One of the most significant changes in the crypto market over the past two years has not been a new public blockchain or a trending narrative, but rather the slow but steady migration of derivatives trading from centralized exchanges to on-chain transactions. In this process, Perpetual DEXs have gradually grown from an experimental product into one of the most valuable sectors within the DeFi ecosystem.

Article author and source: MarsBit

If spot trading is the starting point of DeFi, then perpetual contracts are becoming its true "cash flow core".

1. Why did Perp DEX rise to prominence?

In the traditional crypto trading system, perpetual contracts have long been the most important source of profit for centralized exchanges (CEXs). Whether it's transaction fees, funding rates, or the additional revenue from liquidation, CEXs practically monopolize the entire derivatives cash flow. For DeFi, this isn't a question of "whether they want to do it," but rather "whether they have the capability to do it."

Early DeFi lacked the fundamental conditions to support perpetual contracts. Insufficient on-chain performance led to high transaction latency, expensive gas costs, and infrequent price oracle updates, making any leveraged product vulnerable to arbitrageurs. Even attempts to leverage it struggled to compete with centralized exchanges (CEXs) in terms of user experience and risk control.

The real turning point came after the infrastructure matured. The widespread adoption of Layer 2 and the emergence of high-performance public chains significantly improved on-chain transaction throughput and latency; next-generation oracle systems were able to provide faster and more stable price data; and DeFi users, having weathered multiple cycles, were no longer just "mining users" but were gradually evolving into market participants with professional trading capabilities.

More importantly, the crisis of trust in centralized exchanges became the final straw. Asset freezes, misappropriation risks, and regulatory uncertainty have led more and more high-frequency traders and large funds to re-evaluate the costs of "custody." Against this backdrop, Perp DEX offers a new possibility: regaining control of asset ownership without sacrificing leverage and liquidity.

In essence, the rise of Perp DEX represents a redistribution of derivatives profits from centralized institutions to on-chain users.

2. Why are perpetual contracts the most suitable form of DeFi derivatives?

Among all derivatives, perpetual contracts are almost tailor-made for DeFi. Compared to futures contracts, they have no expiration date and do not require frequent rollovers; compared to options, they have a simple structure and intuitive pricing, allowing users to determine direction and leverage without needing to understand complex Greeks or volatility models.

More importantly, perpetual contracts offer extremely high trading frequency. They are not "event-driven" products, but rather infrastructure that continuously generates trading demand. This is crucial for any protocol that relies on transaction fees and liquidity.

This is why almost all successful Perp DEXs design their products around the same goal: to make trading as frequent as possible while keeping transaction costs as low as possible. Whether it's by reducing slippage, minimizing latency, or optimizing clearing efficiency, the ultimate aim is to attract more professional traders to stay on-chain long-term.

3. What problem does Perp DEX actually solve?

Many people simply understand Perp DEX as a "decentralized version of CEX," but this actually underestimates its significance. Perp DEX is not replicating centralized exchanges, but rather reconstructing the underlying logic of derivatives trading.

First, there's the change in the trust model. In Perp DEX, user funds are always held in custody by smart contracts, and the protocol itself cannot arbitrarily misappropriate assets. Risk exposure, margin, and liquidation logic are all publicly verifiable, meaning traders no longer need to "trust" the platform's risk control; they can directly audit the rules themselves.

Secondly, there's the transparency of risk pricing. Centralized exchanges' liquidation, markup prices, and funding rates are essentially black-box mechanisms. On-chain, however, these parameters are explicitly defined by contracts, allowing anyone to see how the market is liquidated and rebalanced.

Finally, there's the change in revenue distribution. Perp DEX doesn't concentrate all trading profits at the platform level. Instead, it returns the cash flow generated by derivatives to on-chain participants through LPs, Vaults, governance tokens, and other means. This makes users both traders and potential "shareholders" of the protocol.

From this perspective, Perp DEX is more like an on-chain risk management system than just a trading front-end.

