SpaceX is a great company, that's for sure; but even great companies need to be bought at the right price to make a good investment.

Foreword: Starting with the mess in the crypto world

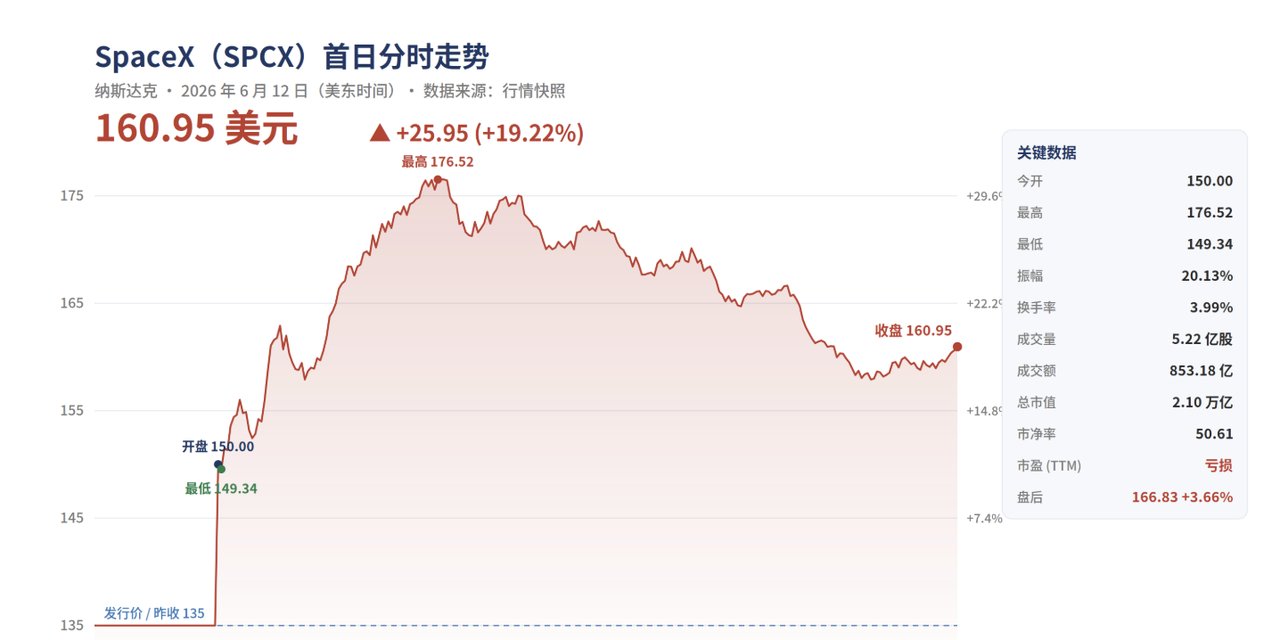

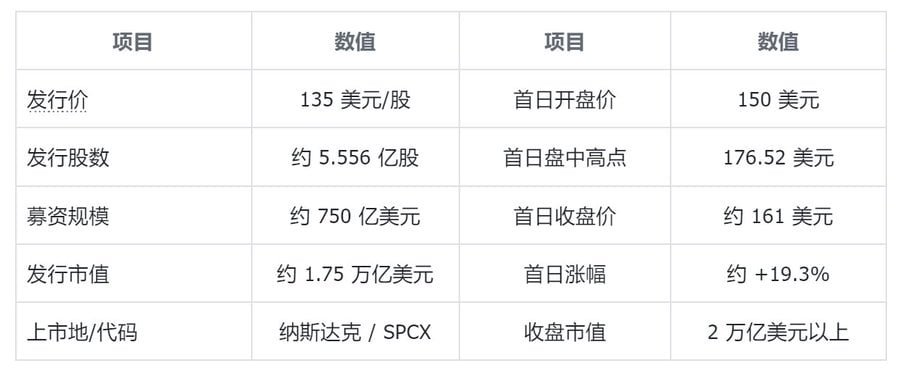

On June 12, 2026, Eastern Time, SpaceX officially listed on Nasdaq under the ticker symbol SPCX. Despite recording a net loss of approximately $4.9 billion for the entire year of 2025, the stock did not fall below its IPO price on its first day of trading as many had expected. The offering price was set at $135, and it jumped to $150 at the open, continuing to rise throughout the day, reaching a high of $176.52 before closing at approximately $161, a first-day gain of about 19%.

