Huobi Research released the research report " RWA : The Next Crypto Wealth Code" , which provides a comprehensive introduction to the development of the RWA track. This research report analyzes 19 representative RWA projects in detail from multiple dimensions such as RWA tokenization mechanism, protocol status, token functions and performance, protocol advantages and risks. Through the analysis and summary of these projects, we can get a glimpse of the overall development and existing problems of the RWA project, as well as its future potential.

Introduction

Blockchain brings trust, liquidity, transparency, security, efficiency and innovation, but the bear market in the encryption industry seems to be difficult to find new growth points. The encryption industry urgently needs a track to carry a new narrative. RWA tokenization can open up the channel between traditional finance and crypto-finance, carrying an asset market worth tens of trillions of dollars. For the crypto industry, it can be the water of life that transcends the bull-bear cycle, so it has been tried since the birth of the blockchain. RWA tokenization has been hindered by multiple factors such as technology, regulation, and market. Nowadays, the RWA track is hotly discussed again, and many organizations have begun to make arrangements. RWA projects have been characterized by a wide variety of projects, mainly DeFi, high returns, and high risks, and have gradually entered the public eye. However, the projects generally still have problems such as poor liquidity, early stage, and lack of price discovery. Whether the RWA track can explode in the next few years also depends on the development of infrastructure and the improvement of the regulatory system. This research report also proposes that token standardization and compliance are the only way for the development of the RWA track. Although the RWA track faces multiple challenges, industry development is always moving forward. We have seen the emergence of many innovative projects, especially projects based on U.S. debt and U.S. stocks, small and medium-sized enterprise financing, and real assets. The main characteristics of these projects are :

1. Cooperate with traditional financial institutions;

2. Maximize the benefits of projects and tokens;

3. Introduce more legitimate third-party participation.

These features can partially solve the problems in RWA tokenization, including supervision, centralization, on-chain and off-chain identities, asset valuation, etc. We look forward to more projects in the future to enrich the RWA track.

1 Narrative in the making

After a bear market that lasted for more than a year, the market value of the entire encryption market has shrunk severely, funds have continued to flow out, activities on the chain have been sluggish, DeFi income is no longer attractive, and mutual cuts are serious. Now we cannot imagine what the encryption industry should rely on to start the next bull market. There is still a big gap between the encryption market and the traditional financial market. But we can also get a glimpse of huge business opportunities from some thunderstorms in the bear market.

It can be said that the main reason for the bankruptcy of some large institutions in 2022 is the use of altcoins for financing and lending. When altcoins plummet in the bear market, the liquidation of loans is further exacerbated, and the death spiral begins. We see that it is institutions and credit that drive the bull market in 2021, and they also contribute to the bear market in 2022. In fact, credit drives trillions of dollars worth of business and much of the global economy. The potential it brings is huge, and currently, in the DeFi market, more and more protocols are entering traditional credit markets such as equity and debt financing. Although it brings some risks, this is the only way to introduce more than 800 trillion US dollars of traditional financial markets onto the chain. What we need to do to bridge the huge gap between crypto markets and traditional finance is the tokenization of real-world assets.

In the first half of this year, the traditional and crypto industries began to pay attention to the RWA sector.

The first is that Goldman Sachs announced the official launch of its digital asset platform GS DAP, which has helped the European Investment Bank (EIB) issue a two-year digital bond of 100 million euros. Soon after, Hamilton Lane, a private equity firm with a management scale of over 100 billion, tokenized part of its $2.1 billion flagship equity fund on the Polygon network and sold it to investors; million euros in digital bonds. Secondly, some government agencies have also begun to test the waters of RWA, including the Monetary Authority of Singapore (MAS), which will cooperate with JPMorgan Chase and DBS Bank.

In April, Binance announced that it would become the operator of Polymesh nodes on the Layer1 blockchain; secondly, DeFi protocols such as MakerDAO, Aave, and Maple Finance are active on the RWA track, and more crypto investment companies are also seeking RWA projects. At present, there are more than 50 projects in the RWA sector, mainly in financial assets, including fixed income, TradFi, and a small number in real estate and carbon credits. Recently, RWA concept tokens have all risen, with some rising more than 10 times. Does the wave of momentum in the first half of 2023 indicate that RWA will lead the crypto narrative in the next few years?

2 RWA’s past and present life

The concept of RWA is not new to the blockchain industry. The earliest RWA project is the BTM Bytom chain that "asset-on-chain". Currently, the most successful RWAs are the digital U.S. dollars USDT and USDC, which map the U.S. dollar to the chain and tokenize it. Stablecoins have subtly influenced the entire crypto industry and have now become an important cornerstone.

The full name of RWA is the value tokenization of real world assets (real world assets-tokenization), which is the process of converting the ownership value (and any related rights) in tangible or intangible assets into digital tokens. This enables digital ownership, transfer and storage of assets without the need for a central intermediary, with value mapped onto the blockchain and traded. RWA can be tangible or intangible assets.

Tangible assets include: real estate, art, precious metals, vehicles, sports clubs, horse racing, etc.

Intangible assets include: stocks and bonds, intellectual property, investment funds, synthetic assets, revenue sharing agreements, cash, accounts receivable, etc.

2.1 Current status of RWA track

There are many types of RWA track projects, most of which are based on DeFi. There are three main categories: 1. Fixed-income projects based on off-chain assets such as U.S. bonds, stocks, real estate, and artwork; 2. Public funds issued or traded on the open market Credit projects; 3. Trading market projects based on virtual assets such as carbon credits. In addition, there are also infrastructure projects such as vertical public chains.

The fixed income category is based on the U.S. Treasury and stock markets and provides loans to private individuals and institutions. The only difference between these projects and other DeFi lending projects on the chain is that the collateral can be real-world assets.

The public credit category can establish investment funds by tracking U.S. bonds or other bonds for crypto users to invest.

