The competition in consumer AI has officially escalated from a "product war" to an "ecosystem war."

Article author and source: 0x9999in1, ME News

TL;DR

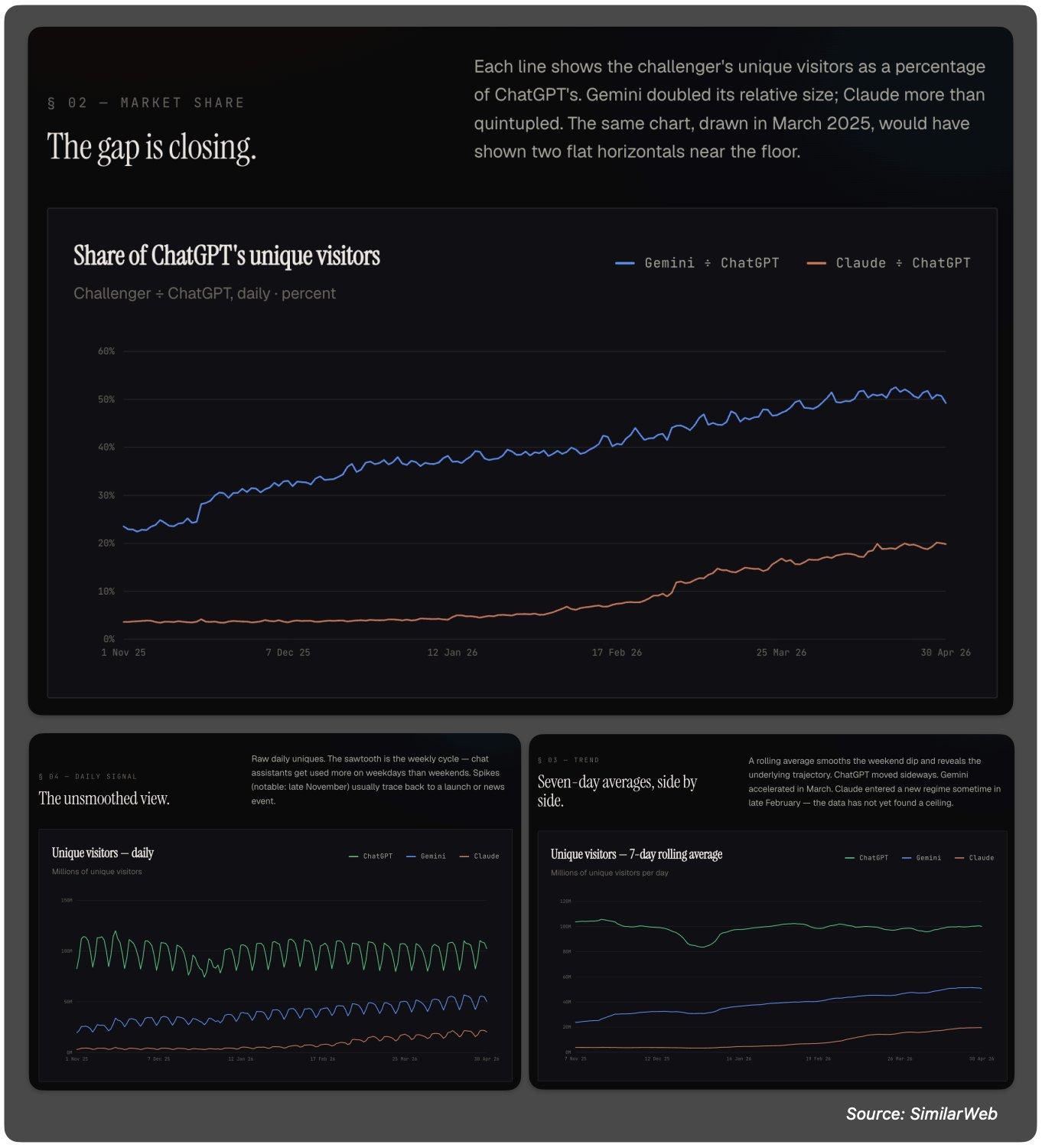

- ChatGPT's global traffic share plummeted from 80% to 60% in six months, marking the end of its era of absolute dominance.

- Gemini's unique visitors have more than doubled compared to ChatGPT, climbing from 20% to 50%, demonstrating Google's distribution capabilities.

