Author: Evanss6

Compiled by: TechFlow TechFlow

TechFlow Dive: Cryptocurrencies were once the sole battleground for seeking "moonshot" returns (100x, 1000x), but this landscape was completely shattered with the massive entry of traditional financial institutions (Boomers) in 2024. Renowned crypto researcher Evanss6 points out that cryptocurrencies not only lost their monopoly on excess returns but were also forced to accept the performance evaluation system from traditional finance—the discounted cash flow (DCF) model.

In an era where fields like AI, semiconductors, and space technology can also offer high returns, Altcoin lacking fundamentals are gradually being abandoned by the market. This article provides an in-depth analysis of the paradigm shift from "emotion-driven" to "fundamental-driven" approaches, and focuses on dissecting how protocols like Hyperliquid and LayerZero are redefining the value of crypto assets through real cash flows.

The main text is as follows:

Cryptocurrencies haven't lost their edge, but they've lost their monopoly. The "moonshot" return curve, once almost confined to the crypto space, is now ubiquitous—in semiconductors, AI infrastructure, storage, space, and any next narrative on the Trump administration's agenda. Savvy money, which used to dart between different cryptocurrencies, has learned to move to other sectors after witnessing the shift in extraction pipelines. Meanwhile, DATs (Direct Token Protocols) and Baby Boomers are draining the supply, locking in the thousandfold returns that early gamblers (OGs) dreamed of. And when these Baby Boomers arrive, they bring their discounted cash flow (DCF) models.

The overwhelming trend in cryptocurrencies over the past few years has been a monotonous increase in financialization and a continuous fusion with traditional finance (TradFi). But for dreamers who entered the Bitcoin and crypto space at least several cycles ago, this level of adoption once felt like a pipe dream. They talked about pension funds, corporate and sovereign wealth accumulation: early players dreamed of throwing chips at them. BlackRock brought about the most successful ETF launch in history, attracting over $63 billion in inflows in two years.

Caption: Bitcoin (BTC) ETF inflow data provided by Farside.

When Ethereum and smart contracts emerged in 2015, the focus shifted from "who would buy" to "creating a completely new financial system on the crypto track." While the crypto space has funded countless ideas over the years, and most have failed in one way or another, one of the most logical ideas has consistently been backend financial infrastructure, or decentralized finance (DeFi). In short, 10 years later, every major institution is involved, continuously deepening and expanding their services. Just yesterday, the New York Stock Exchange (NYSE/ICE) announced they are building a platform for 24/7 trading of tokenized securities with instant settlement and stablecoin backing.

Caption: The NYSE, owned by Intercontinental Exchange, plans to launch 24/7 trading on its crypto infrastructure.

In those days of 2012-2016, there were relatively few tokens available, and initial valuations were very low. Therefore, if you chose the right coin, you could reap huge upside potential due to its extremely early stage. This asymmetric potential for growth was the biggest draw. As more and more people heard success stories, they flocked in, trying to get a piece of the modern-day gold rush.

Encryption has grown

This shift is evident in many ways, including price volatility and market sentiment. Most notably, Altcoin have performed exceptionally poorly in this cycle compared to previous cycles.

There are many reasons for this situation, such as the lowered barrier to entry for issuing tokens (Launchpads) and the escalation of the extraction game (games with low circulation, high fully diluted valuations, and a zeitgeist that makes people less willing to bid for them). I have mentioned these in my previous articles, "There is no PvE I Love you" and "The Sunk Cost Cage." Links are below for your review.

"The Cage of Sunk Costs" https://x.com/Evan_ss6/status/1940886721723302015

"No PvE, only my love for you" https://x.com/Evan_ss6/status/1935733564227616812

Therefore, we see very few success stories outside of mainstream cryptocurrencies. The most notable example is Hyperliquid, which provided tremendous returns for its early community. It is also a prime example of the "Return to Fundamentals" strategy I will discuss later. Despite its enormous success growing from $0 to a fully diluted valuation (FDV) of $24 billion/$8 billion in circulating market capitalization, Hyperliquid is now down nearly 60% from its all-time high. Key elements that enabled its success include:

- There is genuine, unincentivized demand for the product (perpetual contracts). Users find good liquidity extremely useful for speculation and hedging.

