Author: Charlie Perkin , Zach Pandls, Grayscale

Compiled by: Yuliya, PANews

Editor's Note: With the cryptocurrency market's continued decline since the beginning of the year, investors face a crucial question: which digital assets are worth investing in at current prices? For digital commodities like Bitcoin, this assessment isn't easy, but many other crypto assets are similar to financial equities and can be valued through cash flow. This report uses Aave, a leading on-chain decentralized lending platform, as an example to analyze how to accurately calculate the fair value of crypto assets through protocol revenue, token value capture mechanisms, and the industry price-to-earnings ratio (P/E) multiplier. The following is the complete translated content:

Key points

- The crypto market has been in a continuous slump since the beginning of the year : How can investors determine which digital assets are worth investing in at current prices? This may be quite challenging for digital commodities like Bitcoin, but many other crypto assets are more like financial debt and can be valued entirely through cash flow.

- This report focuses on Aave : As a leading blockchain-based lending platform, Aave is an established project with transparent financial data, but it has recently experienced a bumpy period, including the departure of key contributors and deposit outflows.

- Based on traditional discounted cash flow (DCF) analysis , Grayscale Research believes that the AAVE token offers investment value at current levels. Despite recent headwinds, we expect the protocol to still generate approximately $60 million in net revenue in 2026. Using a typical P/E ratio of 20 to 25 times for traditional fintech companies, its fair market capitalization should be between $1.2 billion and $1.5 billion, corresponding to a token price of approximately $80 to $100 (compared to the current market price of approximately $75).

- In the baseline scenario : if regulatory clarification accelerates the adoption of tokenized assets, we believe the fair value of the AAVE token could rise to approximately $175 within a year.

- Aave demonstrates a successful example : it proves that protocol-level success can be explicitly tied to token value capture, thereby supporting the application of traditional valuation frameworks including DCF analysis, price multipliers, and comparable company analysis.

- Token value capture mechanisms are crucial in DeFi protocol economics : they enable projects to translate top-level business adoption into token price increases while preserving a decentralized governance architecture.

- Aave is not a traditional company : it is a DAO. Currently, DAOs still face significant regulatory uncertainty. If the Clarity Act passes and becomes law in 2026, the AAVE token may be classified as a "network asset" under that framework.

*Note: DCF is one of the most widely used pricing models in the fields of corporate finance and investment. It is equivalent to discounting all the cash flows that a company can earn in each of its future years to today and then summing them up.

Digital assets have already established themselves in mainstream technology and finance, but overall, the market is still very young. A simple comparison reveals this: the top 30 cryptocurrencies by market capitalization have an average age of only about 8 years; while traditional, established companies in the Dow Jones Industrial Average have an average lifespan of over 100 years. Because it's a "newborn," everyone is constantly debating how to classify, regulate, and value crypto assets. As the market matures, clarifying these issues will not only lead to more reasonable price points but also attract more capital from outside the crypto sphere.

Grayscale Research believes that as the market evolves, we need a more nuanced approach to digital asset valuation, including incorporating frameworks derived from traditional financial analysis. Before investing in any coin, the first step is to understand its economic underpinnings: What is it used for? How do regulators view it? How intense is the competition? Most importantly, how will the project distribute profits to token holders? Understanding these aspects is crucial to determining how to evaluate it.

For crypto assets, it's not enough to just look at whether a project has users; you also need to examine its tokenomics and governance structure to see if "project profits" translate into "price appreciation." Next, we'll use the DeFi lending sector and the Aave protocol as examples to analyze how to value protocols using cash flow and fundamentals.

Classifying crypto assets

Just like common sense in traditional financial markets over the past few centuries, the driving logics of stocks, gold, foreign exchange, and bonds are completely different, and you cannot use the same method to value them.

Similarly, not all crypto assets should be valued using the same framework. While the early crypto market often lumped all tokens together, investors today are increasingly inclined to differentiate between assets with distinct economic functions, ownership characteristics, and value drivers. Asset classification requires identifying the underlying factors that drive token value growth, such as currency premiums, liquidity premiums, utility premiums, governance premiums, and cash flow-related premiums.

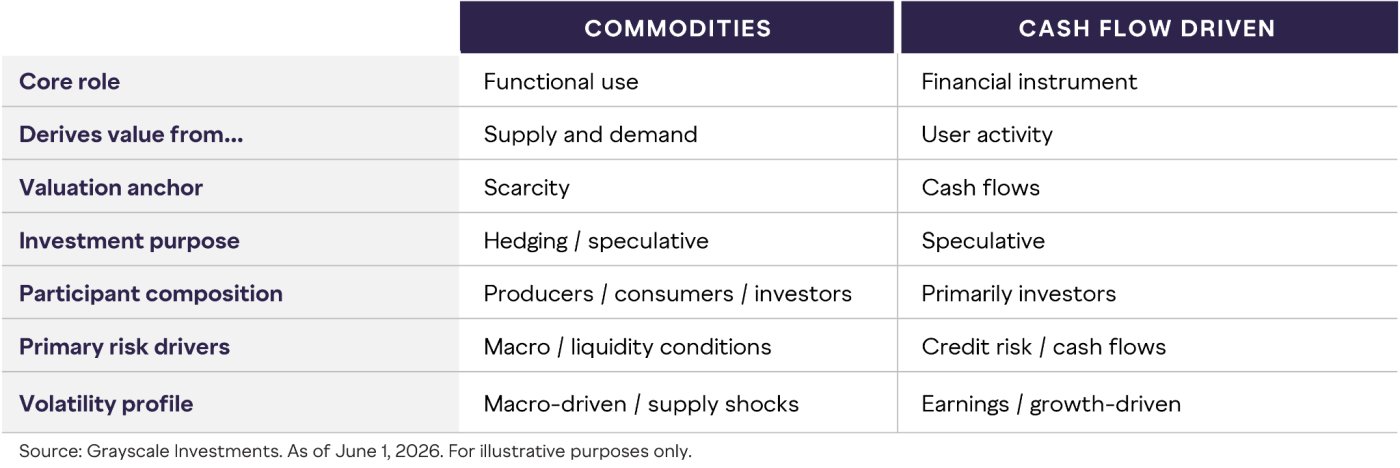

Chart 1: Structural Differences Between Commodities and Financial Claims

Distinguishing between "commodity-like assets" and "cash flow assets" is an important starting point in the classification process.

- Commodity-like assets (such as Bitcoin): These assets don't pay you a salary or dividends. Their value is entirely supported by "scarcity" and the "consensus" that people use them as a medium of exchange, collateral, or a store of value.

- Cash flow assets (such as DeFi tokens): These assets are tightly tied to the underlying business activities of the project. Their value depends on how much transaction fees the project collects, how much operating expenses it incurs, how much money it holds in its treasury, and most importantly—what mechanism the project team uses to return this money to token holders.

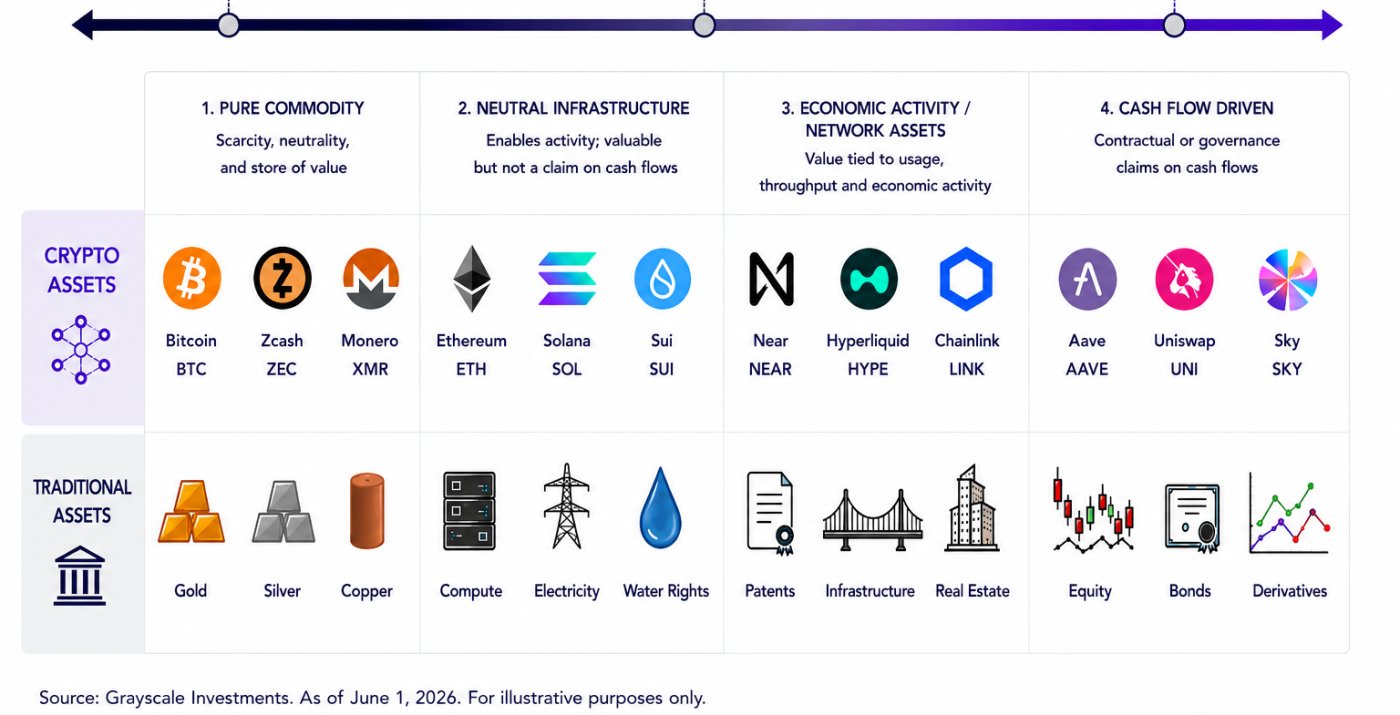

Chart 2: Asset Spectrum from Pure Commodities to Financial Claims

In reality, many cryptocurrencies fall somewhere in between. The valuation methods applicable to a reserve or settlement asset (such as BTC) are fundamentally different from those for a protocol token (such as AAVE) with continuous revenue, treasury assets, governance rights, and a clear value capture mechanism. Many tokens even possess multiple characteristics simultaneously, requiring investors to assess which economic drivers are most critical at specific stages of protocol development.

