Author: ARK Invest

Compiled by: Felix, PANews(This article has been abridged)

ARK Invest releases its flagship research report, "Big Ideas," annually. This report filters out short-term distractions to identify and interpret the technologies reshaping the global economy. This year's report explores 13 major ideas spanning AI, robotics, energy, blockchain, space, and biology, which are generating a compounding effect and redefining productivity, capital allocation, and competitive advantage across industries. This article excerpts topics such as AI and blockchain; details are provided below.

In this era of rapid development, AI serves as the core engine, accelerating the development of five major innovation platforms and triggering a turning point in macroeconomic growth.

Technological convergence is accelerating. Five key innovative technologies (AI, public blockchain, robotics, energy storage, and multi-omics) are becoming increasingly interdependent, as performance improvements in one technology unlock new capabilities for another.

Reusable rockets sending autonomous Mobility AI chips into orbit could be key to expanding next-generation cloud services. Multi-omics data licensed in digital wallets could power neural networks, driving the development of precision therapies and potentially curing rare diseases.

The world is entering an unprecedented cycle of technology investment. Every disruptive technology has the potential to have a profound macroeconomic impact.

AI infrastructure

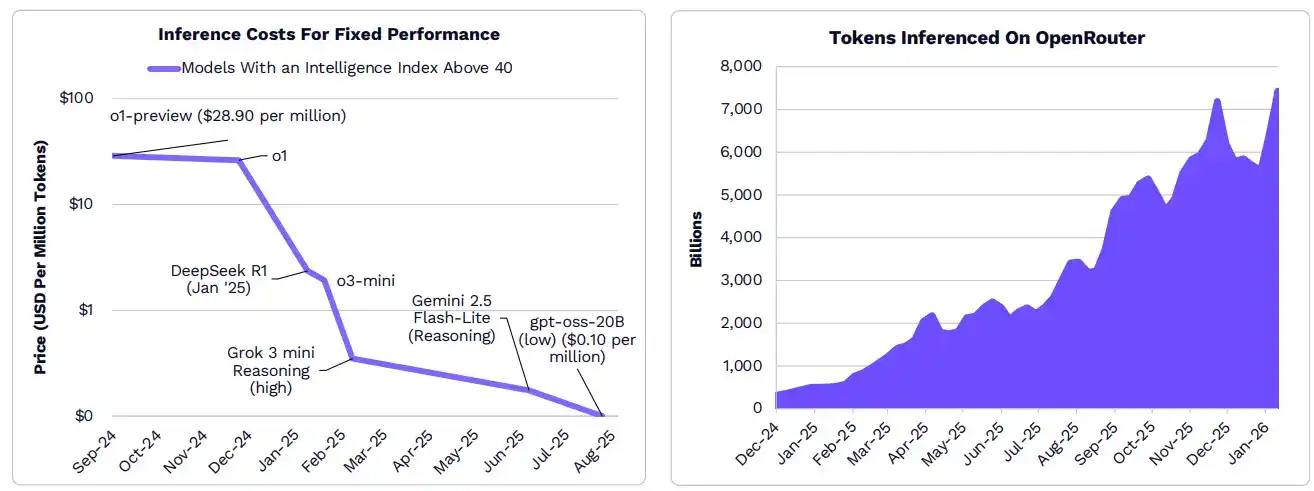

As the cost of reasoning decreases, the demand for AI is growing rapidly.

By some metrics, inference costs have decreased by over 99% in the past year. With the surge in AI-native applications, this cost reduction is driving an explosive growth in the number of inference tokens used by developers, enterprises, and consumers. Since December 2024, computational demands on OpenRouter (a unified application programming interface (API) for accessing large language models) have increased 25-fold.

