Join the 1000’s of founders, investors, crypto funds, brokerage firms, and developers in getting free cutting edge crypto research by subscribing below:

Thanks for reading Decentral Park Research! Subscribe for free to receive new posts and support my work.

Eye of the Storm

After a brief hiatus, it’s time to analyze the key crypto market signals dig into the state of affairs. Economic data like JOLTS and a 2-day testimony by Jerome Powell provided several landmines for investors but it was the collapse of US regional banks that started to shake the market.

It all started with the winding down of crypto-friendly bank, Silvergate last Wednesday following its inability to produce its annual report. Q4 was a devastating year period for the bank with $13.3b in deposits vs. $11.4b in investment securities by September 2022.

Over the course of 3 months, deposits shrank to $6.6b forcing Silvergate to raise money by selling down its securities book - the only (quite significant) problem here is that the value of the securities fell in value due to the high interest rate environment.

Only 1 day later, Silicon Valley Bank (SVB) announced a surprise stock offering to its clients before revising its sharper decline in net interest income - a combination of moves that drove fear among depositors that spiralled in quick succession.

The common thread between these two situations was the more fickle depositor base with both banks being unable to keep up with requests. For SVB, the problem was more related to a duration mismatch in asset and liabilities with SVB needing to liquidate all of its securities available to sale in its portfolio but realizing a loss in the process.

On Sunday, one of the last crypto-friendly banks, Signature announced that regulators have shut down operations citing ‘systemic risk’.

Note - it’s not just banks regulators are shutting down but also privacy network like Aztec which announced the sunsetting of their chain this week

Coming back to the key issue, the fall of regional banks has had a direct impact on the crypto sphere - both due to prominent infrastructure players like Circle having substantial reserves at these banks as well as crypto startups and funds being forced to bank with an increasingly smaller set of providers.

