Rejecting venture capital funding, they have forged a unique development path by relying on the community ecosystem.

Written by: Michael Zhao, Zach Pandl

Compiled by: Saoirse, Foresight News

Key points

- Hyperliquid is a landmark breakthrough project in the contemporary digital asset industry. This DeFi platform fully demonstrates the unlimited potential of blockchain technology.

- The platform's core is a decentralized exchange specializing in perpetual contracts. Perpetual contracts are financial derivatives with no expiration date. Like leading centralized futures exchanges, it supports 24/7 trading, boasts a deep order book, fast execution speeds, and a user-friendly interface. It also adheres to the core principles of decentralized finance: transparent trading and user-managed assets.

- The platform expands its ecosystem through permissionless innovation. With its open architecture, Hyperliquid encourages third-party developers to launch new products, and the platform now covers a variety of trading categories, including cryptocurrency spot trading, traditional asset futures, and prediction markets.

- Due to the lack of clarity in the regulatory rules regarding perpetual contracts and decentralized exchanges, US users are currently unable to use the platform. However, recent regulatory statements and legislative progress in Congress are expected to change this situation and become a significant driving force for the platform's further development.

- Hyperliquid has built a highly cohesive community, largely thanks to its unique fundraising model: the project has not accepted any venture capital investment and directly airdrops approximately 30% of its HYPE tokens to platform users.

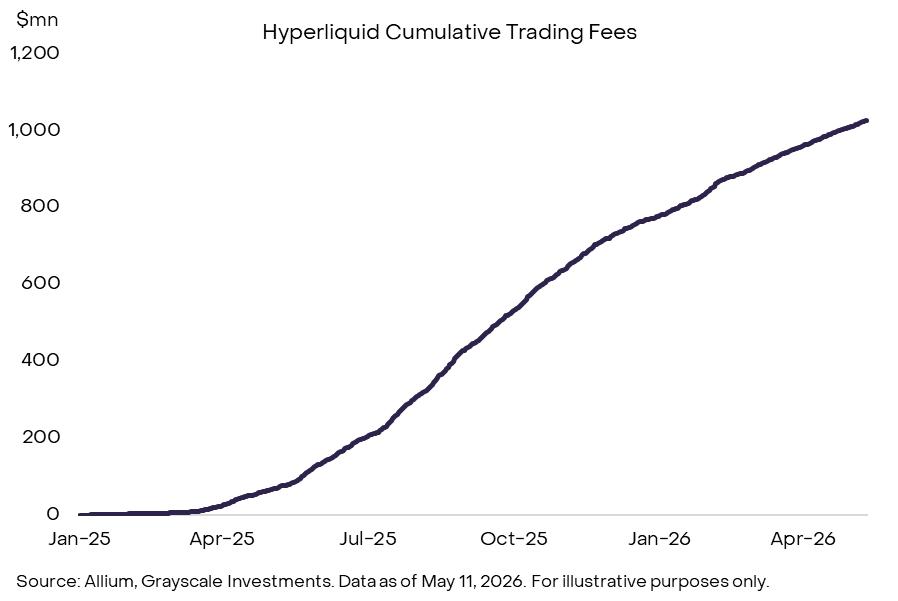

- HYPE is the platform's native utility token, with its value primarily derived from transaction fees. The platform generated approximately $800 million in transaction fee revenue last year. Overall, Hyperliquid boasts strong product competitiveness, a vast market potential, and considerable long-term growth potential.

Imagine a startup that, in less than three years, has distinguished itself in a fiercely competitive industry, generating approximately $800 million in revenue last year alone, possessing a massive target market, a streamlined operating model, and strong profit leverage. Even though a large number of potential users in the US and other major markets are currently unable to access the platform, its growth momentum remains rapid, and this situation will soon change. This company is Hyperliquid.

Figure 1: Hyperliquid is a groundbreaking success story in the modern digital asset industry.

Hyperliquid's core business is a decentralized exchange for perpetual contracts, a type of financial derivative with no settlement date. Cryptocurrency perpetual contracts have now developed into a massive sector: by 2025, the daily trading volume of perpetual contracts across the entire digital asset industry reached $200 billion. Currently, this market is mainly dominated by centralized exchanges such as Binance, OKX, and Bybit, while Hyperliquid is the first blockchain decentralized project to gain a significant market share in terms of trading volume and open interest.

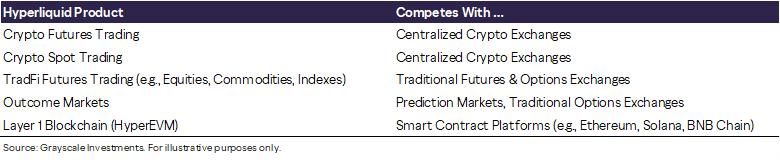

Simply capturing market share in crypto perpetual contracts is enough to support the platform's continued and substantial growth, but Hyperliquid's ambitions extend far beyond that. While perpetual contracts remain the platform's primary source of revenue, it has now evolved into a comprehensive financial services platform with operations spanning multiple sectors.