4. How does the core mechanism of Perp DEX work?

From a mechanistic perspective, the evolution of Perp DEX has undergone a clear process of specialization. Early protocols mostly adopted the vAMM model, using virtual liquidity pools to solve the problem of liquidity cold start. However, this approach is prone to slippage under large transactions and is highly dependent on arbitrageurs for correction.

As trading volume grows, order book models are gradually being introduced. On-chain or semi-on-chain orderbooks allow market makers to place orders directly, significantly improving market depth and price discovery capabilities. In reality, most protocols choose a compromise: off-chain matching and on-chain settlement, or combining AMMs with limit orders to balance decentralization and trading performance.

Behind these models, the real risk lies with the liquidity providers. LPs are essentially betting against all traders, earning fees and funding rates while bearing the risk of market directional fluctuations. If the protocol's risk control is poorly designed, the long-term profits of professional traders will ultimately translate into systemic losses for the LPs.

Therefore, mature Perp DEXs invest heavily in liquidation mechanisms, insurance funds, and parameter adjustments. Liquidation is not a punishment, but a necessary means to maintain system stability. Those who can quickly and accurately complete liquidation under extreme market conditions are qualified for long-term survival.

5. Where exactly is Perp DEX's competitive advantage?

To determine whether a Perp DEX has long-term value, one cannot simply look at the interface or incentives; rather, one must examine whether it has built a genuine competitive advantage.

Liquidity depth is the first hurdle; without stable depth, even the best mechanisms cannot attract large amounts of capital. The security of the clearing system and oracles is the second hurdle; any serious delay or error will directly shake market confidence. The third hurdle is the ability to retain professional traders and market makers, which depends on latency, fees, and the overall trading experience.

Ultimately, all competitive advantages point to the same question: can the protocol be profitable in the long run without relying on subsidies? Only by generating positive cash flow can Perp DEX become true infrastructure, rather than a short-term narrative.

6. How to use data to determine if a Perp DEX is healthy?

At the investment research level, Perp DEX has a relatively clear evaluation framework. The relationship between trading volume and TVL reflects capital utilization, and the comparison between overall trader profits and losses and LP returns reveals whether risk control is reasonable. The stability of funding rates and the frequency and dispersion of liquidations are often more important than daily trading volume.

In addition, the number of active traders and the revenue structure of agreements can help determine whether a platform has truly built user stickiness, rather than relying on short-term incentives to accumulate data.

7. The most easily overlooked risks in Perp DEX

Many risks do not stem from leverage itself, but from systemic details. Oracle delays can be amplified in extreme market conditions, liquidity can dry up instantly during periods of high volatility, and untimely adjustments to governance parameters can trigger a chain reaction.

These risks don't occur every day, but when they do, they are often fatal. Understanding these "low-frequency, high-impact" risks is a prerequisite for using Perp DEX.

Case Study: A Specialized Attempt at the Limits of Perpetual Contracts on the Hyperliquid Chain

While most Perp DEXs start with "how to replicate the CEX experience in a DeFi environment," Hyperliquid's approach has been different from the beginning. It doesn't simply "build a Perp" on an existing public chain; instead, it redesigns an entire underlying infrastructure for the highly specialized scenario of perpetual contract trading.

Hyperliquid's decision to develop its own high-performance L1/Appchain is essentially a very radical but logically sound trade-off: sacrificing versatility for specialization in exchange for matching efficiency, latency, and risk control certainty. This also determines that its target users are not general DeFi users, but rather mid-to-high frequency traders who are extremely sensitive to execution quality, slippage, and capital efficiency.

In terms of trading mechanisms, Hyperliquid employs a fully on-chain orderbook, rather than a vAMM or semi-off-chain matching system. This is crucial. An orderbook means that the price discovery process is closer to that of a traditional derivatives exchange, but it also significantly increases the demands on system performance, liquidation engines, and risk control models. By placing liquidation and risk control at the system level rather than as an afterthought, Hyperliquid makes its behavior more predictable under extreme market conditions.