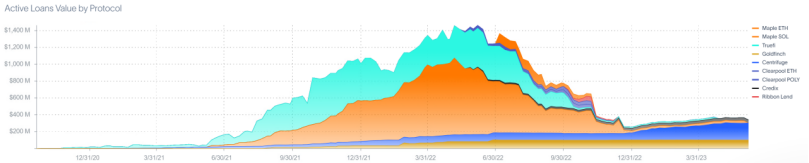

In terms of data, according to statistics from the RWA.xyz website, 8 RWA lending agreements including Centrifuge, Maple, GoldFinch, Credix, Clearpool, TrueFi, and Homecoin have issued a total loan amount of $4.38b, and users can obtain an average APR of 10.52%. Serving countries with a below-middle level of development. These credit lending agreements provide higher returns than most DeFi lending, but in the institutional thunderstorm event in 2022, Maple Finance defaulted on its $69.3 million debt.

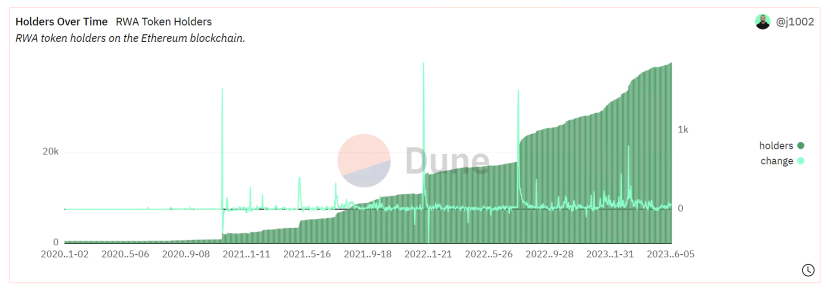

According to the Dune data analysis panel, in the Ethereum RWA project, the number of currency holding addresses of $wCFG, $MPL, $GFI, $FACTR, $ONDO, $RIO, $TRADE, $TRU, $BST is also increasing , currently reaching 3.9k.

2.2 Advantages of asset tokenization

Ideally, any asset of value can be tokenized. The advantages of asset tokenization are also based on decentralization and the bottom layer of blockchain technology, creating some ecological applications to solve the disadvantages of traditional finance, specifically:

(1) Create a potentially huge market and attract investors and retail investors

As leading financial institutions look to benefit from the efficiencies and economic possibilities blockchain brings, the tokenization of real-world assets is gaining institutional attention and several tokenized products have already been developed. The RWA project will also stimulate the investment income of DeFi.

By tokenizing real-world assets, businesses can leverage the DeFi ecosystem to access capital at a low cost and benefit from lower barriers to entry as well as new financing methods, especially for emerging markets. At the same time, the DeFi ecosystem gains new opportunities for investment returns, access to diverse off-chain markets, and expanded traditional financial customer base.

(2) Improve capital flow efficiency and promote positive feedback on asset tokenization

The traditional financial trading market is labor-intensive, and blockchain technology can provide instant settlement, 24-hour transactions, etc., reducing the operating costs and market access of participants. Not only that, asset tokenization can turn illiquid assets into small portfolios without requiring investors to consume a lot of paperwork, money and time. This leads to fairer markets while creating new business and social models, such as shared property ownership or shared rights.

On the securities side, tokenization can be a useful tool for securitization, or refinancing assets from less liquid assets into more liquid security instruments.

Bringing real-world assets on-chain and into the DeFi ecosystem brings unique collateral or investment opportunities, market efficiencies, and liquidity unavailable in traditional markets. The improvement of financial efficiency will further promote the development of the RWA track and form positive feedback.

(3) Lower the entry threshold for retail investors and increase the liquidity of physical assets

Tokenization removes barriers that currently prevent the segmentation of real-world assets, making it possible for most retail investors to gain exposure to asset classes that are usually limited to a few high-net-worth individuals or institutional investors, especially in real assets, allowing retail investors to invest across geographies. Sexual products, or collective investment in a property or a piece of art, require extremely high thresholds in the traditional financial field. These physical objects may have extremely low liquidity in small markets, but once they are put on the chain, they will be accessible to investors from all over the world. Additionally, issuers can reach a broader investor base and create new asset classes. Retail investors gain access to previously inaccessible markets and are able to make more informed investment decisions based on transparent data.

(4) Relying on the advantages of blockchain technology, RWA transactions are more efficient and safer

Blockchain technology ensures the transparency of on-chain payments and data flows, immutability of transaction records, traceability, higher efficiency and lower operating costs, more robust risk management, clear ownership and other advantages, and More composability and a fairer market environment. In the future, as blockchain technology continues to develop, there will be higher-performance public chains or layer2 solutions, more stringent smart contract review mechanisms, and privacy project protection transactions based on zk technology. These are all for the RWA track. Development provides solid soil.

3 Prerequisites for RWA Track Breakout

Asset chaining is the only key point of the RWA track. Solving this key point also requires two foundations, one is the improvement of blockchain infrastructure, and the other is legal supervision. Blockchain involves the interoperability, security, and privacy of various protocols and tokens. Legal supervision refers to whether there are corresponding legal and regulatory support for off-chain assets and on-chain identities. A lot of issues are being actively discussed, but two are discussed here: token standards and censorship.

3.1 Diversification of Token Standards

According to the on-chain token standard, there are ERC-721 and ERC-20 on Ethereum, which correspond to indivisible NFT and divisible token standards respectively. In traditional finance, there are various asset attributes, including tangible assets and intangible assets. For use on the blockchain, we also need to create corresponding token standards to tokenize assets based on their attributes. Fungible tokens and non-fungible tokens have the following characteristics:

Fungible tokens : fungible, each unit has the same market value and validity, meaning token holders can exchange the asset with each other and be confident that it is of the same value; divisible, the asset can be divided when issued Into how many decimal places, each unit will have a proportional value and validity.

Non-fungible assets are not fungible and cannot be replaced because each unit represents a unique value and has unique information and attributes. Non-fungible tokens are also generally non-divisible, although there are ways to split the investment cost to provide fractional ownership, such as in commercial real estate.