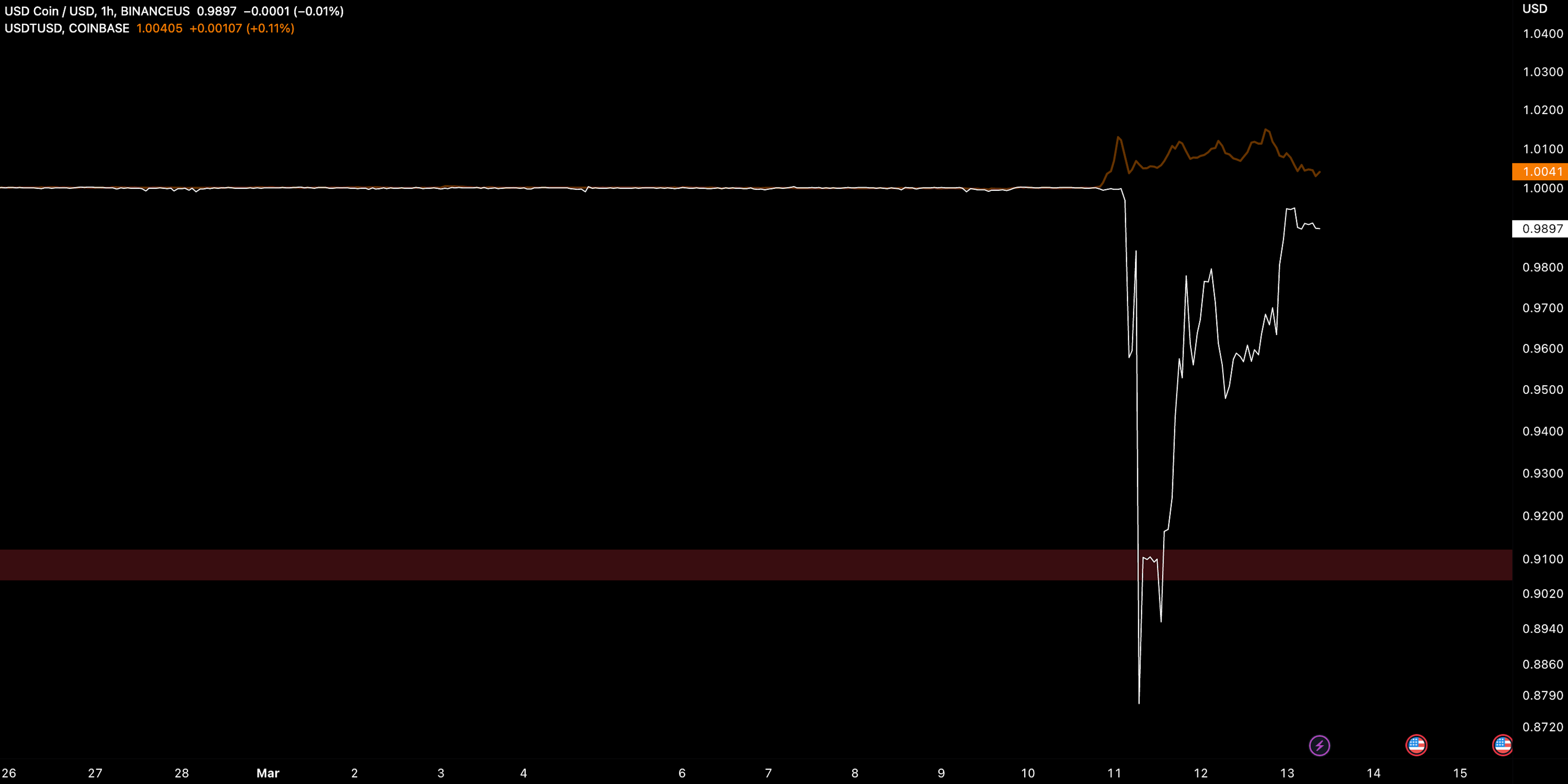

Investors double-clicked on Circle and its ability to continue backing USDC 100% despite having $3.3B in reserves for its 40B USDC supply.

Investors were quick to price in a 8.25% discount to par (effectively adjusting for this collateral risk ratio) after a more extreme de-pegging which drove USDC to trade at $0.87. At the same time, Tether’s USDT broke above its peg due to heightened demand.

At this point, investors were concerned that every redemption would be a drive in a discount widening given that a smaller percentage of the collateral base would be backing the total supply of USDC.

Confidence in USDC was restored from a combination of factors:

The reality is if every USDC outside of the $3.3B at SVB can be redeemed 1:1 for USDC (excl. illiquidity risk and corresponding discounts) then arbs will rationally pay for that USDC closer to $1 (vs. away from $1).

Circle stated they would look to corporate profits/raise to help fill in the hole if necessary

Circle announced USDC operations will open for business on Monday morning including a new automated settlement via a new partnership with Cross River Bank

The Fed Board announced it will make available additional funding to eligible depository institutions to ensure stability

The last point is perhaps the most important as SVB may mark the start of something bigger. The sharp rise in interest rates over the last few years have created $620B in unrealized losses - up from $8b a year.

For risk asset investors, the fragility of regional banks who face higher risk in a high interest rate environment is exactly the catalyst bullish investors were looking for - the need for looser financial conditions in short order.

The safest asset in the world became one of the most risky assets in the world.

