Authors: Artemis and North Island Ventures (NIV)

Compiled by: Felix, PANews

Editor's Note: Robinhood (HOOD), a publicly traded company, has recently seen a strong stock price rebound, surging 6.8% on June 11, boosted by robust operating data and securing IPO underwriting qualifications. In response, Artemis and North Island Ventures (NIV) argue that Robinhood is poised to fully benefit from the largest intergenerational wealth transfer in history, driven by its Gold subscription, forecasting market growth, and the asset inflows expected from mega-IPOs like SpaceX, and that its current valuation remains undervalued. PANews has translated the original article; the details are as follows.

Most investors view Robinhood (HOOD) as a retail broker that fluctuates with the Bitcoin trading cycle. This narrow view overlooks the fact that Robinhood is becoming a financial super-app for Gen Z and Millennials, who are expected to benefit from the largest intergenerational wealth transfer in U.S. history. Robinhood Gold promises to be the "Amazon Prime" of retail finance, turning subscription revenue into a flywheel effect, making Robinhood higher quality, more recurring, and less cyclical over time. Prediction markets are an emerging retail asset class, and Robinhood's monthly active users (MAU) are already more than 20 times that of its second-largest native distribution competitors, such as Polymarket and Kalshi. Thanks to Robinhood's strong product iteration speed and its solid position among Gen Z and Millennials, its assets per customer will continue to grow, making Robinhood a winner in retail finance.

We believe that Robinhood has been misunderstood as an investment vehicle highly correlated with cryptocurrencies. Investors are ignoring the fact that Robinhood is evolving into a financial super app that will benefit from intergenerational wealth transfer, and that Robinhood is poised to benefit from two major catalysts in 2026: prediction markets and large IPOs of companies like SpaceX, Anthropologie, and OpenAI.