Chart 2: Hyperliquid is a diversified financial services platform

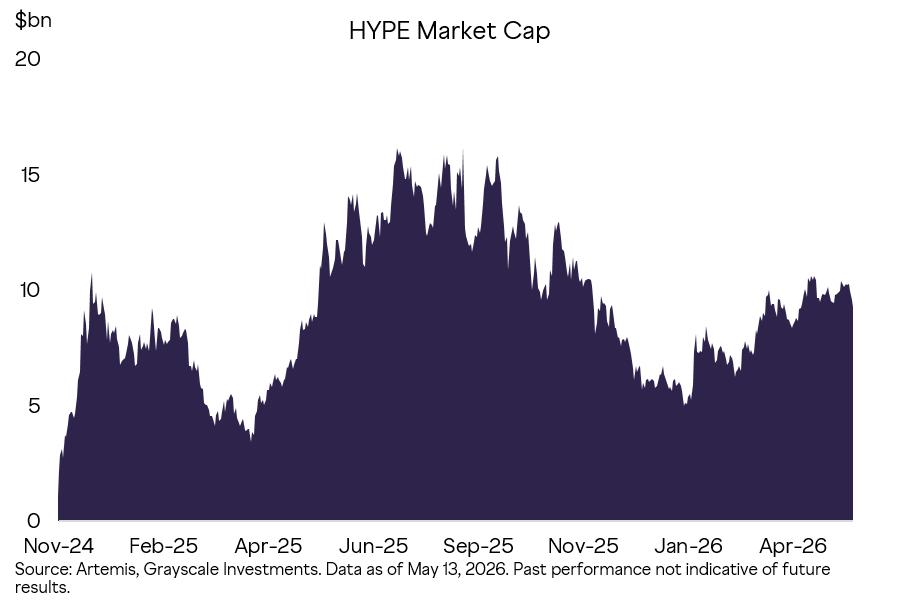

Like other blockchain protocols, Hyperliquid is not a traditional commercial company and does not issue stocks. Its native token provides support for the operation of the network, and its value is generated by trading activities. Currently, HYPE's circulating market value is about $130 billion, and after excluding stablecoins, its market value ranks eighth in the world[2]. Compared with similar traditional listed companies, HYPE's current valuation is in a reasonable range. Combining the platform's stable user growth, broad potential market and upcoming regulatory benefits, we judge that Hyperliquid still has huge room for development in the future.

Chart 3: HYPE's Market Capitalization Since Inception

Basic knowledge of perpetual contracts

Perpetual contracts are the core business that made Hyperliquid famous. These products originated in the crypto industry, and we believe they will eventually be deeply integrated into the traditional financial sector (see the regulatory policy interpretation below for details).

Traditional futures contracts all have an expiration date. Taking crude oil futures as an example, the contract stipulates that crude oil delivery must be completed before a specified date. If a trader holds a position until the contract expires, they must complete the physical delivery or receipt of the underlying asset. If a trader only wants to conduct financial transactions and does not intend to participate in physical delivery, they need to continuously transfer their positions to contracts that expire later.

Perpetual contracts have no expiration date and do not involve physical delivery of the underlying asset. This product is designed for hedgers and speculators, used for simple financial position trading, and generally supports 24/7 trading.

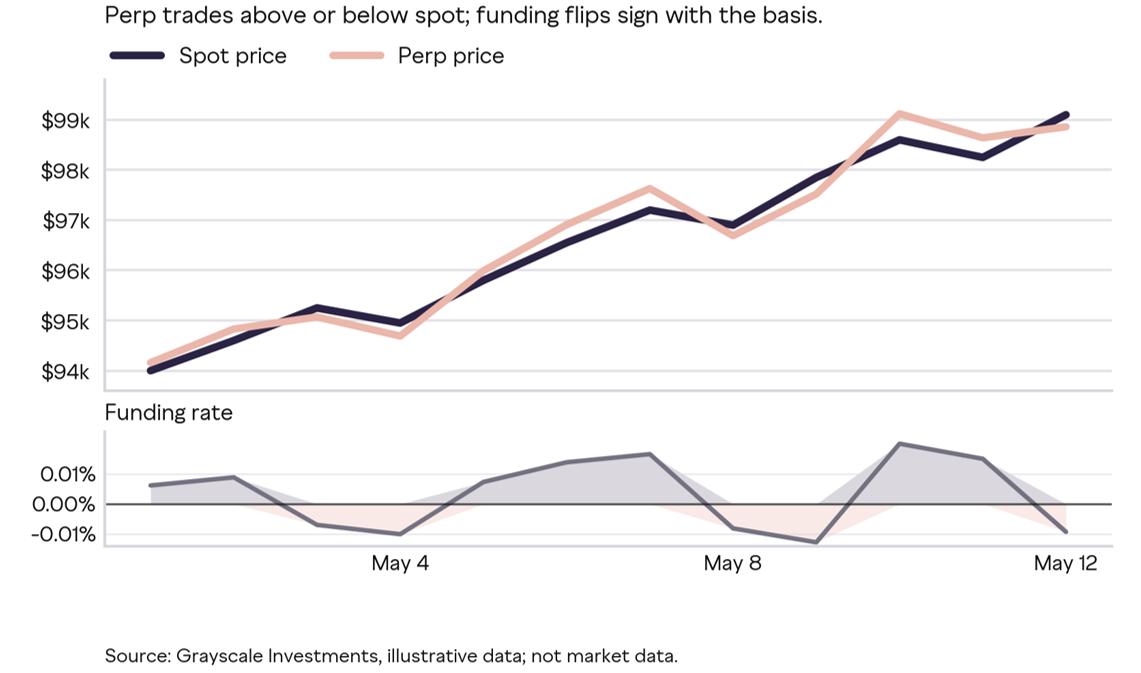

Traditional futures rely on an expiration and delivery mechanism to maintain a correlation between prices and the spot price of the underlying asset. Perpetual contracts, however, do not have an expiration date. Their price's close tracking of the spot price relies on a funding rate mechanism: small-amount funds are periodically transferred between long and short traders. When the perpetual contract price is higher than the spot price, long traders pay fees to short traders; when the price is lower than the spot price, short traders pay long traders. The larger the price difference, the higher the transfer amount. This funding rate, combined with market arbitrage behavior, forms a market adjustment mechanism that pushes the perpetual contract price closer to the spot price of the underlying asset.