Most assets can also use fungible token standards, and some assets, such as bonds and derivatives, may be better tokenized through non-fungible tokens. According to the gradual rise of RWA projects, more rich forms may appear. At this time, simple ERC-20 and ERC-721 can no longer meet the needs of RWA tokenization. Many RWA vertical public chain projects have thought of this and started to create RWA tokenization standards, such as Polymesh. Judging from the current development of RWA projects, most projects are built on Ethereum, so the development of a broader ERC token standard is more universal. ERC-3525 is currently discussed more, and it is possible that more token standards will appear in the future, especially after the baptism of BRC-20. We believe that the token standard that can serve the RWA project well needs to have the following two characteristics:

(1) It has good operability and flexibility for the issuer of RWA tokens, and has the dual characteristics of ERC-721 and ERC-20;

(2) It has certain privacy and can protect transaction information and user information.

3.2 Strict review system

Security is an important part of tokenizing real-world assets, especially when they serve as a source of collateral. It is important for issuers and investors in RWA to conduct due diligence on DeFi protocols and select technology or services that prioritize secured lending, offer strict regulatory compliance, and are built using high-quality open source code. For RWA-related project teams, it may be necessary to provide two necessary solutions:

Avoid KYC/AML Risks - Conduct KYC (Know Your Customer) or AML (Anti-Money Laundering) checks on users and/or transactions on the platform. Avoid potential interactions or transactions by users, directly or indirectly, with counterparties or politically exposed persons listed on OFAC and other sanctions lists.

Provide effective monitoring means - products and services that monitor and detect suspicious activities of DeFi users.

Therefore, the project needs to set up a dedicated compliance team to review and approve or deny user access to the platform based on customer identity, risk assessment, verification and due diligence. In addition, customer activity is continuously monitored for any suspicious activity or behavior that may suggest fraud or money laundering.

4 Representative project analysis

The RWA track has multiple subdivisions. This research report analyzes 19 representative RWA projects in detail from multiple dimensions such as RWA tokenization mechanism, protocol status, token function and performance, protocol advantages and risks. Through the analysis and summary of these projects, we can have a glimpse of the overall development, existing problems and future potential of the RWA project.

4.1 Concept of U.S. Debt

(1)MakerDAO

In 2020, MakerDAO officially included RWA in its strategic focus and released guidelines and plans for introducing RWA. In addition to issuing the stablecoin DAI, Maker has also expanded the types of collateral beyond ETH to include collateral in the form of tokenized real estate, invoices, and accounts receivable. The main source of income for the Maker protocol is the loan interest and liquidation penalties of the stable currency DAI.

Status of the agreement: From the perspective of TVL, Maker is the top three DeFi agreements, ranking behind Lido and AAVE, and is the first in the CDP (Collateralized Debt Position) agreement.

Currently only running on Ethereum, according to 2023-06-02, defillama shows, TVL is $6.29b, 30-day agreement revenue is $23.53m, treasury amount is $68.4m, governance token $MKR has been listed on Coinbase, Binance, Kucoin, Kraken, OKX, Huobi, Bybit, Gate and other mainstream exchanges have a 24h trading volume of $13.58m and a 30-day average trading volume of nearly $20m.

Token function : $MKR, as the governance token of MakerDAO, performed poorly. The main reason is that the protocol’s value capture ability is too weak, but governance has played an important role. The utility of $MKR token includes the following 4 aspects:

Governance rights : MKR token holders have governance rights over the MakerDAO system. They can participate in voting and make decisions on important matters such as system parameters, risk management measures and protocol changes. The voting results of token holders have an important impact on the development and operation of MakerDAO.

Collateral Stabilization : MKR tokens can be used as collateral in the MakerDAO system. When users generate stablecoins (such as DAI) by locking a certain amount of encrypted assets (such as Ethereum), they need to pay a certain amount of MKR as collateral. This mechanism is designed to ensure the stability and security of the system.

System Stability Buyback : The MKR tokens used as collateral are also used in the system stability buyback mechanism. When the value of the stablecoin DAI in the MakerDAO system drops and deviates from the anchor value with the US dollar, the system will automatically initiate the repurchase of MKR tokens and destroy them to stabilize the system.

Risk Sharing : MKR token holders bear the risk in the MakerDAO system. If the debt of the system cannot be repaid or other problems occur, the value of the MKR token may be affected. This gives MKR token holders an incentive to participate in and supervise the operation of the system, ensuring the security and stability of the system.

Agreement advantages :

1. Based on EVM and L2 ecology, it has a more loyal user group and stable and secure network support than other public chain RWA protocols;

2. The advantages of the system have gone through the test of the bull-bear cycle, including strict entry thresholds for collateral, coupled with over-collateralization and a perfect auction system, which can guarantee the 1:1 peg between DAI and the US dollar in most cases. In extreme cases, the agreement also sets emergency measures for emergency shutdown.

Agreement risks :

1. Governance attacks. The short-term large-scale convergent ownership of MKR tokens may lead to the concentration of governance power, which will lead to a series of governance attacks such as new garbage collateral, emergency shutdown, and malicious modification of risk parameters. As the value of MKR increases And the risk control measures of the protocol itself are sufficient to prevent such risks in most cases;

2. Market price risk. In the case of increased volatility of mainstream tokens, the serial agreement auction liquidation will actively increase the supply of tokens in the market and worsen market liquidity problems. Happened, but the agreement itself did not suffer large-scale losses.

(2)Ondo Finance

Ondo Finance was one of the most watched RWA projects in the first half of this year. In April, it received $20 million in Series A financing led by Founders Fund and Pantera Capital. Ondo Finance is a decentralized investment bank. Off-chain mainly invests in U.S.-listed currency funds. On-chain, it cooperates with Flux Finance to carry out on-chain stablecoin lending business, including USDC, FRAX, DAI, and USDT. The current average lending rate is about 5% . Agreement income comes from an annual management fee of 0.15%.

Users need to pass the KYC/AML process before they can trade fund tokens and use these fund tokens in licensed DeFi protocols. Ondo Finance has launched four tokenized bond products for investors to choose from, including:

U.S. money market fund (OMMF) : Ondo Money Market Funds invests in debt instruments such as high-credit U.S. government bonds and short-term bonds. The biggest goal is to preserve capital. The current annualized return is 4.5%.

U.S. Treasury Bonds (OUSG) : Ondo Short-Term US Government Bond Fund, investing in U.S. short-term bill ETFs, currently has an annualized rate of return of 4.85%, $100.87M TVL.