The company's market capitalization reached $2 trillion, making it the sixth largest listed company in the United States by market capitalization. This IPO also set a record for the largest IPO in human history.

Source: Nasdaq Stock Exchange

In stark contrast to the enthusiasm in traditional markets, the crypto is filled with complaints. Many exchanges had previously used tokenization to attract users through initial coin offerings (ICOs), only to almost all fail to secure users on the listing day. The core reason was the delayed allocation of the underlying shares.

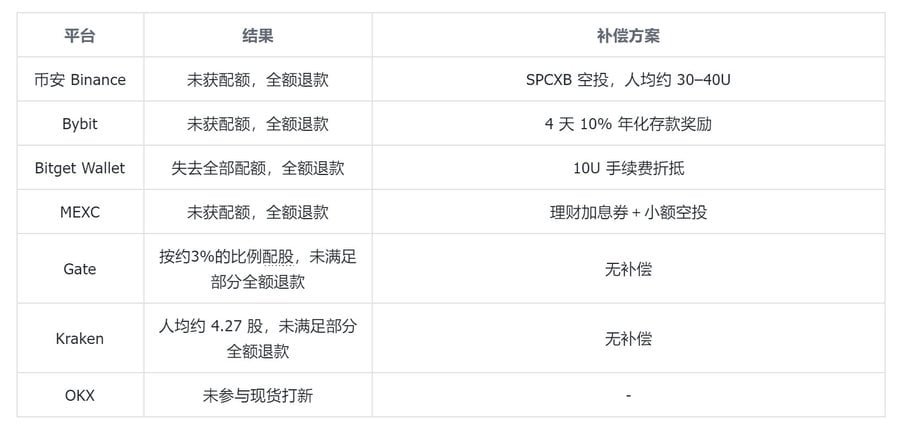

In summary, almost none of the platforms that connected to Kraken's xStocks platform received full shares.

Source: Twitter announcements from various exchanges

Specifically:

- Binance canceled the tokenized initial coin offering (ICO) event and offered full refunds, in addition to compensating the participants with an airdrop of SPCXB tokens worth approximately $1 million, with each participant receiving approximately $30 to $40.

- Bybit also offered a full refund and an additional 4 days of deposit bonus at an annualized rate of 10%;

- Bitget Wallet lost all its quota due to its integration with xStocks, and ultimately refunded users in full and provided a fee rebate of approximately $10.

- Kraken uses its own brokerage channel to distribute a fixed small allocation to all subscribers, averaging about 4.27 shares per person, with full refunds for any shortfall.

In other words, the IPO results given by several platforms were generally lower than users' initial expectations.

The common thread in the failures is clear: platforms that bet on xStocks all lost out because SpaceX was oversubscribed by about four times and the underwriters ultimately allocated a very limited share to crypto channels; and xStocks itself is a tokenized stock business that Kraken acquired at the end of 2025, so the supply bottleneck actually stemmed from Kraken's own operations.

It's worth mentioning a platform called MSX (Maitong MSX). During the SPCX IPO, unlike other exchanges, Maitong continued to offer users full allocations, even at a price lower than the offering price—which raised concerns in the community. Maitong explained that these allocations were obtained through Republic.

However, Bitget CEO Gracy pointed out that Bitget and Republic have an exclusive partnership, implying that Bitget has not partnered with Republic.

Numerous questions subsequently arose within the community, raising doubts about whether the source of the funds was an "electronic trading platform," as well as concerns that the platform might be unable to make payments and that there might be a surge in withdrawals.

Let's set aside this round of debate in the crypto for now. Regardless of the reliability of IPO subscription channels, what truly determines the profit or loss of an investment is the intrinsic value of the company and the purchase price. Therefore, let's return to SpaceX and answer three questions in turn: Is this company worth buying at the current price? Is its valuation justified? And what will the price likely do after its IPO?