Figure 4: Funding rate mechanism anchors perpetual contracts to the underlying asset

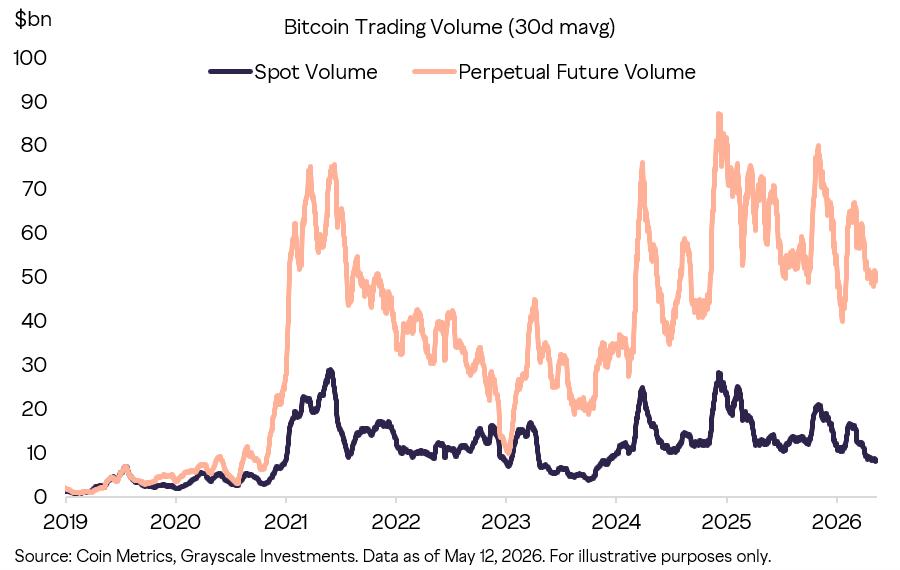

Perpetual contracts are a perfect fit for the crypto market. The cryptocurrency market operates year-round, with strong demand from both individual investors and professional speculative traders, and new assets are listed far faster than on traditional futures exchanges. Perpetual contracts provide traders with a convenient channel to assess price movements, hedge spot positions, and leverage trading around the clock, making them one of the core markets for crypto asset price discovery.

Chart 5: Global Bitcoin Report: Perpetual Contracts vs. Spot Trading Volume

Individual investors have various ways to leverage their investments, including traditional brokerage margin trading, term futures, options, and leveraged ETFs. Judging from the actual performance of the crypto market, when given multiple options, investors often prefer perpetual contracts, primarily due to their ease of use. Therefore, it can be inferred that once perpetual contracts become widely adopted in traditional financial markets, they will also attract a large user base.

Hyperliquid's breakthrough advantages

Hyperliquid has achieved a major breakthrough: combining the high performance of centralized exchanges with the transparency and asset custody model of a blockchain system. From a trader's perspective, it's difficult to distinguish it from mainstream centralized exchanges—both possess deep order books, ultra-fast execution capabilities, and mature position management functions. However, Hyperliquid records all transactions (including forced liquidation records) on the blockchain and supports user asset self-custody, a fundamental difference from centralized exchanges.

Chart 6: Hyperliquid trading experience is similar to centralized exchanges.

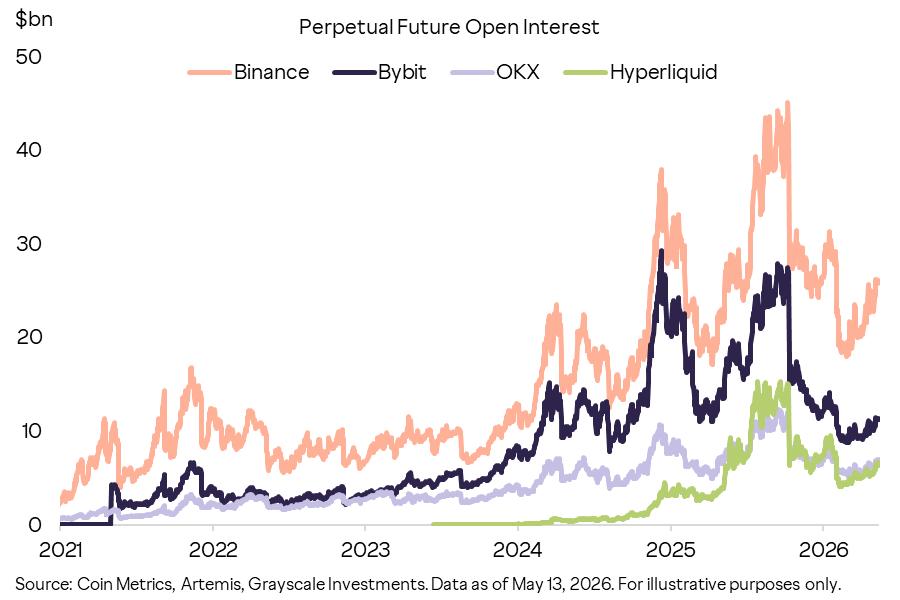

The cryptocurrency leveraged trading market is fiercely competitive, with users demanding high-quality platform experiences. Hyperliquid, however, has established itself as a leading cryptocurrency derivatives trading platform thanks to its high-quality products. In 2025, its total perpetual contract trading volume reached $2.9 trillion, with a current open interest of approximately $70 billion. Based on these figures, Hyperliquid ranks as the third or fourth largest perpetual contract exchange globally. Even as its business expands from native crypto assets to other categories, its trading volume, open interest, fee revenue, and industry attention continue to grow steadily.