- Claude surged to become the 36th largest website globally with a 255% quarter-on-quarter growth rate, making it the fastest-growing mainstream website.

- Converted to active users: ChatGPT approximately 900M WAU/1.5B MAU, Gemini approximately 500M WAU/900M MAU, Claude approximately 150-200M WAU/250-300M MAU

- Non-English speaking markets have become a key battleground, with Gemini already reaching 65%-70% of ChatGPT's market share in India, Brazil, Japan, and other regions.

- The competition in consumer AI has officially escalated from a "product war" to an "ecosystem war."

Sixty percent. What does this number mean?

Six months ago, ChatGPT accounted for 80% of consumer-grade AI traffic.

Eighty percent. It's practically a monopoly.

However, the latest data from SimilarWeb in May 2026 tells us that this number is now 60%.

In six months, it dropped by 20 percentage points.

In any industry, if a market leader loses a quarter of its market share within six months, it's a signal that needs to be taken seriously. It's not a crisis, but it's definitely a turning point.

This isn't because ChatGPT has gotten worse. GPT-5.5 has already been released, and its multimodal capabilities and inference depth are still improving. The problem isn't that it's "getting weaker," but rather that its competitors have finally caught up. And not just one, but two.

Google has arrived with Gemini. Anthropic has arrived with Claude.

The consumer AI market has officially shifted from a "one-man show" to a "three-way competition".

This is not a prediction. This is a fact that has already happened.

Gemini: Google has finally learned how to fight.

Let's look at Gemini's data first.

The percentage of unique visitor traffic relative to ChatGPT has more than doubled, from 20% to 50%.

500 million weekly active users, 900 million monthly active users.

What lies behind these numbers? It's that Google has finally done what it does best—distribution.

Recall the market reaction when Google launched Bard at the end of 2023: ridicule. "Another Google flop." "The search giant doesn't understand AI."

But Google did one thing right: it didn't rush.

They renamed Bard to Gemini, refined the model, and then made a crucial decision—to embed Gemini into all Google products: Search, Gmail, Docs, Android, Chrome. Reaching billions of users was seamlessly integrated overnight.

This is what makes platform companies so terrifying.

ChatGPT requires users to actively open a website or download an app. Gemini doesn't. It's there when you open a Google search. It's there when you compose an email. It's there when you use your phone.

You don't need to "choose" Gemini. You just need to not reject it.

This strategy is particularly evident in non-English speaking markets. Data shows that Gemini's traffic in India, Brazil, Japan, Indonesia, South Korea, and Vietnam has caught up with ChatGPT by 65% to 70%.

Why these markets?

This is because Google's market share in these regions is already extremely high. Over 90% in India, over 95% in Brazil, and over 75% in Japan. Google's infrastructure is essentially Gemini's distribution infrastructure.

What will ChatGPT rely on in these markets? Brand awareness? Product reputation?

These are certainly useful. But when competitors' products are directly integrated into operating systems and browsers, the weight of the term "good product" is diluted.

This is reminiscent of the browser wars of yesteryear. Why did IE win against Netscape? Not because IE was better. It was because IE was pre-installed on every Windows computer.

History doesn't simply repeat itself, but the logic remains the same.

Of course, it's important to note a key difference: a significant portion of Gemini's 900 million MAUs are "passively reached" users—they may have only seen AI-generated summaries in Google searches and are not necessarily avid users. In contrast, ChatGPT's 1.5 billion MAUs likely represent a much higher proportion of users who actively engage and have in-depth conversations.

But does it matter?

In the logic of the internet, first comes reach, then habit, and finally loyalty. What Google needs to do now is to transform "passive reach" into "active usage." Considering that the Gemini model itself is already quite good, this conversion rate will only continue to increase.

Claude: A true dark horse

If Gemini's growth was "expected"—after all, it's backed by Google's distribution empire—then Claude's growth is a more intriguing story.

The website grew by 255% quarter-on-quarter. Its global website ranking jumped from outside the top 100 to 36th. It achieved the fastest growth among the world's top 100 websites.

There is no operating system-level distribution. There is no product matrix with billions of users. There is no traffic entry point from a search engine.

What gives Anthropic the right to do this?

The answer may only be two words: reputation.

Claude's rise to prominence is completely different from ChatGPT and Gemini. It's not a top-down approach—it doesn't rely on overwhelming advertising, bundled sales, or platform distribution. It's a bottom-up approach—starting from the developer community and gradually penetrating to a wider user base.