Short-Term Bond (OSTB) : Ondo Short-Term Investment Grade Bond Fund, an actively managed exchange-traded fund (ETF) designed to pursue maximum current income while ensuring capital preservation and daily liquidity. The ETF invests primarily in short-term investment-grade debt securities, with an average portfolio maturity typically no longer than one year, and currently has an annualized rate of return of 5.77%.

High-yield bonds (OHYG) : Ondo High Yield Corporate Bond Fund, which mainly invests in high-yield corporate bonds, currently has an annualized return of 7.9%.

Protocol status : TVL on ETH is $100.5m, defillama RWA ranks first. OUSG is used on the largest scale, and OUSG holders can also deposit into Flux Finance, a decentralized lending protocol developed by Ondo Finance, to obtain income. Tioga Capital investor Tzedonn mentioned in the latest report that the existing market value of bond tokens is $168 million, and Ondo (OUSG) has a 61% market share, of which 28% is deposited in Flux Finance. At present, the total supply of Flux Finance has exceeded 40 million US dollars, and the market value of OUSG has exceeded 100 million US dollars. The lending protocol FLUX has been sold to the Neptune Foundation.

Token functions : The functions of the governance token $ONDO include the following four,

Platform fee payment : When users conduct transactions, loans or other financial activities on the Ondo Finance platform, they may need to pay certain fees, which can be paid with Ondo Finance tokens.

Voting Rights and Governance : Holders of Ondo Finance tokens can participate in the governance and decision-making process of the platform. They can vote on matters such as platform upgrades, parameter adjustments, and approval of proposals, and express opinions and suggestions on the development direction of the platform.

Rewards and incentives : The Ondo Finance platform may attract users to participate in platform activities and ecological construction by issuing token rewards and incentives. These rewards can be issued in the form of Ondo Finance tokens to encourage users to contribute and support the development of the platform.

Lending and mortgage : On the Ondo Finance platform, users can use Ondo Finance tokens as collateral to obtain lending services. Users who hold Ondo Finance tokens can use them as collateral to obtain more borrowing lines or lower interest rates.

Advantages of the agreement : compliance, the products are either low-risk US government-related debt instruments or high-risk ETFs, all of which are compliant products with third-party accounting disclosures. At the same time, users also need to go through the KYC/AML process.

Agreement risks :

1. Risks outside the circle. The main products are off-chain ETFs, US government debt instruments, etc. Compliance can be guaranteed, but it will also bring market risks, credit risks, etc. outside the circle, especially the credit of high-risk companies such as OHYG. bonds;

2. Risk of going out of the circle. My current personal opinion is that the project is stripping off decentralized products and turning to a centralized + compliance operation. The use of governance tokens may be stripped and marginalized, and only blockchain technology will be used in the future. The purpose of Xiangfenrun + accounting + selling shares is not research and development in the direction of overall decentralization of the project, which is contrary to the purpose of most projects in the currency circle.

(3) Maple Finance

The Maple Finance protocol has been developed for 3 years, and its mainstream business is lending/institutional credit loans. The on-chain business provides USDC and wETH lending services, but an independent centralized pool manager manages the lending business, including lending objects, quotas, interest rates, strategies, etc. It seems that Maple Finance is not a qualified RWA project, but in April it announced plans to launch a lending pool for investing in US Treasury bonds, supporting non-US DAOs, offshore companies, etc. to invest restricted funds into the capital pool set up by Maple Finance.

Protocol revenue: Maple Finance’s revenue mainly comes from the following aspects :

Borrowing Fees : Maple Finance charges a borrowing fee by providing funds to borrowers. These fees are calculated based on the amount borrowed and the term of the loan, and are based on the interest rate setting of the borrowing pool.

Loan Fees : Maple Finance, as a platform provider, may charge fees associated with loan transactions. These fees can include loan application fees, lending fees, and loan settlement fees.

Token Mining Rewards : Maple Finance may issue rewards to participants through a token mining mechanism. Users who hold Maple tokens can earn rewards by providing liquidity or participating in lending pools.

Platform governance fees : As the manager of the lending and borrowing pool, Maple Finance may charge a certain percentage of platform governance fees. These fees are used to support and maintain the operation of the platform, including developing new features, conducting security audits, and maintaining community governance.

Agreement status : Looking at TVL, Maple Finance ranks 145 on defillama, but ranks first among unsecured loan agreements, with a total TVL of $48.56m, a total of $32.22m of debt in transit, a cumulative income of $45.6m, and 18 debts in transit (due to the provision It is a centralized credit-guaranteed debt, so the lending objects are all large institutions and the number is small), and there are 8 cash pools (7USDC+1ETH, the average 30-day return is 7% annualized). In addition, Maple Finance also has a small portion of TVL on Solana, but with the decrease in activity on the Solana chain, it currently only has about $16.4k TVL, and most (99%) of the TVL comes from the ETH main network.

Token function: MPL token is the native token of the Maple Finance platform and has the following functions :

Payment fees : MPL tokens can be used to pay fees for lending transactions on the Maple Finance platform. Users who hold MPL tokens may receive discounts or other benefits to encourage them to use and hold the tokens.

Community governance : MPL token holders can participate in the governance decisions of the Maple Finance platform. They can put forward proposals, vote and express their opinions, influencing the development direction and important decisions of the platform.

Voting rights : MPL token holders have certain rights in voting on the platform and can participate in voting on protocol parameters, protocol upgrades and other important matters.

Share dividends : Users holding MPL tokens are eligible to share the profits of the lending pool on the Maple Finance platform. These profits may come from interest paid by borrowers or other sources of income, and are distributed proportionally to users holding MPL tokens.

Incentive mechanism : The Maple Finance platform may promote the development of its ecosystem by providing incentives to MPL token holders. These incentives may include airdrops, rewards, or other forms of rewards to encourage user participation and support the growth of the platform.

Advantages of the protocol : There is a certain degree of security. The manager of the pool is responsible for the lending risk and charges a certain management fee in return. The liquidity provider can enjoy the lending interest rate and bear less default risk.