I. SpaceX: A prospectus with a celestial tone

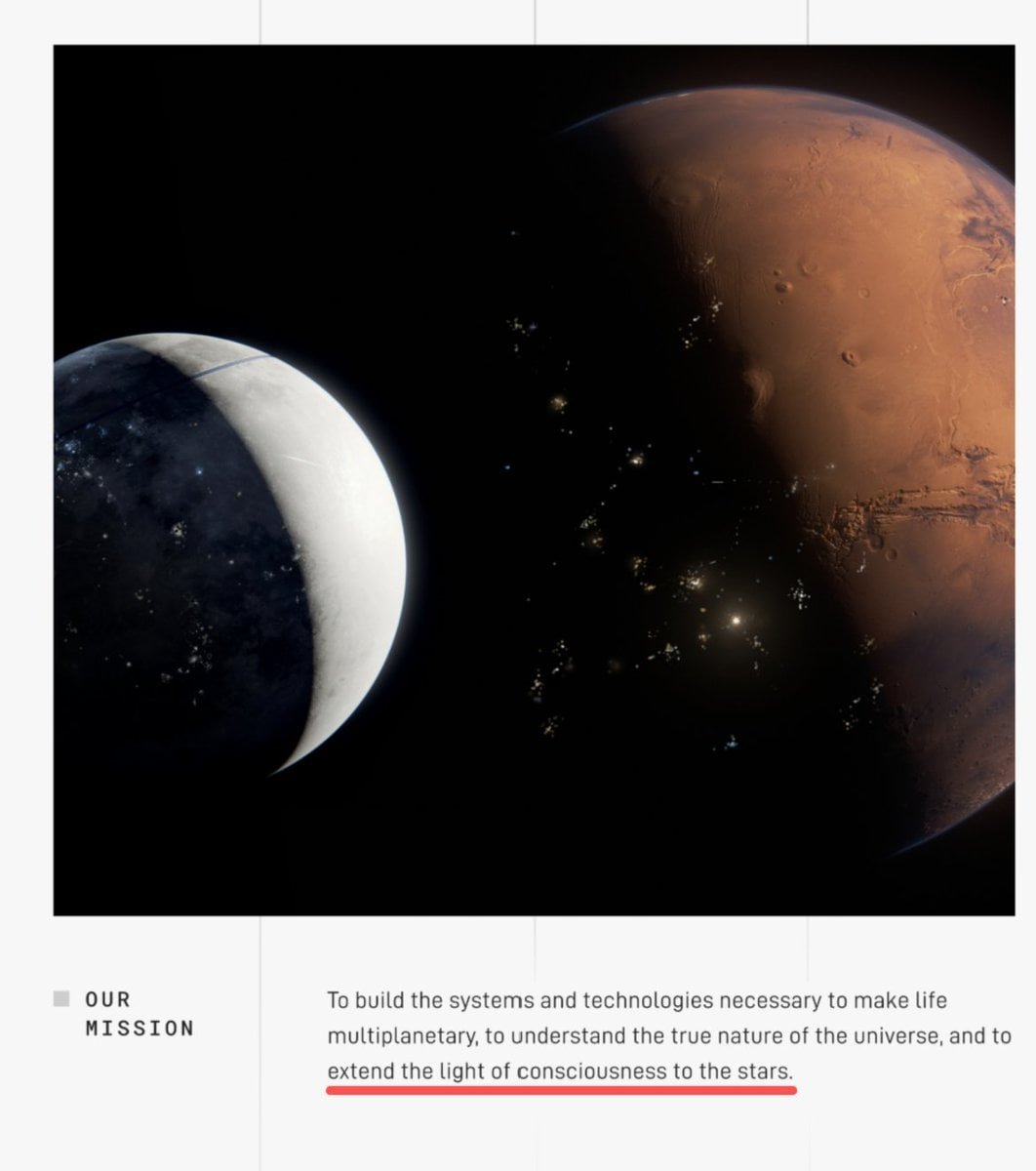

To understand Space Exploration Technologies Corp. (SpaceX), start by reading the first page of its prospectus. In its S-1 filing with the U.S. Securities and Exchange Commission (SEC), SpaceX states its mission in a sentence that hardly resembles a financial document:

The company’s mission is to build the systems and technologies necessary to enable life to reach multiple planets, to understand the true nature of the universe, and to extend the light of consciousness to the stars.

Source: SpaceX Form S-1, SEC EDGAR (Original text: “to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars”)

The prospectus then explains that xAI was founded in 2023 and acquired by SpaceX in early 2026, and has now become a pillar of the company's vertically integrated system; the company plans to begin deploying on-orbit AI computing satellites as early as 2028.

A rocket company that puts the sun, computing power, and consciousness in the first paragraph of its prospectus—this narrative intensity itself is part of the pricing and the starting point for all the subsequent debates.