Think about what has happened in the tech community over the past year.

In AI discussions on X, opinions such as "Claude is better than GPT" have gone from being a minority to becoming quite mainstream. Especially in tasks such as programming, writing, and analysis, the leap from Claude 3.5 Sonnet to the Claude 4 series has enabled many heavy users to make the switch.

Then came the explosion of AI programming tools like Cursor, Windsurf, and Kiro. These tools integrated Claude as one of their core models, allowing millions of developers to access Claude's output quality daily. These developers then promptly recommended Claude to everyone they knew.

This is the classic PLG (Product-Led Growth) path. The product is the growth engine.

From 3% to 20%. The relative proportion increased nearly sevenfold. The absolute number of users reached the level of 150-200 million WAU.

This is an amazing achievement for a company that was founded in 2021.

However, Claude's growth also has its concerns. Anthropic's conservative access strategy in some regions has limited its potential user base to some extent. While SimilarWeb data shows that Claude has seen growth in several emerging markets, its sustainability depends on how far Anthropic can go in its global operations.

The 255% growth rate proves the product's strength. But can product strength withstand the overwhelming dominance of platform distribution? This is the question Anthropic must answer next.

DeepSeek: Not among the top three, but not to be ignored.

Another noteworthy name in the data is DeepSeek.

Ranked 78th globally, with a quarter-on-quarter growth rate of 105% last quarter.

DeepSeek's story is completely different from the three companies mentioned above. It proves one thing: in the field of AI, "low cost and high efficiency" is a viable path.

But why did I say "three-way standoff" instead of "four-way competition"?

In terms of absolute size, DeepSeek is still orders of magnitude behind the top three. While its 105% growth rate is rapid, its current base means it's more of a regional, specific group's choice than a major player in the global consumer market.

However, DeepSeek's existence has made the competition healthier. Like a catfish, it reminds all the giants that AI capabilities aren't just about burning money.

Behind the 20 percentage point increase: What structural changes have actually occurred?

The 20 percentage points ChatGPT lost didn't disappear overnight. It was the result of several forces acting simultaneously.

First, the capabilities of the models are converging.

In 2023, there was a generational gap between GPT-4 and other models. By mid-2026, the gap between GPT-5.5, Gemini 2.5, and the Claude 4 series had narrowed to a level that most ordinary users could hardly perceive.

When the capabilities of models converge, what determines user choices will no longer be "who is smarter," but rather "who is more convenient," "who has a better experience," and "who feels more natural in my workflow."

This is bad for ChatGPT, because "being smarter" has been its core competitive advantage over the past three years.

Second, the diversification of AI entry points.

In 2023, consumers who want to use AI will almost have only one option: go to ChatGPT.

By 2026, if consumers want to use AI, it may already be embedded in their search engine (Gemini), their IDE (Claude via Cursor), their operating system (Apple Intelligence), and their social media software.

AI has transformed from "a destination" into "an infrastructure." When AI becomes infrastructure, the traffic of standalone AI applications will naturally be diverted.

Third, the differentiation of user needs.

What did early users do with AI? Chat, write copy, and ask questions. In these scenarios, ChatGPT's first-mover advantage was strong enough.

However, as the AI user base expands and deepens, needs are beginning to diversify. Programmers find Claude better suited for coding. Researchers find Gemini superior in its long context and multimodal capabilities. Creative workers have their own preferences.

The era of a single product serving all scenarios is over.

Is this a "ChatGPT crisis"?

To be honest, not entirely.

In absolute terms, ChatGPT's 900M WAU and 1.5B MAU remain number one in the industry, far ahead of the competition. Its user base is still growing, but its market share is declining.

It's like the iPhone. The iPhone's market share has never exceeded 30%, but it takes over 80% of the industry's profits. Market share and commercial value are not entirely equivalent.

The real problem OpenAI faces now isn't "user churn," but rather "where is the growth ceiling." With ChatGPT already a world-leading website, its growth rate will naturally slow down. Gemini and Claude, starting from a lower base, will naturally have higher growth rates.

However, one warning cannot be ignored: if the share continues to decline at this rate—20 percentage points in six months—then ChatGPT will only have 40% left after one year.

What does a 40% market share mean? It means being a "leader" rather than a "dominant player." It means developers will consider multi-platform compatibility. It means enterprise customers will seriously evaluate alternatives. It means a dispersion of power.