- The product is excellent.

- Correspondingly, the product can generate considerable revenue (for which users are willing to pay).

- It features a unique and superior token economics (no investors, team lock-up).

- Revenue from the product directly benefits token holders through buybacks.

I have long held the view that any crypto product, simply because it is a crypto product, will be valued at 10 to 10,000 times higher than its corresponding Web2 or traditional financial (TradFi) product.

My argument is that the combination of baby boomer/traditional financial adoption and the declining prospects of 99% of Altcoin has ushered in an era where Altcoin will be forced to compete based on traditional business metrics such as cash flow, rather than on atmosphere (Vibes) or hopes and dreams. The premium derived solely from the use of crypto has been significantly eroded, which is a good thing.

Stock market and rotation bubbles

While cryptocurrencies were once the battleground for asymmetric upside, we've seen a shift towards the stock market, with many crypto natives turning their attention entirely to traditional markets. It's hard to blame them. Look at these success stories that everyone can participate in.

Caption: The asymmetric upside potential for ordinary retail investors in stocks such as Nvidia (NVDA), Carvana (CVNA), Advanced Micro Devices (SMCI), and Suntory (SNDK).

As speculative funds are channeled to areas that appear to offer a better risk-return profile than Altcoin(such as many AI-related stocks and precious metals), it's not surprising that less money is being spent chasing Altcoin. Bubble chasers, or what GCR once defined as the "Generation Moonshot," are increasingly finding themselves able to participate in various rotating bubbles from the comfort of their personal securities accounts.

Caption: About a year after the Gamestop legend, the rules of the game had clearly changed.

While it's not entirely accurate to say that these Altcoin"may be worthless," the main point remains that a large number of people are simply trying to chase the "fastest horse" to achieve rapid capital accumulation and compound interest, rather than engaging in disciplined betting and research like Bogleheads (a term for prudent index fund investors).

The increasing gamification, attention-grabbing, and narrative-driven nature of the stock market is another reason why Altcoin are forced to compete on real fundamentals such as earnings. Cryptocurrencies are no longer the hot industry that can absorb all speculation and bubble-chasing capital (compared to fields like AI, robotics, and space). Most things will gradually go to zero and be abandoned as the tendency for capital to back them weakens. Only a few will survive through sustainable profitability.

change

All of this suggests that we need to adopt a different approach to crypto trading and investing than most people (and even the successful ones) did between 2009 and 2021. The broader logic is that the crypto industry is undergoing a "boomerification" through deeper integration with traditional finance. In a world where you can trade BTC, ETH, SOL, gold, NVDA, TSLA, GOOG, and any other NYSE stock in a single account, what truly matters, aside from non-sovereign stores of value (SoV) tokens, will be assets that can generate sustainable fees to support their valuations.

The existence of these assets validates the viewpoint from 2015-18: back-end financial infrastructure is an excellent use case for smart contracts. If you still want to invest in this logic, I think it makes sense to focus on the "picks and shovels" (i.e., infrastructure) that drive its development. Just as you can invest in Interactive Brokers (IBKR), you can also invest in crypto products and protocols that can earn fees through trading-related activities.

These opportunities are not insignificant. If you can foresee a future where finance completely shifts to a crypto track, then many crypto protocols are still small in scale relative to that prospect.

I identified four verticals that I believe are worth looking for investment opportunities in: (1) exchanges, (2) lending, (3) RWA (real-world assets), stablecoins and tokenized assets (especially equity), and (4) interoperability.

I will not elaborate on (1) and (2) because I believe they are self-evident, and the players and protocols involved (such as Binance, Bybit, Coinbase, Hyperliquid, Lighter, Aave, Maker, Morpho, etc.) are widely understood and in a more mature state. However, I will elaborate on the opportunities in (3) and (4).