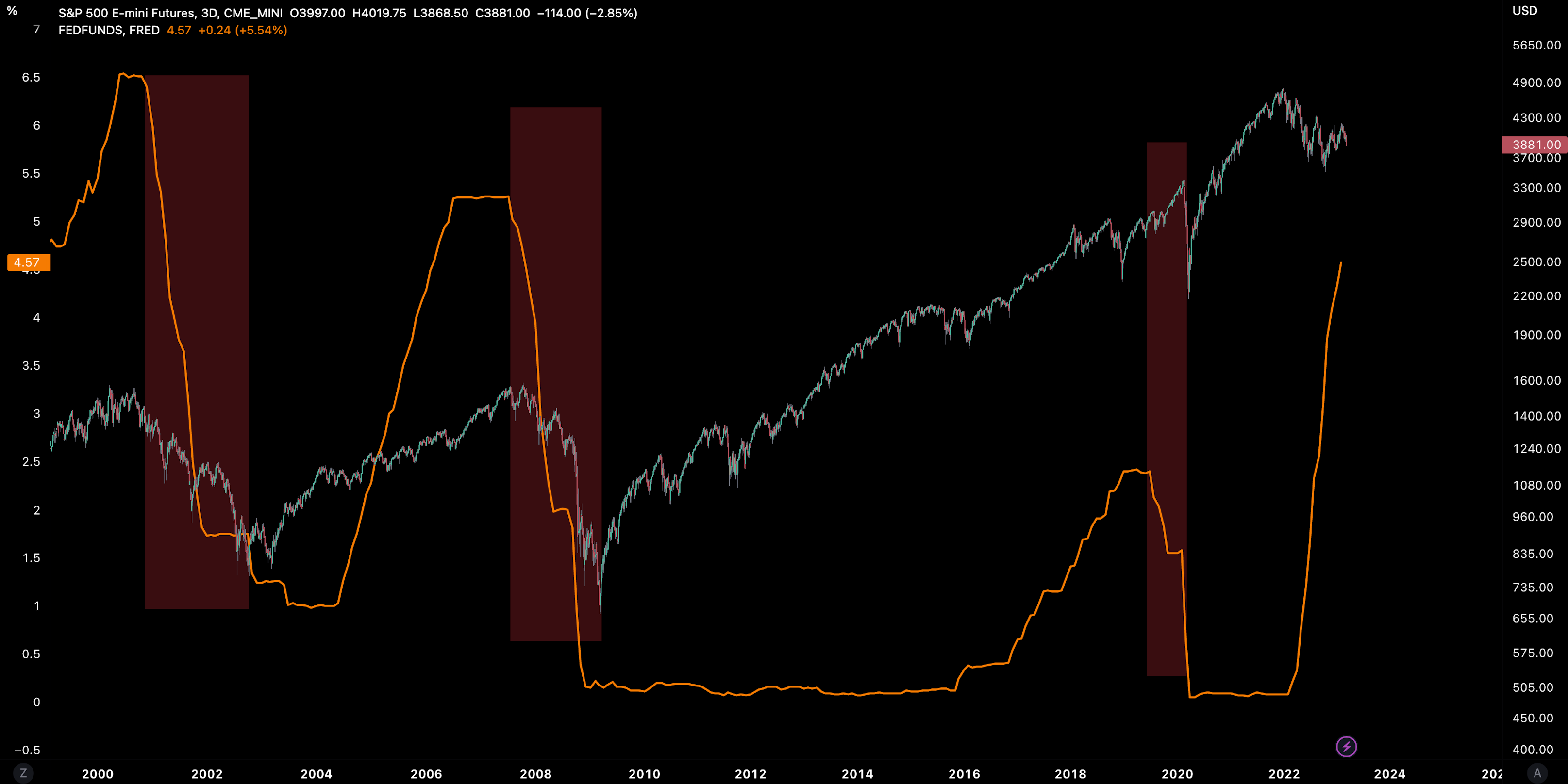

In just over a couple of week, the interest rate discussion has moved from a 50bps hike potential to a pause/cutting potential. Traders are now pricing in terminal Fed funds rate of 5.1% from 5.7% with 2-years falling ~50bps in just 3 days.

Investors are now looking to the Fed’s balance sheet to understand how liquidity may expand and, therefore, run counter to the tightening effect that has negatively impacted risk asset markets including crypto for some time.

The thinking here is the Fed’s balance will begin to expand more steeply which will increase USD liquidity. Why is this exciting? The correlation between the crypto market index and market liquidity remains positive.

However, a pause does not equal pivot with the gap between Fed pauses and pivots being anywhere from 8 months to 15 months since 2000. Capitulation also comes when the Fed cuts rates vs. simply pausing. The former still feels some time away given the Fed’s continued need to tame prices while providing a new lending facility to back banks.