Figure 7: Hyperliquid is currently the third or fourth largest cryptocurrency perpetual contract exchange.

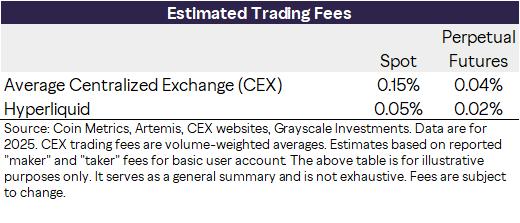

In terms of transaction costs, Hyperliquid is also competitive compared to centralized exchanges. Based on Bitcoin and Ethereum trading data from 2025, the volume-weighted average transaction fee for spot trading on mainstream centralized exchanges was 15 basis points, and for futures trading, it was 4 basis points; while Hyperliquid's spot transaction fee was 5 basis points, and its futures transaction fee was only 2 basis points. Note: The above data is based on basic account order placement and taker fees, and does not include other factors affecting the total transaction cost such as fee tiers, promotional activities, and order book depth; the centralized exchange data is a volume-weighted average of multiple platforms.

Figure 8: Volume-Weighted Costs

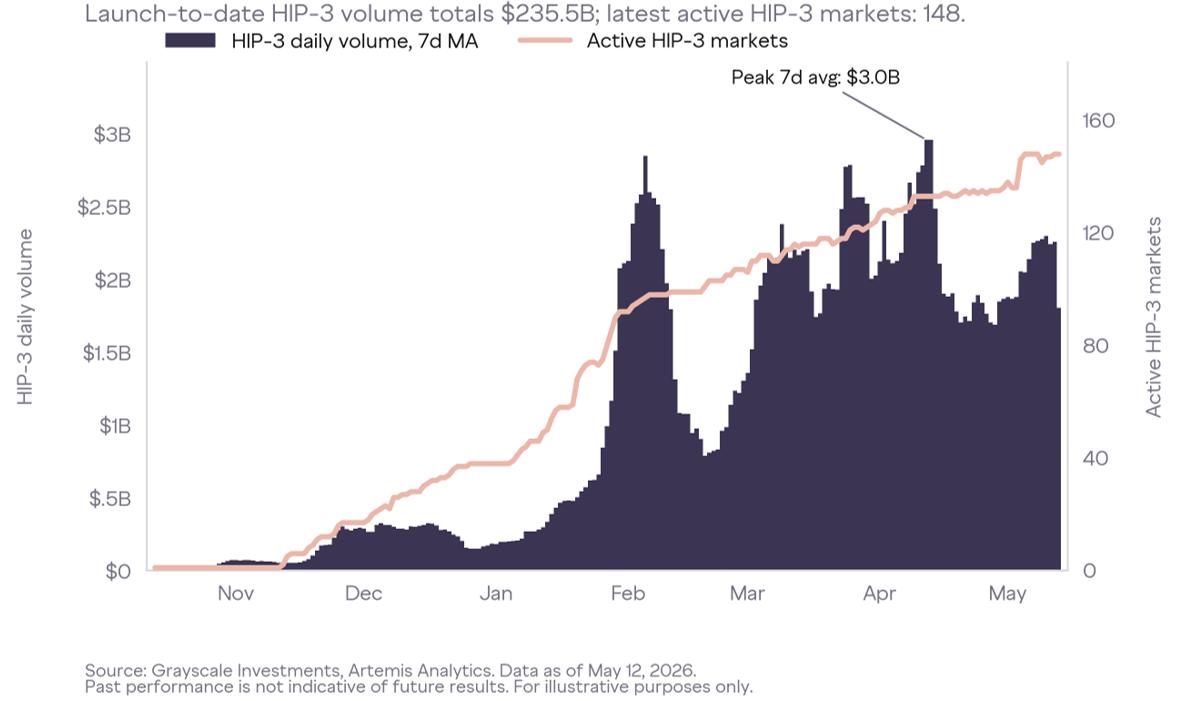

The platform's greatest potential lies in its open architecture, allowing it to expand its business beyond crypto perpetual contracts to include more product categories. New features are typically introduced through Hyperliquid Improvement Proposals (HIPs), and all new products are deployed by third-party developers, rather than by the native Hyperliquid team.

HIP-3 allows developers to list new perpetual contract trading markets covering non-crypto assets such as stocks, commodities, and indices. These markets are gaining popularity and are gradually becoming an important channel for after-hours price discovery in traditional financial assets. Bloomberg has commented that the price movements of perpetual contracts for crude oil, gold, and silver on the Hyperliquid platform can provide a reference for the market trends after the traditional market opens. In another report, Bloomberg called it a "24/7 commodity leveraged trading platform," which aptly reflects its growing status as a 24/7 trading infrastructure for real-world assets.

Trading volume data also confirms this value. During the significant silver price volatility in February 2026, the daily trading volume of HIP-3 silver perpetual contracts exceeded $4 billion. On February 5th of the same year, the trading volume of this category once reached 1% of the notional trading volume of silver contracts on the New York Mercantile Exchange. During the recent oil price volatility caused by the Middle East situation, the 24-hour trading volume of HIP-3 crude oil perpetual contracts exceeded $4 billion on April 9th, briefly surpassing the trading volume of Bitcoin perpetual contracts. Currently, the platform has launched officially authorized S&P 500 index contracts, which can be traded normally on weekends. Since its launch, the cumulative trading volume of the HIP-3 sector has exceeded $230 billion, and there are currently more than 140 trading pairs in normal operation.

Figure 9: HIP-3 expands Hyperliquid's business beyond crypto perpetual contracts

HIP-4 extends its business to the outcome trading market, launching binary options products similar to prediction market contracts. These products are also deployed by third-party developers, and all transactions still generate fee revenue for Hyperliquid.

