Today

Intel

Market

Earn

Settings

Account

Theme Selection

Light

Dark

Language

English

简体中文

繁體中文

Tiếng Việt

한국어

Followin APP

Mine Web3 Possibilities

App Store

Google Play

Log in

Domingo_gou

92,646 Twitter followers

Follow

Posts

Domingo_gou

03-01

Thread

#Thread#

I've been checking the leaderboards these past few days and noticed my points are increasing incredibly slowly, only a few hundred a day. It might be due to incorrect tagging or poor posting timing. But since I can still submit, I'll keep writing and take it slow. Currently, I have 169K MP points, ranking 18th. This position is actually quite comfortable; I don't have to anxiously strive for higher rankings every day, nor am I blindly optimistic. It allows me to calmly observe more realistic aspects. Recently, I've noticed that this tiered points system, over time, might subtly alter everyone's actual financing costs. It's not just emotional speculation; this observation is becoming increasingly clear. @TermMaxFi's design was initially very clean: fixed interest rates, settlement at maturity, and a fully transparent Leaderboard—everyone sees the same interest rate curve. However, after participating for a while, you'll find that while the interest rates on the screen are the same, everyone's actual costs are not necessarily the same. The difference isn't in the contract terms, but in your position within the ecosystem. High-scoring users receive XP, MP, and various incentives, which, while not directly changing the borrowing rate, significantly reduce their net cost. New users see a 7% interest rate on a single loan, while existing users, including reward rebates, might only receive 6% or even less. The interest rate remains the same, but the real cost differs significantly due to tiered pricing. Going deeper, when a new market opens, those familiar with the rhythm can jump in immediately and reap the most favorable interest rate. Newcomers are still figuring out the rules, farming badges, and completing tasks; by the time they understand and enter, the curve has already changed. Within the same market, different entry orders naturally lead to different costs. There's also the information layer. Public leaderboards are inherently good—transparent and verifiable—but attention naturally gravitates towards those at the top. Those at the top are more likely to be seen, receive feedback, and anticipate market trends. Over time, this creates a compounding effect not on assets, but on position and perception. I think in a fixed-interest-rate market, interest rates can be the same, but position changes costs. This might be the most real long-term impact of a points system. Personally, I quite agree with #TermMax's direction. Fixed interest rates, structured liquidity, and RWA collateral are all pushing on-chain lending towards a more mature market. However, the more mature it becomes, the more we need to address the question of whether ordinary users will still be able to access the same favorable financing conditions if incentives are consistently concentrated at the top. It's not about weakening the strong, but about ensuring a place for newcomers. For example, creating a cold start pool for new users, giving special weight to the first few real loans, or using referral bonuses that gradually diminish. These aren't complex; they simply level the playing field and allow more people to truly participate. What do you think? In the long run, will the points system mean that only a few people in DeFi can access the optimal financing costs? Feel free to share your observations. 👉app.termmax.ts.finance/alpha/c...… #TermMax #DeFi #Oracle #RiskManagement #BNBChain #ProjectResearch #DYOR This tweet is not investment advice. Cryptocurrency is risky; invest with caution! twitter.com/Domingo_gou/status...