Therefore, when choosing a valuation model, we need to look at the "economic essence" of the asset, rather than just whether it is a coin issued on-chain. As projects mature and the market changes, their attributes will also change.

Within this asset class, DeFi protocols are the most typical example of "cash flow driven" systems. Here, their economics are directly linked to token value, and they can be valued using a traditional valuation method.

DeFi: The Real Money-Making Sector

If there's one truly viable and profitable application of blockchain technology, DeFi is definitely one. DeFi protocols facilitate numerous businesses, including trading, lending, collateral management, liquidity provision, and risk transfer. These activities generate clearly visible income from real users, creating a financial profile that is increasingly comparable to traditional financial companies, networks, and software platforms.

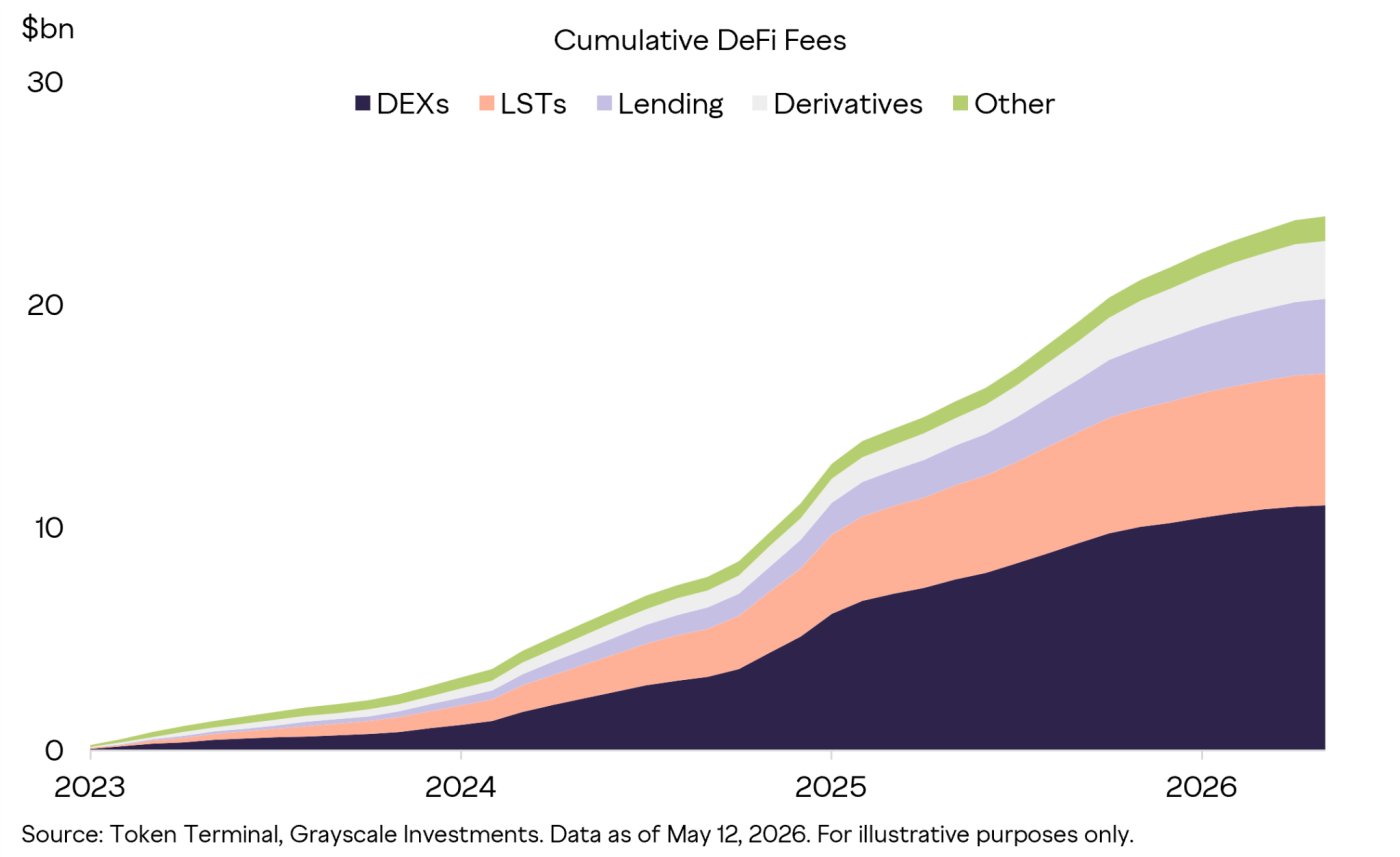

Since the beginning of 2023, DeFi protocols have generated nearly $25 billion in fee revenue, primarily driven by DEXs, liquidity staking, lending, and derivatives. This demonstrates that DeFi has moved beyond purely speculative experimentation and begun to support sustained financial activity across multiple verticals, although speculative trading remains a significant driver. Many leading DeFi protocols also exhibit highly attractive operating characteristics, including high gross margins, extremely low capital expenditure requirements, and scalable, software-driven business models.

Chart 3: Cumulative Fees Generated by DeFi Protocols and Strong Revenue Growth (Unit: Billion USD)

(Data source: Grayscale Research, based on publicly available on-chain data statistics)

As projects mature and their financial data stabilizes, we can analyze them just like traditional assets. Take the DeFi lending sector, for example; it's a prime example of a stable business model that generates revenue steadily. We can consider the total fees paid by users as "total revenue," and the portion ultimately kept by the lending protocol as "net income." By understanding these two calculations, you can grasp the earning power of different projects and how that money ultimately flows to investors.

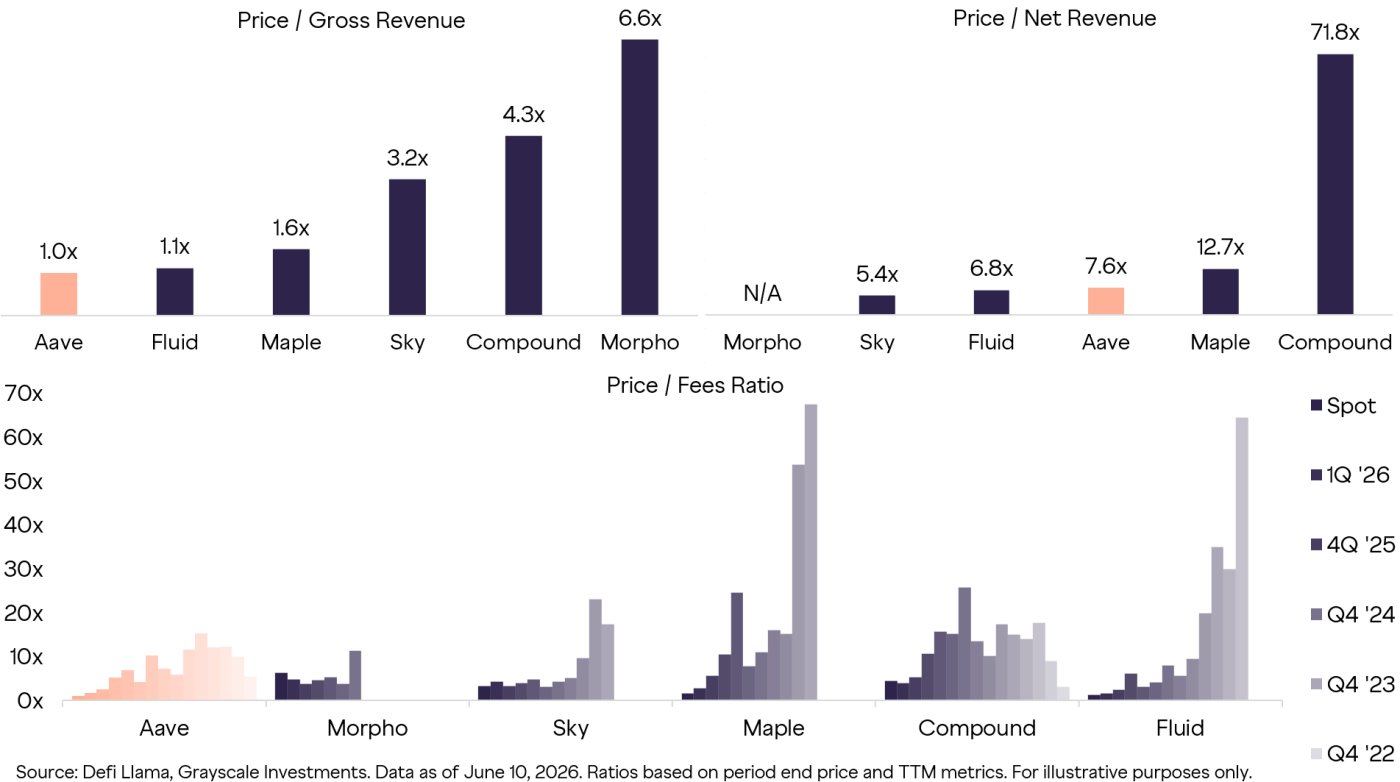

We can even compare these lending protocols using the price-to-earnings ratio (P/E), much like we would use the stock market. Currently, valuation multiples across the entire lending sector have been significantly compressed, indicating a marked maturation of the market. Meanwhile, each protocol has demonstrated its own innovation in its business model: Morpho's vault is growing exponentially; Sky (formerly MakerDAO)'s on-chain collateralized stablecoin continues to expand its product-market fit; and Maple, focusing on institutional clients, has achieved high returns. With the increasing adoption of stablecoins and the tokenization of RWA, these lending applications are likely to soon return to the spotlight.

