Tria is publicly building its first self-custodied new bank (Neobank): we're sharing its operating mechanisms, growth strategies, and upcoming product plans. This report is a retrospective of the landmark year 2025 and a record of Tria's system performance as it enters its next phase of growth.

Why publish this article?

Tria is building a new self-custodial bank designed for everyday use. From the beginning, our view has been simple: trust stems from clarity and consistency.

As Tria has grown, more and more users, partners, and infrastructure reviewers have asked the same questions: How exactly does the system work? What is it like in actual use? As the product scales up, how are decisions made?

This article is a snapshot of Tria's current operations. We showcase what we've built, our data performance, the experience gained delivering products in real-world environments, and our priorities going forward. We're publishing this because transparent disclosure is crucial for assessing the value of financial infrastructure as it scales. This is our first public transparency update, and we plan to make it a regular practice.

Our construction results

Tria's architecture revolves around a set of core product principles that guide all decisions regarding product, operations, and growth:

Self-managed by default: Users retain control over their assets at all times, including during consumption.

Everyday usability: Holding, consuming, and transferring value are completed in a continuous process.

Native Global: Designed for regions where digital dollars and on-chain rails have become part of everyday financial life, it currently supports use in more than 150 countries worldwide.

Cost transparency: Fees and routing are clear and transparent, with no hidden exchange rates or bundled interest rate spreads. Bank card spending enjoys Tria's 0% transaction fee.