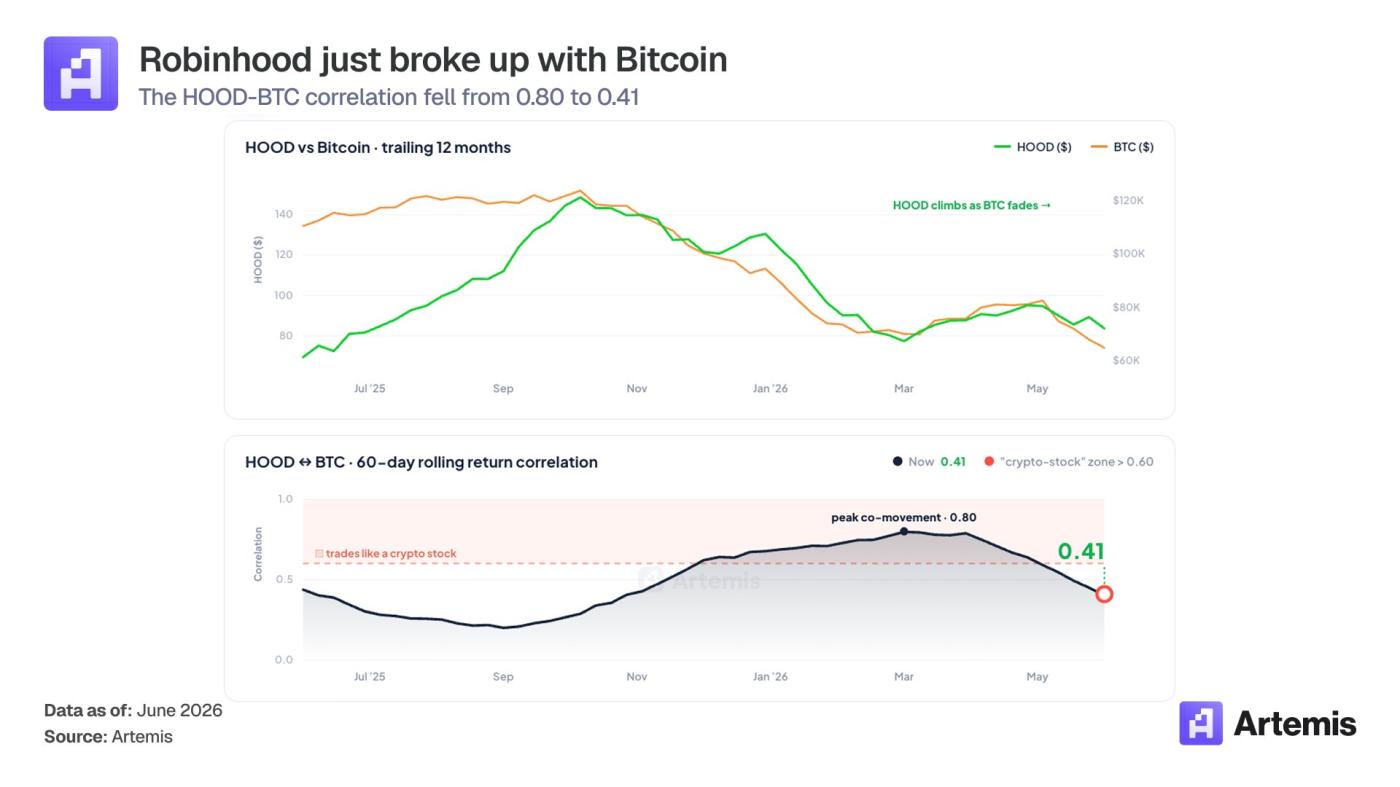

Most investors still categorize Robinhood as a "retail broker" and view it as an asset highly correlated with Bitcoin. This article aims to clarify this misconception: Robinhood's correlation with Bitcoin is gradually decreasing; it remained above 0.70 for most of 2026, but recently dropped to 0.41. Market pricing of the stock appears to tightly link it to options and cryptocurrency trading cycles. This view is incorrect, and this pricing bias will disappear as the super app concept gains traction.

1. Intergenerational wealth transfer and super applications

With a median age of 35, Robinhood users are poised to benefit from the wealth transfer from Baby Boomers to Generation Z and Millennials over the next two decades, a move expected to be one of the largest intergenerational wealth transfers in U.S. history. While Baby Boomers' account balances at traditional financial institutions are more than 20 times the median average balance of Robinhood users (approximately $12,000), Robinhood's relatively young user base means it doesn't have the heavy historical debt burdens that traditional financial institutions often carry.

As for why "now," the answer is a super app. Robinhood has a complete product portfolio across investment, retirement, savings, consumption, and speculative products, enabling it to absorb the funds that will soon flow in from intergenerational wealth transfer.

