Aerodrome TVL is as high as US$196 million, accounting for "half" of the total TVL of the Base chain.

Written by: 0xMingyue Wu Blockchain Blockchain

As described in Aerodrome's official documentation: Aerodrome Finance is a next-generation AMM designed to serve as Base's central liquidity center, combining a powerful liquidity incentive engine, a voting locking governance model, and a friendly user experience [1]. Since the Aerodrome protocol was officially launched on August 31, the protocol has attracted nearly 200 million US dollars in TVL in just 24 hours, and its native token $AERO has an uncompounded annualized profit of liquid mining close to 1000% . According to data from Defillama on September 2, the total TVL of the Base chain on September 2 was 379 million US dollars, while the Aerodrome TVL was as high as 196 million US dollars, accounting for 51.7% of the total TVL of the Base chain, which can be said to occupy "half of the country" of Base. What is the "magic" mechanism that allows a Dex to achieve such great achievements in a short period of time? This article will start from Ve(3,3) (the core mechanism of Aerodrome) and introduce the core mechanism of Aerodrome, the origin of flywheel and its development prospects in a simple and easy-to-understand way.

1 Game Theory and Flywheel: Ve(3,3)

The Ve(3,3) mechanism originated from the Solidly protocol of Andre Cronje created by Fantom, but due to the flaws in the mechanism design of the protocol, it is close to a "failure" state. Velodrome, the largest Dex protocol currently in the Optimism chain, has improved the defects of the Solidly protocol, and Aerodrome has inherited the latest features of VelodromeV2. Aerodrome's core mechanism Ve(3,3) can be disassembled into two parts: Ve&(3,3). Ve comes from the veCRV model of Curve, and (3,3) comes from the 3v3 game of OlympusDAO. The combination of the two attempts to balance the holder and trader in the supply, bringing more agreement income to the projects (especially the initial projects) that join the Ve(3,3) agreement, and at the same time improving the lease liquidity. reward efficiency[2]. The ve and (3,3) mechanisms will be introduced respectively below.

1.1 veNFT, evolution of veCRV

ve is the abbreviation of Voting Escrow (voting escrow), which is the step of exchanging Curve's governance token CRV for VeCRV's pledged lockup to obtain more rewards as LP. Curve was first launched to strengthen the long-term token Incentives for holders.

In the Aerodrome protocol, there are two protocol tokens, 1) $AERO, 2) $veAERO, $AERO is the protocol token used by the protocol to reward liquidity providers, it is an ERC20 standard, lock$AERO can Get $veAERO; $veAERO is packaged in veNFT, which is the ERC721 (also known as NFT) standard. The amount of $veAERO obtained by locking is determined by the time of locking $AERO (following the linear correspondence). The longest lock-up time is 4 years, and you can get 1:1 ratio of -20232023202320232023 -5- , similarly, if you lock the warehouse for one year, you can only get 1/4 of the locked warehouse $AERO quantity. If the locked warehouse is very short (such as one week), you can only get the locked warehouse 1/208 of the $AERO quantity. After the lock-up time is over, the user can get back all the $AERO at the time of lock-up.

Aerodrome will emit a certain amount of $AERO every week, and holders of $veAERO will vote to decide which liquidity pool $AERO will be emitted to.

1.2 (3,3) game

(3,3) comes from OlympusDAO's (3,3) game theory (from Nash equilibrium theory), this term comes from the standard notation in game theory, used to describe an important feature of the game: the strategy of the game participants and payment. In this notation, the first number in parentheses indicates the number of strategies available to the first player (usually the actor), while the second number indicates the number of strategies available to the second player (usually the opponent). The number of strategies to choose from.

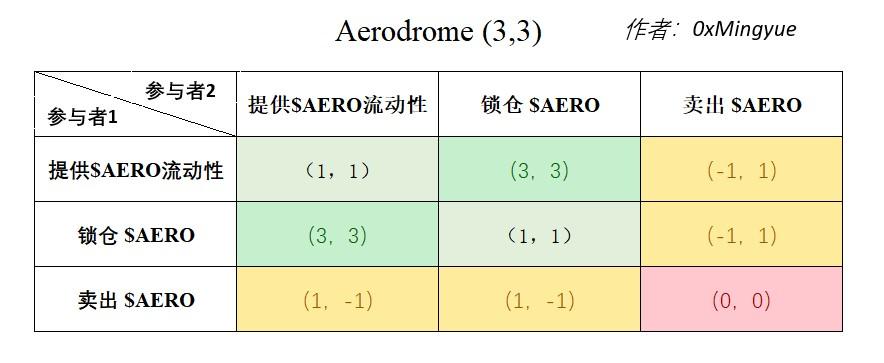

In the Aerodrome protocol, all protocol participants have three options for the $AERO they get, which are 1) provide $AERO liquidity; 2) lock $AERO and get $veAERO, Long-term holding; 3) Sell $AERO. In order to simplify the multi-agent game, the following figure lists the different behaviors of the two Aerodrome protocol participants and their rewards.