Agreement risk :

1. Credit risk. Lending pool managers and lending objects are all reviewed by centralized institutions, and debt mainly relies on credit mortgages rather than asset mortgages (the mortgaged assets come from the pool managers). Therefore, once a large-scale institutional default occurs, there may be Insolvency;

2. The threshold is too high. In order to ensure the safety of debts, the lending threshold is high and is not suitable for most users, so the community is not very popular.

4.2 TradFi

(1)Polytrade

Polytrade is a decentralized trade finance platform designed to provide seamless lending to businesses across multiple industries. Currently, the project is being transferred from V2 to V3. There has been no debt default since January 2022, and the LP loss is 0. It is expected that the NFT function of real assets will be added to V3, and there may be a secondary trading market for NFT in the future.

Current status of the agreement: The governance token TRADE has been listed on Kucoin, Gate, MEXC, Bitfinex and other exchanges. The main market is MEXC. Defillama shows that the TVL of the project is only $10,984, which is far from the fully unlocked market value of the project token of $17.27m and is overvalued. Risk, on March 30, 2023, the project raised $3.8m in seed financing from Polygon Studios, Matrix, CoinSwitch, Alpha Wave Global and other companies.

Token function: TRADE is the governance token of the project. Its main function is to vote and make decisions on protocol income and updates. More detailed disclosure of token functions may be disclosed after the release of V3.

Agreement advantages:

1. The transaction cost on the Polygon chain is lower, and the natural advantages of EVM such as gas and transaction speed;

2. Track advantage, officially funded by Polygon, is expected to ensure the competitive advantage on Polygon EVM.

Agreement risks:

1. Credit risk. Although lending transactions remain on-chain, the loan objects, business, review and other processes are all off-chain. The project party claims that the transactions are protected by institutions such as AIG and Mercury, but it cannot avoid breaches of contracts by offline entities;

2. Technical risk. The project is in the migration stage from V2 to V3. Currently, the protocol code does not provide a third-party audit report, and there may be bugs in unknown code technology.

(2) Defactor

Defactor aims to provide financing opportunities and liquidity to enterprises by connecting traditional financing with DeFi. The project is not yet online yet and is in its early stages. According to its roadmap, the second half of 2023 is still in the investment + recruitment + development stage. According to the project’s official website, $FACTR is the native token of the defactor ecosystem and aims to lower the threshold for using applications and infrastructure. It aligns interests and incentivizes ecosystem growth.

4.3 Borrowing

(1)Goldfinch

Goldfinch is a decentralized credit protocol for off-chain entities, debt funds and fintech companies, similar to Maple Finance. Goldfinch offers zero-collateral USDC line of credit loans. Goldfinch's model is much like a traditional financial bank, but with a decentralized pool of auditors, lenders and credit analysts. Borrowers can convert USDC into fiat currency and deploy it to end borrowers in the local market. Before borrowers can apply for a loan, they must get approval from the protocol’s decentralized auditors. Auditors are independent entities that must stake the governance token GFI to have the opportunity to verify borrowers in exchange for rewards.

Protocol income source: 10% of all interest payments by Goldfinch are retained in the protocol treasury. At the same time, users’ redemption from the premium pool will incur a 0.5% fee, which will also be deposited into the protocol treasury.

Current status of the agreement: Currently, the total outstanding principal amount of all loans in the Goldfinch agreement is $101.34 million, the total loss rate is 0%, and the total principal and interest that has been repaid is $25.1 million. In the past 30 days, the agreement generated revenue of US$100,100. There are no bad debts yet.

Token function: Goldfinch currently has two ERC20 native tokens, GFI and FIDU.

GFI is the core native token of Goldfinch and can be used for governance voting, auditor staking, auditor voting rewards, community grants, staking supporters, protocol rewards, and can be deposited into the member treasury to obtain member rewards to ensure the development of the protocol.

FIDU represents liquidity providers' deposits in premium pools. When liquidity providers provide funds to the advanced pool, they will receive equal amounts of FIDU. FIDU can be redeemed for USDC in the Goldfinch dApp at an exchange rate based on the premium pool’s net asset value, minus a 0.5% withdrawal fee. Over time, the exchange rate for FIDU increases as interest payments are added to the premium pool.

Advantages of the protocol: The mechanism adopted lowers the borrowing threshold, which can help users with lower credit ratings obtain loans to a certain extent. Compared with traditional platforms, Goldfinch is easier to use, and the process is basically handled by smart contracts.

Protocol risks: The adoption of DeFi is global, but different laws in different countries may lead to higher costs and problems in Goldfinch's business. Moreover, because there is no collateral, the Goldfinch senior pool also has default risk.

(2) Centrifuge

Centrifuge was launched in 2017 and is one of the first DeFi projects to get involved in RWA. It is also the technology provider behind head protocols such as MakerDAO and Aave. Similar to the above lending protocols, Centrifuge is also an on-chain credit ecosystem designed to provide small and medium-sized business owners with a way to mortgage their assets on the chain and obtain liquidity.

Centrifuge allows anyone to start an on-chain credit fund and create pools of collateralized loans. Centrifuge created Tinlake, an open asset pool based on smart contracts. Borrowers can tokenize physical assets through Tinlake. Physical collateral will be divided into two tokens, DROP and TIN, based on risk and return, representing fixed interest rates at the senior level and floating interest rates at the secondary level respectively. Investors can choose to invest in DROP or TIN based on their own risk tolerance and return expectations. Currently, there are no fees for the Centrifuge protocol.

Project status: On May 23, Centrifuge announced the launch of a new Centrifuge App to replace Tinlake. The new Centrifuge App improves the speed of KYC and investment participation, adds KYB (Know Your Business) process automation, and lays the foundation for subsequent multi-chain support. Previous Tinlake will be automatically migrated to the new application. According to official data, Centrifuge’s current TVL is US$201 million, with total financing assets reaching US$397 million.

Token function: Centrifuge Chain’s native token CFG is used as an on-chain governance mechanism, and CFG holders can manage the development of the Centrifuge protocol. At the same time, CFG is also used to pay Centrifuge Chain transaction fees.

Project advantages: 1. The financing threshold is low, while allowing investors to obtain income from real assets. Centrifuge basically simulates the corporate credit process in traditional finance; 2. Committed to compliance, Centrifuge is based on the legal structure of US asset securitization.