Chart 4: Valuation Multiplier Comparison of Major Protocols in the DeFi Lending Sector

Among its peers, Aave is an excellent subject of study. While continuously upgrading its business, it has increasingly and clearly focused on "delivering value to AAVE token holders." Despite facing macroeconomic and ecosystem risks, Aave has maintained its dominant position in the industry by navigating multiple crypto cycles thanks to its clear tokenomics.

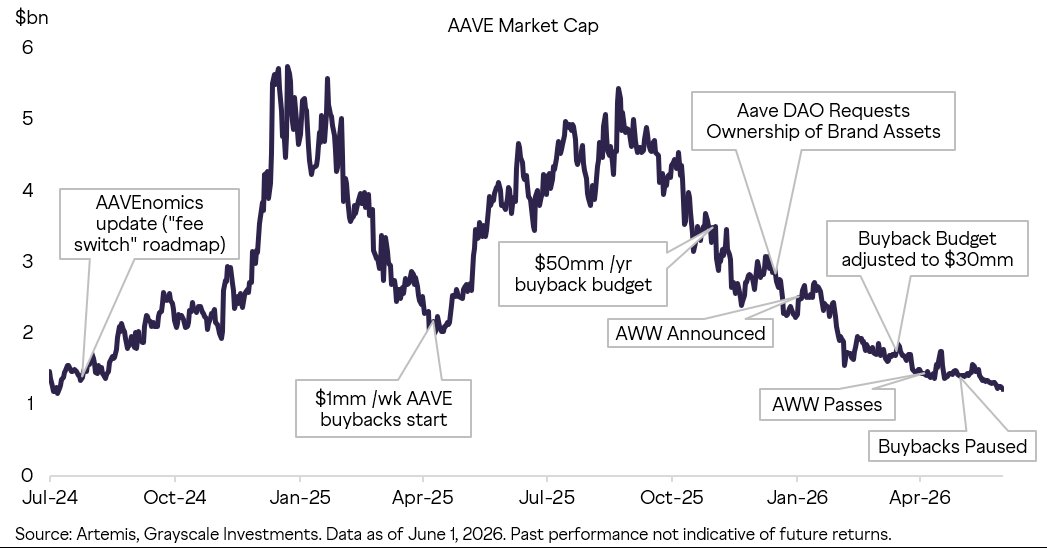

Of course, it is not immune to all risks. For example, the Kelp DAO rsETH security vulnerability in April 2026, while not a direct attack on Aave, triggered a chain of market panic, causing a temporary drop in protocol activity. Although funds were subsequently confirmed safe and the problem was quickly fixed, the lasting impact remains. Currently, token buybacks are suspended pending governance review, and the total value locked (TVL) has also shrunk significantly. However, Aave's efficient decision-making and high level of transparency during this ordeal have actually strengthened, rather than weakened, its institutional credibility.

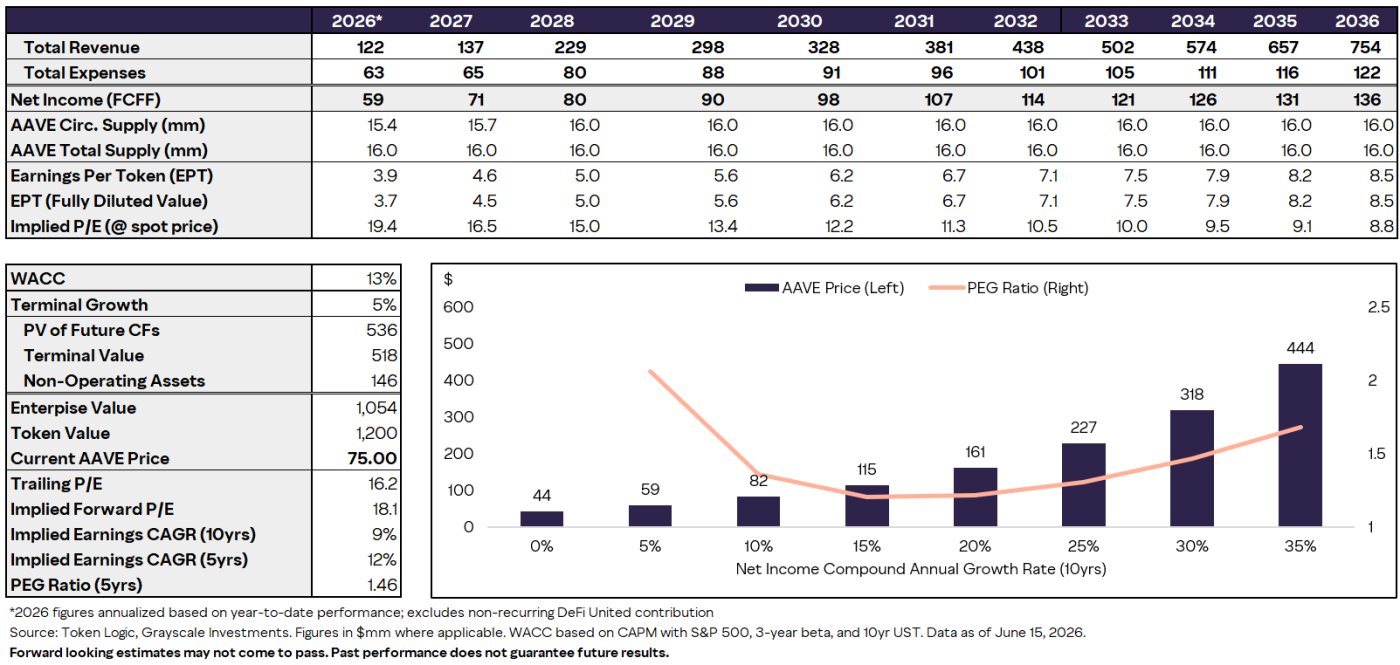

Let's do the math on Aave: How much is it really worth?

After careful calculations by Grayscale Research (based on discounted cash flow models and comparisons with peer price-to-earnings ratios), we believe that AAVE's current fair value should be between $80 and $100. Aave not only holds an unshakeable position in the DeFi community, but also boasts stable profits and a solid financial foundation. In the future, provided the macro environment (such as the adoption of stablecoins and regulatory policies) is favorable, it will definitely have significant upside potential in a bull market.

Aave is a decentralized lending protocol that allows users to deposit crypto assets to earn yield and borrowers to use those assets as collateral for loans. Instead of relying on traditional financial intermediaries, Aave uses smart contracts to aggregate liquidity, set lending terms, manage collateral, and automatically liquidate positions below the liquidation line when necessary. In this model, depositors provide the funding base (such as USDC and ETH), borrowers create credit demand, and the protocol earns revenue from interest rate spreads, fees, and related services. Despite some technical differences, Aave is often aptly described as an "on-chain permissionless bank." This makes it the clearest counterpart to traditional financial companies in DeFi: it facilitates credit creation, generates continuous protocol revenue, and increasingly returns a portion of its economic value to AAVE token holders through governance-approved mechanisms.