Sources: SpaceX pricing announcement, CNN, NPR, The Motley Fool, June 2026

On its listing day, the stock opened at $150, reaching a high of $176.52 during the day before falling back to close at approximately $161, a gain of about 19.3% over the offering price. Based on the closing price, the company's market capitalization surpassed $2 trillion, and Musk's personal net worth also exceeded $1 trillion for the first time. The table below summarizes the key figures.

What made this day special wasn't just the price increase, but its structure, which was a result of a sophisticated supply-demand imbalance. Only about 4% of the company's equity was issued as Class A shares, with the remainder locked up; approximately 30% of the offering (about $22.5 billion) was allocated to retail investors. In other words, the entire $1.75 trillion company was priced through trading based on about 4% of its outstanding shares, with most sellers locked off —a point that will be repeatedly emphasized later, explaining both the initial surge and foreshadowing future volatility.

II. Valuation Breakdown: Why are they willing to give it two trillion?

To understand the $2 trillion valuation, SpaceX must be broken down into three business segments, as their profitability and valuation logic are completely different. According to the S-1 filing, in 2025, the company's consolidated revenue was $18.674 billion, operating loss was $2.589 billion, adjusted EBITDA was $6.584 billion, and net loss was approximately $4.9 billion.

Financial comparison of SpaceX's three main business segments (Source: SpaceX Form S-1)

The first segment is rocket launches (Space segment). This is SpaceX's core business and the part most familiar to the public, but it's not actually profitable in terms of financial statements. In 2025, this segment's revenue was approximately $4.1 billion, a year-on-year increase of only about 8%, and it recorded an operating loss of approximately $657 million, mainly dragged down by research and development investment in the next-generation Starship—Starship R&D expenditure alone was close to $3 billion in 2025.

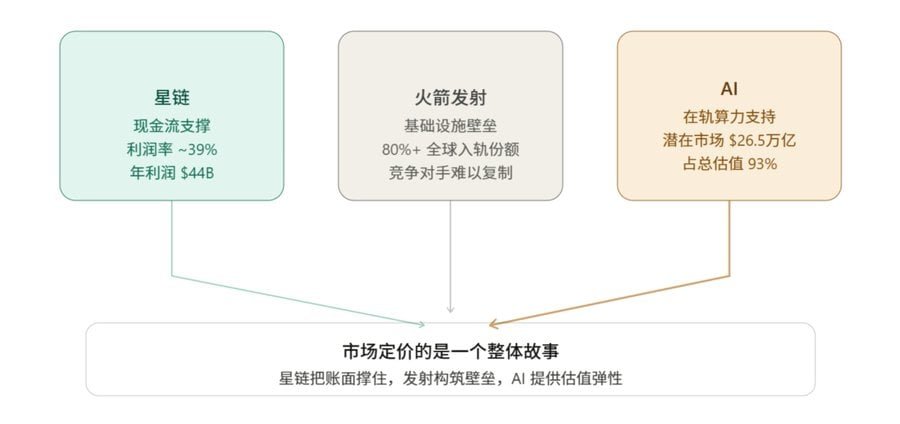

The second segment is Starlink (categorized under Connectivity), which is the real money-maker and the engine supporting the company's cash flow. In 2025, this segment generated approximately $11.4 billion in revenue, accounting for about 61% of the company's total revenue, and produced approximately $4.4 billion in operating profit, with an operating profit margin of nearly 39%. As of the end of March 2026, Starlink had approximately 10.3 million users, covering more than 160 countries and regions, with approximately 9,600 satellites in orbit. The key to its business model lies in economies of scale: once built, the marginal cost of adding a new subscriber is very low, and the more users there are, the greater the potential for profit margin expansion.

The third segment is AI, which has the greatest potential for valuation but also burns the most cash. It consists of xAI, which was incorporated in February 2026, and includes Grok large models, X platform advertising and subscriptions, and Colossus data center computing power. In 2025, this segment generated approximately $3.2 billion in revenue but recorded an operating loss of approximately $6.35 billion—Starlink's profits were essentially consumed by the expansion of this business.

Source: SpaceX prospectus

Based on the above, we can draw two conclusions:

- The biggest driving force behind SpaceX's IPO is actually AI, rather than the "rocket launch" itself. Therefore, SpaceX is also an important part of the AI narrative—which is also a major manifestation of the "AI bubble" that people have been worried about.