Operating principle

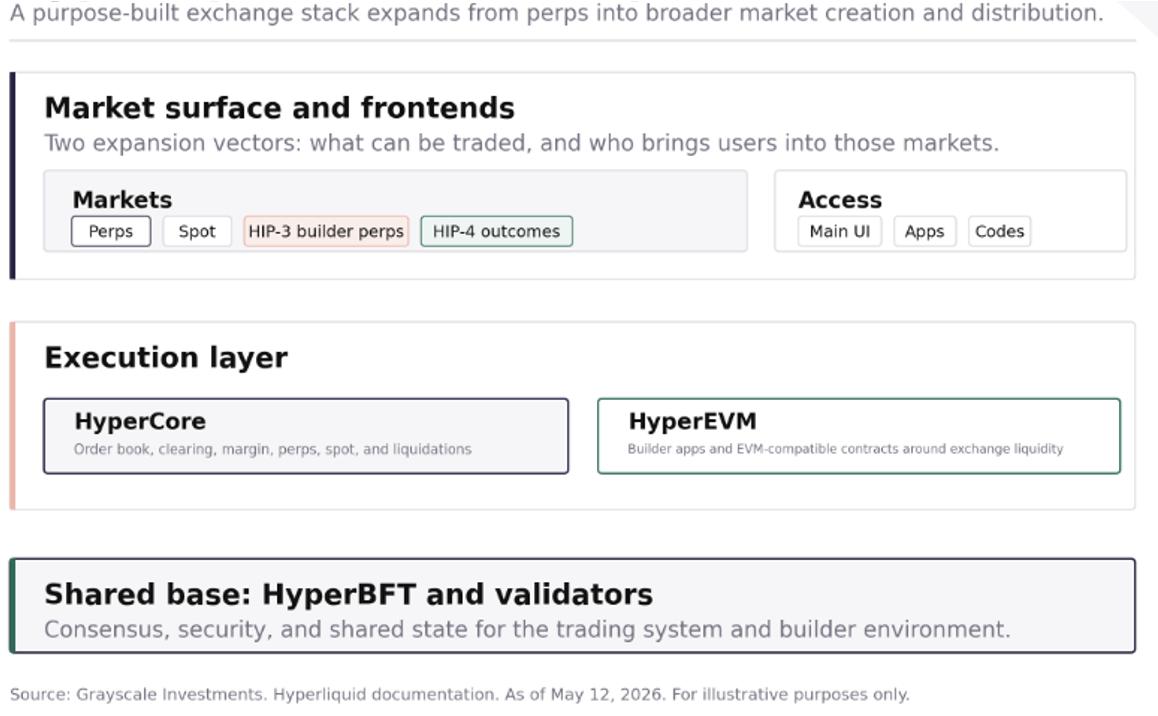

Hyperliquid's underlying architecture consists of two main core components:

- HyperCore: The core trading system, integrating functions such as order book, clearing and settlement, perpetual contracts, spot trading, margin management, and forced liquidation. It is also the core module for traders to interact with directly.

- HyperEVM: A runtime environment for developers, compatible with the Ethereum Virtual Machine (EVM) and integrated with the Hyperliquid system. Its core design philosophy is that developers can build applications based on the existing liquidity, user base, and asset base of exchanges, without having to start from scratch.

In addition, HyperBFT, as the delegated proof-of-stake consensus layer, is responsible for ensuring the secure and stable operation of the entire system.

Compared to the complex technical details, the project's architectural design philosophy is more crucial: Hyperliquid is not an ordinary application built on a general public blockchain, but a dedicated public blockchain and execution architecture customized for exchange trading performance, with the goal of making the overall experience of on-chain trading platforms comparable to centralized trading infrastructure.

Chart 10: Hyperliquid as a Marketplace Platform

Core elements of success

Hyperliquid officially launched in August 2023, at a time when the US had not yet launched any Bitcoin exchange trading products, and the entire DeFi industry was in a relatively sluggish phase. Its success did not stem from market speculation, but rather from precisely addressing industry pain points: creating a smooth on-chain trading platform for high-frequency traders.

We have summarized five key elements for success:

- Product positioning is focused: the platform is deeply refined around the perpetual contract trading scenario, rather than treating trading functionality as just one of many applications. It prioritizes meeting the core needs of high-frequency traders: fast order placement, stable execution, clear position information, and an interface that aligns with the usage habits of mainstream exchanges.

- Precise market selection: Timely launch of trading instruments in high demand by crypto traders, especially niche assets and popular instruments other than Bitcoin and Ethereum, thereby quickly gaining attention.

- The platform is flexible and open: relying on the HIP-3 mechanism, third-party developers can directly list on the new perpetual contract market, completely abandoning the centralized review and listing model and transforming into an open market creation system.

- A robust traffic distribution system: The platform's developer code and front-end integration model attract various third parties to direct users to the same liquidity pool, preventing traffic fragmentation. This model has already generated substantial revenue: Phantom has historically earned approximately $19.7 million from referral transaction fees through its integration with Hyperliquid perpetual contracts.

- A solid community foundation: Token distribution prioritizes rewarding platform users, rather than venture capitalists or insiders. Early token holders consisted primarily of traders, market participants, and developers. This group is deeply integrated with the project, reinforcing the perception that the project won't extract profits from the community before the product is mature. This is especially crucial in an industry environment where trust is scarce.

While none of these advantages are absolute barriers on their own, when combined, they make Hyperliquid one of the few projects in the industry that can prove its value through real user activity, rather than just remaining at the conceptual level.