2. Prediction Markets as an Emerging Asset Class for Retail Investors

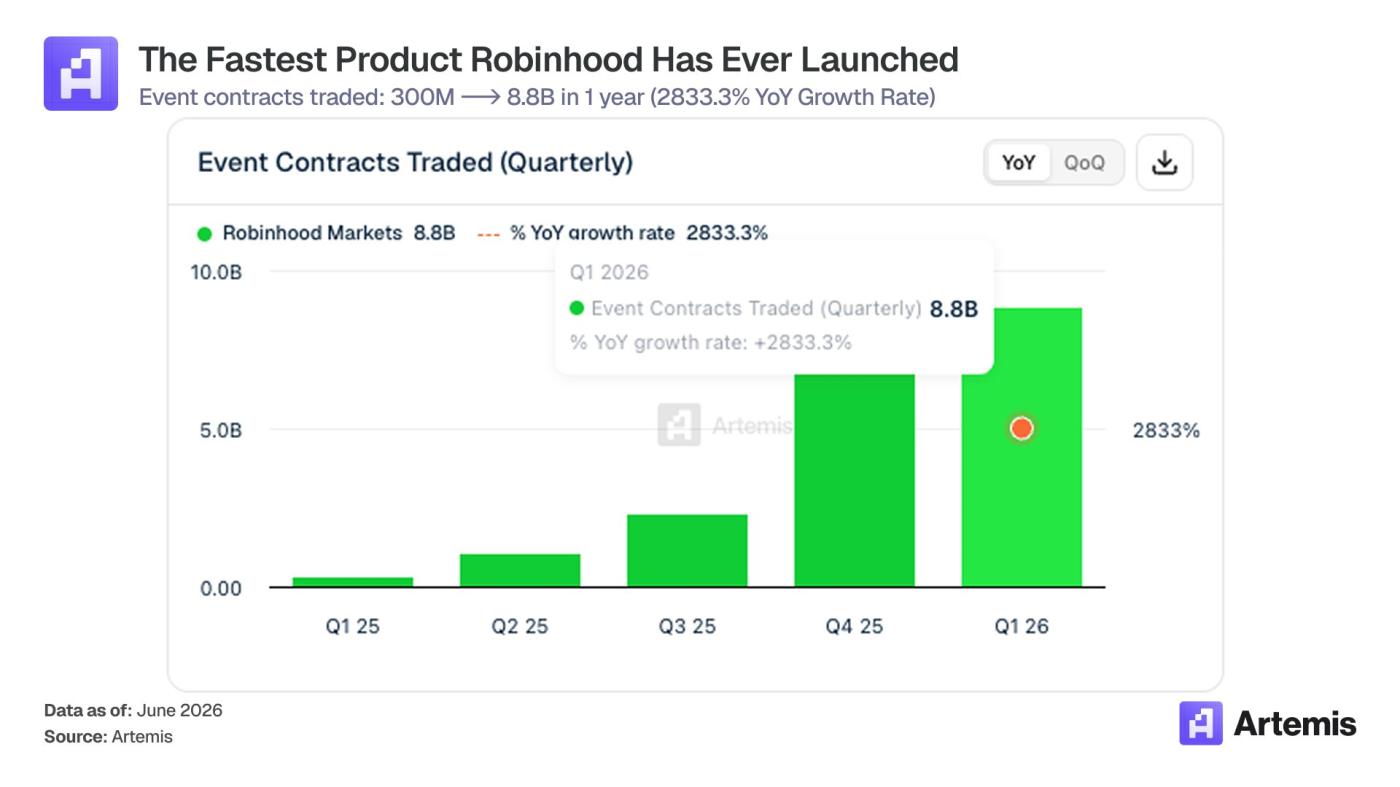

Event contract trading volume on Robinhood surged 30-fold from 300 million in Q1 2025 to 8.8 billion in Q1 2026, a 30-fold increase in four quarters. Revenue from prediction markets is projected to grow from approximately $3 million to approximately $104 million during the same period. This is one of the fastest-growing product lines in Robinhood's history, and major catalysts are still to come: the World Cup, the US midterm elections, the full NFL season, and the launch of Rothera, Robinhood's vertically integrated exchange and clearinghouse regulated by the CFTC.

Currently, trading volume on prediction markets on Kalshi and Polymarket has surged, and this is likely to be reflected in Robinhood's financial reports for the second and third quarters of 2026.

Both of these positive factors are still in their early stages and have not yet been reflected in the current forward price-to-earnings ratio.

3. Mega-IPOs may boost retail investor participation.

SpaceX plans its IPO on June 12, allocating a record 30% of its shares to retail investors. Typically, IPOs allocate 5-10% of their shares to retail investors. Anthropic and OpenAI are also likely to go public in the coming months. These companies have unprecedented funding needs, and retail investor interest is extremely high. These IPOs could boost user engagement on the Robinhood platform.

Why can HOOD benefit from wealth transfer?