- What SpaceX is really selling to investors isn't its current financial reports, but a blueprint: using Starship to send data centers into orbit, directly harvesting solar energy to power AI, bypassing the constraints of the terrestrial power grid. The company is actually selling the concept of a "cosmic-scale AI data center," not the rockets themselves or large-scale AI models. —And the prospectus values the company's potential reachable market (TAM) at $28.5 trillion, with approximately 93% of that tied to AI-related sectors.

When you look at these three parts together, SpaceX's valuation logic becomes clear: the market is not pricing it as a rocket company or a satellite broadband company, but rather as a package of Starlink's cash flow, its launch moat, and its long-term vision of on-orbit AI computing power, all packaged into a cohesive story for pricing: Starlink is responsible for maintaining cash flow, rocket launches are responsible for building a capability barrier that others cannot replicate, and AI is responsible for providing upward flexibility.

The question above is: what exactly is the value of this flexibility space?

III. Valuation Support: Two Large Computing Power Orders and a Solid Cash Flow Base

High valuations require verifiable earnings anchors. SpaceX's S-1 prospectus does indeed contain several clues that can support the story: two signed computing power leases, plus the subscription-based cash flow generated by Starlink itself.

SpaceX's main profit drivers (Data source: SpaceX Form S-1, DatacenterDynamics, Markman Capital Insight)

Anthropic's $15 billion computing power contract: According to S-1, Anthropic is indeed continuously leasing computing power from SpaceX on a monthly basis for $1.25 billion per month. The leased computing power is located in the Colossus data center in Memphis. The contract text is written until May 2029, with an annualized value of approximately $15 billion and a total contract value of over $40 billion for the entire contract period.

Google's $11 billion computing power lease: Google has signed its second computing power lease, paying approximately $920 million per month to lease approximately 110,000 GPUs and associated computing power, with a term from October 2026 to June 2029.

Cash Flow Foundation and Pricing Shift: Besides the two major deals mentioned above, Starlink itself is the company's most stable source of revenue. In the first quarter of 2026, the Connectivity segment achieved an operating profit of $1.188 billion, and the number of subscribers reached 10.3 million as of the end of March. In May 2026, SpaceX raised prices on all Starlink consumer plans by up to $10 per month, marking a shift in the company's strategy from the past few years of trading price reductions for scale to monetizing its large existing user base.

Adding up these three guaranteed revenue streams, SpaceX is expected to collect at least $40 billion a year—a figure that already far exceeds its total revenue of $18.7 billion for the entire company in 2025.

IV. Questions: Fine print in the contract, outrageous multipliers

After clearly outlining the supporting points, we must also examine the vulnerabilities in its valuation: it will be very difficult for SpaceX to deliver on this valuation, for three reasons.

The contract is valid until 2029, but can be terminated at any time.

The two large computing power contracts appear to lock in revenue for several years, but a crucial line in the terms states that either party can terminate the agreement with 90 days' notice. Furthermore, Musk himself clarified on X that Anthropic's arrangement is essentially a 180-day lease, after which both parties have a rolling 90-day cancellation right. Google's contract also allows for termination 90 days in advance after December 2026.

This means that valuing the approximately $26 billion in annual computing power revenue as a guaranteed contract backlog is untenable: a lease that can be cancelled within 90 days and a long-term contract locked in until 2029 correspond to entirely different cash flow certainties . Any valuation model that treats it as a fixed backlog will be refuted by this fine print.

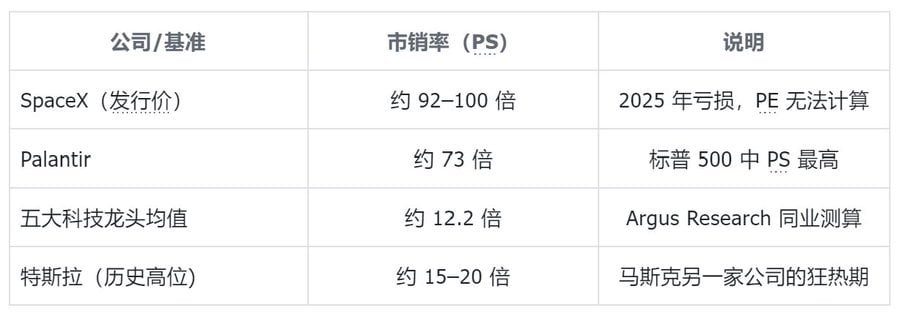

Price-to-sales ratio nearly 100: How outrageous is this compared to historical levels?