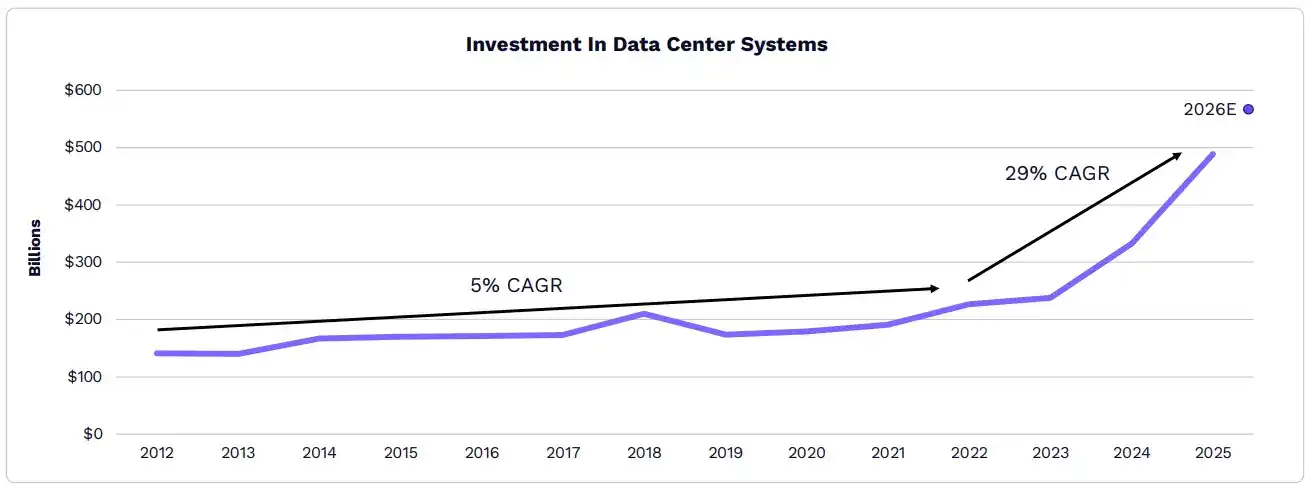

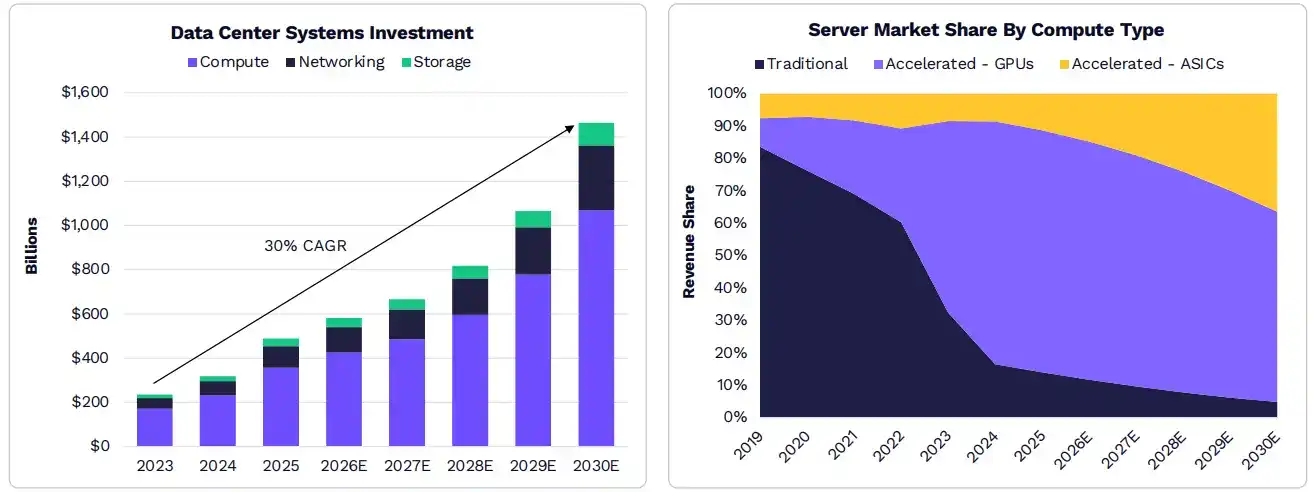

Since the “ChatGPT moment , ” the growth rate of data center systems has accelerated from 5% to 29% , with the annual growth rate continuing to climb.

By 2025, annual investment in data center systems will reach approximately $500 billion, nearly 2.5 times the average level from 2012 to 2023. According to ARK research, such investment will continue to grow, potentially tripling to approximately $1.4 trillion by 2030.

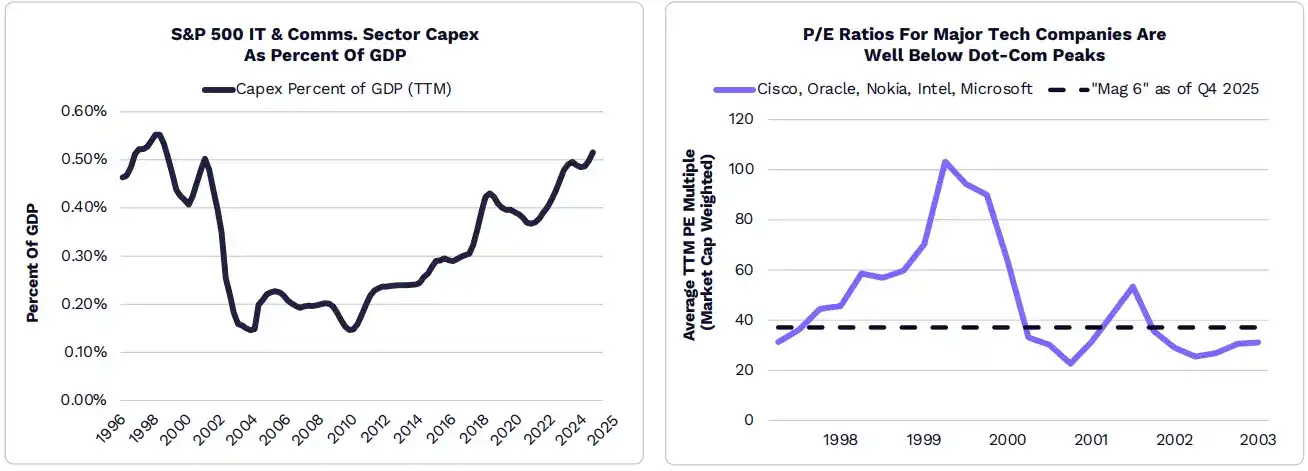

Technology capital expenditures have reached levels seen during the boom years of the technology and telecommunications industries, but the valuations of technology companies are far lower than they were then.

According to ARK research, hyperscale data center operators will spend over $500 billion in capital expenditures in 2026, almost three times the $135 billion spent in 2021 (before the ChatGPT boom in 2022). Despite capital expenditures in the information technology and communications services sector reaching their highest level as a percentage of GDP since 1998, the technology sector's price-to-earnings ratio (P/E) is far below its peak during the tech and telecom bubble.

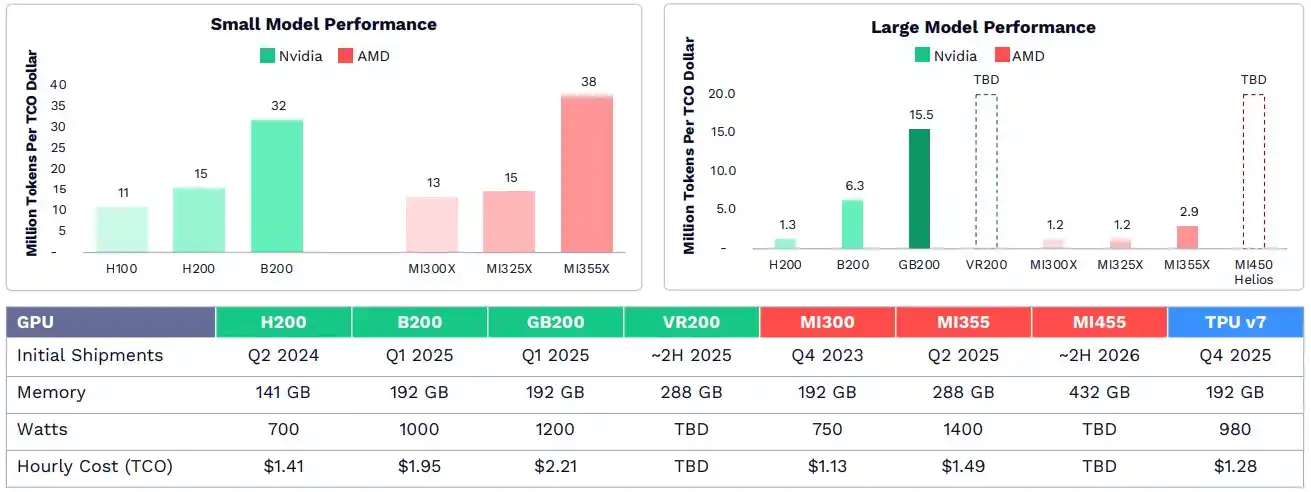

Nvidia faces increasingly fierce competition.

Nvidia's early investments in AI chip design, software, and networking have enabled it to achieve an 85% market share and a 75% gross margin in graphics processing units (GPUs). Today, competitors like AMD and Google have caught up in certain areas, such as small language model inference. Nvidia's Grace Blackwell rackmount system leads the way in large model inference, supporting state-of-the-art foundational models.

The demand for AI will drive sustainable growth in infrastructure.

As AI workloads proliferate in enterprise and consumer environments, AI infrastructure investment could exceed $1.4 trillion by 2030, with the majority going towards accelerating servers. ARK research indicates that ASICs designed by companies like Broadcom and Amazon's Annapurna Labs will continue to dominate market share as AI labs and hyperscale enterprises seek cost-effective computing power.