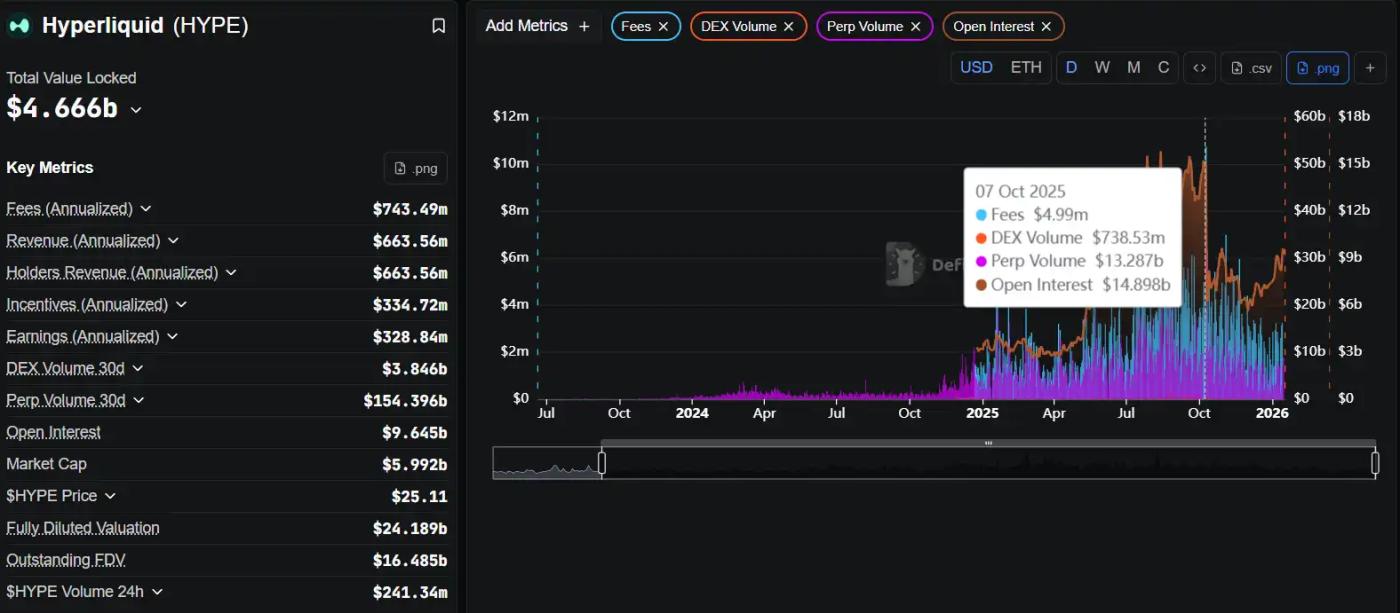

From the perspective of on-chain data, the most worthy of study for Hyperliquid is not a single metric, but the "combination relationship" between metrics.

On DefiLlama, you can observe that Hyperliquid has consistently maintained a very high daily trading volume/TVL ratio. This isn't just the result of "volume manipulation," but a clear signal: the liquidity entering the system is being used frequently and intensively, rather than lying idle in pools waiting for subsidies. High capital efficiency often indicates high-quality traders.

Further analysis of the active trader structure on Dune reveals that Hyperliquid's daily and weekly active users (DAUs) do not experience brief spikes during airdrops or events, but rather exhibit a relatively smooth and consistent pattern. This type of curve typically corresponds to "tool-based usage" rather than "mining-based participation." For investment research, this is a crucial dividing line.

Combining Nansen data with observations of large account behavior makes it easier to understand Hyperliquid's true competitive advantage: the system contains consistently participating professional accounts whose trading behavior exhibits consistent strategies, rather than one-off games. This means that what's happening at Hyperliquid isn't "attracting users to try it out," but rather traders migrating to their primary trading venue.