BNB

0.58%

Domingo_gou

02-27

Thread

#Thread#

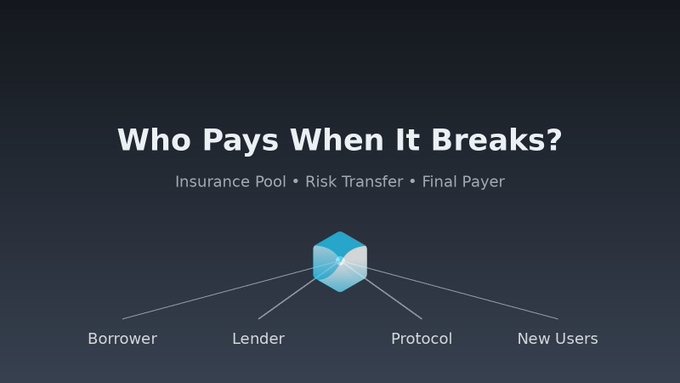

The proposed bad debt insurance pool raises the question: if a crisis occurs, who will be left holding the bag? Recently, the atmosphere on Twitter has been somewhat somber. Market volatility, tightening liquidity—everyone is contemplating a solution. On this stage, some are anxious, some are numb, and some have given up. Humans are actually quite fragile; the body only needs a little energy to survive, but what's truly difficult to settle is your—corrupted soul. We used to discuss returns; now, more people are discussing who will bail us out if things go wrong. After working in DeFi for a while, you'll find that what truly determines your long-term survival is never the annualized return. It's who, when bad debts occur in the system, is ultimately footing the bill. @TermMaxFi's recently recurring discussion about insurance pools is actually focused on this point. It's not a new approach; it's an endgame question. 1. First, clarify the current risk hierarchy. TermMax's risk path is currently clear and traceable. Fixed-rate lending + maturity structure: When pressure arises, the collateral bears the risk first, then liquidation waterfall occurs. Only in extreme cases is physical delivery and time-lock buffering triggered. The order is simple: Borrowers bear the risk first, then collateral assets, then market liquidity, and finally the agreement layer. In other words, the risk is not hidden, but layered and placed in different locations. 2. If an insurance pool is added, the risk will not disappear, but will only be redistributed. The role of the insurance pool is to smooth out extreme situations, but it will not create safety out of thin air. It only changes who bears the risk last. Different sources of funds lead to completely different results: From borrowers → increased borrowing costs From lenders → diluted actual returns From the agreement treasury → using future growth as a safety net From new users → postponing and transferring historical risks. The insurance pool itself is neutral; the key is where the money comes from. 3. A frequently overlooked detail: Risk is transferred, not eliminated. Once an insurance pool exists, the risk in the system begins to migrate. From explicit losses to implicit sharing, From individual positions to collective sharing. Many traditional financial products operate this way: They appear more stable on the surface, but long-term returns are gradually eroded. The advantage of the on-chain world is inherent transparency. Therefore, who provides the funds and who bears the consequences must be clearly stated on the chain. 4. If an insurance pool is indeed introduced in the future, at least three things must be recalculated: Triggering conditions: Must be verifiable on the chain, not subjectively determined. Payment order: Is it intervention before liquidation or a last-minute guarantee after liquidation? These two designs are completely different. Where does the funding come from? Is it continuously injected? Will it be misappropriated? All of these must be traceable. 5. A statement I've been pondering recently: The maturity of a protocol isn't determined by the level of returns. It's determined by whether each participant knows their position in advance when the system incurs losses. 6. Why this kind of discussion is important: Many projects avoid the endgame issue, but systems that truly want to exist long-term must face it. When a protocol begins to publicly discuss who will ultimately pay the price, it means it has moved from focusing on returns to pricing risk. This step is difficult but necessary. This is also why I've recently been seriously revisiting #TermMax. #ProjectResearch This tweet does not constitute any investment advice. Cryptocurrency involves risk; invest with caution! twitter.com/Domingo_gou/status...

Domingo_gou

02-25

Thread

#Thread#

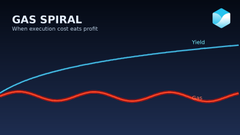

I seriously did the math on TermMax's Badge tasks last night. I went through @TermMaxFi's task page again last night, not to climb the leaderboard, but just to figure out what these Badges actually generate. I treated each task as a small investment, and after calculating, I felt much calmer. Now, before doing a task, I only look at the real cost of earning 1 point. How long is the capital tied up? How many on-chain operations are involved? What are the gas and slippage costs? Is the position exposed during this period? Adding all of that up and dividing by the XP or AP earned, there's only one result left—very clean. I actually did the calculations yesterday. A typical Badge path, including entry, exit, and holding, involves about five on-chain actions. Gas and slippage add up to nearly 1u, and the capital is tied up for three days. Only at the end did I realize that every point actually has a price, but nobody usually writes it down carefully. The easiest thing to overlook is time. Once the capital enters the task cycle, it's locked up. When the market moves, you can only watch. This isn't a loss, but it definitely exists. Add to that the slight fluctuation window, and the cost becomes even more realistic. I'm increasingly certain that on #TermMax, points aren't rewards; they're a costly entry ticket. You spend gas, time, and bear some volatility, and what you get in return isn't points, but your place in the system. So if you're hesitant about continuing to do tasks, don't look at how much others are earning. First, figure out your own costs and benefits. If you still want to stay after figuring it out, then continue. It's not about getting freebies; it's about choosing your own path. #ProjectResearch This post is not investment advice. Cryptocurrency is risky; invest with caution! twitter.com/Domingo_gou/status...