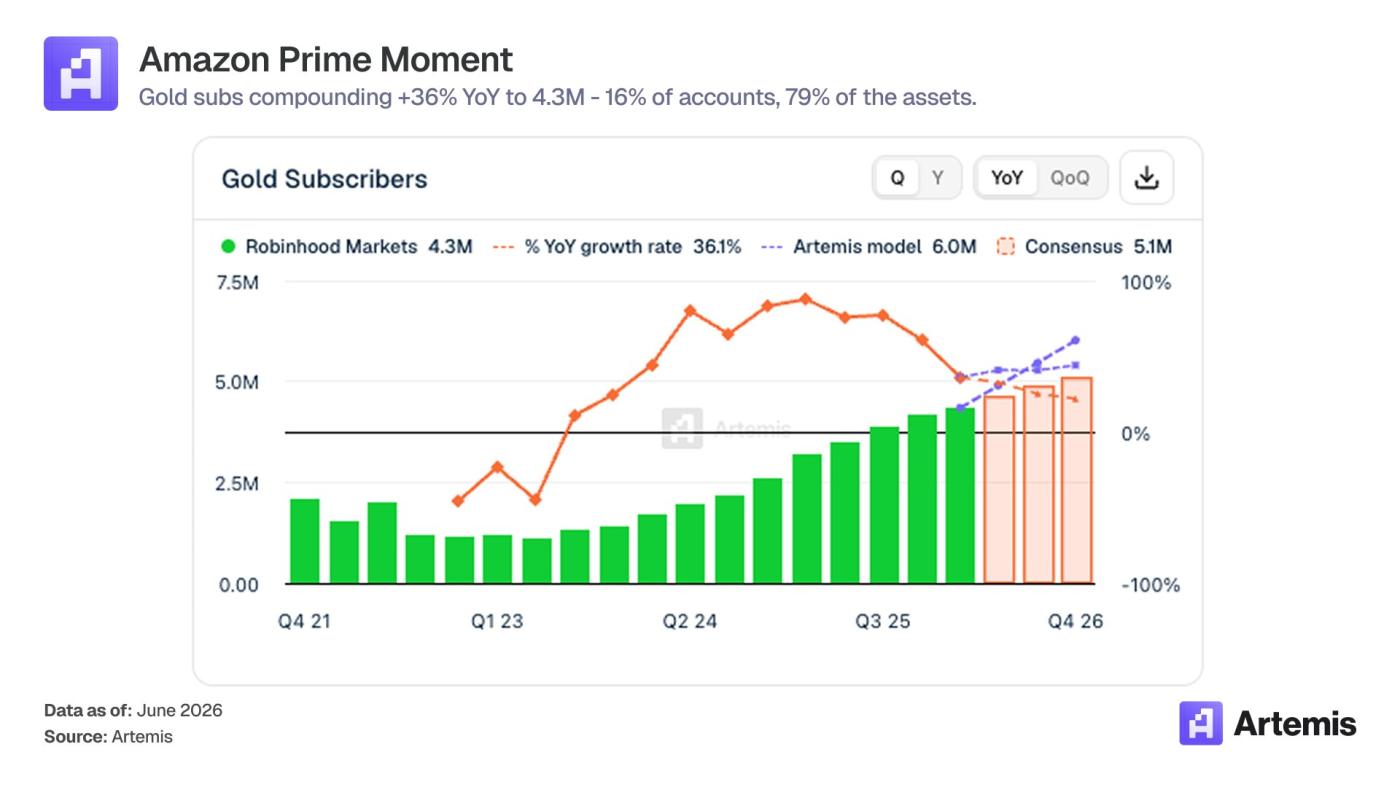

Robinhood's Gold membership grew 3.8 times in just three years, from 1.14 million at the end of 2022 to 4.34 million in the first quarter of 2026. The product costs $5 per month (or $50 per year). Members are estimated to receive approximately $880 in total value annually (including higher cash earnings, IRA matching, free margin, lower option fees, Robinhood Gold status, Morningstar research, secondary data, and Robinhood strategies).

The user demographics are crucial. Gold members comprise approximately 16% of funded accounts but account for around 79% of the platform's assets. They are the primary contributors to asset growth. Robinhood's expanding product portfolio allows it to better convert more users from its existing 27 million funded accounts into Gold members. As Gold membership penetration increases, all growth metrics—ARPU (Average Revenue Per User), net deposits, user retention, and gross margin—will increase accordingly.