Figure 1.1 Aerodrome(3,3) game

The first number in brackets indicates the profit of participant 1, and the second number indicates the profit of participant 2. The larger the number, the more profit, and the negative number indicates the loss. The above picture is drawn according to the author's understanding and does not come from official documents.

As shown in Figure 1.1, based on the different actions of the two protocol participants on $AERO, there are a total of 9 possible results, which can be generally divided into 3 categories, namely: 1) Both parties Cooperation, lock the obtained $AERO or add $AERO liquidity to get more tokens; 2) One party does evil, that is, a protocol participant sells the $AERO it has obtained; 3) Both parties commit evil, a typical case of the "digging, selling and withdrawing" model. Both parties involved will sell the obtained -20232023202320232023-15 until the agreement is unprofitable. For result 1) both parties cooperate, both of them have made positive contributions to the agreement, they cooperate to increase the TVL and participation of the agreement, and together get more $AERO; for result 2) one party does evil, the perpetrator will be sold The short-term gains obtained by the tokens, while the protocol contributors (those who provide liquidity/lock positions) will realize losses; for result 3) both parties commit evil, all protocol participants participate in the protocol in the form of "mining, selling, and withdrawing", and the obtained Tokens are sold quickly, resulting in the value of the protocol quickly returning to zero. In Aerodrome, the “shovel” of mining (that is, the token used to provide liquidity) is usually the protocol-related token, which means that the protocol’s The interests of liquidity providers will also be lost when the value of the agreement returns to zero. Therefore, in the case of result 3) when both parties commit evil, the editor of this article believes that neither of them can benefit.

In reality, the real market is often formed by the joint efforts of countless protocol participants. Compared with the game of 2 protocol participants, its form is more complex. For almost all ve(3,3) protocols, especially some ve(3,3) protocols without background, due to the huge annualized income given to liquidity providers in the early stage, the result of market forces leads to the "mining of result 3) The "sell and raise" model is the most common. Only those "star" projects have gained sufficient market participation, and their equilibrium points will move with the help of external influences (various factors, such as market environment, funding, etc.) As for the result 1) cooperation between the two parties, this is also a dynamic balance that will change with the addition of new market participants.