The platform leverages liquidity, traffic distribution, and developer incentives to create a synergistic effect, building competitive barriers. Increased trading activity optimizes liquidity and the trading experience, attracting more users and third-party front-end integration. Furthermore, developer code and the HIP-3 mechanism encourage external developers to channel traffic back to the same liquidity pool, rather than diverting it to competing platforms. This creates a network effect that is difficult for new entrants to replicate: liquidity attracts traffic, traffic drives up trading volume, and trading volume further solidifies the protocol's economic foundation.

HYPE Token Explained

The HYPE token is the core driving force of the Hyperliquid ecosystem. Unlike most current crypto projects, this platform has not accepted traditional venture capital investment and instead airdrops approximately 30% of its total token supply directly to early users. This also determines the token holder structure: early holders are mostly platform users, traders, and community members with a deep understanding of the product.

Figure 11: Price of HYPE token since listing

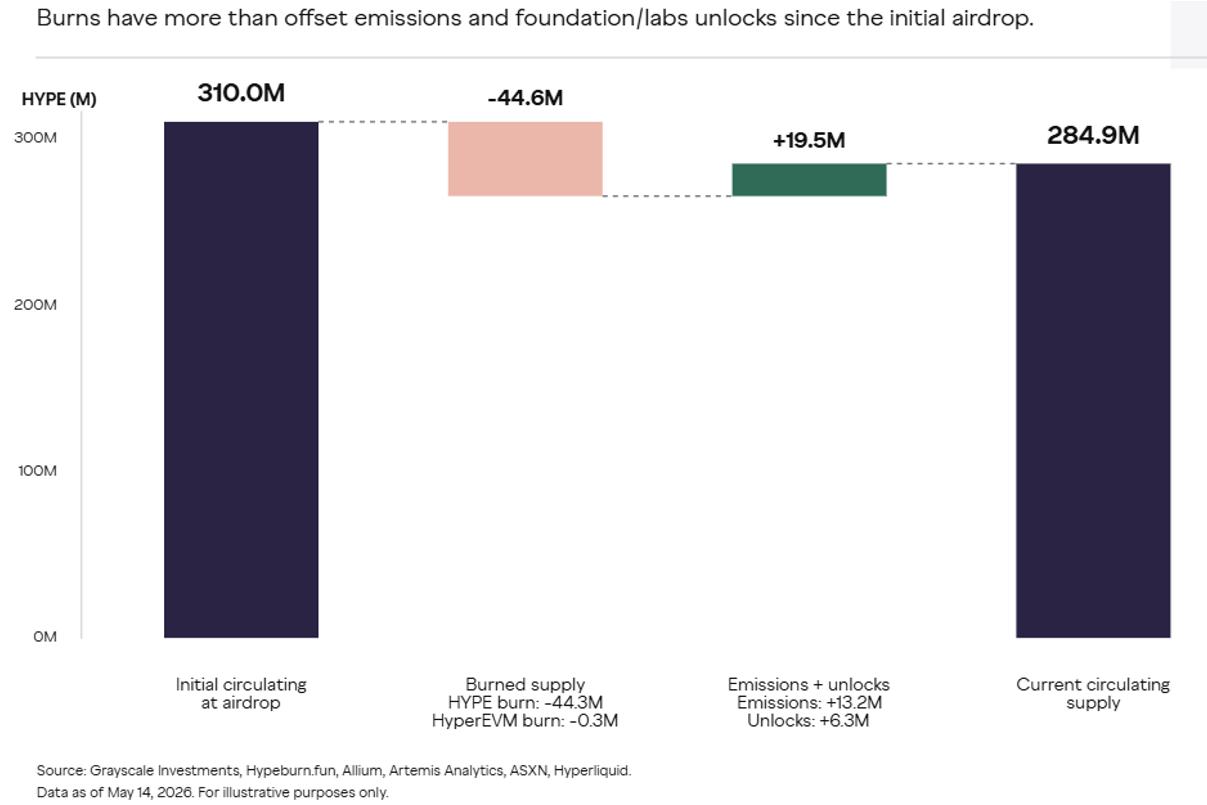

HYPE's value stems from transaction fees and its practical applications within the ecosystem. Hyperliquid Labs has confirmed that 99% of the platform's transaction fees will go to a rescue fund, which will then convert these fees into HYPE and burn them—a model similar to share buybacks in the traditional stock market. As the amount of tokens burned consistently exceeds the amount newly issued, the total circulating supply of HYPE is gradually decreasing.

Chart 12: HYPE Destruction, Issuance and Circulation Supply

At the same time, HYPE has several practical uses within the ecosystem:

- Staking and Node Verification: Users stake HYPE to participate in node verification, providing security for the entire network.

- Gas Fees: As the native fee token of HyperEVM, the base fee and priority fee of this module will be burned.

- Fee reduction: Pledged HYPE can enjoy preferential transaction fees.

- Market Collateral Creation: Developers wishing to deploy a perpetual contract market via HIP-3 must pledge 500,000 HYPE tokens. This pledged asset serves as both a guarantee of shared benefits and a safeguard for the market's operational quality. The HIP-4 results trading market is now live; if similar staking rules are adopted, the application scenarios for HYPE will be further expanded.

HYPE leverages trading platforms with real trading volume, fee revenue, and developer demand to achieve value growth. The higher the platform's trading volume, the more prominent the roles of fee rules, staking levels, developer reward systems, and bailout fund mechanisms become. As HyperEVM, HIP-3, and HIP-4 continue to expand the platform's boundaries, HYPE's application value and value growth potential will also increase accordingly.

Development Prospect Analysis

Hyperliquid has created a unique integrated financial services platform, making it challenging to accurately assess its growth potential. However, based on reasonable industry benchmarking analysis, we believe both the platform and its token have ample upside potential.