We believe Prime transformed Amazon from a retailer into a consumption habit. The Prime subscription model increased user engagement, ultimately leading to increased spending on Amazon and creating more loyal, higher-value customers. We believe Gold can achieve a similar effect for Robinhood and has the potential to make Robinhood the next generation's preferred financial platform.

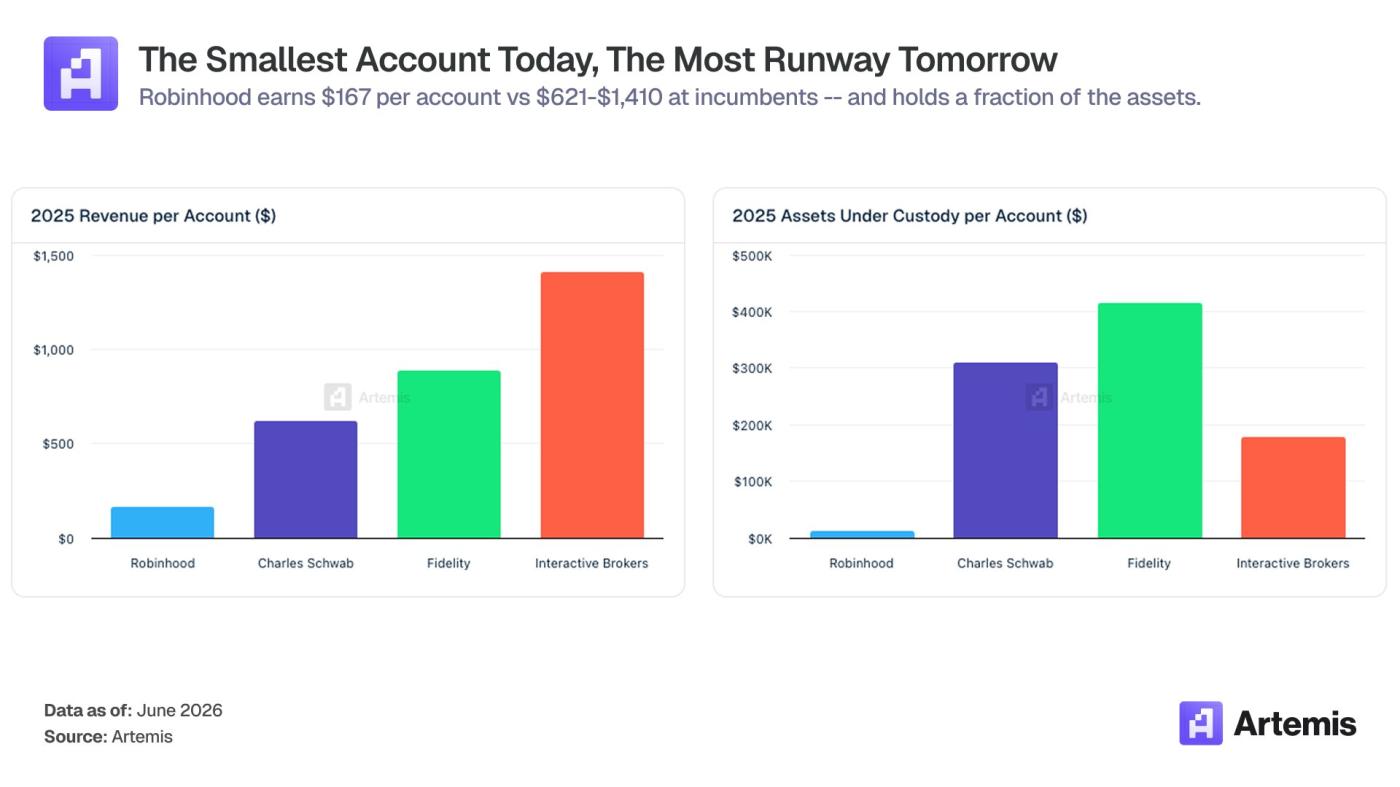

The asset base is converging. The average assets under management (AUC) per depositor grew from $2,700 at the end of 2022 to $11,900 at the end of 2025. Even at this rate of growth, Robinhood's AUC per client is still only about 5% of that of Charles Schwab, Fidelity Investments, and Interactive Brokers, all of which have much older assets under management than Robinhood.