1.3 Viewing Ve(3,3) Core Player Interest Game from Prisoner’s Dilemma

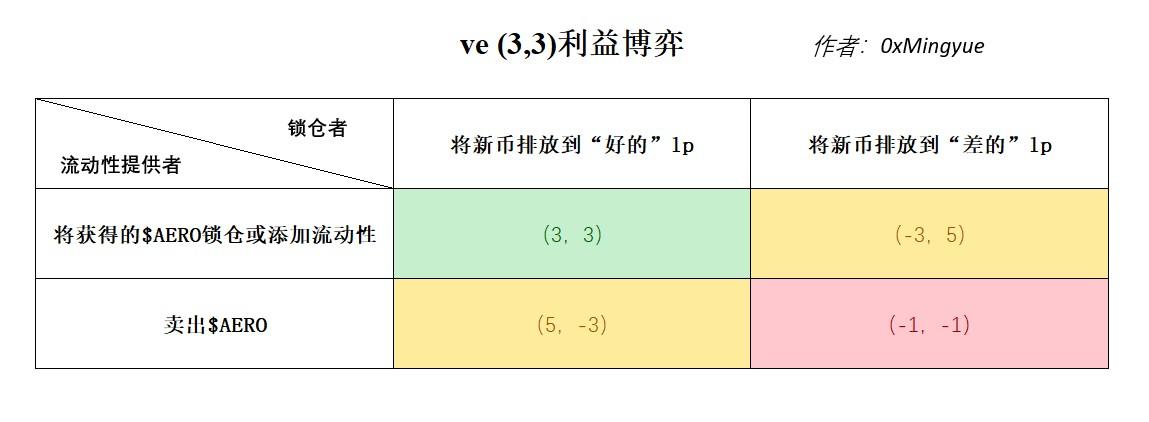

When a ve(3,3) protocol has proven its value in the short term and accumulated more lock-ups, the game has quietly changed. At this time, both liquidity providers and lock-ups have Upgraded to "stakeholders" of the protocol, for situations where multiple protocol participants form a complex market, in this section all core game members of the protocol are divided into two categories, namely 1) $AERO's liquidity provider; 2 )$AERO locker, long-term holder. The different behaviors of these two types of members will also determine the fate of the agreement, as shown in the figure below.

Figure 1.2 The Prisoner's Dilemma of Aerodrome Liquidity Providers and Lockers

The first number in the brackets represents the profit of participant 1, and the second number represents the profit of participant 2. The larger the number, the greater the profit, and the negative number represents the loss. The above picture is drawn according to the author's understanding and does not come from official documents.

As shown in Figure 1.2, the different behaviors of these two types of core participants will also lead to three types of completely different results: 1) win-win; 2) one party gains; 3) both lose. 1) Lockers cooperate with liquidity providers, and lockers will direct the newly emitted $AERO to those liquidity providers who make positive contributions to the protocol, and the liquidity providers will transfer the newly obtained $AERO Lock positions or continue to provide deeper liquidity, the protocol develops positively, the fundamentals improve, and both parties win-win; 2) The lock-up person or the liquidity provider does evil, such as the lock-up person will $AERO emissions lead to some evildoing MEME tokens, or the liquidity provider sells all the $AERO it obtained, which causes the perpetrators to make profits and the protocol value to return to zero for a long time; 3) Lockers or liquidity providers commit evil together, The fundamentals of the agreement will deteriorate rapidly, and the value of the agreement will quickly return to zero.

This kind of situation is similar to the "Prisoner's Dilemma". For a single liquidity provider or a lock-up person, the most rational choice an individual makes is to choose to do evil. At this time, the Nash equilibrium point [3] in the game is at The point where the loss of the entire system is the largest, and the equilibrium point is far from Pareto optimality [4].

How to break the "prisoner's dilemma"? From the perspective of stakeholders, the ve(3,3) protocol usually establishes a whitelist mechanism to prevent stakeholders from doing evil at the protocol level; from the perspective of liquidity providers, the protocol usually provides staking rewards for liquidity providers. When liquidity providers obtain more locked-up amounts and become the main force of lock-up players, the relationship between liquidity providers and lock-up players is no longer a zero-sum game. Liquidity providers will do this for their own benefit. The agreement makes a greater contribution, and at this time the Nash equilibrium point is transformed into the Pareto optimality where the agreement benefits the most.

2 The Flywheel in Action: Ascending Spirals and Death Spirals

The game theory of ve(3,3) is explained in detail above, so what is the "magic" that allows the Aerodrome protocol to absorb 200 million US dollars in TVL in just one day? In this section I will explain the Aerodrome's "flywheel" mechanism.

2.1 Flywheel effect and the mystery of gold absorption

The flywheel effect takes its name from the mechanical flywheel, a rotating device that becomes more difficult to stop or change direction as its rotational speed gradually increases. In business, this concept means that once a business or organization has established some competitive advantages, these advantages accumulate and strengthen like a spinning flywheel.