Bitcoin

Bitcoin is gradually becoming a leader in the new institutional asset class.

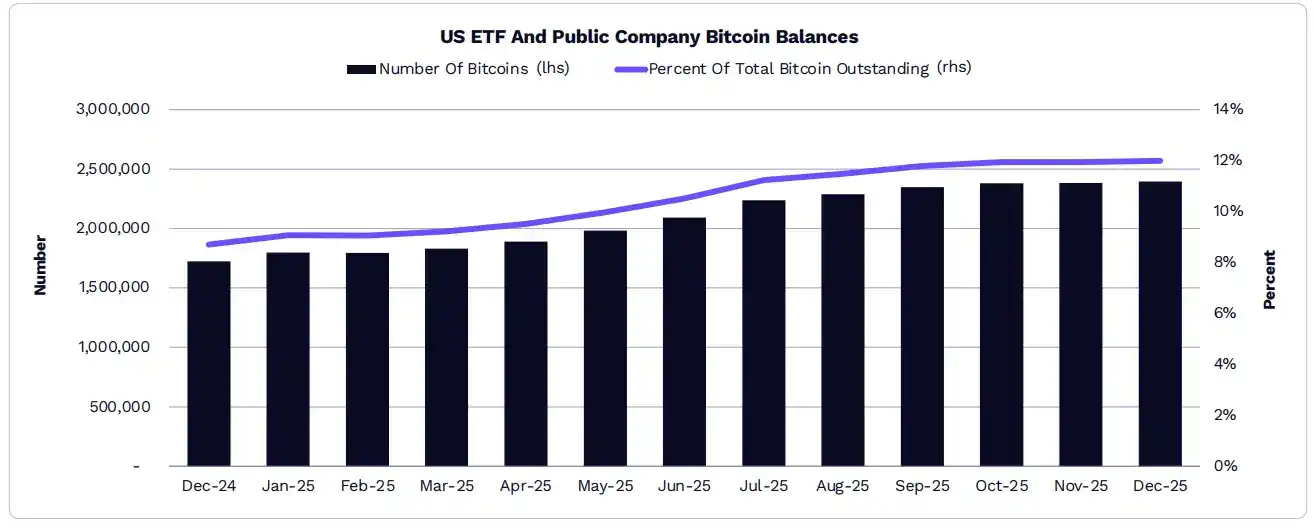

US ETFs and listed companies hold 12% of the total amount of Bitcoin .

In 2025, Bitcoin ETF holdings increased by 19.7%, from approximately 1.12 million to approximately 1.29 million; while the amount of Bitcoin held by publicly traded companies increased by 73%, from approximately 598,000 to approximately 1.09 million. Therefore, the total share of Bitcoin held by ETFs and publicly traded companies rose from 8.7% to 12%.

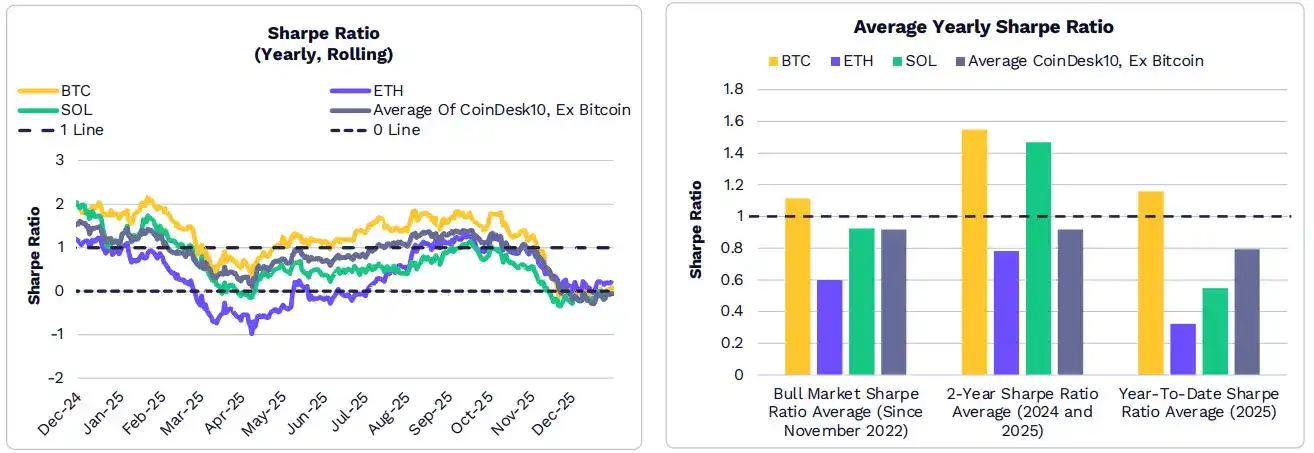

Bitcoin’s annual risk-adjusted return (Sharpe ratio) has long been higher than that of the overall crypto market.

For most of 2025, Bitcoin's risk-adjusted returns outperformed most other large-cap cryptocurrencies and indices. Since the most recent cycle lows (November 2022), early 2024, and early 2025, Bitcoin's average annualized Sharpe ratio has also surpassed the average of Ethereum, SOL, and the other nine constituent coins in the CoinDesk 10 index.