From the perspective of multiples:

First, the company is currently operating at a loss, so the price-to-earnings ratio (PE) method cannot be used to calculate it.

Secondly, if we use the price-to-sales ratio (PS) method commonly used by technology companies, the company's market capitalization of $1.75 trillion corresponds to approximately $18.7 billion in revenue in 2025, resulting in a price-to-sales ratio (PS) of approximately 92 to 100 times.

Price-to-sales ratio comparison (Source: Investing.com )

For reference, the average price-to-sales ratio (P/S ratio) of the five largest US tech stocks is about 12.2; Palantir, the stock with the highest P/S ratio in the S&P 500, is about 73. This means that SpaceX's P/S ratio upon listing was about 30% higher than the most expensive stock in the S&P 500.

Historical experience is also not on its side:

- According to data from Jay Ritter of the University of Florida, of the 14 IPOs with revenues exceeding $100 million and price-to-sales ratios above 40, 12 underperformed the market in the three years following their listing.

- Another analysis reviewed over a hundred popular tech stocks and found that only about eight stocks in history had a price-to-sales ratio that exceeded 100, and without exception, they all fell sharply after peaking, with an average drop of over 50% from high to low.

Therefore, from the perspective of valuation and pricing alone, no matter how you look at it, SpaceX's valuation is excessively high—this is beyond doubt.

What magnitude does doubling mean?

Let's take a reverse approach: If someone expects SpaceX's stock price to multiply several times over, they need to first understand what kind of scale that corresponds to.

Its current market capitalization has exceeded $2 trillion, ranking sixth in the United States.

- If its market capitalization doubles to approximately $4 trillion, it will approach or even surpass Nvidia, currently the world's most valuable company.

- If the stock price increases five or six times from the offering price, the corresponding market value will reach the level of 10 trillion US dollars, which is equivalent to the combined market value of several of the largest technology companies in the current US stock market.

Given that the company is still operating at a loss, its core profit comes solely from Starlink, and its computing power contracts can be cancelled within 90 days, the difficulty of delivering this scale of computing power in the foreseeable future is self-evident.

This is also the source of the saying uttered by many short sellers and institutions— while they were scrambling for quotas at $135, they were also writing in their models that: this price is inconsistent.

V. Short-term perspective: Timeline for index inclusion and passive buying

Clarifying the long-term valuation does not necessarily mean a short-term decline is imminent. On the contrary, due to changes in the index rules, SpaceX experienced support from forced buying by passive funds (ETFs) for a period after its listing.

Nasdaq did indeed change the rules "for him".

Historically, new stocks typically undergo a stabilization period of three months to a year before being eligible for inclusion in major indices. This window is designed to allow the market to complete price discovery and protect passive investors.

However, Nasdaq officially launched the "Fast Entry" mechanism in March 2026, which took effect on May 1: newly listed companies whose market capitalization ranks in the top 40 of the index can be included in Nasdaq-100 within just 15 trading days after their IPO, exempting them from the original minimum three-month stabilization period and restrictions - this was even considered to be a rule change specifically for SpaceX.

At the same time, the Nasdaq-100 also waives the 10% minimum free float requirement—which corresponds to SpaceX's extremely low free float of only about 4%, otherwise it wouldn't qualify at all.

Other index providers have differing opinions:

- FTSE Russell has shortened the post-IPO waiting window to just five trading days—SpaceX has met the requirements.

- Morningstar's CRSP index introduces a liquidity screening for mega-IPOs—SpaceX can be included in advance.

- However, after a formal consultation on June 4, 2026, S&P Dow Jones Indices decided to maintain its 12-month stabilization period and GAAP earnings threshold unchanged—meaning that SpaceX's inclusion in the S&P 500 will not occur until at least mid-2027.

SpaceX's major stock index inclusion timeline (Source: SpotGamma, Morningstar, CNBC, ETF Stream, June 2026)

The core value of index inclusion lies in forcing passive buying.

This point deserves special mention: the essence of index inclusion is not honor, but rather triggering "passive buying".

Once SpaceX is included in an index, all passive funds tracking that index—regardless of the fund managers' views on its valuation—must unconditionally buy it by weight. This buying is rule-driven, does not rely on active judgment, and is therefore highly predictable and mandatory.

Inclusion in the Nasdaq-100 will directly trigger forced buying of the following major ETFs:

- QQQ (Invesco QQQ Trust, with a size of approximately $495.7 billion)

- QQQM (Invesco Nasdaq-100 ETF, with a size of approximately $98.5 billion)

SpotGamma analysts estimate that Nasdaq tracking funds alone would need to be forced to buy approximately $7 billion worth of SpaceX stock on the day of inclusion.