XP

1.34%

Domingo_gou

02-24

Thread

#Thread#

Don't rush to celebrate on the TermMax Hot List; first separate contribution from action. These days, browsing the @TermMaxFi leaderboard, I've had a very noticeable feeling: some scores rise very quickly, but it's not easy to explain why they're rising. So now when I look at the Hot List, I don't look at the rankings first; I only look at whether it's long-term value or short-term action. I generally only look at whether the transactions resemble genuine demand, whether the interaction spreads naturally, and whether there's retention after the window closes. If any of these don't match, even a high score is questionable. Many strong trends are actually not difficult to identify, such as small, high-frequency repetitive transactions, large nominal volume but low real cost, simultaneous actions across multiple wallets, a surge before settlement followed by a drop to zero, and dense content without new information. These are more like actions driven by incentives, not necessarily genuine contributions. Therefore, I increasingly recognize the value of the Hot List: it's not about who's number one, but about whose growth can be clearly explained. Only those who can explain it clearly will stay. If your score hasn't been moving much lately, don't rush to post more. First, ensure that each piece of content has a record, new information, and clear boundaries. It's okay to be slow; your real score will catch up eventually. #TermMax #InvestmentResearchProject This tweet does not constitute any investment advice. Cryptocurrency carries risks; invest with caution. twitter.com/Domingo_gou/status...

Domingo_gou

02-14

Thread

#Thread#

Tonight, while browsing the TermMax leaderboard, MP jumped a bit. I thought someone had overcharged, but the announcement said the X API missed a capture and they're now adding back the history. MP can be added back, but TVL can't. Points can be manipulated at will, and fund growth is fake. This round of XP was all distributed. The rules were simple: sign in for a few days and add some balance to get it. It mainly bought users; funds barely came in. The calculation is just three lines: Points: How much XP/MP/AP was burned today? Check the leaderboard; this is the cost. Funds: TVL 27m, ETH 25m, BSC only 1.5m. The entry point is clearly BSC, but all the money is in ETH; it hasn't been migrated in. Total TVL growth is fake. Usage: Only 2m was lent out, accounting for 7%. Fees are 0 per day; only a few thousand dollars in 30 days. Still building the framework; not really making money. These three lines clearly show the truth: only the money left after the XP→rTVL activity counts as growth; the rest is traffic. The community shouldn't keep asking if TVL has increased; they should be asking about the net increase in BSC and whether anyone has migrated to the mainnet. If no one has migrated, the growth is fake. The official response of supplementing MP is just a way to correct the narrative. I directly suggest @TermMaxFi release daily tables showing the increase in points, TVL changes by chain, and changes in lending, with a note on how much is being added. If they dare to release these, everyone can only reconcile the accounts. TermMax's most valuable asset is genuine retention. It's not how much is issued, but how much is retained; it's not hype, it's efficiency. If they continue to issue massive amounts without considering retention in the next round, the funds will run out, and they won't say they weren't warned. Fixed-rate platforms are most vulnerable to users leaving and tables empty. Have your opinions? Let's debate. 👉app.termmax.ts.finance/borrow?...… #TermMax #Mindshare #BNBChain #DeFi #TMX twitter.com/Domingo_gou/status...