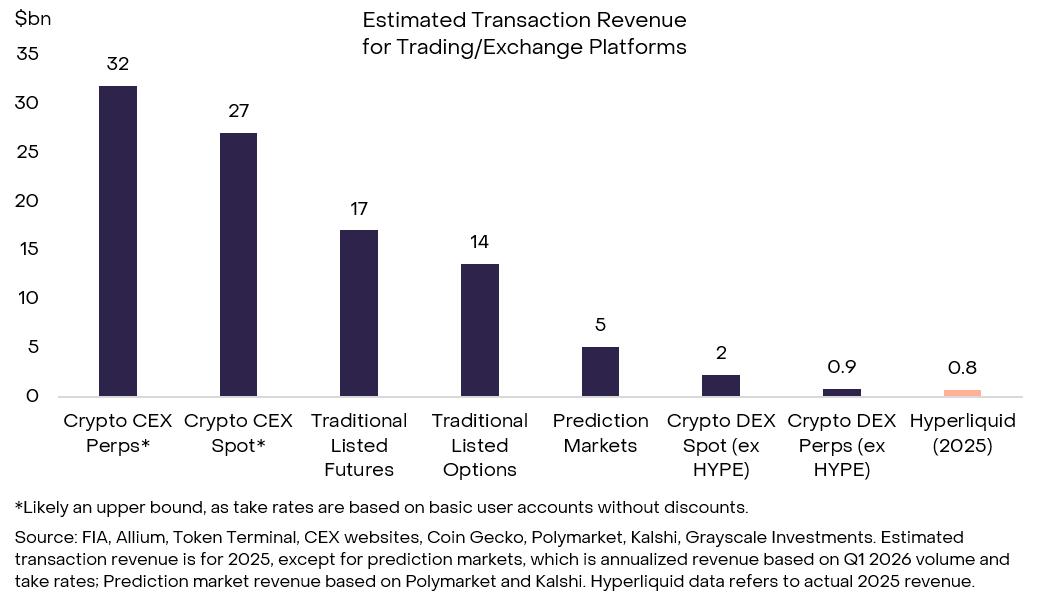

A comparison of revenue data from various trading platforms reveals that while Hyperliquid's revenue of approximately $800 million in 2025 is already considerable, it only accounts for about 2% of the total trading revenue of crypto perpetual contracts. If the platform's non-crypto asset-related businesses continue to expand, it is expected to gain a share of the global derivatives trading industry, which is valued at $35 billion to $400 billion annually.

Chart 13: Hyperliquid's revenue remains at a moderate level compared to the exchange industry.

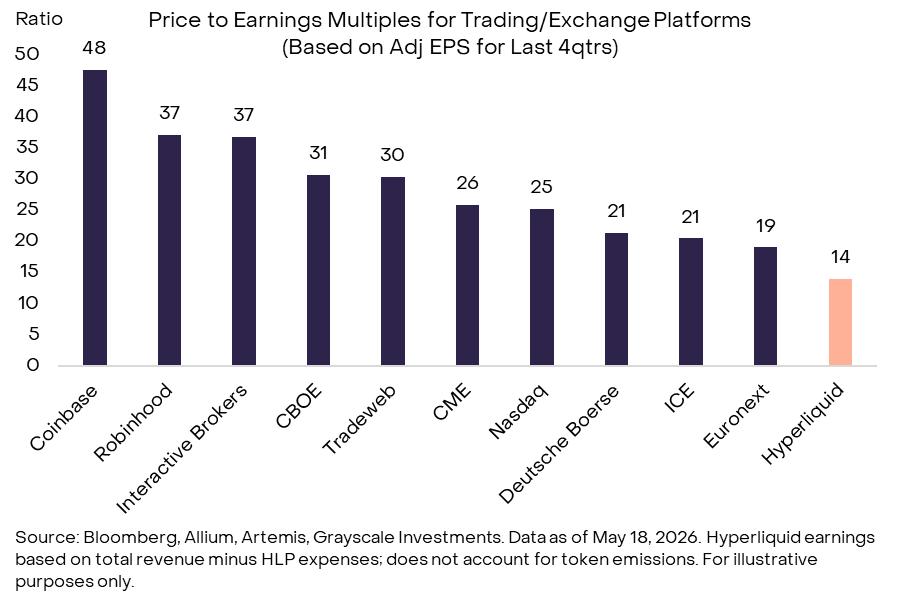

HYPE is not a traditional stock, but its valuation can be compared with listed companies in the financial industry. Based on earnings for the four quarters ending in Q1 2026, HYPE's current price-to-earnings ratio (P/E ratio) is approximately 14. In contrast, the valuation ranges for exchange-traded and brokerage firms vary, with high-growth companies like Interactive Brokers and Robinhood typically having P/E ratios between 35 and 50.

Chart 14: Hyperliquid's valuation multiples are lower than its stock counterparts.

The Development Prospects of Perpetual Contracts in the US Market

Hyperliquid sits at the intersection of two major regulatory vacuums in the United States: perpetual contracts and decentralized exchanges. Currently, the regulatory frameworks for both areas are gradually becoming clearer.

For a long time, perpetual contracts have been largely unable to operate normally in the US market. While not explicitly prohibited by regulations, the product does not fully comply with the Commodity Exchange Act (CEA), which regulates commodities and derivatives. This act clearly defines clearing rules, margin requirements, and trade execution standards for registered exchanges. This ambiguity in regulations has led regulators to continuously crack down on centralized platforms and DeFi platforms offering over-the-counter derivatives services. This is the core reason why Hyperliquid chose to operate overseas and block US users.

