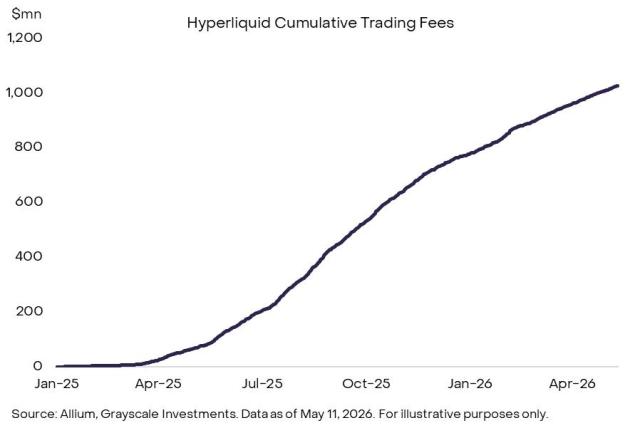

Huawei's "Tao Law" has sparked bearish sentiment towards Nvidia and AMD? My assessment: this bearish logic is flawed. Tao Law refers to design architecture innovation, not manufacturing process breakthroughs. These two things are completely different in the semiconductor value chain. Let's dismantle the biggest misconception first. Huawei's claim of "equivalent 1.4nm density by 2031" is not equivalent to process technology. So-called "logic folding" involves vertically stacking planar circuits and compressing signal distances; its essence is optimization at the packaging and architecture levels, not a breakthrough in lithography. TSMC has already mass-produced 2nm, its 1.4nm is projected for 2027-28, and its sub-1nm for 2030+. Huawei's 2031 target is TSMC's 2027 position, and the gap will still exist then. No matter how advanced the design, it's useless if you can't manufacture it. China cannot obtain ASML's EUV lithography machines, and SMIC's mass production ceiling is still at the 7nm level DUV. Tao's Law can only optimize on existing equipment—like top-tier driving skills in a speed-limited car, the physical limits are there. There's another easily overlooked layer: the EDA ecosystem. Cadence and Synopsys together control over 75% of the EDA market, deeply tied to US export controls. ARM architecture is penetrating data centers, and TSMC's OIP integrates over 110 partners; these certifications require at least five years of accumulation, not something a single paper can bypass. Look at the market structure. Huang himself said the Chinese AI chip market has basically been ceded to Huawei—this isn't news, it's already priced in. After export controls, China accounts for about 15-20% of Nvidia's revenue; the real growth isn't there. Global cloud vendors' AI capex is still skyrocketing, all flowing into the NVDA/AMD/TSMC supply chain. CUDA has over 5 million developers, over a decade of code accumulation, and a deeply locked global AI training pipeline. Huawei dominates the Chinese market, Nvidia dominates the global market; they're not mutually exclusive in the short term. Financially, there's no support for a bearish outlook. NVDA's latest quarterly data center revenue was $75.2 billion, with total revenue of $81.6 billion. The real concern is macroeconomic inflation leading to a Fed shift, or AI inference demand falling short of expectations—not a design methodology geared towards 2031. Tao's Law is a significant milestone in China's semiconductor self-sufficiency and deserves respect. However, a technological narrative ≠ a financial catalyst; confusing these two is the most dangerous thing. Do you think Tao's Law will have a substantial impact on the US semiconductor stock market? 👀

This article is machine translated

Show original

Huawei

@Huawei

05-25

HUAWEI has presented the Tau (τ) Scaling Law, a new principle for guiding the future development of the semiconductor industry. By 2031, HUAWEI's high-end chips based on this law are expected to feature a transistor density that is equivalent to 14 Å (1.4 nm) processes.

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content