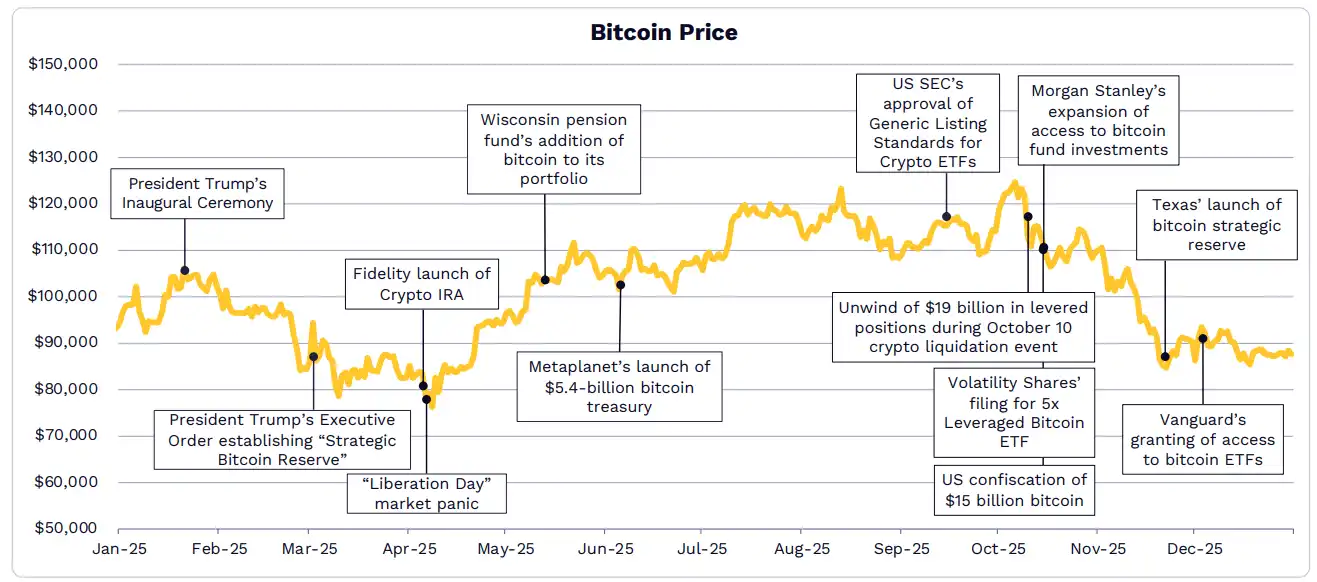

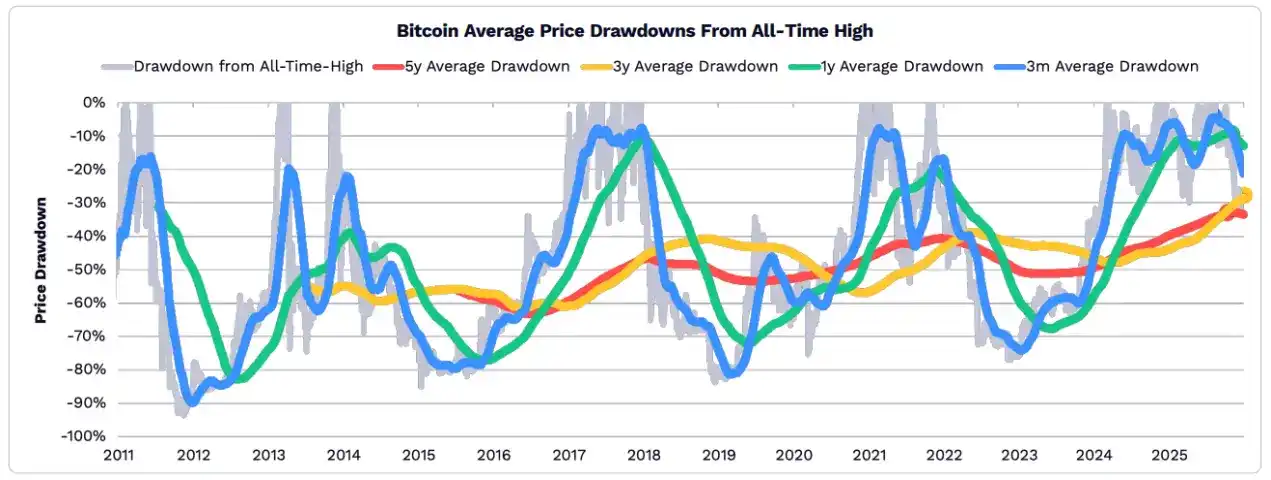

In 2025 , the average decline in Bitcoin's price relative to its all-time high was relatively moderate.

As Bitcoin's role as a safe-haven asset has grown, its volatility has decreased. Looking at timeframes of 5 years, 3 years, 1 year, and 3 months, Bitcoin's decline in 2025 is relatively moderate compared to historical levels.

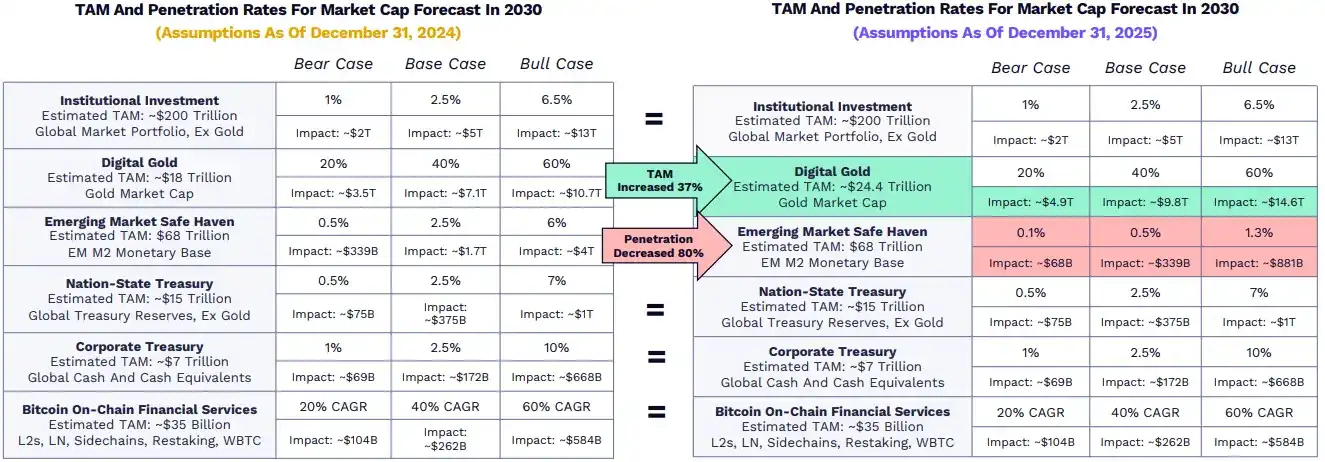

ARK has changed his assumptions about Bitcoin's growth, but his forecasts remain largely unchanged.

ARK's predictions for Bitcoin in 2030 have remained fairly stable, with only two assumptions changing: as digital gold, its potential market (TAM) grew by 37% after gold's market capitalization surged by 64.5% in 2025; and as a safe-haven asset in emerging markets, its projected penetration rate declined by 80% to reflect the rapid adoption of stablecoins in developing countries.

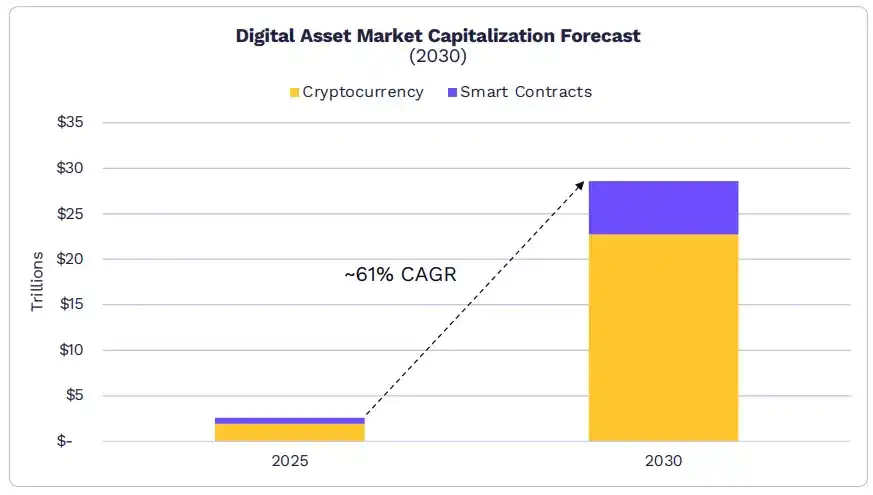

The market value of digital assets could reach $ 28 trillion by 2030 .