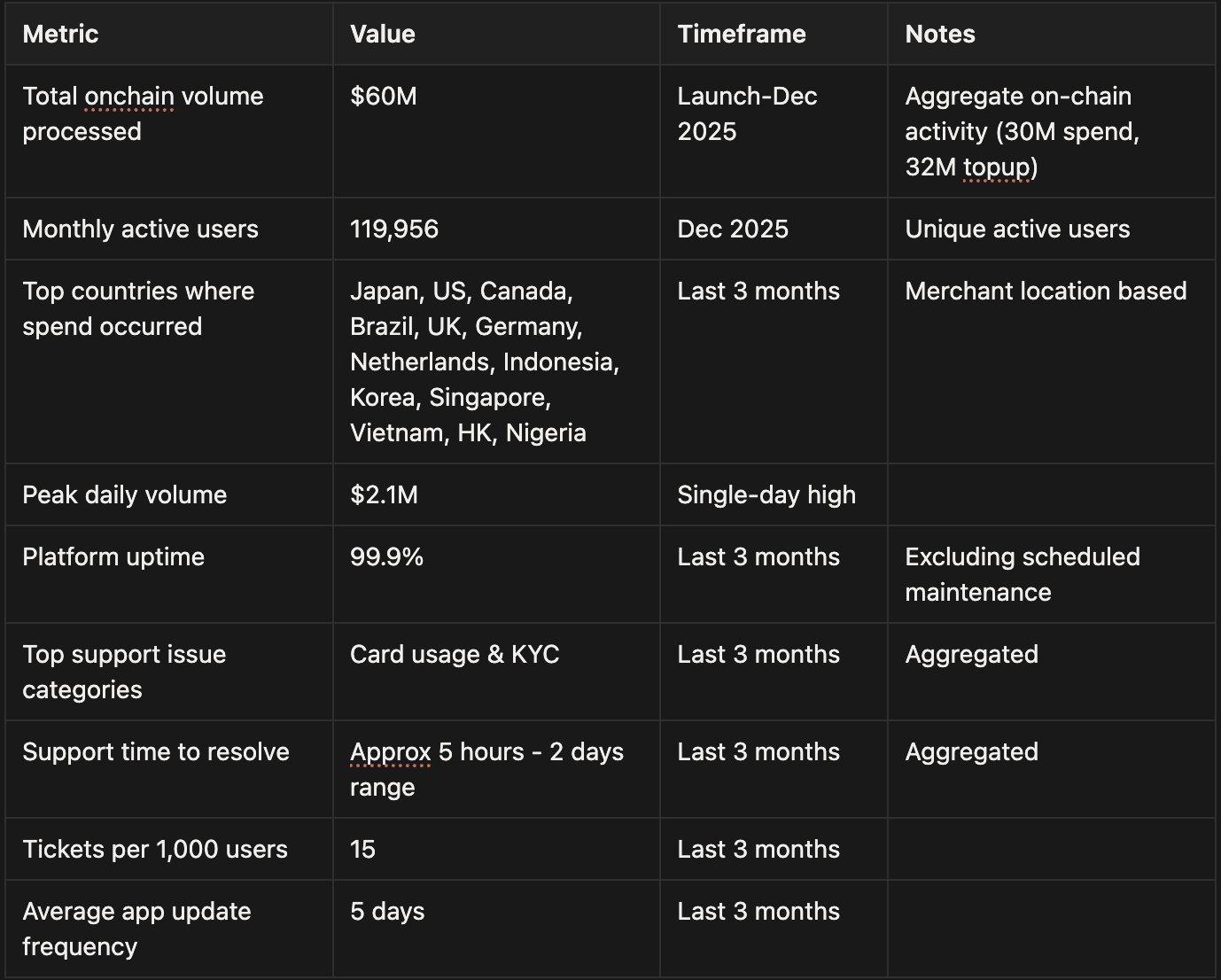

Key data

We selectively share or collect metrics. We only publish data that we believe can be referenced, tracked, and compared over the long term. In the first three months of closed beta testing, Tria became the fastest-growing new self-custodian bank.

All data below has been aggregated and rounded, and is sourced from Tria's internal analytics and support systems. These metrics are published to demonstrate operational transparency.

Note: Rounding is used to avoid a false sense of precision; data is sourced from Tria's internal systems. Future updates will include simple trend charts to illustrate the evolution of these indicators.

Our lessons learned

We view product development and growth as a series of experiments. Each experiment follows the same cycle: hypothesis, observation, adjustment.

1. Self-hosting is a core concern for users.

Assumption: Self-hosting is conceptually understood, but it is not a decisive factor for most users.

Observation: Users want to know where their funds are stored, what will happen if there is a failure, and who will bear the risk if the infrastructure is disrupted.

Adjustment: We have clearly and consistently defined the hosting boundaries in our products, support processes, and documentation.

Conclusion: Tria does not hold user funds in custody. Private keys remain under user control at all times. Tria's infrastructure only handles routing, execution, and card settlement logic. If Tria's infrastructure becomes unavailable, user funds remain on-chain and are recoverable. We anticipate that as on-chain finance usage grows, clarity regarding self-custody and liability boundaries will become increasingly important in 2026.

2. Cash rebates are not a universally applicable incentive.

Hypothesis: Credit card rewards will be the main driver of increased engagement.

Observation: In many regions, users value asset preservation and balance growth more than consumption-based rewards.

Adjustment: We have accelerated the development of savings and income-generating products while keeping the card reward mechanism simple and clear.

3. Holding BTC does not equate to spending BTC.

Assumption: Most BTC holders already have convenient ways to spend their money.

Observation: Many users hold BTC for the long term, but lack an easy path from storage to daily use.

Adjustment: We have added support for BTC top-up Tria cards, reducing friction between holding and spending.

4. Transaction history is not a secondary feature.

Assumption: Users are primarily concerned with their balance and whether the payment was successful.

Observation: In markets with complex reporting requirements, transaction history has become a core workflow. Japanese users, in particular, rely heavily on export functions for record saving and account reconciliation.

Adjustments: We have expanded export options and optimized access to transaction records, prioritizing clarity and completeness.

How do we enter new markets?

Market expansion follows a fixed operational checklist. We don't take shortcuts:

Verify spontaneous demand signals.

Simulate unit economic benefits and long-term sustainability.

Review local regulatory and compliance requirements.

Assess the readiness of partners and infrastructure.

Enable country support within the app.

Released to a limited testing group.

Scaling up will only begin after reliability and support quality have been verified.

We take compliance and user safety seriously. We review local requirements before each promotion. We avoid using misleading language that might imply that approval has not been obtained.

How do we support users?

Operational resilience includes the ability to handle problems.

Event definition: An event that affects transaction execution, routing, or card settlement. On-chain asset damage is handled separately from infrastructure events.

Internal escalation: Issues are immediately tiered and escalated to the engineering and operations departments based on their severity.

User communication: When an event affects functionality, users will be notified promptly, and clear status updates will be provided until the issue is resolved.

Post-mortem analysis: Root cause analysis will directly contribute to product and operational improvements.

As part of the reliability report, future transparency updates will include event metrics and summaries.

Next steps

Key areas of focus recently include:

We will continue to introduce savings and income-related features.

Publicly disclose the product changelog.

Monthly transparency updates and quarterly operational reviews.

Small, focused user feedback groups.

Regular AMAs and text updates are conducted on the community channel.

Note: All forward-looking projects are plans, not guarantees.

Conclusion

This article is part of Tria's ongoing "open build" effort. We will continue to share how the system works, changes, and data performance. If you would like us to explore certain areas in more depth, please reply to this post or join our upcoming Space on "Transparency and Market Execution."