If we include the funds tracking QQQ, FTSE Russell, and Russell 1000, the recent mechanical buying volume is estimated to be between $22 billion and $27 billion. This figure already includes passive funds from earlier inclusions such as CRSP, which will flow in in batches within weeks of listing, providing temporary support for the stock price. If the S&P 500 inclusion is completed in 2027, an additional $8 billion to $12 billion in passive buying is expected.

This mandatory allocation means that global investors holding QQQ ETFs will automatically hold SpaceX shares without having to make any active decisions.

Shareholding structure: Most shares are locked up, few are in circulation, limiting short-term selling pressure.

Passive buying describes the certainty of demand; from the supply side, the current shareholding structure is also tight, and the available selling power in the short term is quite limited.

SpaceX's Class A shares represent only about 4% of its equity, while Musk holds approximately 42% of the equity and 85% of the voting rights. Given such a small float, even small-scale passive buying could have a greater-than-expected impact on the stock price.

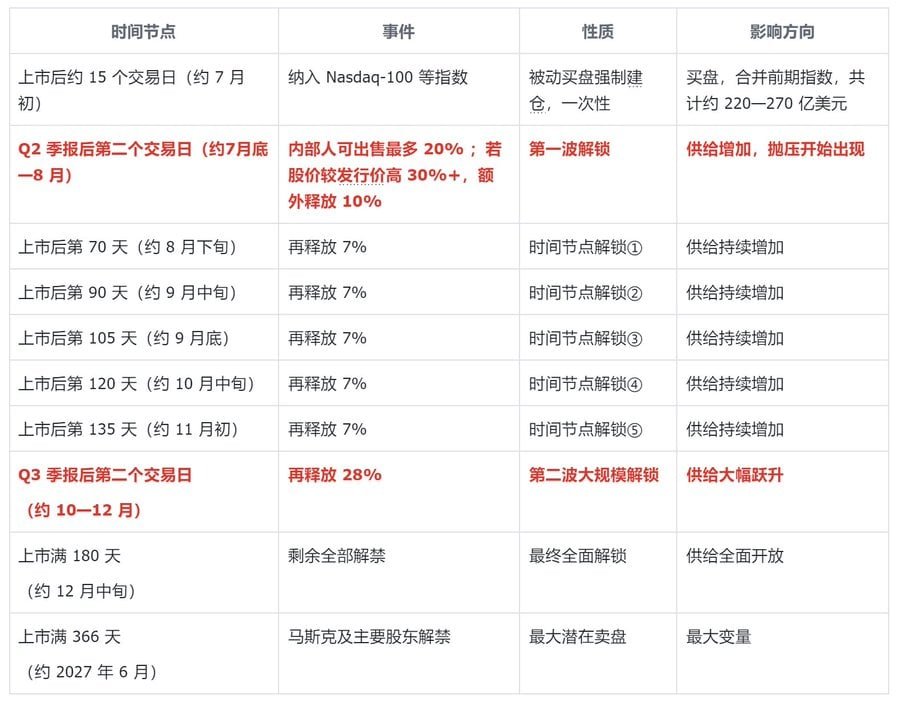

The lock-up period is more stringent than in a regular IPO because SpaceX uses a tiered unlocking mechanism:

- Two days after the Q2 earnings report is released, insiders can sell 20% of their shares; if the share price is more than 30% higher than the offering price at this time, an additional 10% can be unlocked.

- After that, 7% will be released in five separate periods every 15 days (on days 70, 90, 105, 120, and 135 after listing).

- Another 28% will be unlocked after the Q3 financial report is released, and the remaining portion will be fully unlocked 180 days after listing (approximately mid-December 2026).

- Musk and some major shareholders were individually restricted, with a lock-up period of up to 366 days.

This structure means that large-scale sell-offs will not occur all at once in the early stages of listing, but will be released in batches and over a period of time.

During the lock-up period leading up to the Q2 earnings report release at the end of July, only the approximately 4% of shares issued during the IPO were freely tradable on the market. All insiders who held shares before that date—including early employees and venture capitalists—had to wait until the lock-up period ended before they could sell.

