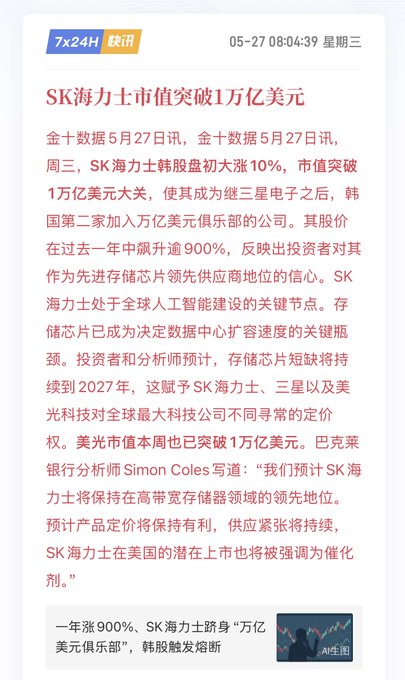

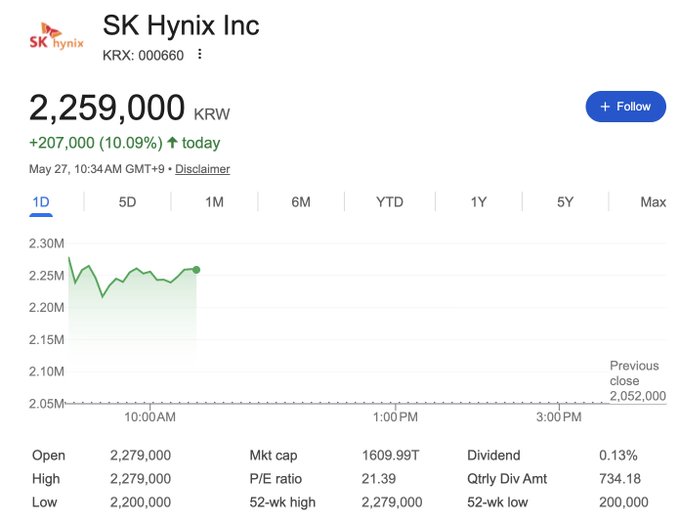

Storage stocks are breaking free from cyclical patterns and becoming infrastructure stocks for the AI era. This could be the second time, after cloud computing, that a "commodity → infrastructure" asset revaluation has occurred. In the 50-year history of the storage industry, no pure storage company has ever entered the trillion-dollar club. Now, Micron ($MU) and SK Hynix have both surpassed a trillion-dollar market capitalization in a single day. Why now? For decades, memory has been a typical commodity. Prices fluctuated with supply and demand cycles. Samsung, Micron, and SK Hynix engaged in decades of price wars, winning by "losing less than their competitors," without any pricing power. HBM changes the underlying logic. Physically stacked next to GPUs, it serves as a dedicated bandwidth interface for AI chips, with no alternatives. NVDA directly locks in the supply chain, with only three suppliers globally. Yields are extremely difficult to improve, and new capacity can take at least 18 months to come online. This isn't a boom-bust cycle; this is a textbook example of an oligopolistic structure. The fact that both companies simultaneously surpassed a trillion-dollar market capitalization indicates that market pricing isn't based on the execution capabilities of any single company—it's based on the structural scarcity of the entire HBM sector. When supply is locked down and demand is driven by the AI arms race, the analytical framework for cyclical stocks becomes ineffective. The only real question that needs answering is: Where is the ceiling for AI computing power expansion? If you believe this arms race will last another 3-5 years, the revaluation of storage has only just begun. If you believe it's already overheated, then this is the biggest cyclical stock trap in history. Which side are you on?

This article is machine translated

Show original

Followin 华语 - 热点风向标

@followin_io_zh

Micron ($MU) has seen its gains expand to 16%, reaching $875, a new all-time high. UBS has already raised its price target to $1625—implying an additional 87% upside.

This isn't your typical analyst hype.

The underlying logic is: HBM (high-bandwidth memory) is becoming the real

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content