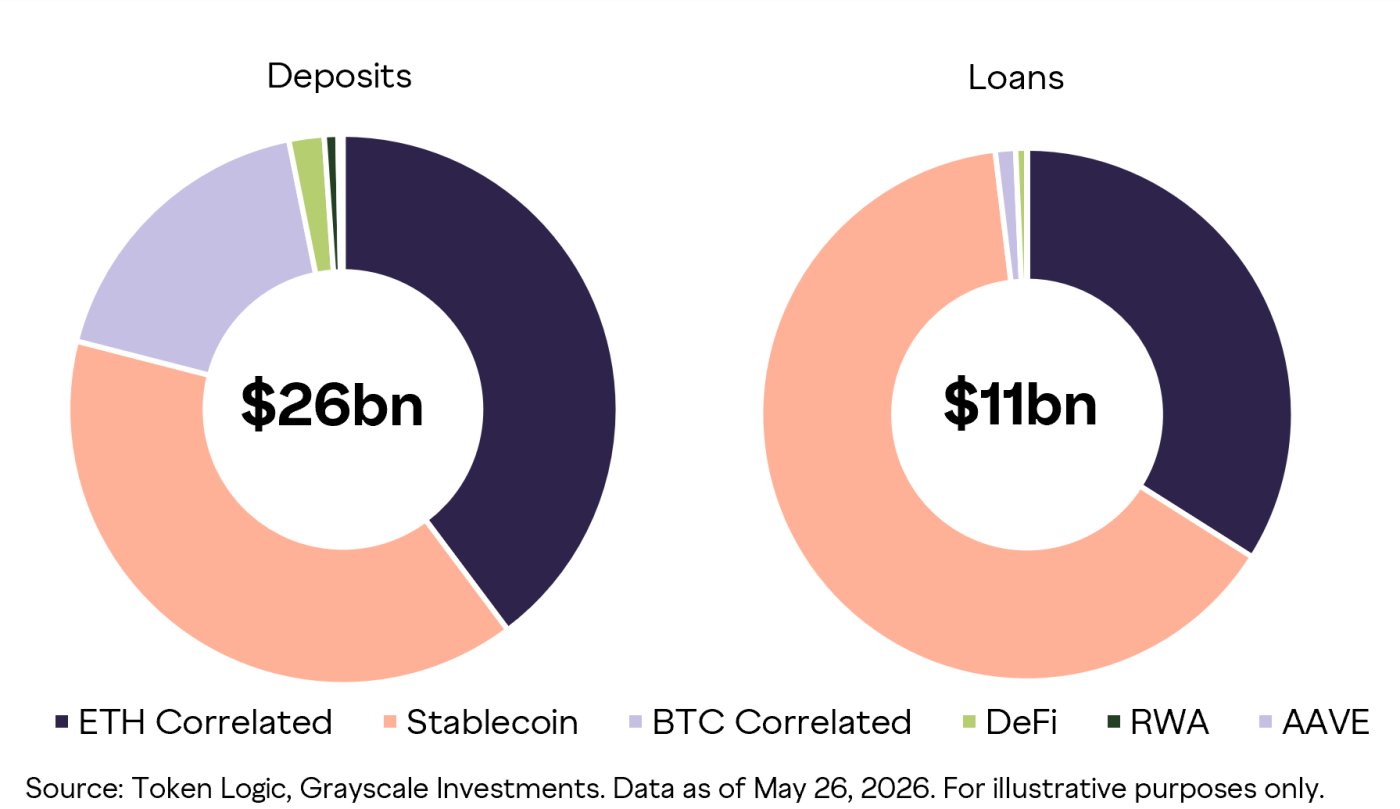

Chart 5: Aave's massive loan ledger drives on-chain lending business

The entire DeFi ecosystem boasts over $59 billion in total deposits and $25 billion in open loans, making on-chain credit creation one of its most fundamental cornerstones. Aave is the undisputed market leader, holding a dominant share of total deposits, open loans, and user activity. On USDC positions, Aave currently pays depositors 3.29% interest and charges borrowers 4.04%, offering a highly competitive alternative to traditional off-chain rates. With a stable user base of nearly 200,000 monthly active users, Aave's central role in DeFi gives it a significant competitive advantage.

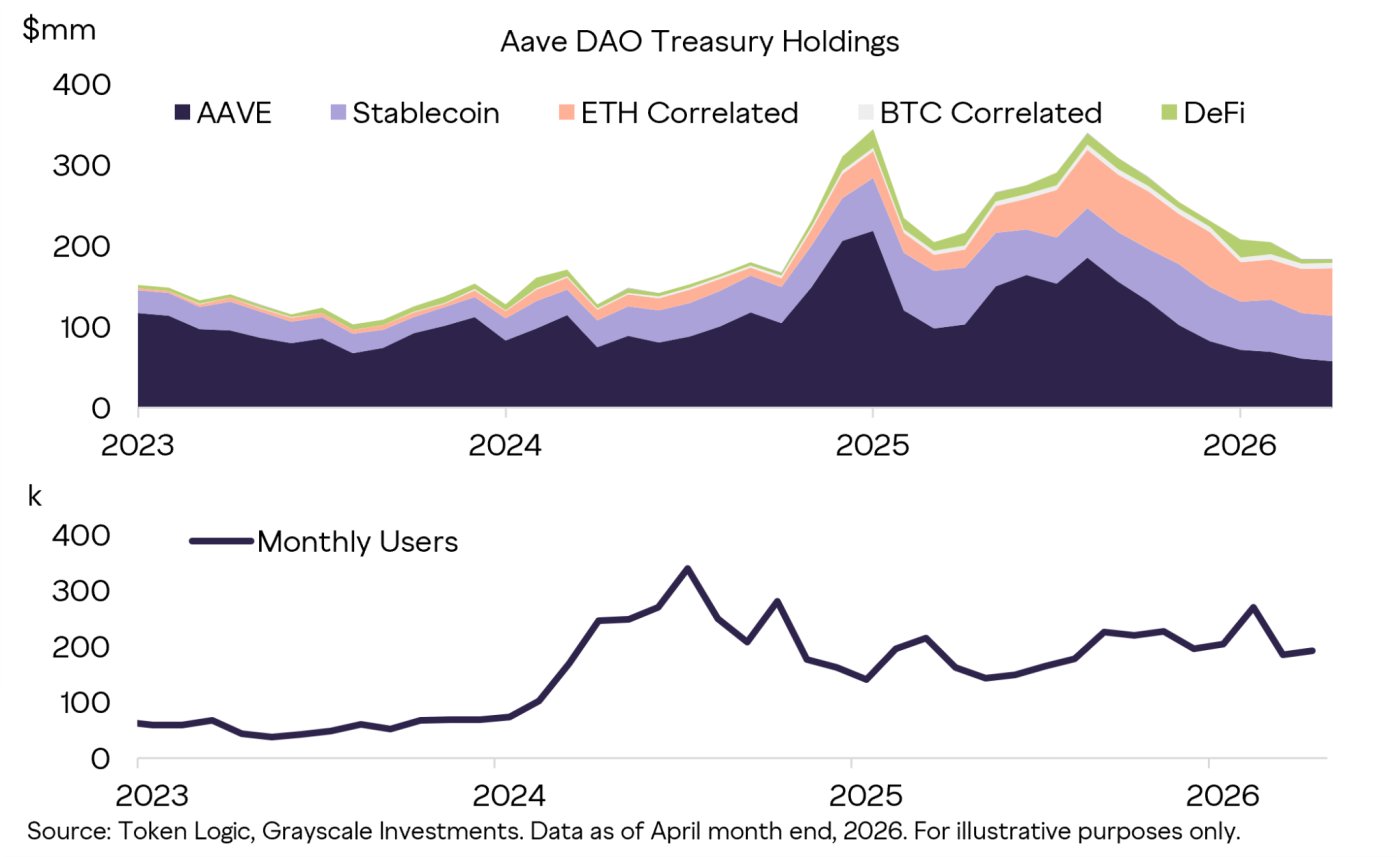

Chart 6: Aave's Continuous Usage and Diversified Asset Treasury

What sets Aave's DAO apart from its competitors is its large and diversified balance sheet, governed by token holders, which provides solid financial backing for its core growth initiatives. The Aave DAO serves as the vehicle for governance and operational coordination across the various functions of the protocol. Thanks to the appreciation of the AAVE token and the accumulation of protocol revenue, the DAO's treasury has historically exceeded $360 million.