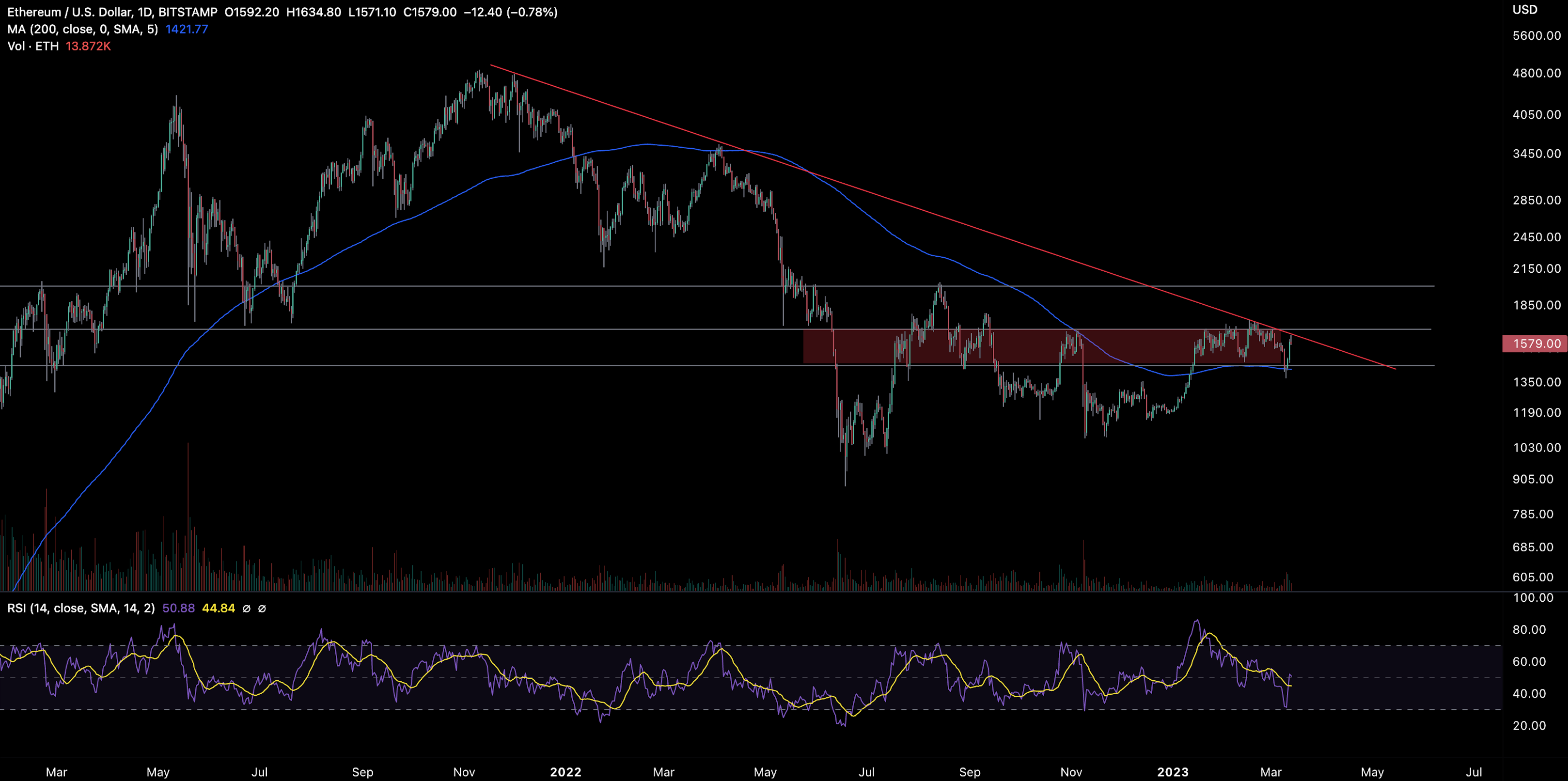

Beta assets like BTC and ETH have held up well all things considering, holding above $22k and $1.4k respectively.

We also note that ETH/BTC has also managed to gain 6% from its February bottom showing some evidence that risk-on appetite remains in tact leading up to the Shanghai upgrade in the coming weeks.

Binance is also looking to swap $1B of BUSD to BNB, BTC, and ETH which may create an effective TWAP into those high cap names in the near-term.

The need to be cautious

However, we see clear reasons to be cautious in nearer-term.

The Binance conversion may be viewed as an inability for Binance to offramp its BUSD as the US may end of blocking such a request.

Related to this, the ongoing risk related to banking is that there are a smaller subset of fully operational regional banks that can service crypto businesses. These include:

BCB Group

Cross River

Customers Bank

Jewel

Mercury

Series

Circle’s partnership with Cross River is out of necessity, not out of desire. What is unclear now is how much at risk is Cross River given the distinction between crypto-related banks and fintech related banks when it comes to bailout for depositors?

On monday, BCB has paused US dollar payments pilot after Signature Bank closure.

Circle may be saved for now by the Federal Reserve white knight but can that be said of all its existing partnerships? This will be an ongoing assessment in real-time and the market’s pricing of USDC will be a proxy measure of overall confidence in crypto’s survival in the face of regional bank collapse.

On Monday, OKCoin decided to pause USD on-ramp due to Signature’s Bank collapse. This is the first exchange to lose its ability to process USD deposits following SVB.

However, as we see with the unrealized losses chart, the banking stress is not crypto-related. Rather, a function of purchase concentrated risk on balance sheets in a low to high interest rate environment.

Liquidity Remains King

While investors look to recent announcements by the Fed as ‘unofficial QE’, making the printer go brrrr may not actual translate to a capital expansion within the crypto ecosystem.

Why? Because the very issue the industry faces is the regulators choking the infrastructure servicing the on/off fiat ramp to cryptoassets. To put it more flippantly, the top three cornerstone fiat ramps for crypto were all shutdown last week.

Stablecoin supplies, which was a key driver of liquidity expansion in the past bull cycle, continues to show net negative growth. Last week, stablecoins had one of the sharpest short-term declines since June 2022.

Crypto’s market capitalization is also getting challenged at key levels including the psychological $1t mark once again while stablecoin supply

Stablecoin issuers are also seeing fewer options to be able to mint stablecoins after Signature Bank shutdown. The question remains: “Where can billions of stablecoin issuance be facilitated with confidence in the current environment?”.

We are seeing strong pulses of stablecoin issuance which may signal confidence being restored in Circle’s ability to navigate the ship for now.

ETH is also getting rejected at the $1.6k level on Monday. Performance swings across assets (one asset benefits at the expense of the other) while the overall pie is shrinking.

Overlaying stablecoin supplies with DeFi MCAP dominance provides further evidence of upside caps. The sector has failed to gain ground when the pie has been shrinking…

And Euler Finance being hacked for $200m will do little to boost confidence in the sector in the near-term.