The profit margin curve shows that the operating leverage effect has already materialized. Adjusted EBITDA margin rose from -7% in 2022 to 29% in 2023, 48% in 2024, and 56% in 2025. Costs are largely fixed: technology, operating, and general and administrative (G&A) expenses combined account for approximately 70% of the cost base. Therefore, the additional profit margin generated by new revenue exceeds 70%.

Why is HOOD likely to outperform in the prediction market?

This is perhaps the most underrated part of the whole story.

The prediction market has become a winner-takes-all market due to three key factors: distribution channels, product user experience, and integration with the user's broader financial graph. Robinhood has the potential to succeed in all three areas.

Distribution Channels: Robinhood boasts 27 million top-up accounts and approximately 13 million monthly active users. Kalshi's monthly active users are estimated at around 5 million; Polymarket has approximately 500,000. Robinhood's user acquisition gap with its second-largest native distribution competitor is more than 20 times.

Product Interface: Event contracts can coexist with stocks, options, and cryptocurrencies within the same application, using the same wallet, reporting, and risk management system. Standalone prediction market applications cannot achieve this without acting as brokers.

Vertical integration: Robinhood's exchange and clearinghouse, Rothera, is regulated by the U.S. Commodity Futures Trading Commission (CFTC), allowing it to control commission rates, launch markets quickly, and avoid paying third-party exchanges. Even if profitability remains constant, vertical integration can typically increase revenue by 25% to 30%.

We view the prediction market as a new asset class: much like spot cryptocurrencies in 2017 or zero-commission stock trading in 2014. The same pattern was seen in both cases: brokers who control retail distribution channels dominate the category and drive up valuations.

How can HOOD monetize through super apps?

Robinhood's revenue structure is changing.