For OpenAI, the most important thing now is not to stop the decline in market share—which may be impossible to stop—but to ensure that it remains at the forefront when AI enters the next stage (Agent, Embodied Intelligence, Multimodal Fusion).

Will the tripartite balance of power remain stable?

My assessment: It will happen in the short term, but not necessarily in the medium term.

In the short term, each of the three companies has its own competitive advantages. OpenAI has brand recognition and first-mover advantage, Google has distribution and data, and Anthropic has a strong reputation for technology and developer loyalty. None of them can completely eliminate the others.

However, in the medium term, several variables could disrupt the balance.

First, Apple. Apple Intelligence currently integrates multiple models, but if Apple decides to deeply integrate with one, it will be a game-changer. Its distribution capabilities across billions of iOS devices are enough to rewrite the landscape.

Second, the Agent ecosystem. As AI evolves from a "conversation tool" to an "execution agent," the concept of the entry point will be completely rewritten. Whoever has a more mature and user-friendly Agent ecosystem will be able to lock in the next stage of users. Currently, three companies are betting on this: OpenAI has Operator and Codex, Anthropic has Claude Code and the MCP protocol, and Google has Project Mariner. The outcome is still uncertain.

Third, regulation. The EU AI Act has been implemented, and other countries are following suit. If regulations become stricter on certain types of companies (such as platform giants like Google with massive amounts of user data), the landscape may be reshaped by external policy forces.

Fourth, price wars. Currently, the price difference between the free tiers and subscriptions of the three companies is not significant. However, if one company decides to trade price for volume—for example, Google making Gemini's high-end capabilities completely free—the other two will face enormous pressure. It's no secret that Google's ability to absorb losses far exceeds that of OpenAI and Anthropic.

What does this mean for the industry?

A three-way competition is good for users. Competition means faster iteration, lower prices, and a better experience.

This is also good for developers. It means no single platform can "lock you in." APIs can be switched, and models can be replaced. Developers' bargaining power has increased.

For investors, the signals are complex. On the one hand, the overall AI market is still growing rapidly—the absolute number of users for all three companies is increasing. On the other hand, the "winner-takes-all" narrative has been broken, which means that the uncertainty of individual company valuations is increasing.

OpenAI's latest valuation of $300 billion—what assumptions is this figure based on? If it's based on the assumption that "there can only be one winner in the AI market," then that assumption is being challenged by data. If it's based on the assumption that "the AI market is large enough to accommodate three giants," then this valuation might still hold true.

The key is: which story do you believe?

Conclusion

On the day ChatGPT was released in November 2022, the market narrative was "OpenAI has changed the world".

By May 2026, the market narrative had shifted to "AI changed the world—not just one company."

This transformation is of profound significance.

This illustrates that AI is not a product, but an era. Just as "Internet" is not equivalent to "Yahoo" or "Google," "AI" is not equivalent to "ChatGPT." When a technology is important enough, it will inevitably not be monopolized by a single company.

ChatGPT remains great. It ignited this fire. But once the fire is lit, it no longer belongs solely to the one who started it.

A 60% market share, 900 million weekly active users, and 1.5 billion monthly active users—these figures would be the envy of any industry. But for OpenAI, the important thing is not how much it has today, but how much it can maintain tomorrow.

Or to put it another way: In the era of AI agents, does the concept of "traffic" itself still have meaning?

Perhaps on that day, all the data we discuss today will become historical footnotes.

But at least for today, this SimilarWeb data tells us one thing for sure:

The era of AI's reign has ended. The era of many contenders has begun.

References

- SimilarWeb, "Top Websites Ranking & Digital Market Intelligence," May 2026 data release. https://www.similarweb.com

- OpenAI, "ChatGPT reaches 900 million weekly active users," Official announcement, Q1 2026.

- Google, "Gemini surpasses 900 million monthly active users," Google I/O 2025 keynote, May 2025.

- Anthropic, "Claude usage and growth update," Company blog, Q1 2026.

- Reuters, "AI chatbot market fragments as Google and Anthropic challenge OpenAI dominance," March 2026.

- The Information, "Inside Anthropic's Rapid Growth: From Developer Tool to Consumer Product," February 2026.

- Bloomberg, "OpenAI's $300 Billion Valuation Faces Scrutiny as Market Share Erodes," April 2026.

- Statcounter, "Search Engine Market Share Worldwide," GlobalStats, Q1 2026.