Project risk: Loan overdue default risk. According to rwa.xyz data, Centrifuge has US$10,194,481 in loans overdue for more than 90 days.

(3) Clearpool

Clearpool is a DeFi lending protocol that provides institutions with unsecured loans. Clearpool has two products, Prime and Permissionless. Clearpool Prime is only available to whitelisted institutions, and no collateral is required to borrow money on Prime. Borrowers create pools with specific terms in the core smart contract. Once the pool is created, the borrower can invite any other whitelisted institution to fund the pool. Loan assets are automatically transferred directly to the borrower's wallet address without the need for Clearpool to keep them. Clearpool Permissionless requires the borrower to be a whitelisted institution and has no requirements for the lender.

Agreement Income: Clearpool charges 5% of all interest payments as agreement fees.

Current status of the agreement: Clearpool has accumulated loans of US$398 million, with a current loan balance of US$16.58 million and a Permissionless TVL of US$20.78 million.

Token function: CPOOL is Clearpool’s utility token and governance token. CPOOL holders can vote on a whitelist of new borrowers.

Advantages of the protocol: The advantage of Clearpool is that it requires no collateral at all and the issuance of its loans only needs to go through the protocol itself, which greatly improves efficiency.

Protocol risks: Without collateral, Clearpool’s current whitelist and credit scoring mechanisms will be unable to prevent borrowers from defaulting once the market environment deteriorates.

4.4 Public Fixed Income

(1)Swarm Markets

Swarm Markets provides compliant DeFi infrastructure for RWA token issuance, liquidity and trading and is supervised by German regulators. Swarm Markets combines an on-chain compliance layer with regulatory clearance to tokenize US Treasury bills and stocks. SwarmX, the issuing entity, acquires publicly traded equity securities as the underlying assets for on-chain tokens, which are held by institutional custodians.

Protocol Revenue: Swarm will receive 25% of the pool exchange fee or 0.1% of the assets being exchanged (whichever is greater).

Agreement status: Swarm currently provides TSLA (Tesla), AAPL (Apple) stocks and TBONDS01 (iShares U.S. Treasury Bond 0-1 Year ETF), TBONDS13 (iShares U.S. Treasury Bond 1-3 Year ETF) bonds ETF. On April 25, Swarm officially announced that it will launch BLK (BlackRock), COIN (Coinbase), CPNG (Coupang), INTC (Intel), MSFT (Microsoft), MSTR (Micro Strategy), NVDA (NVIDIA) stock tokens .

Token function: $SMT is the native token of Swarm Markets and can enjoy trading discounts and rewards. When traders choose to pay with $SMT, they can get a 50% discount on the agreement fee. $SMT holders can enjoy loyalty rewards, and the specific ratio will vary according to different levels. Similar to the concept of centralized exchange platform currency.

Protocol advantages and risks: The advantage of Swarm is that it provides more choices for DeFi users, combining blockchain and traditional assets, and mixing TradFi and DeFi. Of course, Swarm currently offers fewer stocks and bonds, and its depth cannot be compared with traditional markets.

(2) Acquire.Fi

Acquire.Fi is a cryptocurrency M&A marketplace that simultaneously provides everyone with real-world gains from fractional stakes in cryptocurrency companies, traditional businesses, and real-world assets. In Acquire.Fi, equity will be NFTized and can be bought and sold through the secondary market. Sellers in the market, sellers, and buyers in the investment pool all need to pass KYC (subsequent, investments below $250 may not require KYC).

Protocol Income: Acquire.Fi uses multi-structured commissions. For business values below $700,000, the commission will be fixed at 15% of the sale price. Commissions will be reduced to 8% between $700,000 and $5 million. Commissions over $5 million will be further reduced to 2.5%.

Status of the agreement: Currently, the Acquire.Fi market provides equity sales for many companies including the NFT market, metaverse, media, DAO and other tracks. According to official statistics, 2k+ online business sales have been completed.

Token function: $ACQ is Acquire.Fi’s utility token. Staking $ACQ can enjoy an exclusive investment pool, encrypted M&A transaction flow, LP mining rewards and other exclusive advantages.

Advantages of the agreement: Using Acquire.Fi to sell your business online does not require the purchase of additional services or the need to contact a website host, and it can also gain higher attention. Compared with other platforms, it has the advantage of being more convenient and faster.

Agreement risks: There are still legal risks in conducting mergers and acquisitions or purchasing equity through Acquire.Fi, especially when the buyer and seller are not within the same legal entity.

4.5 Summary of financial products

Lending agreements are the most successful example of RWA projects. The unsecured lending model has been welcomed by institutions in the bull market, but it is also a catalyst for the arrival of the bear market, so the most difficult part of the credit agreement is the risk of default. Projects based on U.S. debt and U.S. stocks are relatively mature, and users can also obtain higher returns in a bear market. There are fewer TradFi projects, and the current business is still focused on financing for small and medium-sized enterprises.

The development space of institutional credit business is very limited. User income mainly comes from stable currency + protocol token. Moreover, due to insufficient mortgage, borrowers need to bear certain bad debt risks. In the bull market stage, the risk-free return of DeFi is also very high, so the institutional credit business may not be sustainable.

We believe that treasury bonds or currency funds similar to those launched by Ondo are potential directions in the future. First, these funds are already popular choices for investors in traditional finance and have low risks; second, they provide different options for users on the chain. At the same time, the threshold is lowered.

Although the RWA project in the financial field is in its early stages, there are already many interesting use cases. As the composability of each protocol increases, there may be many ways to play and high-yield projects. It is a segmented track worth looking forward to.

4.6 Real Estate Concept

(1) RealT

RealT is a real estate tokenization platform, established in 2019, mainly serving real estate projects in Detroit, Cleveland, Chicago, Toledo and Florida. Investors can purchase RWA tokens to realize real estate investment. To date, the platform has processed over $52 million in real estate tokenization for 970 homes.

There is no native ecological token in the agreement, and $DAI (XDAI/WXDAI) is used for value exchange within the ecology, and realtoken is issued for each real estate asset to obtain rent sharing as collateral.