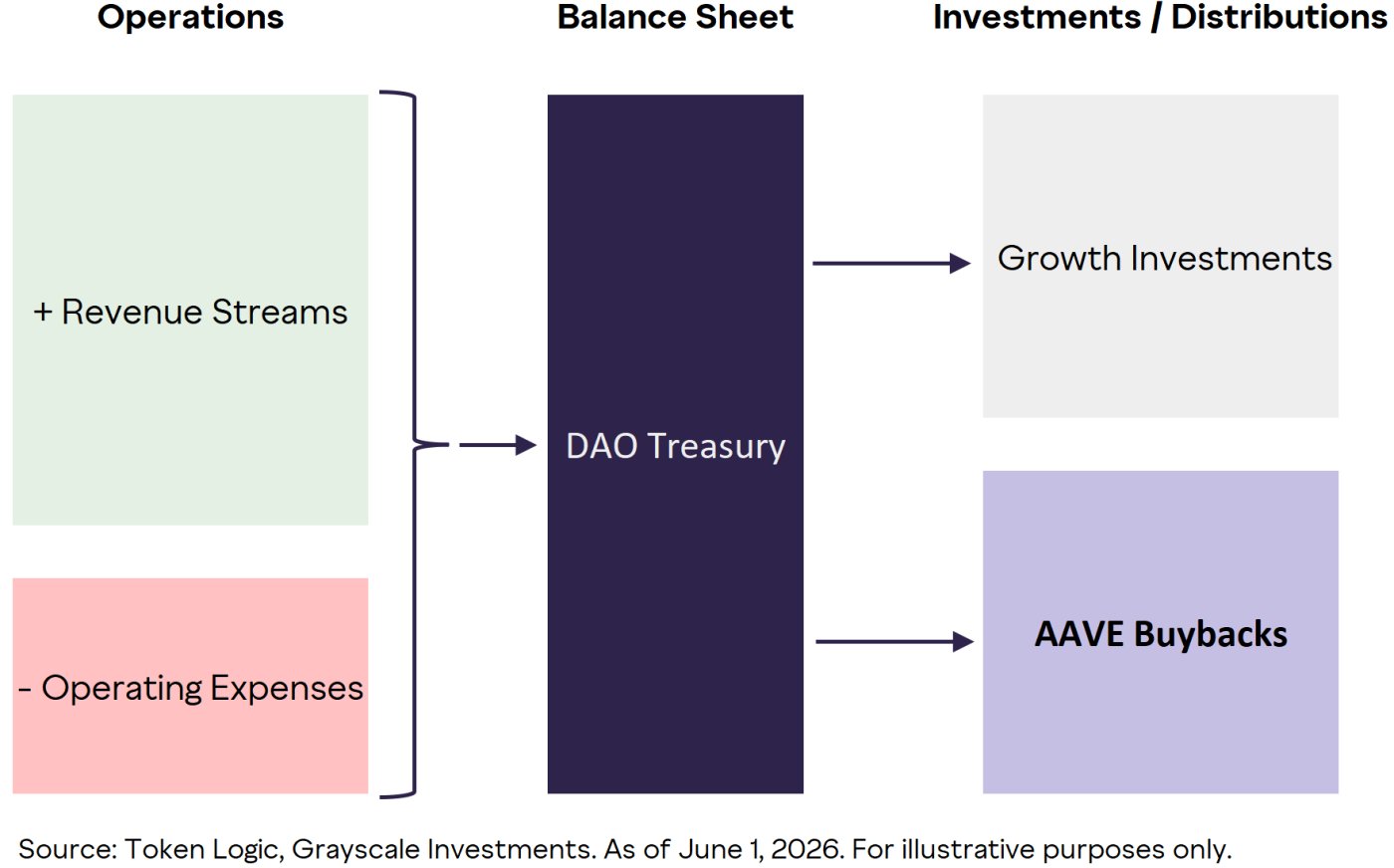

Aave's core revenue drivers include lending activities, treasury revenue, and income from its native stablecoin, GHO. All of these cash flows are channeled into the DAO treasury, which then manages capital allocation. Token holders then vote on how to allocate these resources for capital expenditures, AAVE token buybacks, or to retain them in the DAO treasury for future projects.

Chart 7: The path of Aave's profits flowing from the protocol to DAO capital allocation

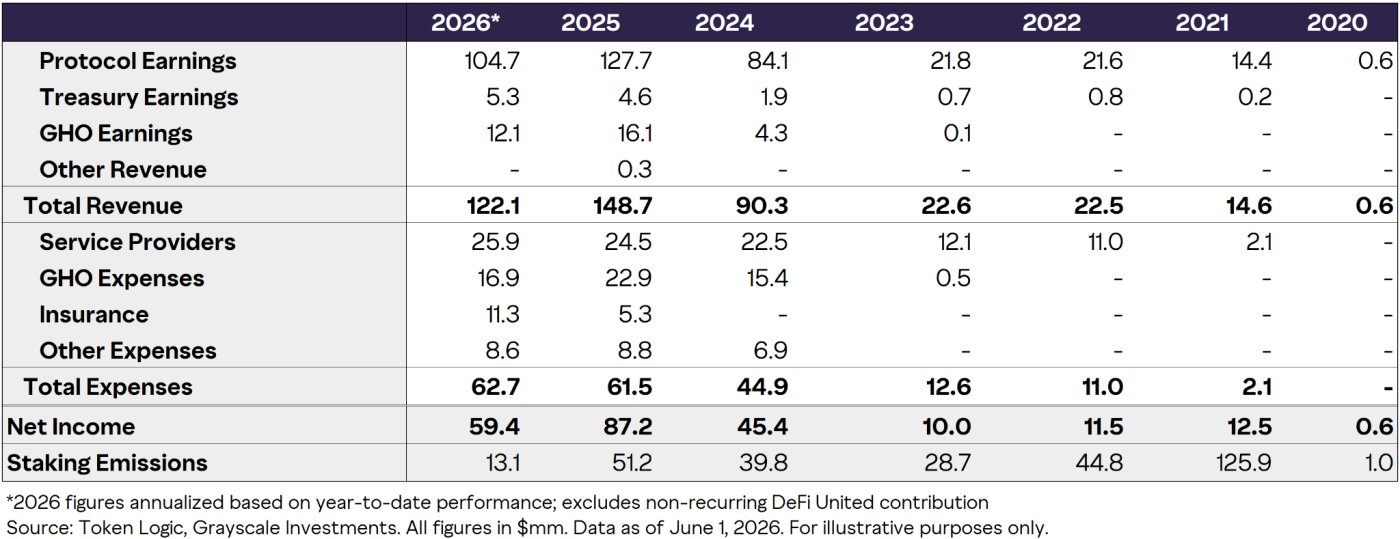

As shown below, Aave's revenue grew more than 6.6 times from 2023 to 2025.

- Agreement income: Historically, it has accounted for approximately 85% of total income, mainly derived from the interest rate spread between lending and borrowing rates;

- Treasury revenue: Interest generated from held assets;

- GHO Revenue: GHO is an overcollateralized stablecoin issued by Aave, with a current circulating market capitalization of $283 million. Its fees account for approximately 10% of total revenue.

- Other revenue streams include liquidation fees, flash loan fees, and partner revenue sharing.

Chart 8: Aave Simplified Profit and Loss Statement (Unit: Million USD)

During the same period, the agreement's spending increased approximately 4.9 times. In other words, its earning speed far outpaced its spending speed.

- Service providers: refers to the various teams that work through contracts to support and develop the Aave protocol, including developers, risk curators, governance coordinators, and other core contributors.

- GHO expenditures primarily include liquidity-making subsidies and user incentives provided to support the growth of the stablecoin.

- Insurance outflow: Used to support Aave's on-chain risk management system to provide advance payment in the event of potential bad debts.

- Other costs: including projects related to ecological partnerships, representation, and security audits.

Currently, Aave's net profit margin is around 50%. Based on the current spot price of around $75, the market's assumption that its earnings will only grow at 9% annually over the next ten years is incredibly conservative. Keep in mind that established companies in the S&P 500 often project growth rates of 10% or even 20%. If we assume Aave can maintain 25% annual growth like mainstream fintech companies, its price should be $227; if the growth rate reaches 35%, the price could reach $444.

Chart 9: Implied AAVE Cash Flow and Growth Expectations Based on a Spot Price of $75

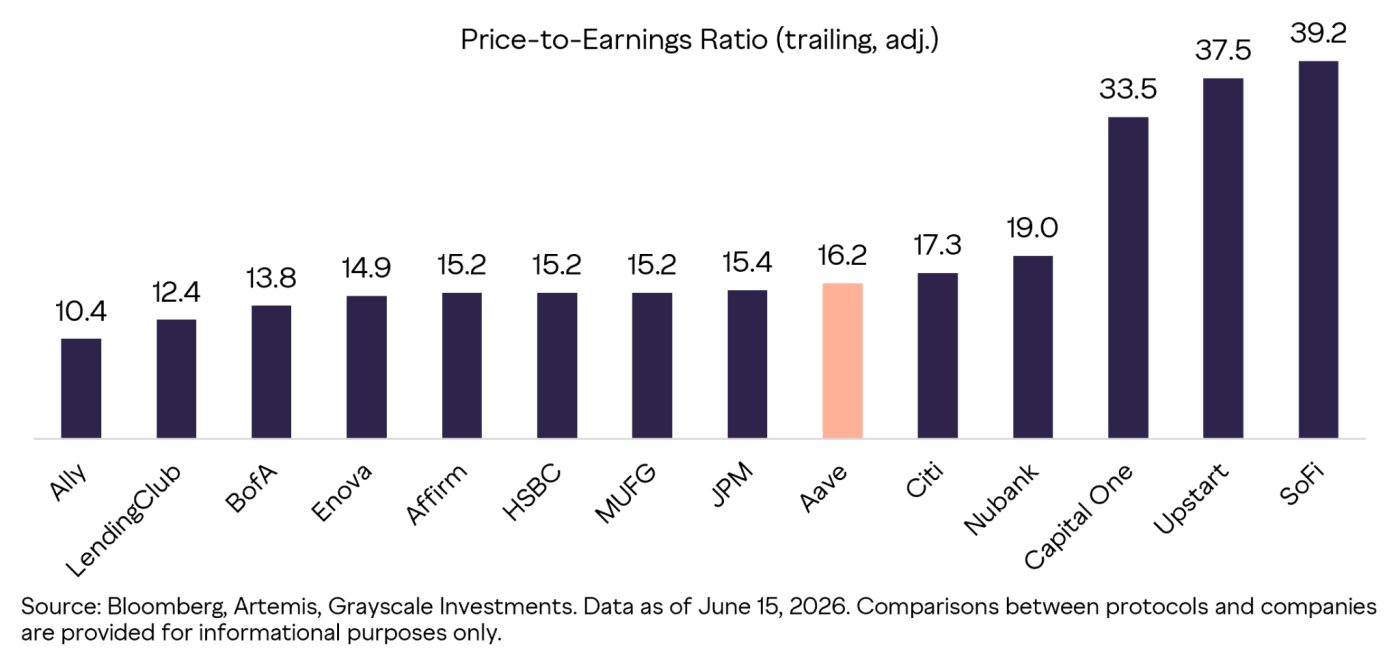

At the current price of $75, Aave's historical price-to-earnings ratio (P/E ratio) is approximately 16.2, and its forward P/E ratio is approximately 18.1. In comparison, the average P/E ratio of the S&P 500 is around 24. Aave, a highly profitable and rapidly growing on-chain bank, is valued precisely between traditional large banks (around 14 times earnings) and internet finance companies (around 21 times earnings). This current valuation "discount" is largely due to external investors' concerns about regulatory hurdles. Once compliance is achieved, this discount will eventually be closed.