The market size for smart contracts and pure digital currencies (the latter serving as a store of value, medium of exchange, and unit of account on public blockchains) is projected to grow at a rate of approximately 61% per year, reaching $28 trillion by 2030. ARK believes Bitcoin could capture 70% of the market share, with the remainder dominated by smart contract networks such as Ethereum and Solana.

- According to ARK's forecast, Bitcoin is likely to dominate the cryptocurrency market over the next five years with a compound annual growth rate (CAGR) of approximately 63%, growing from nearly $2 trillion to approximately $16 trillion by 2030.

- The market capitalization of smart contracts could grow at a rate of 54% per year to approximately $6 trillion by 2030, with annualized revenue of approximately $192 billion and an average transaction fee rate of 0.75%.

- Two or three L1 platforms will capture the majority of the market share, but their market capitalization will come more from their currency premium (value storage and reserve asset characteristics) than from discounted cash flow.

Tokenized assets

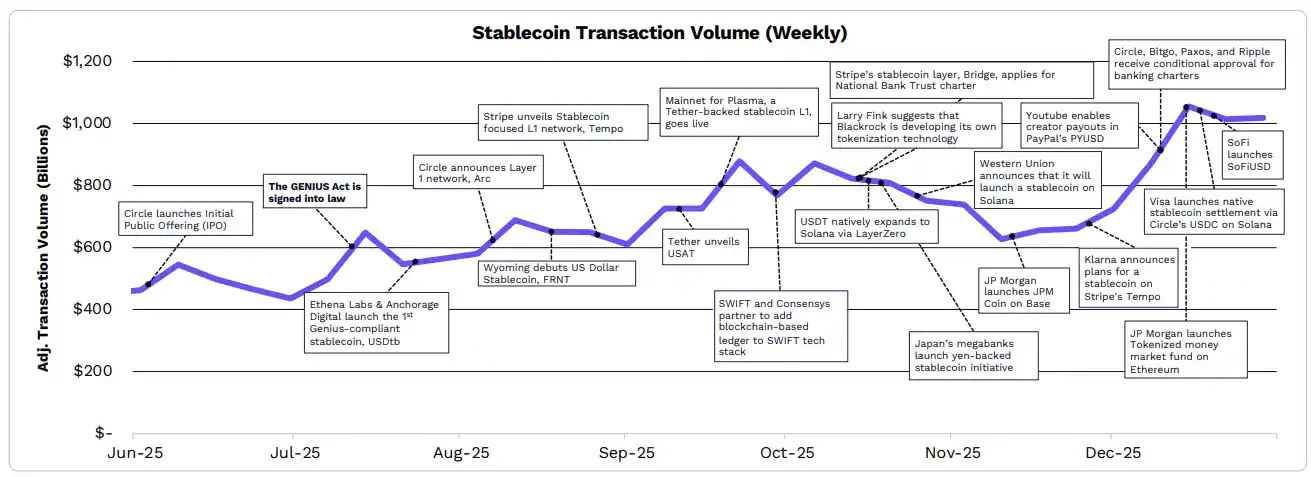

Thanks to the GENIUS Act, financial institutions are reassessing their stablecoin and tokenization strategies.

Thanks to the regulatory clarity brought about by the GENIUS Act, stablecoin activity has surged to an all-time high. Numerous companies and institutions have announced the launch of their own stablecoins, while BlackRock has revealed it is preparing an internal tokenization platform. Major stablecoin issuers and fintech companies such as Tether, Circle, and Stripe have launched or supported L1 blockchains optimized for stablecoins.

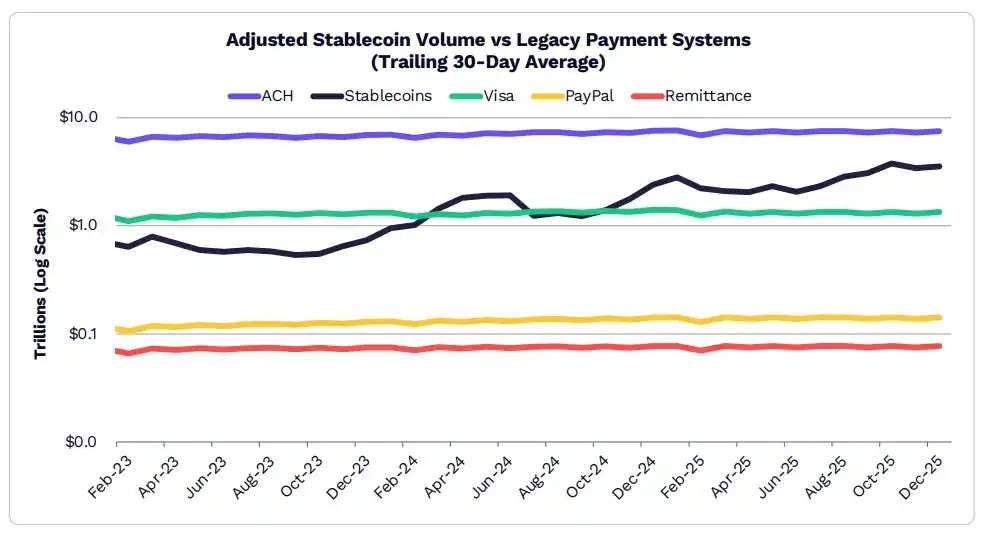

Stablecoin trading volume reached $ 3.5 trillion in December , far exceeding most traditional payment systems.

In December 2025, the 30-day moving average of stablecoin transaction volume was $3.5 trillion, which is 2.3 times the total value of Visa, PayPal, and Remittances.

Circle's stablecoin USDC dominates trading volume, accounting for approximately 60%, followed by Tether's USDT, which accounts for approximately 35%.

By 2025, the supply of stablecoins will grow by about 50%, from $210 billion to $307 billion, with USDT and USDC accounting for 61% and 25% respectively.

Sky Protocol is the only stablecoin issuer, besides others, with a market capitalization exceeding $10 billion by the end of 2025.

It is worth noting that the market value of PayPal's PYUSD has increased more than sixfold, reaching $3.4 billion.