Tokenization packaging process:

Off-chain: Through the third-party real estate management agency, according to the real estate contract, the ownership of the real estate is confirmed, and the rights and interests of members are divided into equal units; the rent of tenants is converted into US dollars through real estate management services. Legal support: RealToken submits documents to apply for securities exemptions in accordance with Regulation D and Regulation S of the US Securities Act, and RealToken shall not be provided or sold within the United States or for Americans or for the benefit of Americans.

On the chain: realtoken investors need to use the stablecoin DAI deposit and loan service of the RMM application (RealT market maker) in exchange for realtokens as collateral according to the price of the oracle, and the chain is sent to the realtoken related to the leasing contract in the form of DAI every day The total amount of digital wallet address is 1/30DAI for daily payment.

Agreement revenue: No specific revenue model found. Possible income comes from the interest rate difference between deposits and loans in the DAI capital pool, and off-chain and on-chain rents.

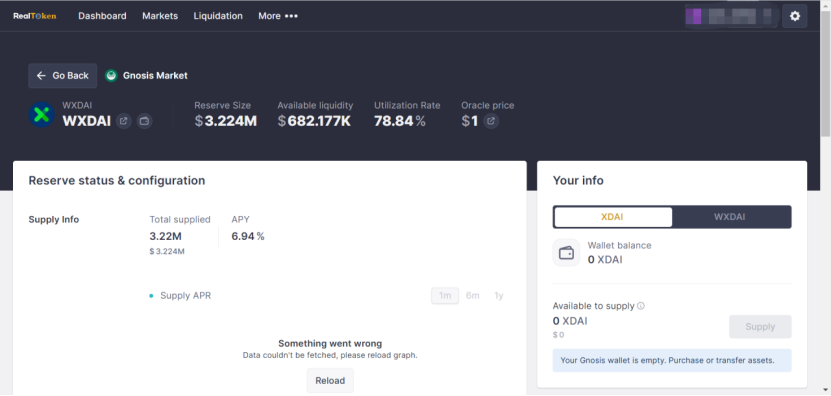

Current status of the agreement: The current agreement market size is $10.51m, the total supply of XDAI is $3.224m, the supply APY is 6.94%, the total borrowing is $2.54m, and the borrowing APY is 9.93%. There are currently 40+ properties available for investment on the market within the agreement.

User income status: There are 17 users with weekly rental income >1k DAI, and the highest income is 6187.83DAI/week.

Advantages of the protocol: Since its issuance in 2019, the protocol has maintained a market size of tens of millions of dollars and has sustained real cash flow income.

Agreement risk: Affected by the real estate rental market price and supply and demand, there is a difference between expected rental income and actual rental income.

(2) Tangible

Tangible is a RWA tokenization project that provides users with access to RWA tokenization by launching the native income stable currency Real USD. RWA physical goods include but are not limited to art, high-end wines, antiques, watches, and luxury goods.

Tokenization packaging process:

Off-chain: There are four tokenized product categories on the platform, including gold, wine, watches and real estate.

For the trading and storage of gold bars, Tangible uses the services of Swiss-based PX Precinox.

For wine, they work with London-based Bordeaux Index.

For the watches, they partnered with UK-based BQ Watches.

For real estate, Tangible creates native special purpose vehicles (SPVs). These are the legal entities established for each property. The SPV manages the property by finding tenants, collecting rent, or managing repairs. All properties are rented out and rental income is paid to TNFT holders in the form of USDC.

Legal support: Each property located in the UK has its own UK SPV. This is because real estate cannot be tokenized directly. However, legal entities can. Real estate TNFT holders have ownership rights in the SPV, which gives them beneficial ownership rights in the real estate. However, legal ownership of both remains with Tangible's legal entity, BTS TNFT Ltd, registered in the UK. Tangible also has an entity of the same name registered in the British Virgin Islands.

On-chain: Tangible launched Real USD (USDR), a native yield stablecoin backed by real estate. Users can use TNGBL or DAI to mint USDR at a 1:1 ratio. On Tangible, users can use USDR to purchase valuable physical goods, including but not limited to artwork, fine wine, antiques, watches, and luxury goods. When a user purchases RWA listed on Tangible, TNFT ("Tangible non-fungible token") will be minted, representing the physical object. Tangible will store physical items in a physical vault and send TNFT to the buyer’s wallet. TNFT can be transferred and traded freely.

Methods and liquidation mechanism to ensure over-collateralization rate:

If USDR's CR drops below 100%, half of the rental yield will be held in the USDR collateral vault. Therefore, daily rebalancing will be reduced by 50%. In other words, USDR holders will earn less interest until CR returns to 100%.

Vaults supporting USDR always hold a diverse mix of liquid assets for fast liquidation (such as DAI, protocol-owned liquidity, and TNGBL).

If all DAI and other reserves are exhausted, the real estate TNFT will be liquidated. In this case, the user will receive pDAI instead of real DAI. pDAI is an IOU Token that represents a claim to real DAI, which can be cashed out once liquidation is performed.

Protocol Income: Owners of TNFT are required to pay storage fees. For example, the storage fee for gold bars is 1% per year. When redeeming, transportation costs must be paid by the person redeeming the TNFT.

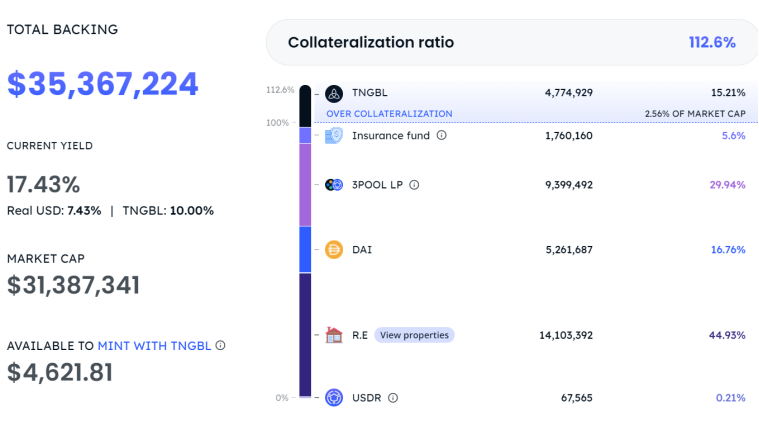

Current status of the agreement: Agreement TVL $33,665,846, total collateral price $35,367,224. According to the USDR white paper, the mortgage structure should theoretically be as follows: 50 - 80% tangible real estate; 20 - 30% tokens; 20 - 30% liquidity owned by the agreement; 5 - 10% insurance fund; 0 - 10% TNGBL. The actual USDR collateral structure is as follows, which is quite different from the proposed mortgage structure:

Token function: $TNGBL passively earns USDC after locking and minting NFT; used as a reward token to incentivize market use and subsidize USDR income; can be used to mint USDR.