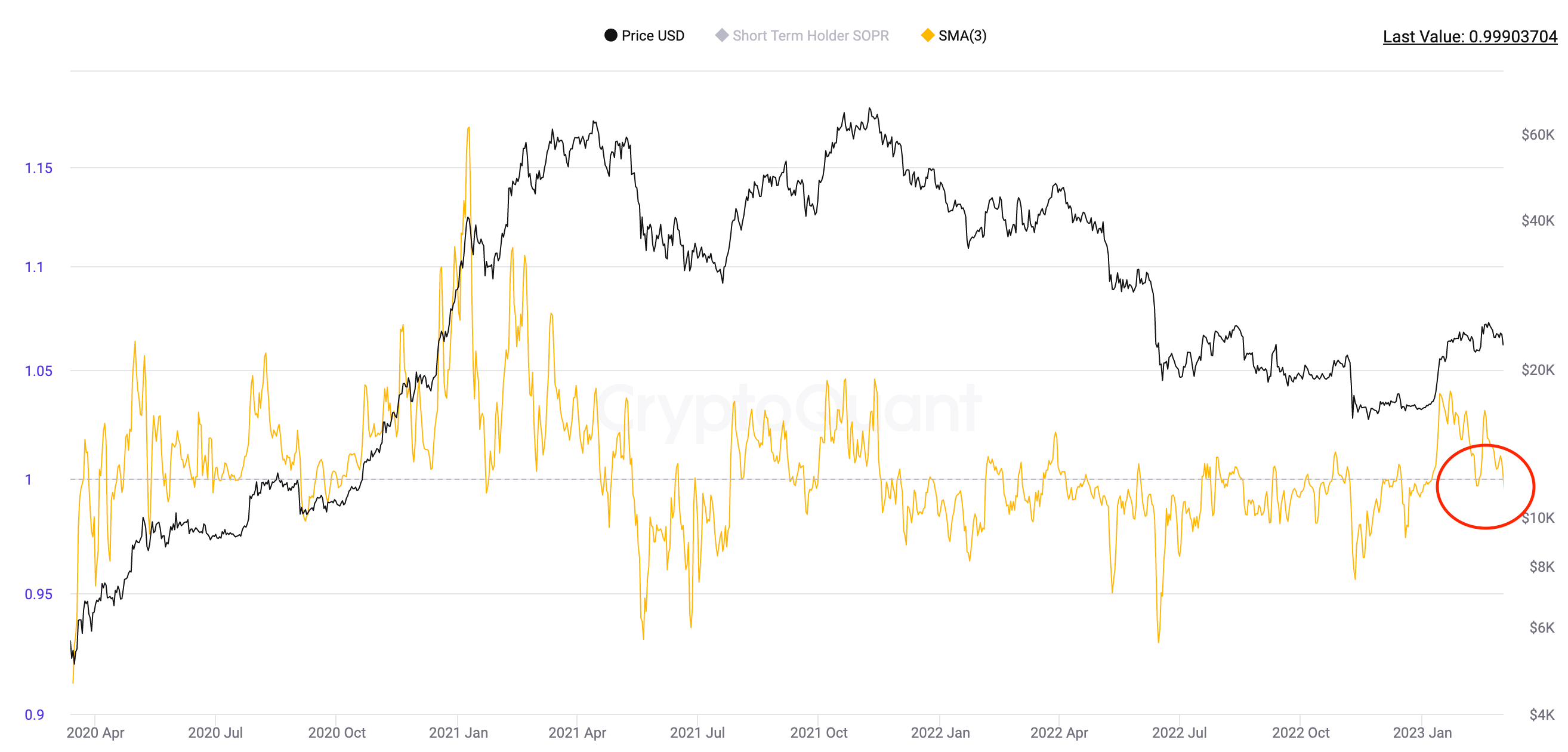

Analyzing short-term traders who are more likely to impact price near-term show that those traders are starting to sell at a loss. STH-aSOPR is falling below 1 after being supported above 1 (bullish period) which indicates markets are not yet showing high level of constructiveness.

Correlations between the crypto market and tech stocks remains moderately positive with some noise. The 8% lift in cryptoassets on Monday is met with moderate gains in NASDAQ.

Investors are starting to become wary in fear of a wider fallout in the financial system. Should the correlation between these two markets remain positive in a crisis, the cryptoasset market path of least resistance is down, not up.

After all, the need for managers to gain liquidity fast often means selling out of riskiest assets first.

On a relative basis, BTC has the potential to gather pace under a collection of narratives including the Bitcoin halving which is ~420 days away.

We still see a path for BTC dominance to climb back up to its 3 year highs of 47%+ after bouncing of its cycle lows.

The BTC and ETH dominance index is getting closer to breaking/rejecting its 3 year resistance too. The outcome being a useful signal for risk-on or risk-off momentum continuation or change.

Closing thoughts

The Fed now finds itself needing to prioritising financial stability over inflation. It may end up being the bank runs and the fast unwinding of highly leveraged institutions that will act as the ultimate deflationary catalyst.