RWA, stablecoins, and tokenized assets

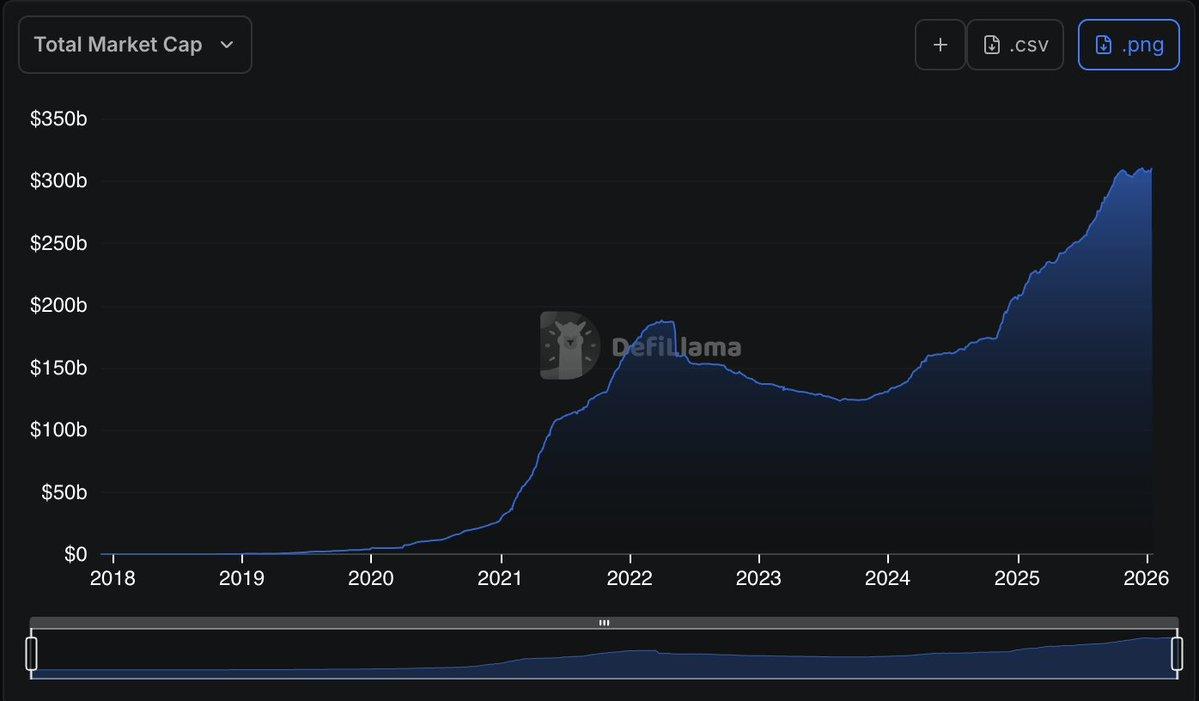

Stablecoins have gained significant attention over the past few years. With the Market Structure Bill expected to pass sometime this year, many different players are trying to get a piece of the growing stablecoin trend. Many crypto natives lament the difficulty in gaining exposure to this trend, as many of the best opportunities are not easily accessible (especially from giants like Tether and Circle).

Caption: The market capitalization of stablecoins has grown from almost zero in 2018 to $311 billion.

Another project that has greatly interested me is Superstate , founded by Compound founder Robert Leshner. Unfortunately, I currently have no investment exposure to this project. I find it unique and intriguing because they have built a technology and compliance system around issuing genuine tokenized stock on the Ethereum and Solana blockchains, rather than some random wrapper. This will allow companies to issue real stock on the crypto track, and even open up the possibility of IPOs or other financing. This model, combined with strong investors/partners and deep crypto-native leadership, should make it a key player in the space for years to come.

Interoperability with LayerZero ($ZRO)

Overall, this is a rather forgotten sector. But as every institution launches its own products (from stablecoins to exchanges, ETFs, and structured products), a dominant standard will be needed to make all of this work in a user-friendly way.