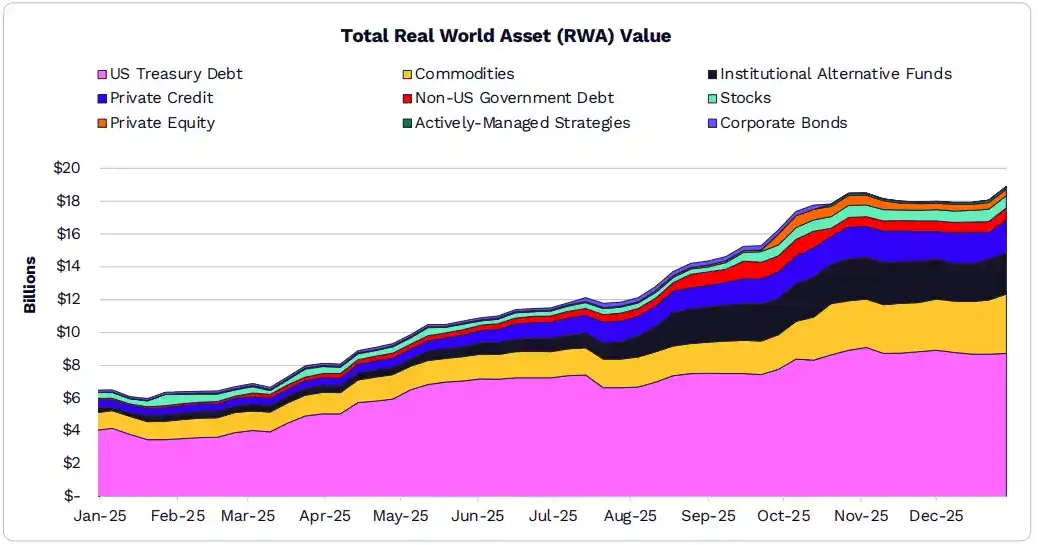

Driven primarily by U.S. Treasury bonds and commodities, the tokenized asset market tripled in size in 2025 , reaching $ 19 billion.

RWA's market capitalization grew by 208% to $18.9 billion in 2025.

BlackRock’s $1.7 billion BUIDL money market fund is one of its largest products, representing 20% of $9 billion in U.S. Treasury bonds.

Tokenized gold products from Tether (XAUT) and Paxos (PAXG) lead the tokenized commodities market, with market capitalizations of $1.8 billion and $1.6 billion respectively, accounting for a combined 83%.

The tokenization of publicly traded shares is close to $750 million.

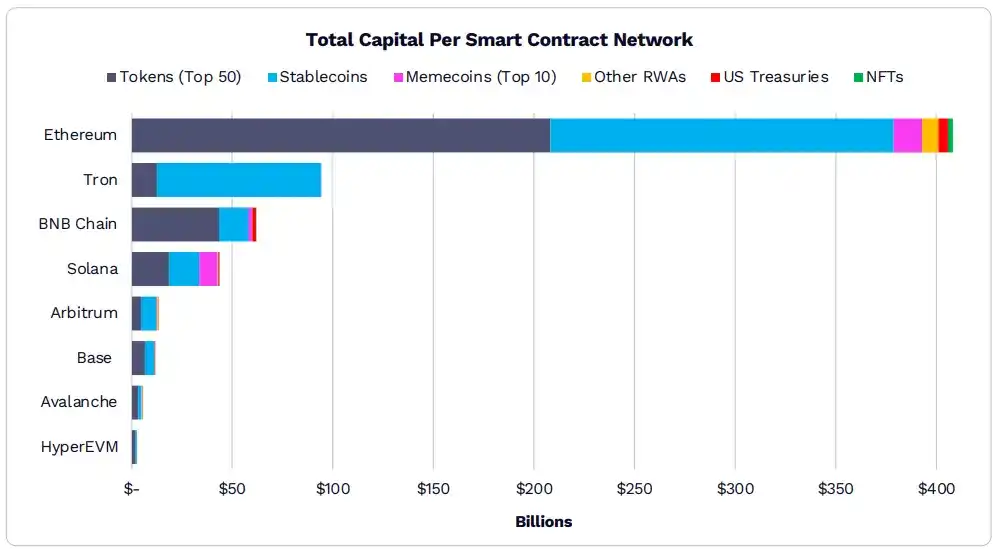

Ethereum remains the preferred blockchain for on-chain assets.

The total value of assets on Ethereum has now exceeded $400 billion. Of the eight most popular blockchains, seven chains have 90% of their market capitalization backed by stablecoins and the top 50 tokens.

On blockchains other than Solana, memecoins account for approximately 3% or less of the market capitalization. On Solana, however, memecoins account for approximately 21% of the asset value.

RWA tokenization is poised to become one of the fastest-growing categories. Since the majority of global value resides off-chain, off-chain assets remain the biggest growth opportunity for on-chain adoption.

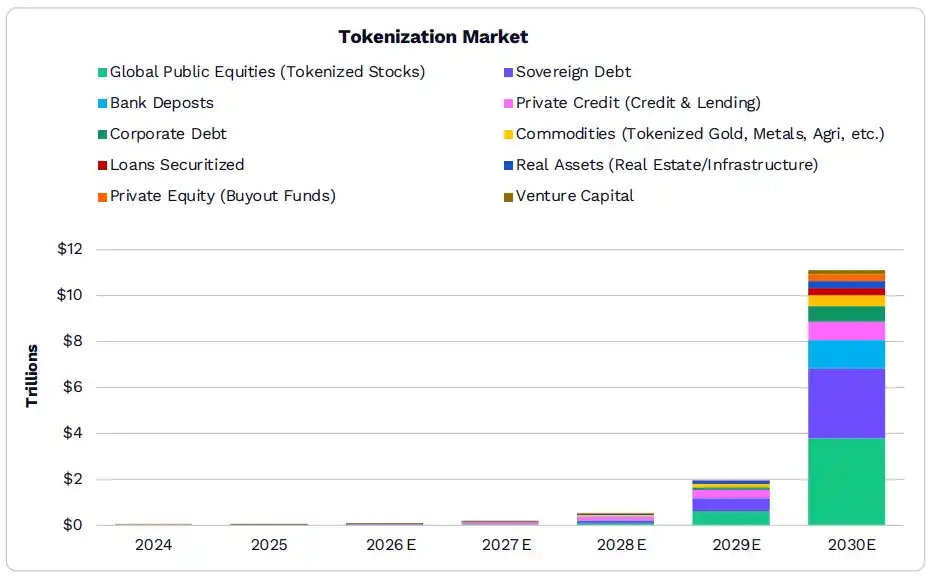

The global market size of tokenized assets may exceed $ 11 trillion by 2030 .

According to our research, the size of tokenized assets could grow from $19 billion to $11 trillion, at which point it would account for approximately 1.38% of all financial assets.

While sovereign debt currently dominates the tokenization space, the on-chain value of bank deposits and globally listed stocks is likely to be higher than it is now within the next 5 years.

ARK believes that the widespread adoption of tokenization will depend on clearer regulatory policies and improved institutional-grade infrastructure.

Traditional enterprises are expanding their influence on the blockchain by building their own infrastructure.