Chart 10: Horizontal Comparison of Key Metrics Between Aave and Traditional Financial/Fintech Giants

Aave's revenue is increasingly reliant on stablecoins rather than volatile crypto assets, making its core business extremely robust. With the growing popularity of stablecoins and the significant structural benefits of RWA tokenization, Aave is fully capable of growing its loan volume independently of market cycles. Furthermore, the following product initiatives have been the most important catalysts driving the recent appreciation of the AAVE token:

- The full rollout of GHO stablecoin : GHO is Aave's native overcollateralized stablecoin, minted directly against the protocol's collateral. By capturing the entire lending spread internally, rather than distributing it to depositors, GHO represents an important and continuously growing revenue stream for the protocol.

- Horizon (US Treasuries and RWA Institutional Market) : Horizon is a dedicated institutional market that allows compliant participants to access DeFi liquidity using tokenized RWAs (such as tokenized US Treasuries) as collateral. By connecting traditional capital markets with the Aave protocol, Horizon represents a significant potential source of lending growth.

- Umbrella (Upgraded Security Module) : Umbrella is Aave's upgraded security module, providing a more automated and capital-efficient mechanism for covering protocol deficits. By reducing reliance on AAVE token inflation releases while enhancing depositor protection, Umbrella strengthens the protocol's resilience and improves long-term token economics.

- V4 (Next Generation Architecture Upgrade) : V4 is Aave's next-generation protocol architecture, built around a unified "hub-and-spoke" liquidity model that separates shared liquidity from market-specific risk logic. This design improves capital efficiency, reduces liquidity fragmentation, and enables Aave to launch new lending markets, including RWA and institutional products, without requiring each market to independently drive liquidity.

- Aave Native App : The Aave App is a consumer-friendly interface designed to simplify the lending process for traditional retail users. By eliminating the technical friction typically associated with DeFi, the App aims to significantly expand Aave's potential user base beyond its existing crypto-native audience.

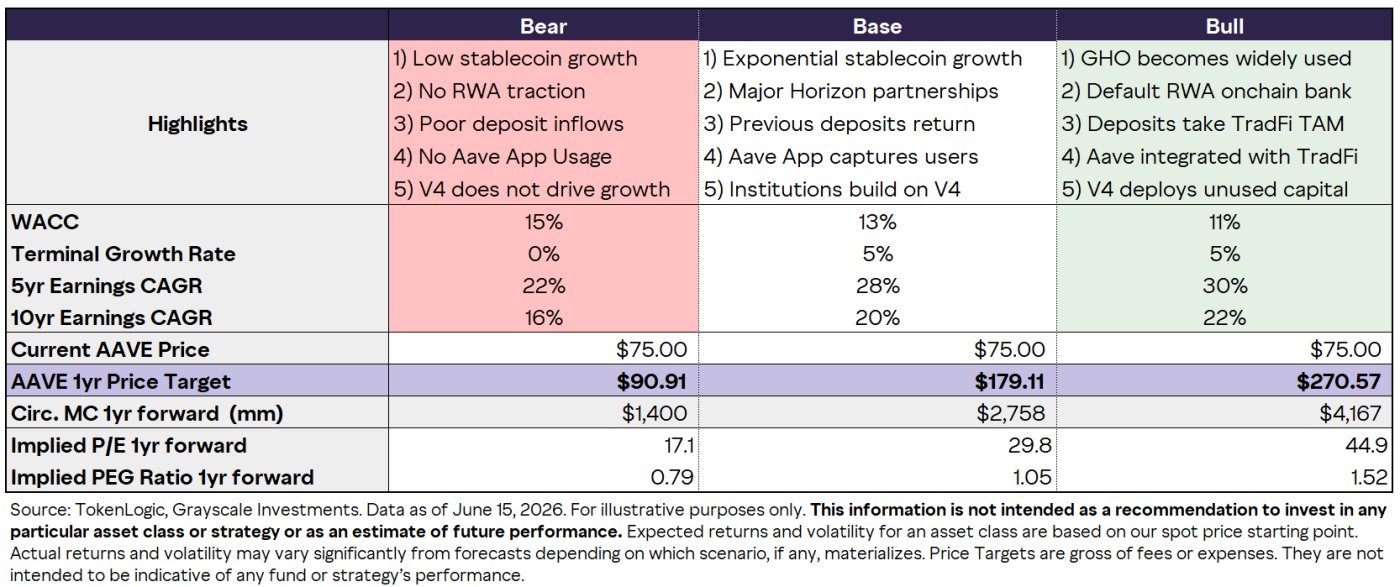

Looking ahead to the next year, we have made three scenario predictions for the Aave protocol and AAVE token price. The core assumptions mainly depend on the adoption of stablecoins, the progress of RWA tokenization, and the participation of traditional institutions.

Chart 11: One-Year Bear/Benchmark/Bull Market Scenario Calculations for the Aave Protocol and AAVE Token Price

These scenarios provide target prices for the next year. The target price range is wide, mainly due to the significant uncertainty surrounding the macroeconomic environment of stablecoin growth and institutional adoption of DeFi. However, thanks to its dominant position in the DeFi ecosystem, diversified revenue streams, and substantial national reserves, Aave possesses exceptional resilience. This means that at the current price, regardless of the scenario, its risk-reward ratio is very attractive.

Aave's recent evolution in its governance model has further strengthened the link between the protocol's economic benefits and the value captured by AAVE token holders. Previously, Aave's revenue streams were primarily used to support a broad ecosystem of needs (including payment service providers, providing various incentives, covering security costs, and supporting growth initiatives), with value capture for token holders being relatively indirect.

Recent governance proposals increasingly favor the DAO in terms of these economic benefits. Specific measures include reassessing contracts with service providers, clarifying ownership of assets related to the protocol, introducing an AAVE buyback and burn mechanism, and making capital allocation more explicitly centered around tokens.

This marks a significant transformation in Aave's economic model: from initially blindly funding the protocol's extensive growth to finding a balance between "protocol reinvestment" and "disciplined value returns to AAVE holders approved by governance." Over the past two years, Aave has launched buybacks (currently temporarily suspended following the rsETH incident) and implemented the "Aave Will Win (AWW)" framework to channel value into the DAO.

Although this is a complex and iterative process, aligning the interests of protocols with those of token holders is essential for the crypto industry to move toward the next stage of growth.

Chart 12: Correlation between the evolution of token value capture and the historical price trend of AAVE

How important is the token "value capture" mechanism?

Remember this: Just because a project makes money doesn't mean its tokens are valuable.

In traditional stock markets, investors can typically analyze revenue, profit margins, and free cash flow through shareholder ownership and residual claims.