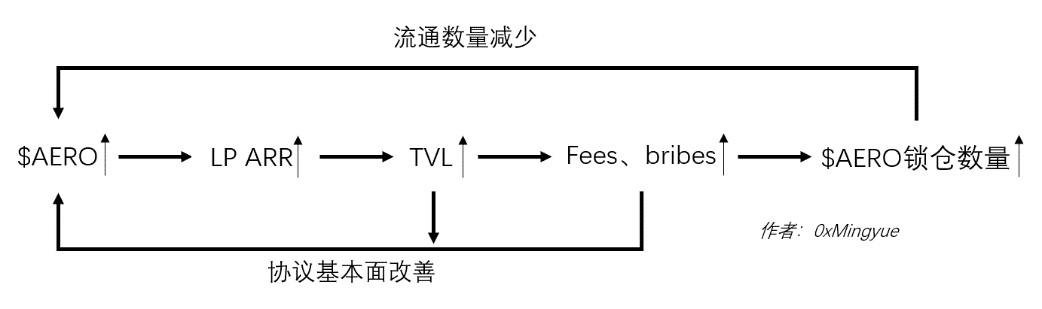

In Aerodrome, protocol fundamentals (TVL, trading volume, and total external protocol bribes) and protocol tokens $AERO form two levels of the flywheel. Imagine that when the price of the protocol token $AERO rises, the income obtained by the liquidity provider increases, and the liquidity provider will provide more liquidity; the liquidity is deeply optimized, the increase in trading volume leads to an increase in the protocol income, and more people Choose to lock up $AERO to obtain agreement benefits; the popularity of the agreement increases, and more external agreements participate in the operation of the agreement. And all of the above (fundamentals) will continue to push $AERO tokens to rise, and the value of the agreement will show an upward spiral, as shown in the figure below.

Figure 2.1 Aerodrome positive flywheel (price positive feedback)

When Aerodrome officially went live on August 31, the Aerodrome team contributed nearly 7% of $AERO emissions to the $AERO-USDC pool by controlling its $veAERO emissions. Due to the extremely small amount of $AERO circulating on August 31, when the first $AERO transaction was generated, $AERO was priced. At this time, due to the huge lp income and the extremely small lp pool, at At 8:01 on August 31, the lp APR (not APY, APR is annualized without compound interest) of the $AERO-USDC pool was once as high as 10,000% (this number is what the author saw, theoretically because of the very small pool and high rewards case, the APR can be higher), at this time due to the huge liquidity providing benefits triggering $AERO token scarcity, liquidity providers buy more $AERO providing liquidity, and thus promote- 20232023202320232023-30- The price rise, the price rise of $AERO promotes liquidity providers to obtain more income, and the positive flywheel is generated. In just one day on August 31, the Aerodrome protocol attracted $200 million TVL, accounting for half of the total locked value of the Base chain.

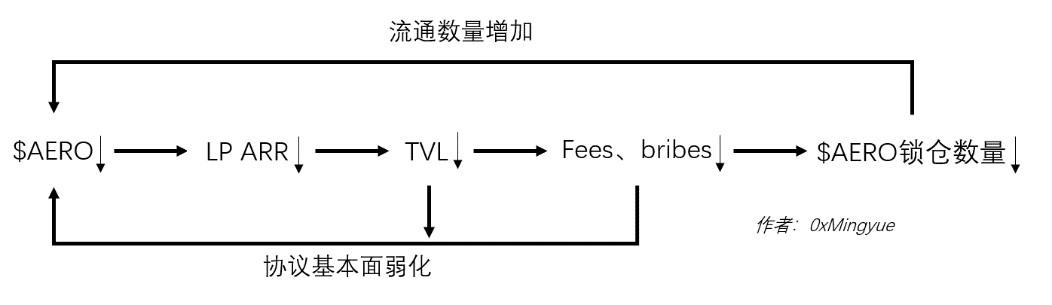

2.2 Ascending spiral and death spiral: how to break it?

When Aerodrome achieves an upward spiral, we may wish to think, when will this spiral end? We all know that money does not come out of thin air, so in this mining feast (obtaining $AERO rewards by providing liquidity), how will the money flow in the short term?

Due to the linear emission of $AERO tokens obtained by providing liquidity, the $AERO flowing in the market will gradually increase. When a critical point is reached, smart market participants will find that with $AERO- The depth of the USDC liquidity pool increased, and liquidity mining income was no longer profitable. At this time, this group of market participants chose to sell $AERO in their hands, which led to a decline in the price of $AERO , when the selling power and buying power reach a balanced state, the rising flywheel is broken, $AERO the price no longer rises, and the income of the $AERO-USDC liquidity pool no longer changes. As time goes by more $AERO is released, and when the selling power exceeds the buying power, the $AERO price will fall, followed by a downward spiral, as shown below.

Figure 2.2 Aerodrome Negative Flywheel (Price Positive Feedback)

There are many ve(3,3) tokens in the current market that are in a downward spiral. One representative is the CHRONOS protocol on Arbitrum, as shown below. Its project token $CHR is $1.81 higher than the opening high on May 4. It has fallen to the current price of $0.0168 in 4 months, a drop of 99%.