From a long-term perspective, Hyperliquid's risk lies not in its product form, but in the inherent difficulty of this path—a high-performance chain, orderbook, and professional traders place extremely high demands on operations, risk control, and system stability. However, once this flywheel is running, its user stickiness and migration costs will be far higher than those of a typical Perp DEX.

8. Who is suitable to use Perp DEX, and who is not?

Perp DEX is better suited for traders with a strong risk management mindset, rather than those who rely on emotions. On-chain trading means you are responsible for your own positions; there is no customer service or human intervention. Low to medium leverage and clear stop-loss strategies are the fundamental rules for survival in on-chain trading.

For LPs, this is not a "risk-free return," but rather a passive market-making strategy. While you earn transaction fees, you also bear the brunt of market volatility.

9. The Next Stage of Perp DEX

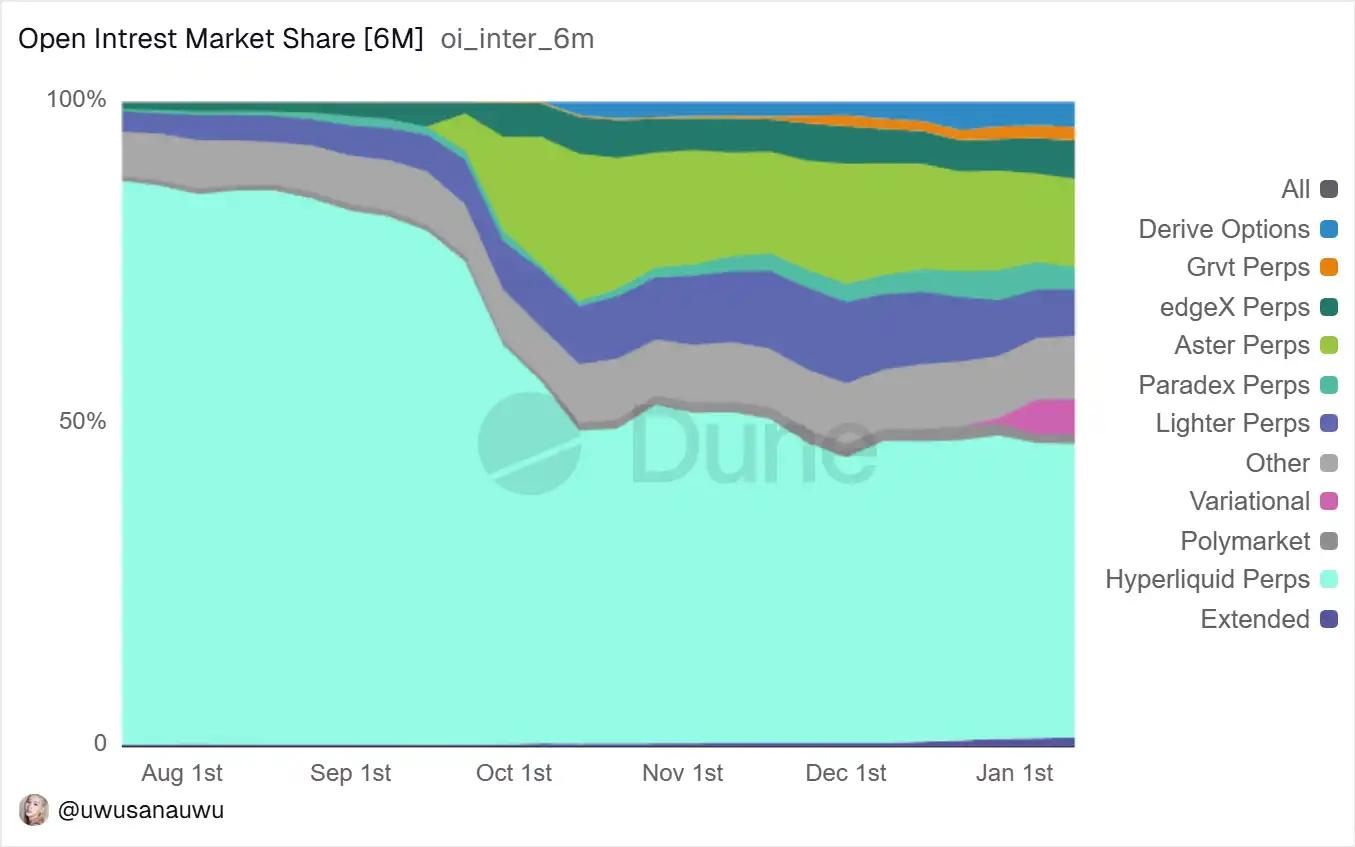

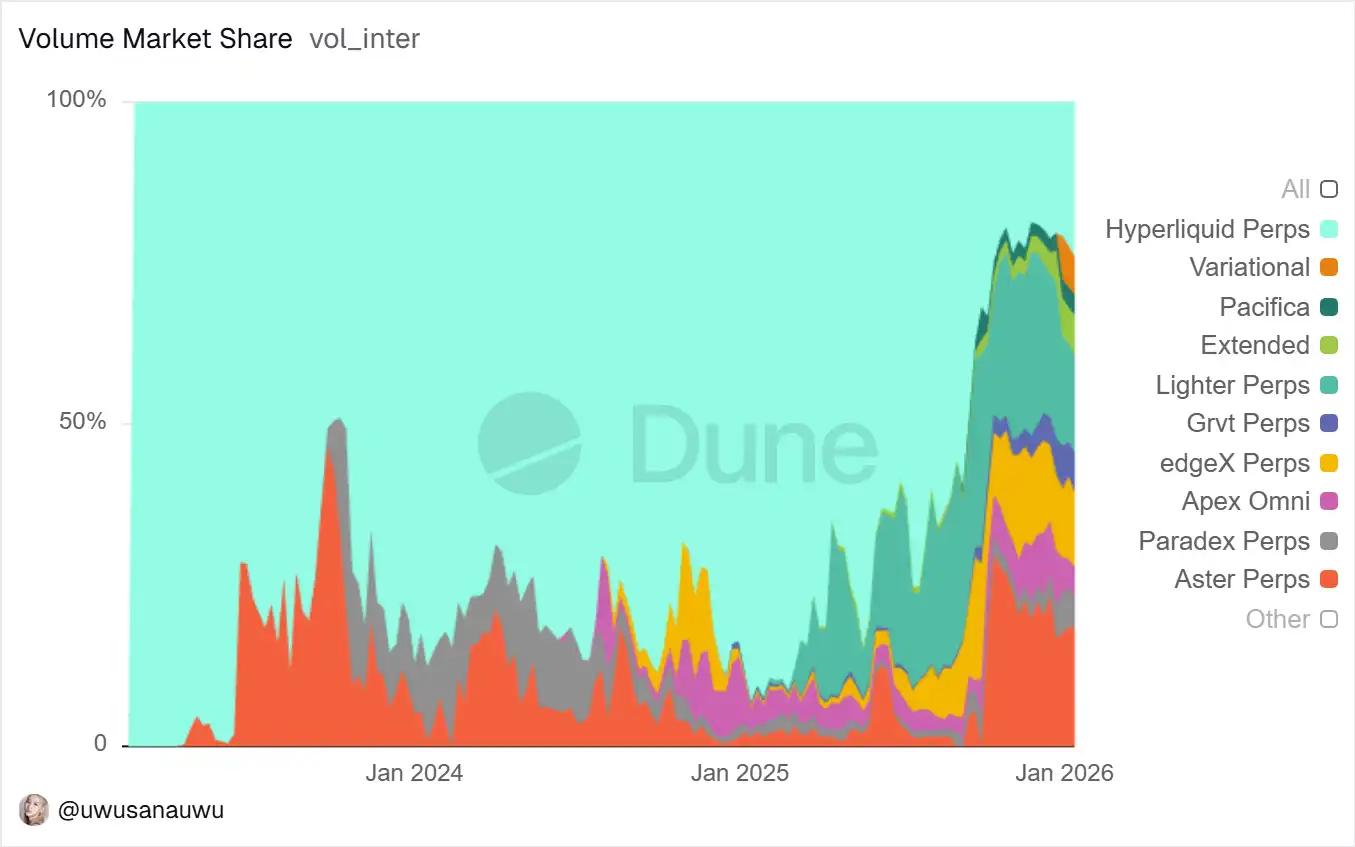

The changes the perpetual contract DEX ecosystem has undergone in the past year can no longer be simply summarized as "growth." A more accurate description would be a systemic restructuring of trading structures and market share. If Perp DEX was still in the product feasibility and user education phase from 2021 to 2023, then 2024 to 2025 marked the period when efficiency began to dominate everything. The market's focus shifted from "whether decentralized perpetual is feasible" to "which structure can support professional-grade trading in the long term."

Starting with the most direct data, this round of changes exhibits a clear trend of centralization. According to the latest statistics from DefiLlama, Hyperliquid's perpetual contract trading volume reached $156 billion in the past 30 days, establishing an overwhelming advantage over similar protocols in terms of volume. In comparison, dYdX v4's trading volume during the same period was approximately $8.7 billion, GMX approximately $3.7 billion, while Aevo, which covers both options and perpetual contracts, has consistently maintained a monthly trading volume of over $15 billion. Extending the time horizon to the past year, this disparity is not an isolated event but the result of continuous accumulation, indicating that users and liquidity are concentrating on a few protocols with superior structures.

This concentration trend is even more pronounced on the revenue side. Hyperliquid generated approximately $61.4 million in transaction fees over the past 30 days, while GMX generated approximately $2.66 million and dYdX only $320,000 during the same period. For the first time in the perpetual contract DEX sector, a project has simultaneously generated positive feedback on the three curves of trading volume, active users, and real revenue. This also means that this sector is no longer just about "good-looking trading data," but truly possesses sustainable cash flow capabilities.