Looking at the supply and demand sides together, the logic becomes clearer: in the weeks following the IPO, the demand driven by passive buying is governed by rules and has a predetermined timeframe; while the supply side is constrained by the lock-up period, making large-scale shipments virtually impossible in the short term. These two factors combined create a bullish sentiment structure for SpaceX in its initial listing phase. The crucial point to watch is the second half of 2026, when the lock-up period begins to expire in batches—at which time the supply side will gradually unfreeze, and the market structure will undergo a shift.

When will selling pressure appear?

To understand the pace of selling pressure, we must first understand the true structure of SpaceX's lock-up period. The first wave of unlocking began at the end of July and with the Q2 earnings report in August. Subsequently, new shares became available for sale every few weeks, and the pressure was gradually released throughout the second half of the year, rather than a sudden, concentrated impact. The lock-up period remained 180 days, but insiders (employees and early investors) could sell in batches at multiple points within these 180 days. In other words, the selling pressure began as early as the Q2 earnings report at the end of July and continued throughout the second half of the year, rather than concentrated in December.

Key timelines for SpaceX after its IPO (Source: SpaceX Form S-1; CNBC; Darrow Wealth Management)

In short, the above table shows that buying pressure is one-off, while selling pressure is continuous.

The $22-27 billion in passive buying resulting from index inclusion is a single event with a fixed timeframe and measurable scale, and it ends once it is completed—index funds will stop buying once they have bought the positions they were supposed to.

In contrast, the unlocking process began after the Q2 quarterly report, with a new release window appearing approximately every two weeks, continuing throughout the second half of the year until full opening in December. Each node represents a new release of supply, and potential sellers only need to sell at their respective window periods, thus the pressure is gradual and continuous.

The institutions on the shareholder list include Andreessen Horowitz, Founders Fund, Sequoia, and Alphabet. Among them, Founders Fund and Valor Equity Partners have unrealized gains of over $60 billion each. Any exit by any of these institutions, even if it's just a small percentage, would amount to a considerable sum.

In summary, the trading structure in the second half of 2026 is essentially a standoff between buying and selling pressure based on time differences: passive buying is concentrated in the first three weeks, while the release of supply starts from the seventh or eighth week and continues until the end of the year.

- The window with the lowest overlap between the two (i.e. before and after the inclusion of the Nasdaq) is likely the stage with the most abundant chip structure.

- Once we enter the Q2 earnings season, the market will have to simultaneously digest the exhausted passive buying and the continuous influx of unlocked selling pressure. This is the real pressure zone that needs to be watched closely.

VI. Conclusion: A great company is not necessarily at the right price right now.

No one can deny that SpaceX is a great company.

It monopolized global commercial launches, turned Starlink into a truly profitable satellite broadband network, and is now attempting to bring data centers into orbit—a level of integration that almost no other company on Earth can replicate. The phrase "extending the light of consciousness to the stars," written on the first page of its prospectus, truly reflects its engineering achievements.

But a great investment isn't just about buying a great company. Warren Buffett wrote a frequently quoted phrase in his 1989 letter to Berkshire Hathaway shareholders: "Buy a great company at a reasonable price." The key phrase is "reasonable price," not "any price." Even the best company isn't a correct investment if you buy it at the wrong price.

Returning to SpaceX, a price-to-sales ratio of nearly 100, still-expanding overall losses, profits supported solely by Starlink, and those two computing power contracts that could be canceled within 90 days all indicate that the current valuation already includes very optimistic long-term assumptions.

- In the short term, thanks to the extremely low free float of approximately 4%, the 180-day lock-up period, and the forced inflow of passive buying from indices such as Nasdaq-100, the stock price may be supported or even continue to rise.

- However, this support system, consisting of scarce shares and one-off buying, is not very robust. When the lock-up period expires and the passive buying is exhausted, the valuation will likely experience a correction towards the fundamentals.

Therefore, from an investment perspective rather than an emotional one, a more prudent approach is to acknowledge its potential while waiting for a more reasonable price. Of course, from a speculative standpoint, betting on the massive passive buying expected after its inclusion in index funds in two weeks is indeed plausible. However, one concern remains: is it possible that this valuation expectation was already factored into the $15 opening jump premium?

Since most people in the market can judge that the current valuation is too high and a value correction will eventually occur, there is no need to rush in when the narrative is hottest and the chips are tightest. Instead, wait for the pullback to be the real entry opportunity.

SpaceX is a great company, that's for sure; but even great companies need to be bought at the right price to make a good investment.