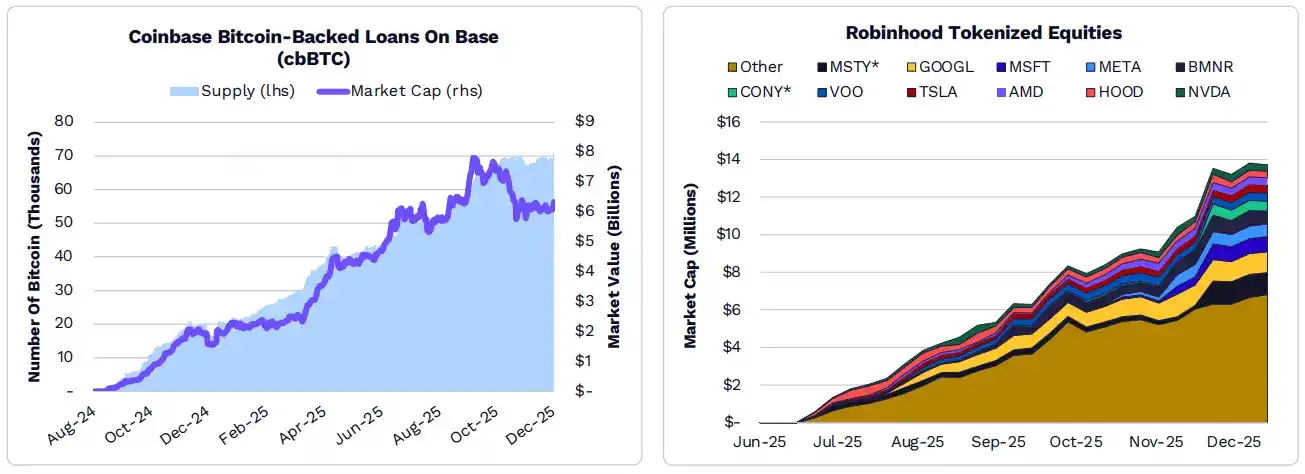

Traditional companies are building their own on-chain infrastructure. Circle (Arc), Coinbase (Base, cbBTC), Kraken (Ink), OKX (X Layer), Robinhood (Robinhood Chain), and Stripe (Tempo) are launching their own branded L1/L2 networks to support their own products, such as Bitcoin-backed loans, tokenized stocks and ETFs, and stablecoin-based payment channels.

DeFi applications

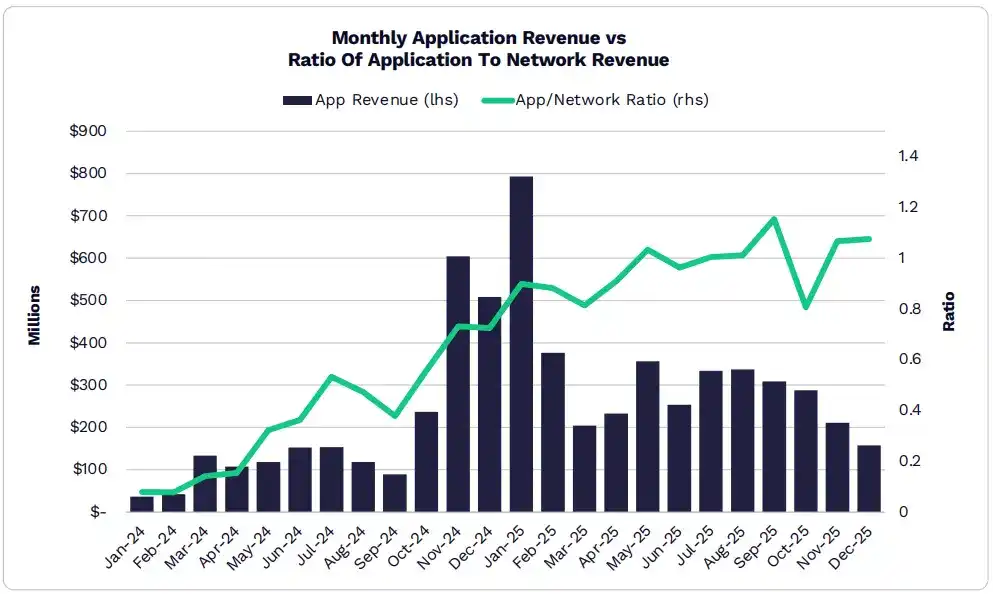

The acquisition of value from digital assets has shifted from the network to applications.

The internet is gradually transforming into a public utility, shifting user economic benefits and profit margins to the application level.

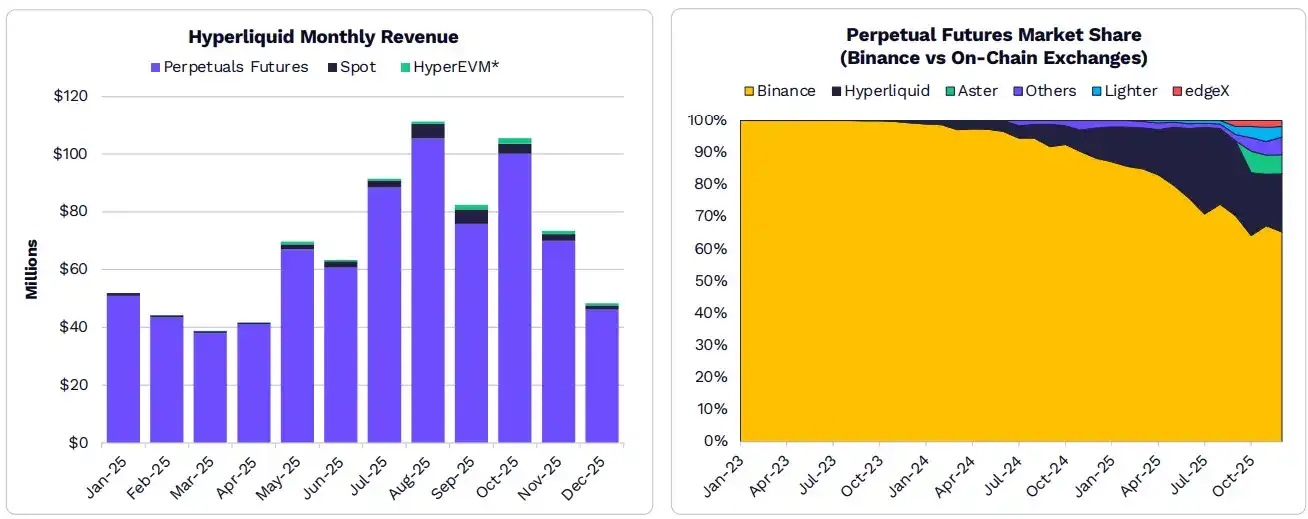

Led by Hyperliquid, Pump.fun, and Pancakeswap, total app revenue reached a record high of approximately $3.8 billion in 2025.