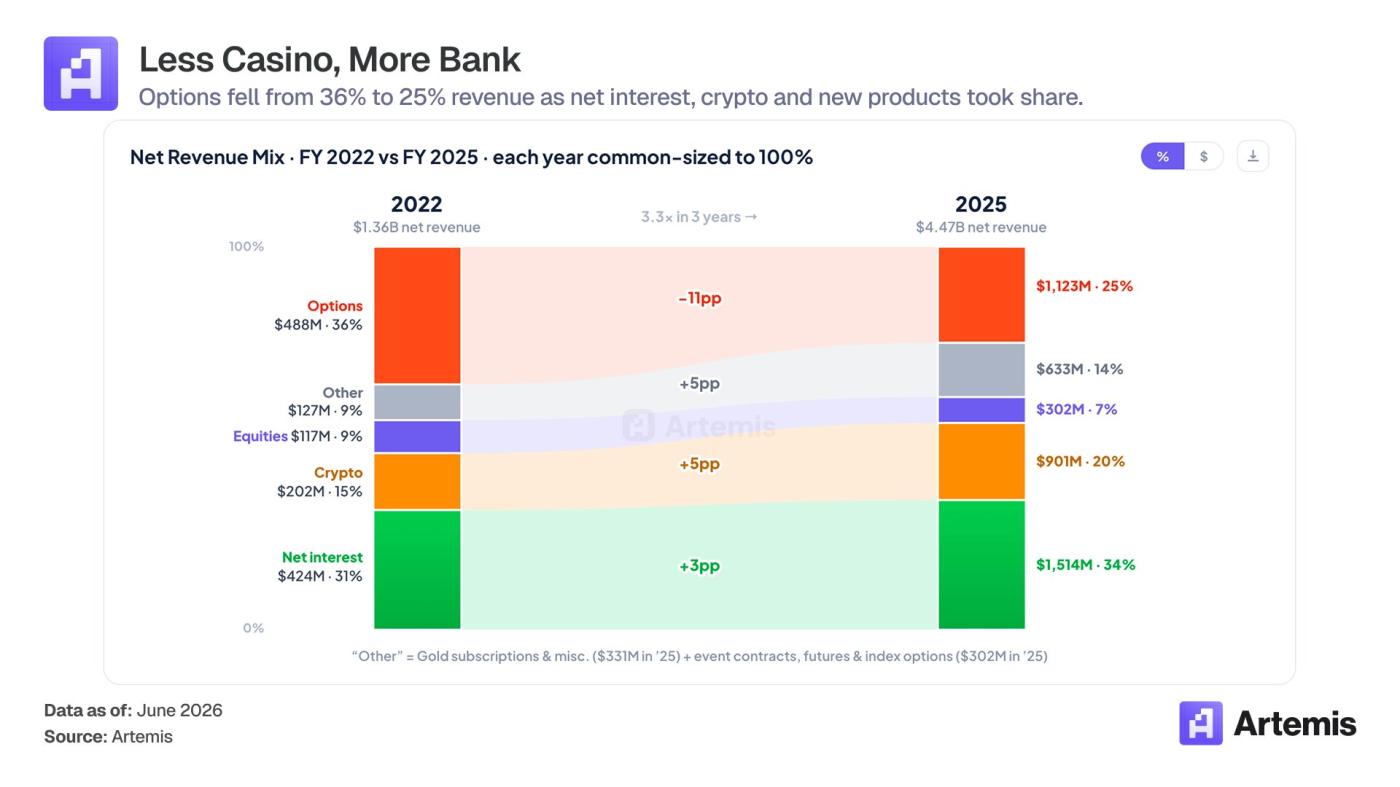

Trading revenue is no longer Robinhood's sole business. Net interest, Gold subscription fees, prediction markets, Robinhood's high-yield checking account, Gold credit card, retirement planning (TradePMR added approximately $40 billion in advisory AUM in 2025), Robinhood Strategies, and more recently, estate planning, are all independent revenue streams. Each targets a different stage of the user lifecycle and strengthens user relationships. We believe that these businesses work together to transform Robinhood from a company reliant on speculative trading revenue into a platform where users can generate sustainable income throughout their financial lives.

Why is there a discrepancy in the market's pricing of Robinhood?

HOOD is trading at approximately 34 times its projected 2027 earnings per share, roughly in line with the projections from Interactive Brokers and Coinbase. Three points suggest a discrepancy in HOOD's pricing:

- Gold accounts still account for only about 16% of the total number of accounts. As this percentage rises, compared to HOOD's current ARPU (average revenue per user) of $167, its ARPU is expected to structurally converge towards the range of $621-$1410 per account for traditional institutions. This is not a prediction, but rather the structural setting of the business.

- Prediction markets have become one of the fastest-growing product lines in the US retail finance sector, and Robinhood controls the distribution channels.

- The cost base is largely fixed. Even though the platform is still in the investment phase, its adjusted EBITDA margin has already reached 56% by 2025.

Because Robinhood occupies a different investment category, market attention has not yet caught up. Brokerage analysts are under-recognizing it. Fintech analysts view it as a cryptocurrency-related company. Cryptocurrency analysts view it as a traditional brokerage.