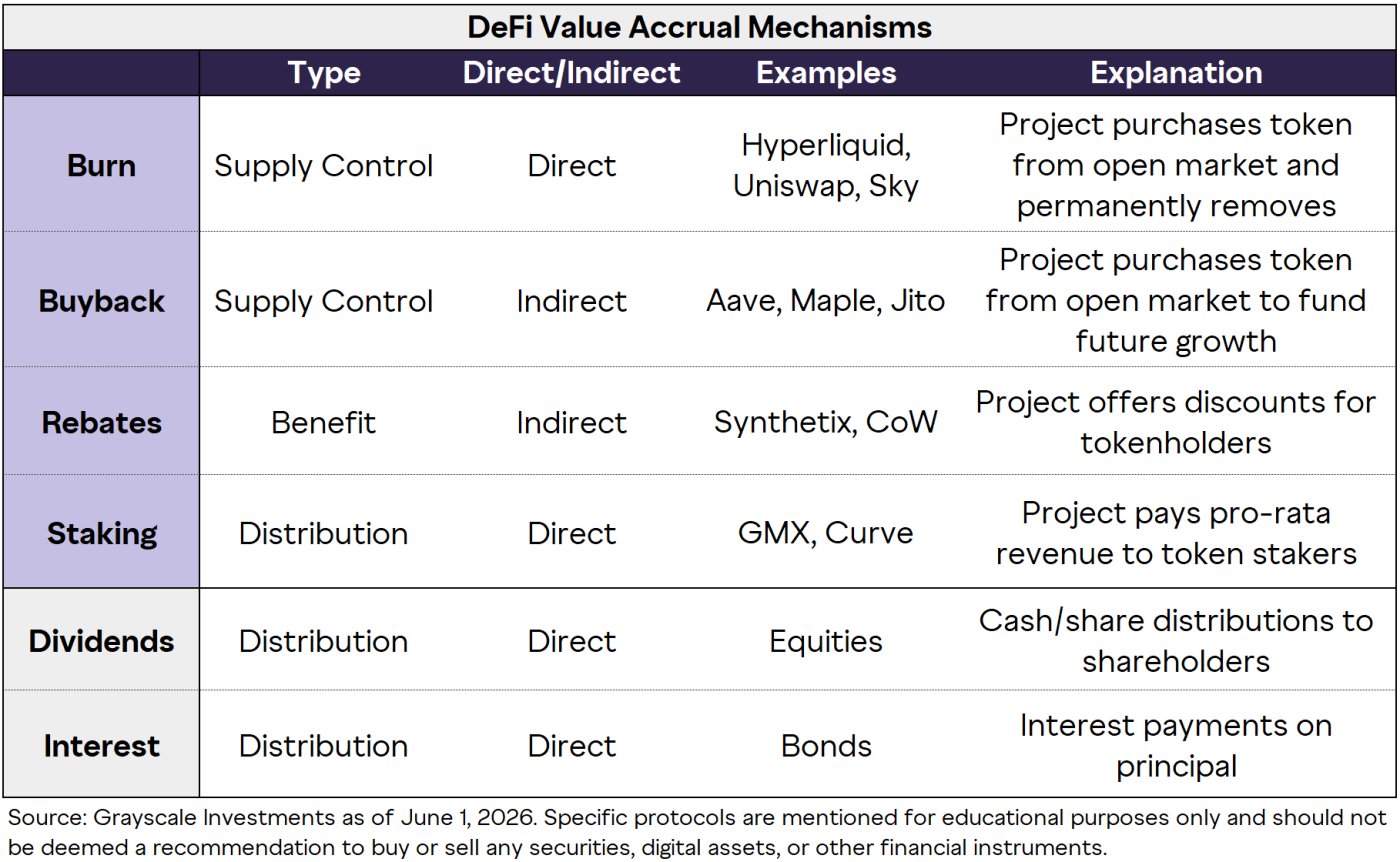

However, in DeFi, there's no unified standard for how projects handle their profits, nor between protocol economics and token holder value: fees can be retained by the protocol, kept in the treasury, used to subsidize liquidity providers, or redistributed to token holders through governance mechanisms. The most common creative ways to distribute profits are nothing more than: burning, buybacks, rebates, and staking.

Chart 13: Four Main Structures Driving Token Value Capture by DeFi Protocols

These mechanisms differ significantly in their directness, persistence, and economic impact. Some protocols reward value by explicitly reducing supply or distributing dividends, while others rely on more indirect, utility-based benefits (such as discounts or treasury allocations controlled by governance). This results in vastly different proportions of the money earned by the protocols ultimately reaching token holders.

Therefore, valuing DeFi involves much more than simply measuring the total revenue of top-level protocols; investors must also rigorously assess the "conversion rate from protocol economics to token value." The stronger and more transparent this conversion mechanism, the more suitable it is to use a cash flow-oriented framework to evaluate the token.

It's important to reiterate that not all protocol revenue can be unconditionally attributed to token holders from an economic perspective. Fees generated by DeFi protocols often need to be used first to incentivize supply-side users (such as depositors and limited partners) and cover daily operating expenses. Therefore, protocol profits (rather than total fee revenue) may better reflect the cash flow that ultimately supports the growth of token value for token holders.

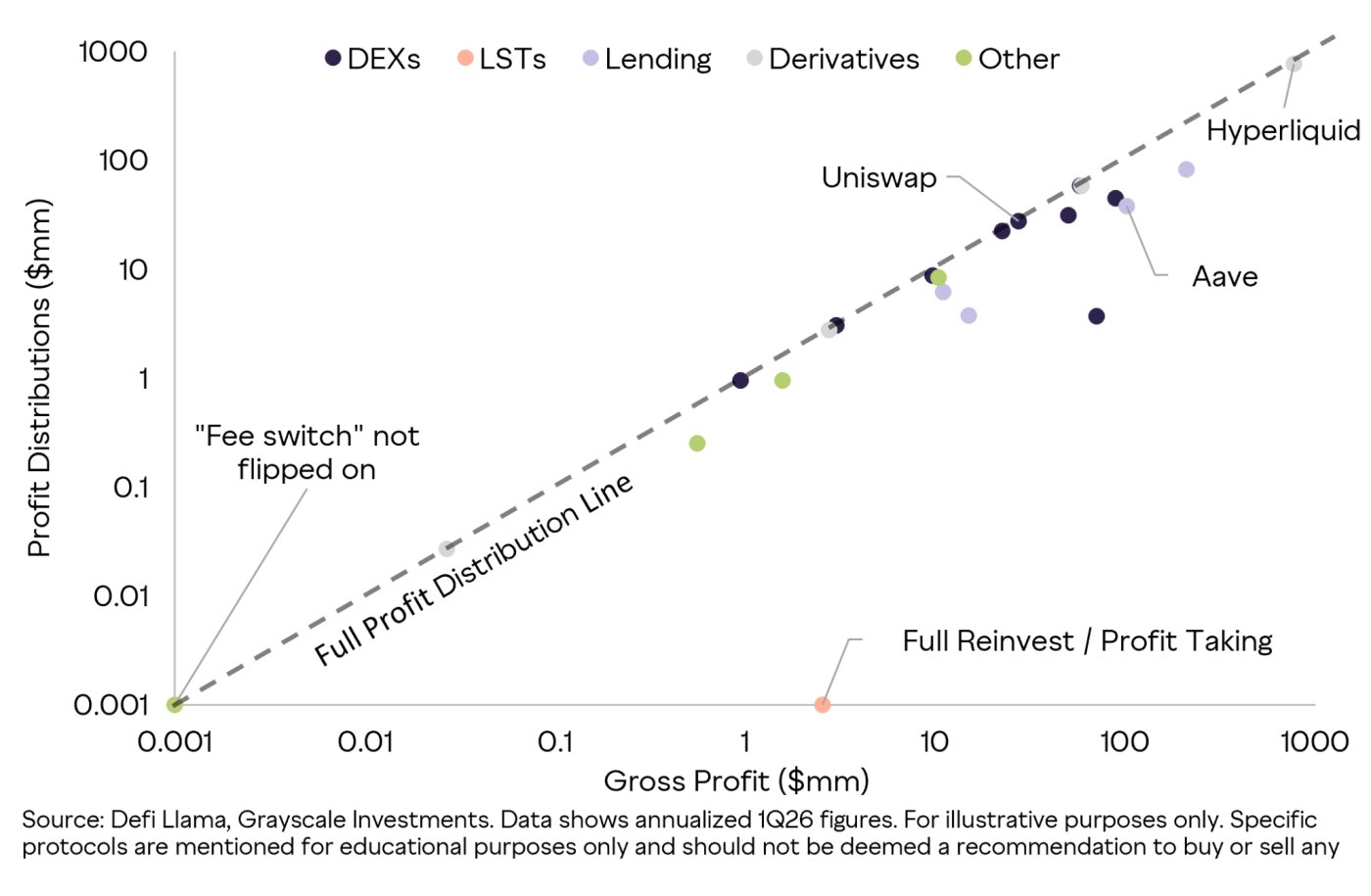

Throughout the DeFi industry, different protocols vary drastically in their profitability and willingness to share profits with token holders. This difference can largely be attributed to the fundamentally different underlying business models across different DeFi sectors.

Chart 14: Differences in the conversion of protocol profits to token holders (taking major DeFi protocols as examples)

This immense decentralization precisely illustrates why we must never solely focus on the total revenue of a protocol when valuing DeFi tokens. Two projects that earn the same amount of money may yield drastically different actual returns for token holders due to differences in cost structures, governance decisions, government policies, and specific value capture mechanisms.

Of course, a lower distribution rate is not necessarily a bad thing—it is also healthy if the retained profits are efficiently reinvested in projects that can enhance the long-term value of the token (such as improving liquidity, strengthening security, accelerating product development, user subsidies, or ecosystem integration).

Therefore, investors should focus on two points as closely as they would on a company's financial statements: How much of the profit was returned to token holders today? And how was the retained profit efficiently deployed? Only projects that can make a lot of money, know how to reinvest reasonably, and have a transparent distribution mechanism deserve a high valuation using a cash flow model.

DAO's awkward identity and regulatory impasse

There is another unavoidable real-world issue in the crypto: whether token holders have legal and enforceable recourse to the assets or cash flows associated with the protocol.