Figure 2.3 $CHR token price k-line chart

Although Aerodrome has a seemingly reliable team and a partnership with Base, its token $AERO may still be unable to escape into a downward spiral. How to break this downward spiral? In fact, Velodrome, Aerodrome's parent protocol, has already given an answer sheet, and the core of this answer sheet is to increase the lock-up rate and firmly bind the interests of the protocol participants to the development of the protocol. Since the Velodrome protocol was launched on June 1, 2022, with the outstanding business capabilities of the Velodrome team and the cumulative total of 7 million$OP tokens given by the Optimism Foundation, the protocol has made the protocol better by organizing various bonus activities According to Velodrome's official discord statistics [5], the lock-up rate of the agreement was still as high as 79.03% on September 2.

3 ve(3,3) development plan: resume the upward spiral

For the core health indicator of ve(3,3) tokens — lock-up rate, in this section we will discuss some ways to increase the lock-up rate and allow the protocol to resume its upward spiral.

3.1 Give lock-up rewards

It is the simplest and crudest way to give a one-time reward to protocol lockers when they lock their positions, just like what Velodrome has done. Since Velodrome went live in June 2022, the protocol has given funding to new protocol lockers through the Optimism Foundation Almost 15% of the lock-up returns. From the current point of view, Velodrome is successful. Its TVL in the optimism chain exceeds all star protocols, such as Uniswap and Curve.

3.2 Launchpad: Empowering lockers

When the author wondered why Binance Exchange did not list the tokens of such a star project Velodrome on the Optimism network in June this year, the co-founder of Velodrome surprised me with such a sentence in the discord — when some centralized When the exchange expressed its desire to list $Velo tokens and sought cooperation with the team, the team's reply was: We welcome you to list $Velo, but we will not provide support. At first I was very puzzled by the team's behavior, but then I figured it out: CEX's price manipulation often causes short-term speculators to flood into the agreement in large numbers, and they will not participate in any operations and games of the agreement. Just participating in price hype, and for ve(3,3) tokens, price hype is fatal —— price hype leads to an increase in circulating tokens and a decrease in locked positions, which makes the price fall from a high price after the price hype Entering a downward spiral often means the death of the protocol.

It also made me realize the grand narrative of the ve(3,3) protocol. The successful ve(3,3) agreement firmly holds the pricing power in the hands of the agreement, which can serve other agreements and act as another liquidity solution; it is a new type of Impermanent Loss compensation scheme, using agreement tokens to Give liquidity providers benefits; when the market environment is good, it will have a new currency listing place that rivals mainstream CEXs - Launchpad.

ve(3,3) provides certain protocol token rewards to liquidity providers, which makes ve(3,3) DEXs have the inherent ability to launch new coins —— new protocols do not need to hire any market makers For merchants, they only need to import ve(3,3) protocol rewards into their own token liquidity pool, and users will provide liquidity for the liquidity pool. And here, the ve(3,3) protocol can also use the Launchpad to empower lockers, thereby increasing the lock rate of the protocol and improving the health rate of the protocol.

4 Summary and outlook

This article starts from the ve(3,3) mechanism, and after briefly introducing the ve(3,3) game mechanism, introduces the inner principle of the upward spiral and downward spiral caused by the flywheel of this type of protocol, and then gives the solution to the downward spiral of the protocol. some methods. The vision of ve(3,3) is so grand, and different ve(3,3) protocols often make minor modifications to its mechanism. The author's energy and ability are limited, and there will inevitably be errors and incomplete descriptions in the article. Please also Readers give valuable comments.

I learned from different channels that there are still many ve(3,3) protocol participants who do not know how to participate in such agreements to maximize their benefits, and there are already many external protocols based on the ve(3,3) protocol Flourishing, such as Sonne finance, Tarot, Extra finance, fbomb, USDR, etc., the author still hopes to write an article on how these protocols have developed and grown based on the ve(3,3) protocol, and the development status of these protocols. Stay concerned!

refer to

[1] https://aerodrome.finance/docs

[2] https://www.oklink.com/academy/zh/2022/01/27/hot-ve33-curve-olympus/

[3] https://zh.wikipedia.org/wiki/%E7%BA%B3%E4%BB%80%E5%9D%87%E8%A1%A1

[4] https://zh.wikipedia.org/wiki/%E5%B8%95%E7%B4%AF%E6%89%98%E6%95%88%E7%8E%87

[5] https://discord.com/channels/967319632530767924/993229082538029187/1147532036328923286