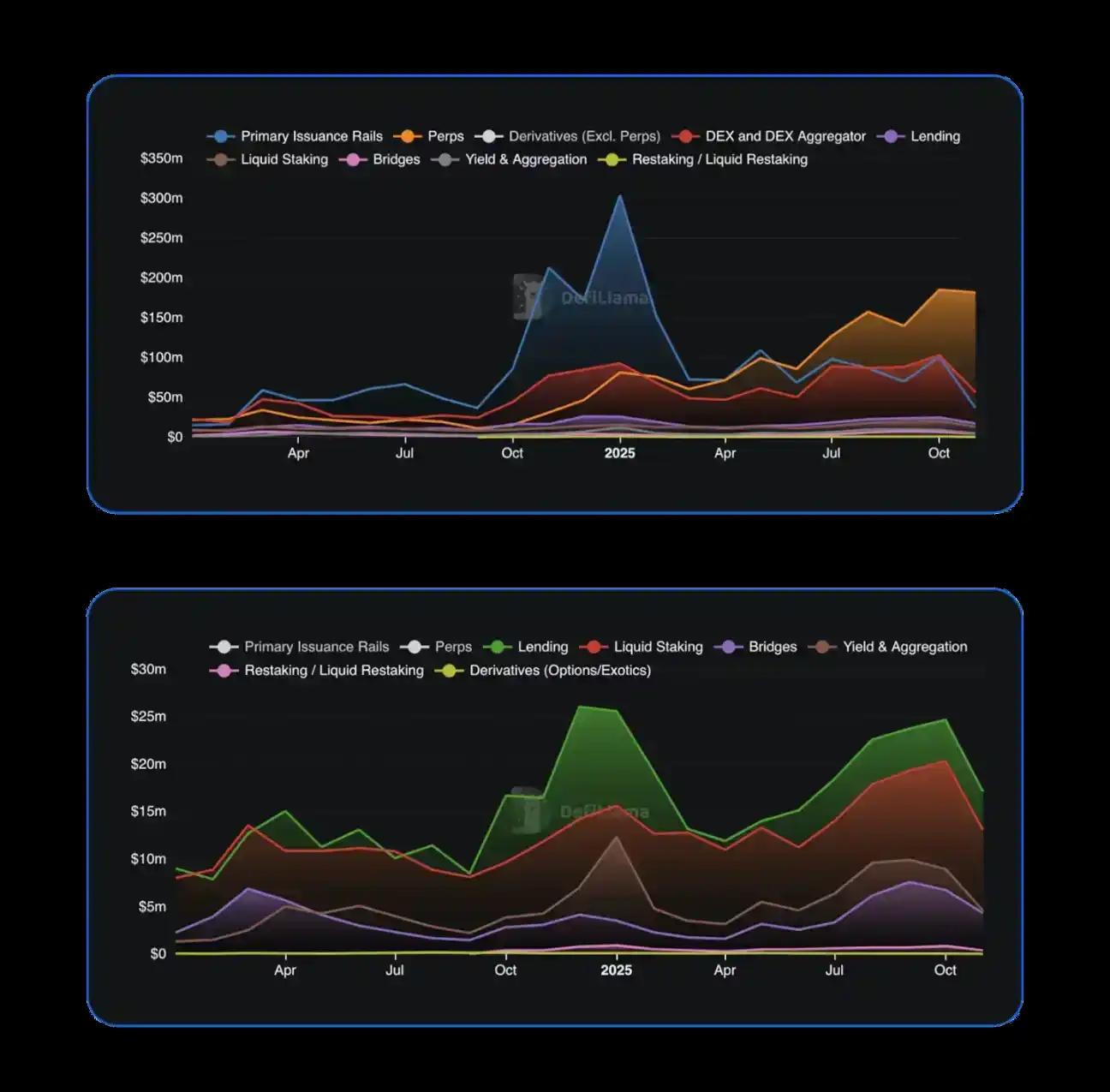

If we broaden our perspective to the entire DeFi market, this shift is not an isolated phenomenon. The DeFi ecosystem as a whole entered a more mature stage in 2025. Perpetual contract DEXs saw an increase of approximately $7.35 trillion in trading volume throughout the year, representing a year-on-year increase of over 170% and setting a new historical record. In contrast, the growth of spot DEXs relied more on cross-chain rotation, with relatively limited overall net expansion. A clear shift in funding structure is underway, with high-frequency, capital-efficient derivatives trading becoming one of the core value capture scenarios on-chain. In terms of revenue share, leading perpetual DEXs such as Hyperliquid, EdgeX, Lighter, and Axiom contributed approximately 7%–8% of total DeFi transaction fee revenue in 2025, a proportion exceeding the combined total of protocols in several mature sectors such as lending and staking.

Meanwhile, the user structure is also quietly changing. The large amount of short-term speculative trading driven by Meme coin prices is gradually cooling down, and the market is beginning to return to professional demand, primarily for hedging, arbitrage, and high-frequency trading. Data released by Aevo shows that its platform has nearly 250,000 active traders, significantly higher than most similar protocols; while the number of DYDX token holders in the dYdX ecosystem has grown from 37,000 to 68,600 in one year, reflecting its gradual recovery of user stickiness after the dedicated chain migration. It can be seen that the competition for Perp DEX is shifting from "attracting traffic" to "retaining professional users."