One-fifth of all app revenue in 2025 will come from January, the highest monthly revenue ever.

Today, 70 applications and protocols have monthly recurring revenue (MRR) exceeding $1 million.

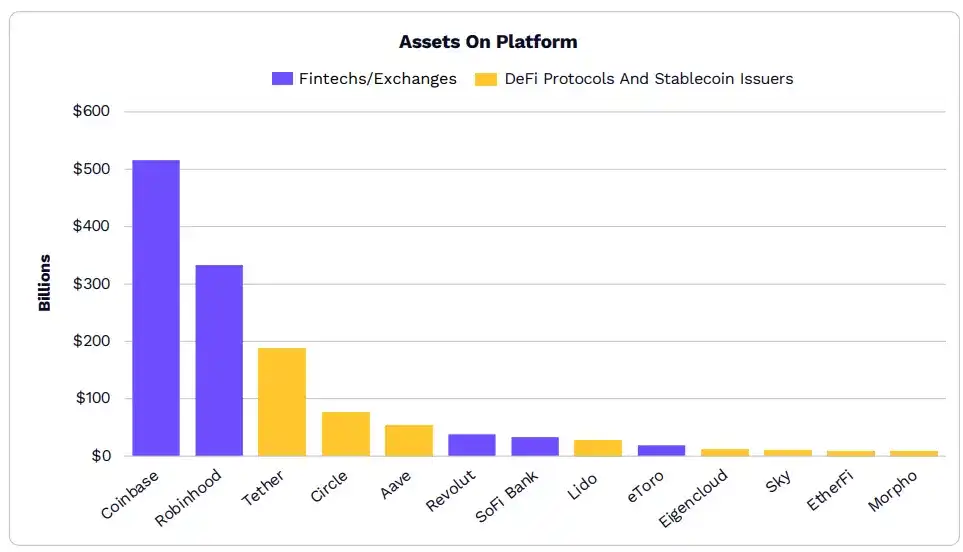

The asset size of DeFi and stablecoin issuers is catching up with that of many fintech companies.

The asset size gap between traditional fintech platforms and crypto-native platforms is narrowing, indicating a convergence of traditional and on-chain infrastructure.

DeFi protocols such as liquidity staking or lending platforms are attracting institutional capital and expanding rapidly.

The TVL of the top 50 DeFi platforms has all entered the billion-dollar club, with the top 12 protocols each exceeding $5 billion.

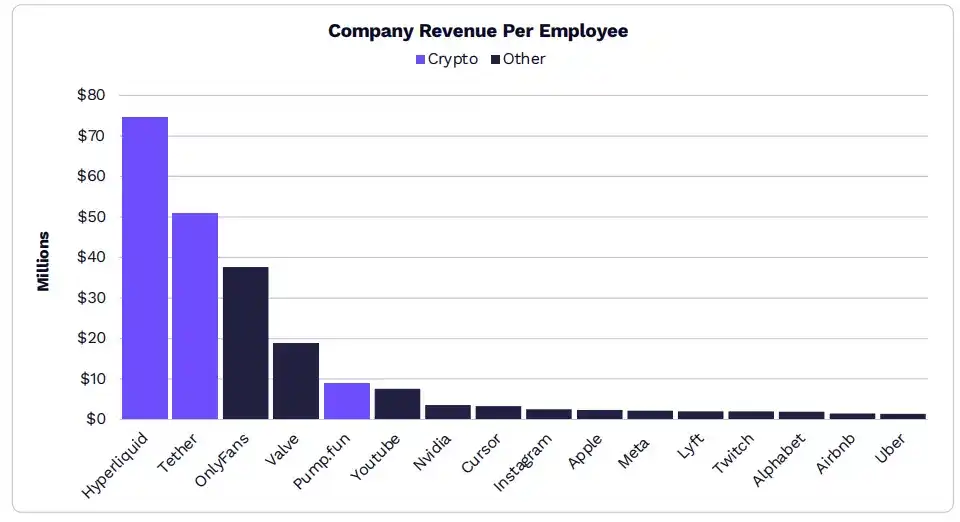

The world’s most revenue-efficient companies include Hyperliquid , Tether , and Pump.fun .

By 2025, Hyperliquid, with only 15 employees, will generate over $800 million in annual revenue.

Through its presence in on-chain verticals such as perpetual contracts, stablecoins, and memcoins, Hyperliquid is attracting users and capital at an astonishing scale and has a clear product-market fit.

On-chain businesses and protocols are redefining productivity, as a handful of people can generate revenue and profitability comparable to world-class companies.

Led by Hyperliquid , DeFi derivatives are taking market share from Binance in the perpetual contract market.

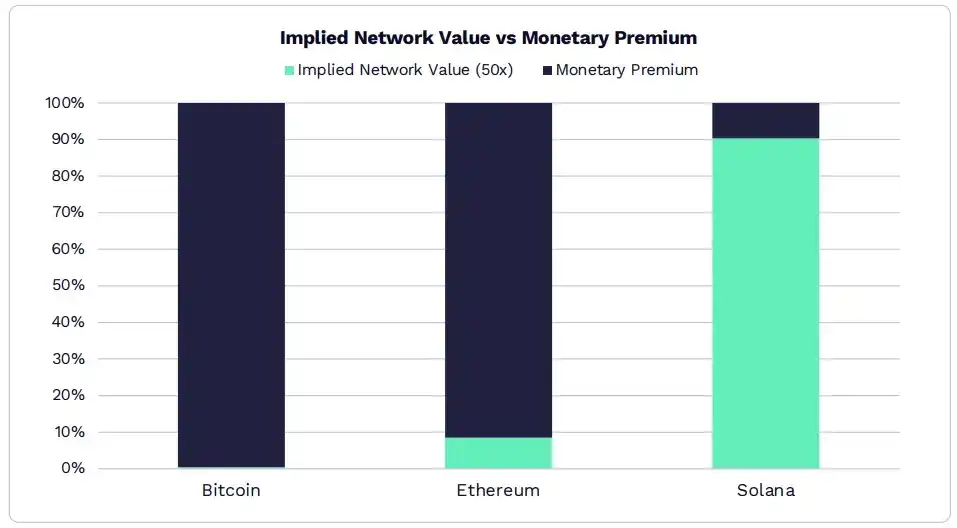

L1 networks are evolving from revenue-generating networks into monetary assets.

If we extrapolate based on a 50x revenue multiple, over 90% of Ethereum's market capitalization is attributable to its role as a monetary asset.

Solana generated $1.4 billion in revenue, proving that 90% of its valuation comes from network utility.

According to ARK research, only a few digital assets can retain monetary attributes and become a highly liquid store of value.

Related reading: Cathie Wood's 2026 Macro & Technology Investment Roadmap