Token secondary market performance:

$TNGBL is only circulated on uniswap and has not been supported by centralized exchanges. The liquidity is poor. The daily trading volume is mostly hundreds to thousands of dollars. The highest single-day trading volume in history is $32,000. The market value of the project is $110 million. Currency holding address 1,021.

Since its release at the end of March, the stablecoin USDR has been trading well. Multiple DEXs have been launched, supporting ETH, BSC, polygon, op, and arbitrum. The 30d average daily trading volume is $0.7m, the price is >$1, and the current price is $1.053.

Advantages of the protocol: Create a TNFT market and obtain a large number of circulating tokens to lock in. It also introduces the purchase of other physical commodities, including art, high-end wine, antiques, watches, luxury goods, etc.

Protocol risk: SDR de-anchoring risk. Centralized risk, the team is both the TNFT issuer and the custodian of the underlying assets.

(3) LABS Group

LABS Group was originally positioned as a real estate tokenization platform, allowing homeowners to tokenize their houses to raise funds without an intermediary, and investors can also access other real estate agents with higher liquidity through the secondary market. currency. Currently, LABS Group has launched a Web3 vacation platform Staynex, which provides members with access to global resorts every year and can earn rewards by holding membership. Tokenize "stay" through blockchain technology and embed it into NFT, so that hotels and resorts can create, design and mint their own timeshare plans on NFT. NFT represents membership status and number of days of stay .

Since it involves cross-border investment, LABS Group's exchange submitted a complete set of business plans to the government and received government approval. LABS Group has obtained a compliance license for retail investment.

Agreement income: LABS Group's primary platform, secondary exchange, and decentralized lending platform can obtain various business benefits such as consulting fees, transaction fees, listing fees, and handling fees.

Current status of the agreement: The resort industry is rich in resources, owns 60 hotels, and cooperates with Arsenal Football Club as its official hotel membership platform. At present, LABS Group is the best-performing project of real estate RWA track tokens. $LABS is supported by centralized exchanges such as kucoin, gate, and bitmart. It once broke through $35 million, and then the transaction popularity declined. In the past year, the single-day transaction volume was <$100,000, the market value was $1.47m, the FDV was $6.66m, and the number of currency-holding addresses on the chain was 11,911.

The community is very popular, with 58,000 followers on Twitter, 19k followers on Telegram, and 511 online users.

Token function: Mainly used as a reward token. Other functions include governance (voting). There is a repurchase and destruction mechanism, and 80% is planned to be destroyed, of which 50% is in the first phase. In addition, 10% of each transaction on the platform will be sent. Go to the liquidity pool for permanent locking. There have been phased staking activities before, such as staking $LABS for football match predictions (https://www.support2win.io/), but the activity has ended.

Advantages of the agreement: The timeshare model adopted, that is, a person's right to use a vacation property during a specific period of the year, is very popular in today's digital nomad culture. In addition, the team has its own resort industry resources, owns 60 hotels, and cooperates with Arsenal Football Club as its official hotel membership platform.

Protocol risk: Token value capture is poor, mainly used as rewards, and empowerment is mainly on NFT. And timeshares have their downsides: high annual management fees, difficult sales, unscrupulous players and scams.

summary

At present, the overall market size of real estate projects in RWA is very small, with insufficient liquidity and poor mechanism transparency. It requires the intervention of large centralized entities for endorsement and supervision. The acceptance of utility tokens issued by relevant protocols in the crypto market is generally poor. . The main reason is that physical assets need to be strictly regulated, and the project party also needs to perform complicated operations on the ownership of assets.

The tokenization of real estate can solve: 1. The cross-regional and real-time transactions of the blockchain can solve the problem of low liquidity of existing real estate; 2. The threshold is low, and retail investors can also invest in real estate globally and obtain profits. But the most difficult problem to solve in real estate tokenization is property certification and valuation. Certification determines the authenticity of property information, and valuation determines the price of loans and liquidations. The Tangible project has made bold attempts in these aspects: it uses the Chainlink oracle to price RWA tokens. The information of the oracle mainly comes from the prices provided by hometrack.com; in terms of real estate authenticity, Tangible uses a third-party auditor cooperation model to independently verify Property ownership. In these projects, we can see that before the real estate is put on the chain, third parties are still required to participate, including evaluation, finance, legal and other related institutions. These require process compliance and legal improvement.

4.7 Carbon credit concept

Carbon credits refer to the amount of carbon dioxide that an enterprise has reduced or neutralized through certification through the organization’s Verified Carbon Standard, similar to the “voluntary emission reductions (CCER)” in my country’s carbon trading system. .

(1) Toucan

Toucan Protocol is a protocol deployed on Polygon with the goal of converting carbon credits into tokens to promote carbon credit transactions using decentralized financial means and ultimately promote carbon neutrality. The carbon credits traded by Toucan Protocol come from the carbon offsets registered on Verra. Verra is a non-profit organization that registers carbon credits.

Tokenization packaging process:

Toucan's carbon stack consists of three modules: Carbon Bridge, Carbon Pools, and Toucan Registry.

Carbon Bridge

Anyone can bring their carbon credits on-chain through Carbon Bridge. Toucan only supports carbon credits withdrawn from the Verra registry, and Carbon Bridge is an irreversible one-way bridge.

(1) At the initial stage of bridging, an ERC721 NFT BatchNFT will be minted to represent a batch of carbon credits;

(2) Permanen