At this stage, performance metrics have become an implicit threshold for success. Early differences between Perp DEXs were primarily in product design and incentive mechanisms; now, transaction execution speed, system stability, and performance under extreme market conditions directly determine whether high-frequency traders are willing to deploy funds long-term. Hyperliquid employs a dedicated L1 architecture with CLOB, achieving millisecond-level matching and extremely low state latency; Aevo claims transaction latency below 10ms on its customized L2; and dYdX v4, after migrating to the Cosmos private chain, has reduced API response latency by approximately 98% compared to earlier versions. In contrast, GMX, still running on Arbitrum and Avalanche, is more susceptible to network load and latency issues under extreme market conditions.

These differences are not merely a matter of "good or bad user experience," but directly impact a platform's ability to support genuine high-frequency and institutional-level trading. The trading volume trend chart over the past 12 months clearly shows that Hyperliquid's monthly trading volume has been steadily increasing, establishing a dominant position; dYdX experienced a significant recovery after the second quarter, with a single-quarter trading volume of $34.3 billion in the fourth quarter; Aevo showed accelerated growth; while GMX's growth remained relatively stable. The revenue distribution histogram further amplifies this structural divergence, indicating that the market is pricing efficiency and performance in real transaction fees.

Against this backdrop, the next stage of Perp DEX's evolution is becoming increasingly clear. On one hand, the platform will continue to evolve towards higher-frequency, lower-latency trading models, attempting to replicate or even surpass the matching experience of centralized exchanges on-chain. Hybrid matching models, state compression, and combinations of more off-chain computation and on-chain settlement are likely to become standard features of future infrastructure. On the other hand, the proliferation of dedicated AppChains or customized Rollups is almost a certainty. dYdX's experience has already demonstrated that the advantages of dedicated chains in terms of throughput, governance flexibility, and parameter controllability are particularly crucial for high-frequency products like perpetual contracts.

Meanwhile, the boundaries between CeFi and DeFi are being redefined. The collaboration between dYdX and 21Shares to launch the DYDX ETP sends a clear signal: on-chain perpetual contract liquidity is penetrating the traditional financial system through compliant products. In the future, ETPs, structured products, and hedging strategies built around Perp DEX may become crucial bridges connecting institutional funds and on-chain markets. Parallel to this is the further integration of on-chain derivatives. Aevo already supports both options and perpetual contracts under a unified margin account. This multi-product shared risk control and margin model significantly improves capital efficiency and indicates that leading platforms in the next stage are more likely to evolve into comprehensive on-chain derivatives hubs.

Of course, expansion in scale does not mean the disappearance of risk. In November 2025, Hyperliquid experienced a bad debt event of approximately $4.9 million under extreme market conditions, and subsequently quickly adjusted its rates and risk parameters. Such events remind the market that liquidation mechanisms, insurance funds, and dynamic risk control capabilities will become crucial for handling larger-scale funds. With changes in the regulatory environment, some perpetual DEXs will also proactively consider compliance frameworks and risk disclosure mechanisms to reduce systemic uncertainty.

In summary, Perp DEX is transitioning from a phase focused on "user adoption" to one focused on "who can sustain professional trading in the long term." Future competition will no longer be solely about trading volume rankings, but rather a comprehensive contest encompassing execution efficiency, liquidity quality, product completeness, and risk management capabilities. The winners of the first half relied heavily on subsidies and narratives; however, the protocols that truly succeed in the second half will undoubtedly be those that can grow rapidly, remain stable under extreme market conditions, and possess the ability to integrate with the broader financial system. This is precisely why Perp DEX, as a core DeFi infrastructure, deserves our long-term attention.

Conclusion: Perp DEX is a core infrastructure of DeFi.

Perp DEX is not a short-term trend, but a core component that will inevitably emerge as DeFi matures. It allows derivatives trading to operate in a trustless environment for the first time, truly opening up the potential profits and risks to users.

In the future, what truly matters is not whether there are Perp DEXs, but which Perp DEXs can survive and become the foundation of the on-chain financial system.