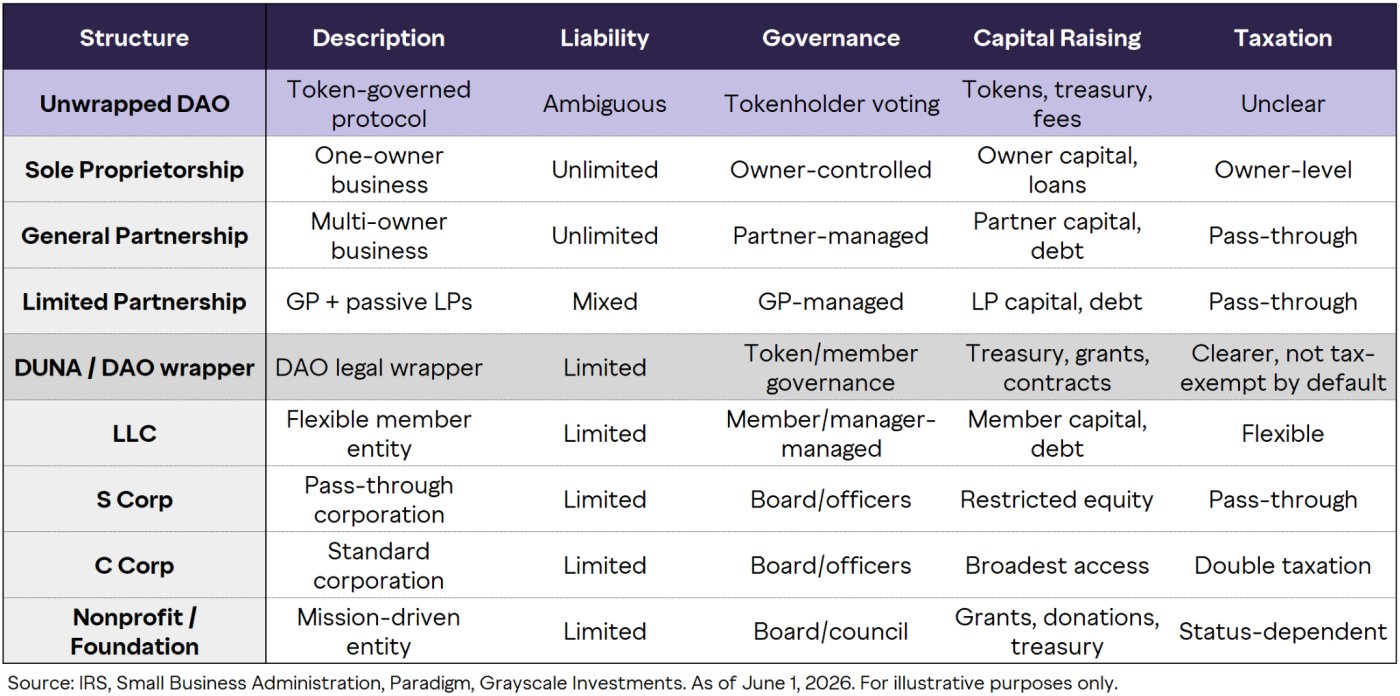

In traditional stock markets, shareholders typically possess clear governance rights, residual claims on company assets, and potential economic claims on future cash flows. Token holders, however, often rely on smart contracts, DAO governance processes, treasury multi-signature controls, and community consensus. In most cases, token ownership does not automatically generate a proportional claim on protocol assets, nor does it provide a legally enforceable right to future income. However, a fully decentralized DAO can forcefully align the interests of token holders with the protocol's development direction through completely transparent token voting.

To overcome this legal ambiguity, an increasing number of DAOs are adopting "legal shells" to grant them legitimate corporate status, limit the personal civil liability of participants, and allow them to conduct off-chain activities such as signing contracts, recruiting, managing public funds offline, and holding intellectual property. Common legal structures include limited liability companies (LLCs), offshore foundations, special purpose trusts, and the recently prominent "Decentralized Non-Institutional Nonprofit Association (DUNA)." These structures can significantly improve operational clarity and protect members from unlimited joint and several liability, but they do not automatically transform governance tokens into equity claims similar to traditional stocks. In most cases, the economic interests of token holders still depend on governance decisions and explicit on-chain value capture mechanisms, rather than default legal ownership.

Chart 15: A Comprehensive Comparison of DAOs and Traditional Legal Entities

DAO governance can help solve the value capture problem by giving token holders direct control over the protocol's economics. In publicly traded stocks, shareholders typically rely solely on management and the board of directors to allocate capital. When management incentives diverge from shareholder returns, potential principal-agent conflicts often arise.

Conversely, protocols governed by DAOs allow token holders to directly vote on business details such as treasury management, fee parameters, incentive amounts, buybacks, and burns. While this structure cannot completely eliminate governance risks such as low participation rates, excessive token concentration, or regulatory uncertainty, a robust governance architecture and clear voting rights establish a more direct link between the protocol's success and the value to token holders.

The legal and governance considerations of DAOs are not merely theoretical; they are central to determining how DeFi tokens should be properly valued. While DeFi protocols can generate clearly visible revenue, token holders do not automatically have the same recourse to this revenue as stockholders own the residual value of a company. Therefore, the core valuation question shifts from "Does the protocol make money?" to "Through what path (if any) does the money earned by the protocol transfer and accumulate on the tokens?"

Furthermore, current market predictions suggest that the CLARITY Act, specifically designed to define the legal status of crypto projects, has a 51% chance of passing in 2026. The core of this act is to examine governance concentration and administrator privileges to determine whether a project is truly "decentralized," with the assessment primarily based on factors such as governance concentration, protocol upgrades/administrator privileges, and the influence of related parties.

This framework makes a strict distinction between "network assets" and tokens that are still deeply tied to investment contracts, issuers, and associated controllers. Since DAOs are inherently decentralized, the focus is on the concentration of token holders: who has voting power. We believe that mature DeFi projects like Aave are likely to meet the criteria for being classified as network assets; however, some ambiguities remain.

Say goodbye to hype, embrace fundamentals

As the crypto market matures, valuation frameworks are rapidly catching up with the underlying economic realities. Many leading protocols are now steadfastly implementing economic initiatives, directly translating protocol activity into token value accumulation. Investors skilled in applying rigorous, context-specific valuation frameworks can expect to reap substantial profits from the still prevalent pricing mismatches.

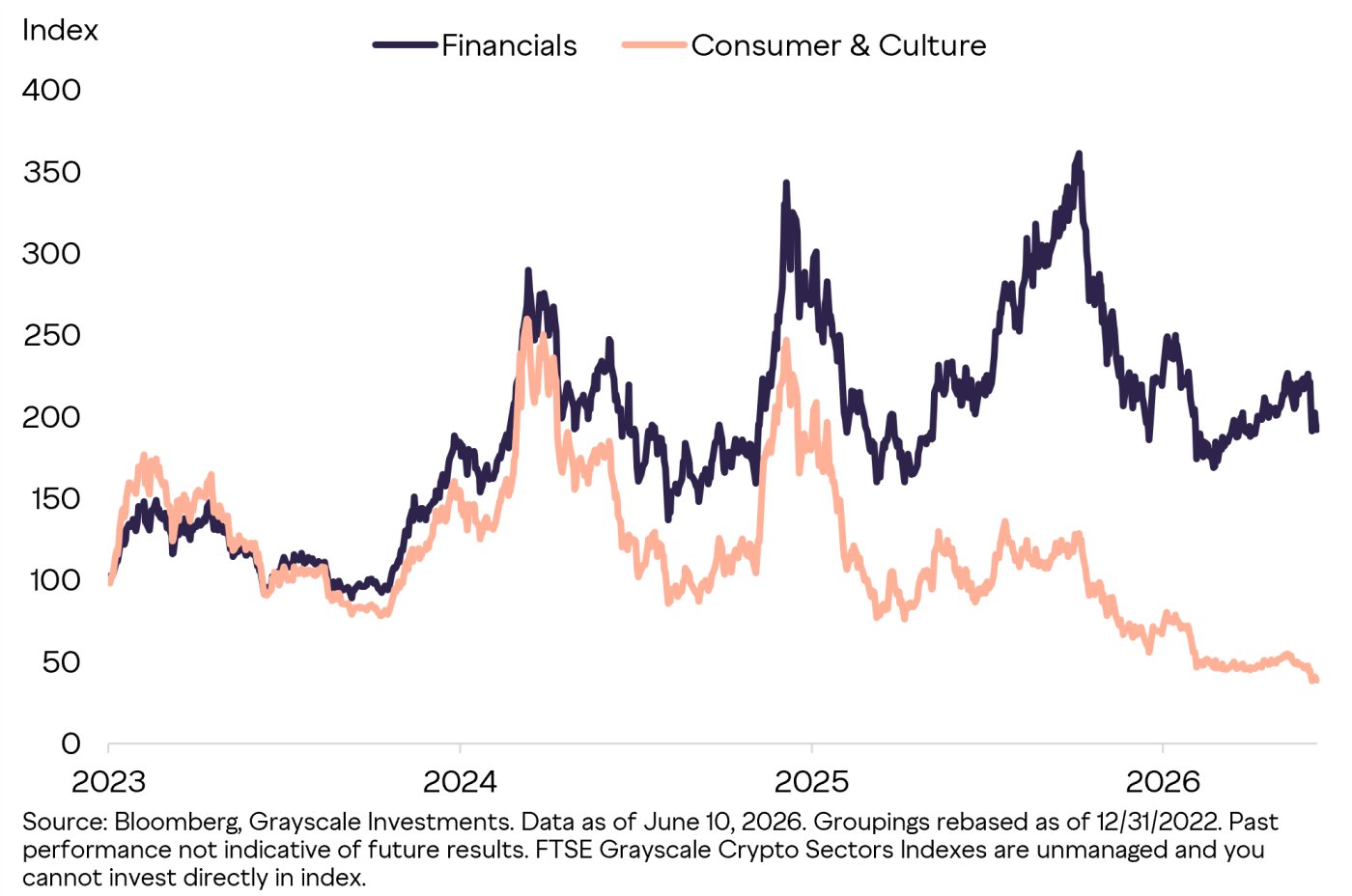

As regulations become clearer and institutions enter the market, market leadership is voting with its feet: leaving behind those worthless cryptocurrencies that rely solely on narratives and flocking to those solid sectors that demonstrate genuine adoption rates, sustainable business models, and observable financial fundamentals.

Chart 16: Performance Returns of Crypto Markets on Protocols that "Create Real Value" (Token Performance Since the Beginning of the Year)

The divergence in the crypto market this year is no accident. It profoundly reflects a complete reshuffling and repricing of the entire market—funds are leaving purely speculative projects and flowing firmly into assets with substantial returns and disciplined capital allocation.

Aave is the best microcosm of this evolution: it turns the true product-market fit into an extremely beautiful financial statement, forcing us to re-examine it with the traditional perspective of financial business.

For investors looking to gain exposure to the next phase of the crypto market, cast aside unrealistic fantasies. Instead, delve into truly profitable projects like Hyperliquid, Aave, Uniswap, Sky, and Maple , and calculate their value using price multipliers and fundamentals. You'll discover that a golden opportunity for value investors has already clearly emerged.