XP

1.34%

Domingo_gou

01-25

Thread

#Thread#

Today I received the OKX Influencer Award from OKX, along with a 10,000u airdrop of strategy grid trading funds. First, thank you @okxchinese, and thank you to the strategy trading product, which allows an ordinary, clumsy user like myself, to make more rational decisions in the market. This award was actually quite unexpected for me. I'm not a high-frequency trader; I rely more on strategies, leaving my emotions to the system and dedicating time to reflection. I also want to especially thank the OKX Influencer Program. I gradually joined through the Influencer Program. The Influencer Planet is very important to me; it made me feel for the first time that my dedicated content creation was seen and respected by the platform. I also want to say on behalf of many creators like myself: we may not be very vocal, but we are truly using, writing, and participating long-term. I hope that in the future, OKX can continue to provide more opportunities for ordinary people, creators, and long-term thinkers to grow together. Thank you again, OKX, and thank you to the Influencer Program! Thank you everyone. #okx #OKXNewYear'sEveDinner #okxExpert #okxStrategyTrading twitter.com/Domingo_gou/status...

Domingo_gou

01-16

Thread

#Thread#

Is the “post-to-earn InfoFi” era really over? I don’t quite buy that. But it has changed. Today, X dropped an official announcement. And honestly, my first reaction wasn’t panic. It was relief. Is the post-to-earn InfoFi era finished? Maybe not. It feels more like this: one big whale sinks, and the water finally clears. Less surface noise. More movement underneath. Let’s be real for a second. Grinding posts every single day is exhausting. Chasing topics, timing replies, forcing output just to stay eligible. This almost feels like permission to pause. To stop posting just because you “should.” To breathe, reset, recalibrate. 1 | X isn’t killing InfoFi. It’s cutting off oxygen to noise. X was very direct. Apps that reward users simply for posting are no longer allowed. The reason isn’t ideological. It’s practical. AI templates. Copy-paste replies. Mass-produced content. The timeline got so crowded that real conversations were suffocating. This isn’t a culture war. It’s a platform trying to save its own usability. And if we’re honest, we’ve all felt how unreadable the feed had become. 2 | Snaps and Yaps didn’t “fail.” They reached the end of this chapter. I went back and reread the announcement from Cookie3. The tone around shutting down Snaps was restrained. Almost heavy. No buzzwords. No fake optimism. Just an acknowledgment: this version of InfoFi, at this moment, wasn’t sustainable anymore. What mattered more was what didn’t stop: -the data layer remains -200+ enterprise clients are still there -CookiePro is still moving toward launch That doesn’t look like retreat. It looks like protecting the core. 3 | Kaito said something uncomfortable, but honest. The takeaway from Kaito was surprisingly clear-headed. Permissionless reward distribution doesn’t really work under today’s algorithms. Not because they didn’t try. They raised thresholds. Tightened filters. Combined social and on-chain signals. But reality is stubborn: if rewards don’t discriminate, content will always slide toward the lowest possible effort. So Yaps winds down. Studio steps in. More like traditional marketing, but layered with analytics, intent, and cross-platform reach. Not romantic. But deliberate. 4 | What disappeared isn’t InfoFi. It’s the illusion that attention is cheap. A lot of frustration right now isn’t philosophical. It’s emotional. For a while, participation alone felt enough. Post something, anything, and value showed up. That was a subsidy phase. Not a permanent state. There’s a line I keep coming back to, worth bookmarking: Once attention is priced seriously, noise is always the first thing to leave. That doesn’t mean everyone wins. It means attention and value stop drifting apart. 5 | There’s a cost. But the direction is clearer. This shift isn’t painless. Smaller creators will struggle more. “High quality” may become narrowly defined. Influence could reconsolidate. Those risks are real. But so is the other side: projects no longer paying for empty impressions, and people who can actually explain products, mechanisms, and judgment becoming rarer again. Final thought So no, I don’t think InfoFi is dead. What’s gone is the illusion built on volume alone. What remains will be slower. Quieter. Harder. And much closer to something sustainable. Maybe this is the real signal: you don’t have to post every day. You don’t have to chase every wave. Find your rhythm again. Then decide which words are actually worth putting on the timeline. Would you rather pause, or keep going differently? twitter.com/Domingo_gou/status...

OXY

4.81%

Loading..