While we will likely see near-term turbulence, it is moments like this where we are reminded why Bitcoin was born out of the 2008 crisis.

The current level of rates are too high relative to the indebtedness across major economies and the need to turn on the liquidity taps to prevent a widespread collapse will mark the beginning of the next bull cycle. There will just likely be more casualties on the way.

Put more poetically, the banking system is starting to fail one year before the Bitcoin halving cycle. Here’s to the good times.

Decentral Park Market Pulse

Want real time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Global Market Cap

$977B; Crypto markets remain flat over the past 2 weeks but unable to breach past the key $1t mark. Facing multi-year resistance level and rejected on Monday with post SVB collapse rally.

DeFi MCAP

$45B; DeFi sector remains above its 200d MA using once resistance as new support on Saturday. Looks to be more constructive if the 200d MA can hold.

Trader Positioning

BTC OI weighted funding rate flips positive after shorts get liquidated following the collapse of SVB and shut down of Silvergate and Signature (consensus trades).

80% of total liquidations over the past 24hrs have been short with $50m longs vs. $191m shorts. Larger liquidation total for ETH at $87m vs. BTC at $75m.

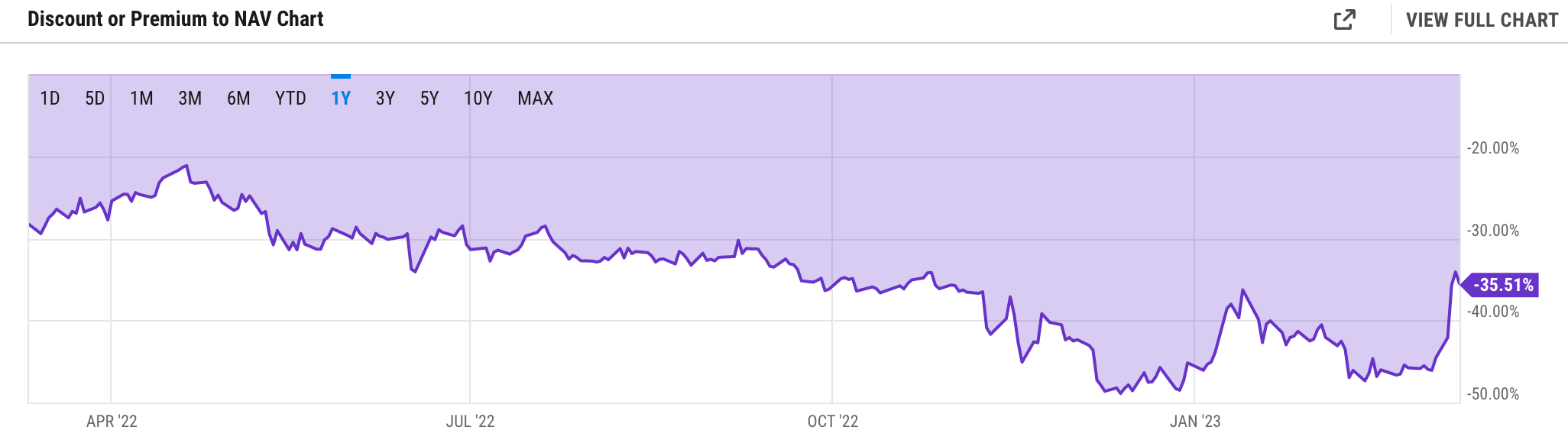

Grayscale Trusts

Narrowing of the GBTC discount to NAV (-35.5%) despite more muted price action around the $20k level. GBTC likely being bid after initial oral arguments are making traders place higher odds of Grayscale’s win over the SEC in the Bitcoin ETF approval effort.

ETHE discount to NAV has narrowed to 46.8% and moving in line with GBTC’s dynamic but to a lesser degree. Stronger emphasis behind GBTC/BTC.