in conclusion

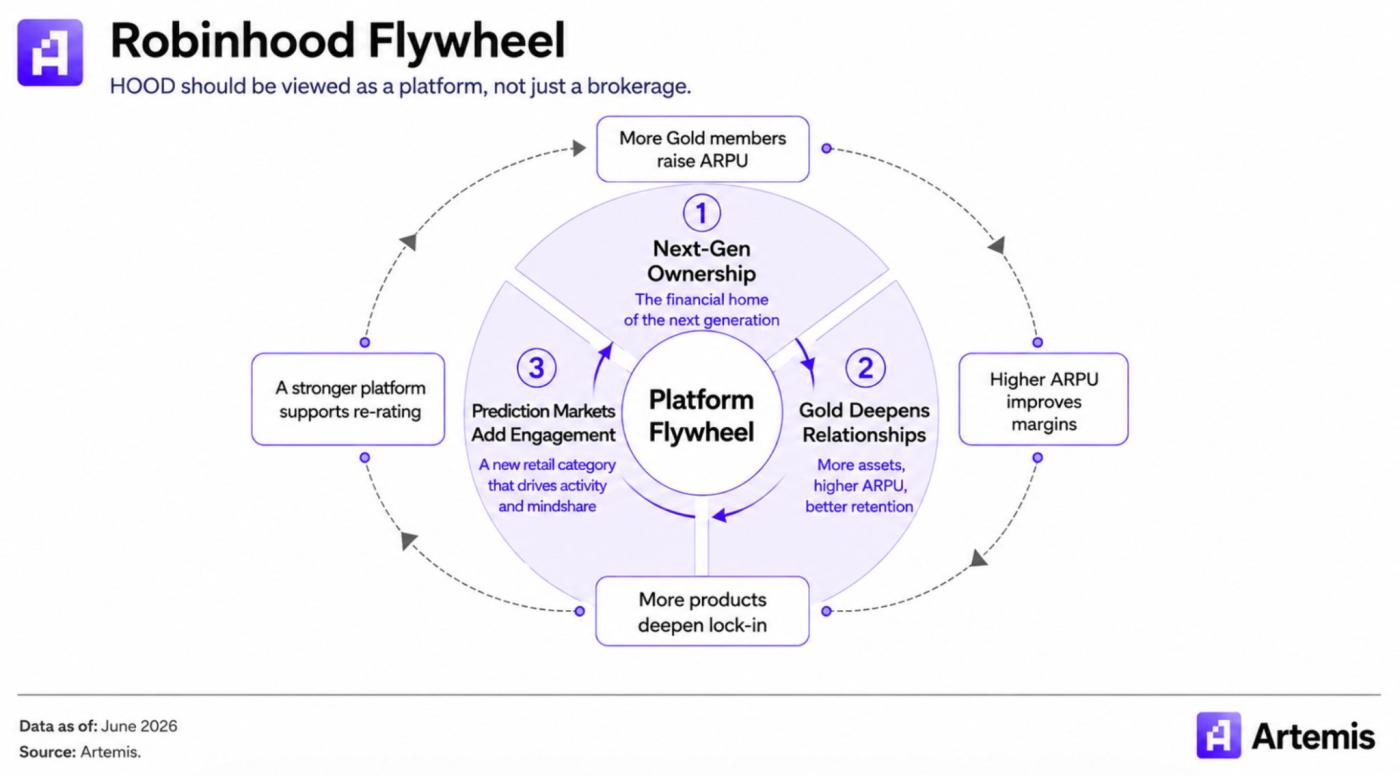

The market currently views Robinhood as a cyclical retail broker. But in our view, it is transforming into a distinct company: a vertically integrated financial mega-app serving those poised to benefit from the generational wealth shift from Baby Boomers to Generation Z and Millennials, with a rapidly growing new asset class operating within its app during this cycle.

We believe HOOD should be valued like a platform company, not a brokerage firm. Its flywheel effect is driven by three factors: (1) target user base percentage × (2) Gold-driven compound growth in assets × (3) market leadership in the predicted market category. Each new Gold user increases ARPU by one dollar, boosting profit margins. Each new product launch further locks in customers. We believe the longer this compounding effect lasts, the stronger its competitive moat will become.

This isn't a story for 2026. It marks the beginning of a decade of platform transformation that will impact how people save, trade, borrow, invest, and accumulate wealth in the next generation.

Related reading:Robinhood vs Coinbase: Who will be the next 10x stock?