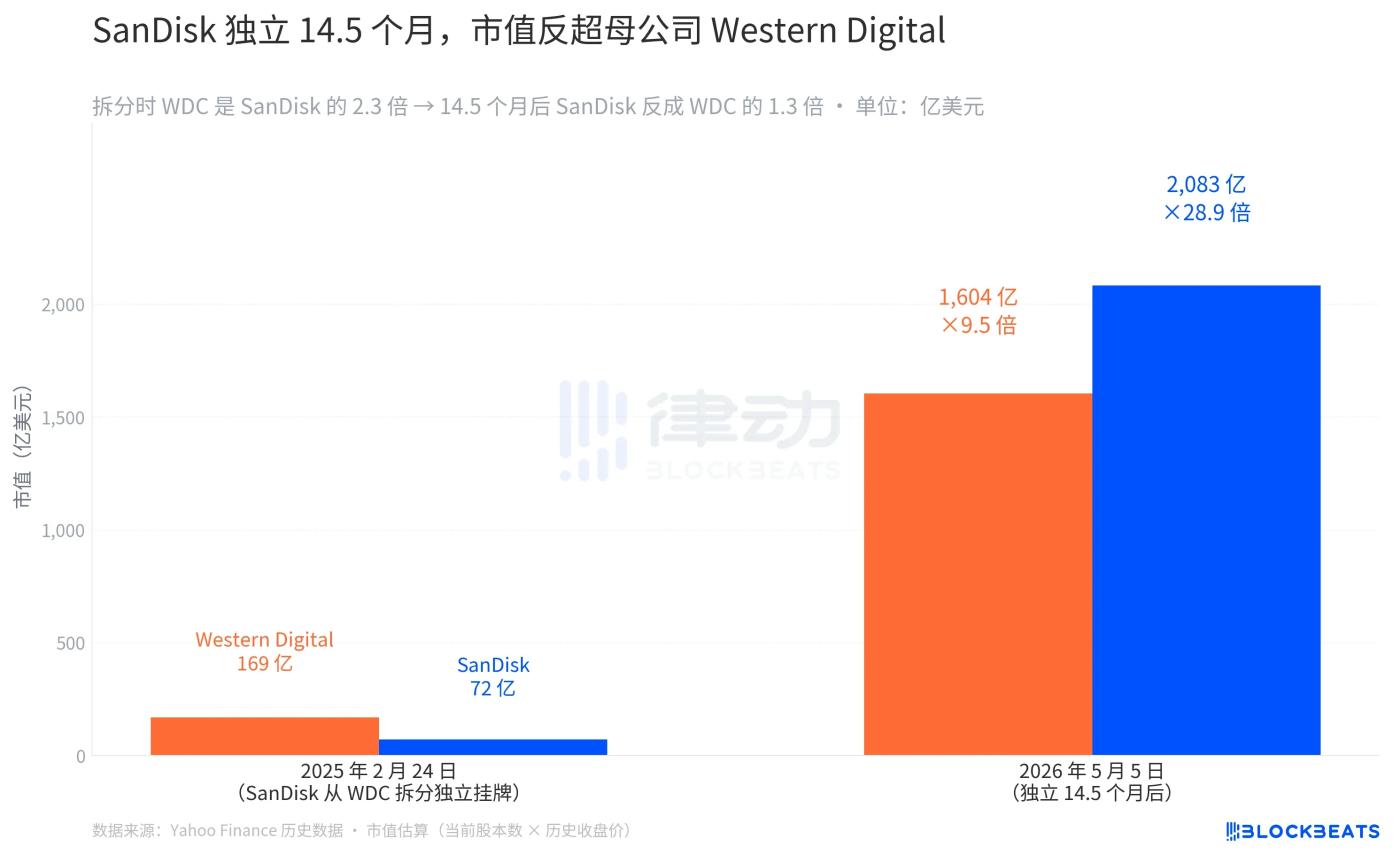

SanDisk spun off from Western Digital on February 24, 2025, and began trading on Nasdaq. It opened at $52 and closed at $48.60, giving it a market capitalization of approximately $7.2 billion. On the same day, Western Digital closed at $49.02, with a market capitalization of approximately $16.9 billion. On the day of the spin-off, Western Digital's size was 2.3 times that of SanDisk.

14.5 months later, SanDisk's market capitalization is $208.3 billion, while Western Digital's is $160.4 billion. SanDisk is now 1.3 times the size of Western Digital. This inversion is rare in the history of large corporate spin-offs. In most spin-off cases, the subsidiary is still rebuilding investor relations in the first year, and it usually takes 3 to 5 years for its market capitalization to catch up with the parent company. SanDisk took 14.5 months.

The reason given was that it was spun off at the perfect time. When Western Digital decided to split up in 2024, its rationale was that "NAND and HDD are in different capital cycles, and separate operations provide clearer valuations." This judgment was later proven correct by the market: SanDisk, after becoming independent, focused solely on NAND, coinciding with the explosive demand for enterprise-grade SSDs from AI data centers. Western Digital, focusing solely on HDD, capitalized on the structural growth of cloud storage archiving. Each company's separation represented a different story. If it hadn't been spun off, with one company encompassing two businesses with completely different supply cycles, the capital market would have placed it in the middle with a more conservative valuation multiple.

On May 4th, Bernstein raised its price target for SanDisk from $1,250 to $1,700, citing visibility into its data center SSD business. SanDisk's financial report revealed that it has signed five long-term contracts, received $11 billion in financial guarantees, and that more than one-third of its NAND bits are locked up by customers by fiscal year 2027. This is the first time a sector traditionally treated as a commodity cycle has seen a "long-term contract + customer prepayment" structure similar to that of advanced process wafer foundries.

Overall, money is flowing from GPUs to memory. DRAM is the real alpha in this round, while HDD is a structural marathon with a different pace. SanDisk, a company that has only been independent for 15 months, has surpassed its parent company Western Digital in market value by relying on NAND data center.

On May 5th, the same trading day, Nvidia fell 1.03%, TSMC fell 1.79%, and SanDisk rose 11.98%. Despite all being "AI beneficiaries," the market is already voting with its feet, clearly identifying which segment of supply is the scarcest.