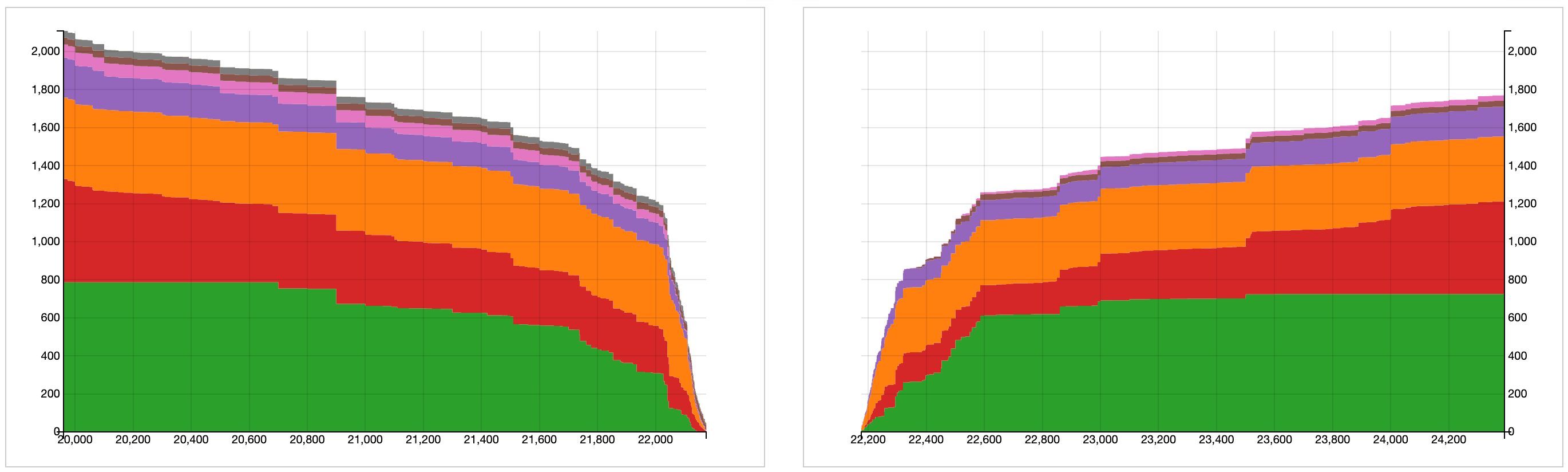

BTC/USD Aggregate Order Books

Order books look much heavier on the bid side. Heavier resistance up to ~$22.5k.