However, the regulatory environment is rapidly changing. The U.S. Commodity Futures Trading Commission (CFTC), responsible for enforcing the Commodity Exchange Act, has recently been making frequent pronouncements, and companies such as Coinbase, Kraken, Robinhood, and Kalshi have also taken action. All these signs indicate that regulators are actively exploring compliance paths and promoting the implementation of perpetual contract products. The core point of contention lies in the product's classification: according to the Commodity Exchange Act, should perpetual contracts be classified as futures or swaps? The regulator's final choice of classification method (formulating new rules, issuing guidance, or granting an exemption) will directly determine the timeline and stability of the product's implementation.

In the short term, regulatory benefits will primarily flow to centralized trading platforms that have already completed registration. However, in the long term, new rules, guidelines, or exemptions issued by the CFTC are expected to open up channels for compliant operations in the United States for platforms like Hyperliquid, reducing their reliance on overseas markets.

Meanwhile, the business nature of Hyperliquid-like exchanges has also embroiled them in regulatory discussions surrounding decentralized finance protocols. Currently, the United States lacks specific regulations for decentralized exchanges. Regulatory bodies adhere to the principle that "decentralization cannot be a reason for regulatory exemption," and, in conjunction with existing rules from the U.S. Securities and Exchange Commission (SEC) and the CFTC, regulate DeFi platforms based on the substance of their business operations.

For decentralized exchanges (DEXs) that primarily focus on derivatives, increasingly stringent regulatory scrutiny presents numerous obstacles to direct institutional investment. Currently, most institutions participate in trading through intermediaries or overseas channels. New legislation, such as the Clarity Act, aims to establish a more comprehensive and clearly defined regulatory framework for the digital asset market, clearly distinguishing between the protocol layer, front-end operators, intermediaries, and registered trading venues. Furthermore, the SEC's initiatives regarding tokenized securities will also drive the standardization of on-chain trading markets. However, for Hyperliquid's perpetual contract business, the most directly relevant regulatory bodies remain the CFTC and the Commodity Exchange Act.

This regulatory distinction is crucial for Hyperliquid: as a non-custodial infrastructure, the ultimate regulatory approach for its underlying protocol may differ from that of the front-end interface and operating entity for ordinary users. While current proposals haven't yet created a complete and feasible regulatory framework for on-chain perpetual contracts, they have pointed the way forward. If subsequent supplementary regulations, clear definitions of brokers, and specific rules for on-chain transactions (margin, funding rates, 24/7 trading, etc.) are introduced, the industry regulatory system will be further improved. The overall policy direction is to "encourage innovation within the regulatory framework," and Hyperliquid's open, global, and non-custodial positioning aligns with the current regulatory approach of "retaining permissionless access while improving market regulation."

Potential risks

Investing in HYPE requires careful consideration of both the platform's and token's inherent and specific risks: First, HYPE's annualized price volatility is approximately 80%, 40 percentage points higher than Bitcoin, indicating significant price fluctuations. Second, compared to other blockchain networks, Hyperliquid has a higher concentration of validator nodes, and the platform operates using closed-source software. Third, the platform's growth potential is highly dependent on adjustments to US financial regulatory policies. If regulatory rules are delayed, the platform will be confined to overseas markets for an extended period, and its growth potential will be limited.

Summarize

In both the crypto industry and traditional finance, it's difficult to find a project that can directly rival Hyperliquid, as it has completely disrupted the industry's established models. We believe it outlines a highly attractive development blueprint for the future of blockchain finance.

This is an open architecture platform that embraces permissionless innovation and adheres to the core principles of DeFi transparency and asset self-custody. Simultaneously, relying on its deeply refined core trading applications, it has gained recognition from both the market and users. If the platform can continue to operate steadily, maintain and expand its community ecosystem, and further benefit from favorable regulatory policies to achieve widespread adoption, Hyperliquid has the potential to grow into a giant in the financial services sector.

refer to

[1] Data source: Coin Metrics, Artemis, Grayscale Investments, data as of December 31, 2025

[2] Ranking source: coinmarketcap.com, statistics as of May 18, 2026, excluding stablecoins.

[3] This proposal mechanism is similar to the public chain upgrade mechanisms such as Ethereum Improvement Proposals (EIPs) and Bitcoin Improvement Proposals (BIPs).

[4] Source: Bloomberg, “Crypto Traders Hedge Iran War Risks With 24/7 Oil, Gold Trading”

[5] Source: Bloomberg, "Oil Trades Are Booming on 24/7 Crypto Exchange Hyperliquid"

[6] Data source: Allium, February 5, 2026, daily trading volume of silver perpetual contracts was approximately US$4 billion.

[7] Data source: Blockworks Research

[8] Data source: Coingecko

[9] Source: S&P Global

[10] Data source: Allium, data as of May 11, 2026

[11] The Ethereum Virtual Machine (EVM) is the underlying software for most public blockchains to run decentralized applications.

[12] Data source: Flowscan

[13] Token airdrop: directly distributed to users' personal wallets

[14] Revenue estimation: Grayscale Investment calculated the revenue based on publicly available transaction volume data and multi-channel industry fee rates.

[15] The estimated trading revenue of centralized exchanges is the upper limit, and the calculated fee rate is based on the basic account and does not include large transaction discounts.

[16] Criteria for selecting benchmark companies: companies whose main business is trading, trading infrastructure, and brokerage services, and which possess market data and network effects; valuations are only for reference when valuing trading platforms, and the companies mentioned in this article do not constitute any investment advice.

[17] Data source: Artemis, Grayscale Investments, based on 90-day actual price volatility statistics, data as of March 18, 2025