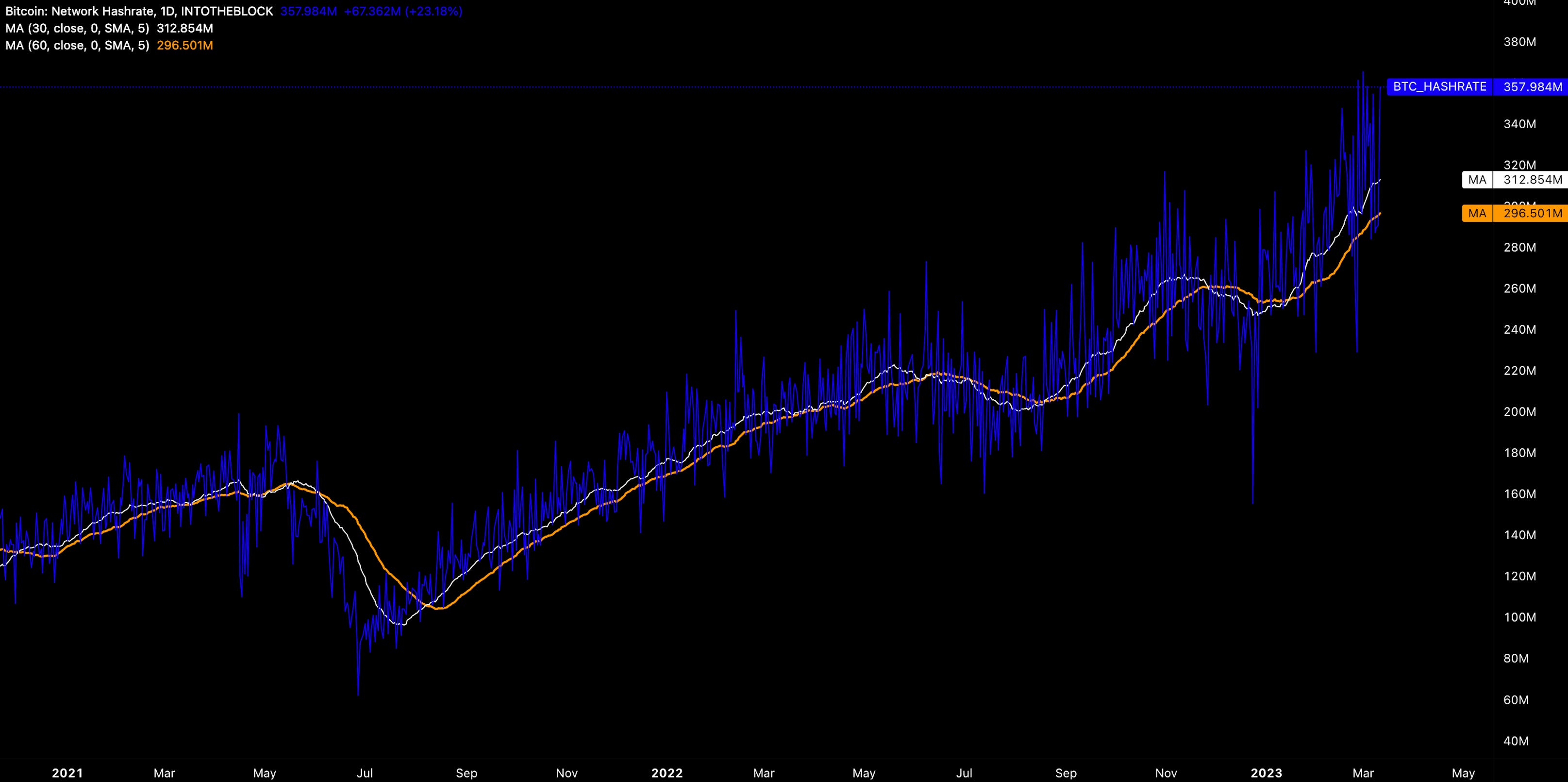

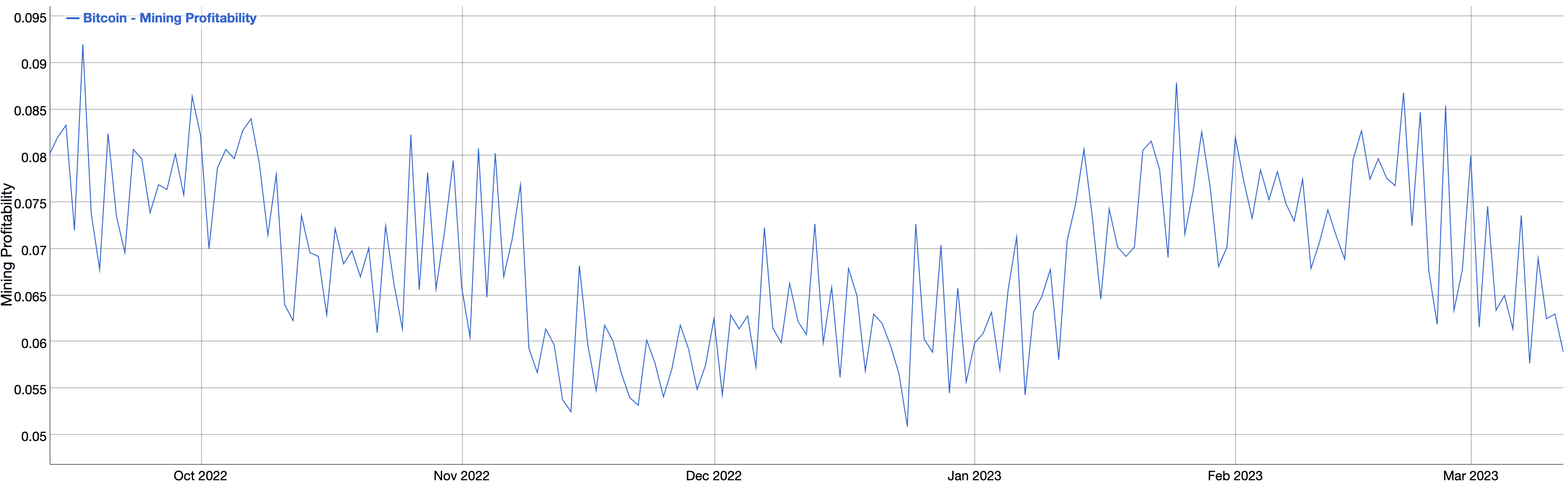

Miners

Bitcoin hash rate climbs to new all-time-highs despite muted price action. Miners continue to double down with miner profitability falling in March to 0.06 USD/day for 1 THash/s.

Hashprice looks to climb to new cycle highs where peaks in this measure correspond to market bottoms (local and cycle). This comes as mining difficulty climbs to new all-time-highs.

Few gainers in the market over the past week with the largest losers being concentrated in the centralized exchange bucket.

Top 100 (7d %):

Kava (+29%)

Aptos (+3.9%)

PAX Gold (+3.8%)

BNB (+3.2%)

Tether Gold (+1.9%)

Bottom Top 100 MCAPs (7d %):

SingularityNET (-24.1%)

Huobi (-22.1%)

OKC (-20.9%)

Dash (-19.7%)

WEMIX (-18.8%)

> The Largest Bank Failure Since 2008 [On The Margin]

> Silicon Valley Bank Implodes [All-In]

> Reinventing the credit card as a Fintech super app [The Fintech Blueprint]

> Solana’s Endgame [The Delphi Podcast]

> Why We’re Investing $20m into DAOs [Blockcrunch Podcast]

> Crypto bank assassinations [Ryan Selkis]

> Market Run down [Ram Ahuluwalia]

> USDC Trading Dominates Record Day for DeFi Exchanges Uniswap, Curve [Coindesk]

> Grayscale Win Over SEC Might Not Change Much, Industry Watchers Say [Blockworks]

> Crypto Funding: Yes, There is Still Crypto Funding [Peter Reservoir]

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.