Most of the following information can be found on this podcast: Podcast Link

While other interoperability protocols exist, LayerZero and its full-chain token (OFT) hold a dominant market share across all metrics.

From a purely technical perspective—it broke out of its consolidation range and rebounded after a pullback test, a good setup for at least a move towards $2.30-$2.50. It demonstrated strong local strength, being one of the few tokens to rise this week, and completely recovered all losses when BTC plunged from $95,000 to $92,000 last night, dragging down Altcoin. Derivatives funding rates are also negative, likely due to spot buying from buybacks, labs, and long-term investors.

Caption: High Time Frame (HTF) Chart

Chart caption: 4-hour chart

One of the most common problems in Altcoin systems is that as tokens unlock, a large number of investors, team members, and foundations continuously blading, causing the price to drop. However, LayerZero's situation is unique:

- Cleaning up token distribution: They let investors who wanted to exit exit. For example, a16z purchased an additional $55 million worth of tokens in 2025 and locked them up again for 3 years.

- Buyback: LayerZero Labs (a self-sufficient independent entity that provides functionality to the LayerZero network) has bought back tokens and added them to its balance sheet (it bought back $10 million in November and said it would continue to do so).

- Refusing to offer discounts: They didn't conduct any DATs (Direct Token Agreements/Discounted Transfers) for the simple reason that they were unwilling to sell at this price, let alone at a discount. There was little or no selling by insiders; instead, actual insider buying replaced persistent selling pressure.

- Business unification: LayerZero recently unified its product line by acquiring its cross-chain bridge product, Stargate. Stargate revenue is currently being used to repurchase $ZRO.

- Strong cash flow: Buybacks currently account for 50% of revenue, but will reach 100% in a few months. The founders predict revenue will reach an annualized scale of $100 million by the end of the year (see approximately 36 minutes into the podcast above). Given the current market capitalization, even half that level is very impressive. Details of the buybacks are described and documented here: [Buyback Documentation Link].

- A new growth curve: all new product lines will be used to buy back $ZRO. The founders hinted that they have several products in development that could generate up to nine figures in annual recurring revenue (ARR). In addition, some very significant moves are on the horizon, which I don't know the specifics of, but were hinted at in the podcast as potentially related to traditional finance; they plan to announce on February 10th content they've been building for the past 2.5 years.

Caption: A "release announcement" is released using pure encryption.

- Cost Switch: Voting on LayerZero's cost switch will reopen in June. It may not succeed this time, but imagine each LayerZero message having a negligible cost, accumulating over billions of transactions. This will increase existing buyback sources.

- Macro logic: My overarching logic is the "baby booming of the crypto industry," meaning cryptocurrencies are converging with traditional finance. LayerZero holds a dominant market share in the interoperability space. I believe interoperability is a clear "water-selling (shovel and spade)" business for the fully "baby booming" version of crypto that I anticipate will continue to unfold. It also has relevance to stablecoins.

- Flywheel effect: Compared to the current circulating supply and the lack of internal selling, the buyback flywheel will soon become extremely significant. Token unlocking has had no impact on price for several months.

Reset

For better or worse, cryptocurrencies are much more boring than before. Memecoins and alternative L1s no longer have the momentum they had in 2021-2024. Even good perpetual contract DEXs seem to be exhibiting a familiar "euthanasia rollercoaster" pattern.

Caption: Each cycle is lower than the last.

There may still be something undiscovered (perhaps something AI-native) to look forward to, but my baseline scenario is less romantic. The next generation of successful crypto products will hold no appeal for those "trench rats" who see every new meta as a savior. They'll be boring, but attractive to baby boomers because they can make money. That's what happens when baby boomers emerge—they don't buy "atmosphere," they buy "cash flow." In such a world, the only logic is to allocate non-sovereign SoV competitors (BTC + and maybe privacy coins) and industry "water sellers" who benefit from trading and related activities.

The "Moonshot generation" is not dead, just temporarily absent—they will only come back to life when cryptocurrencies prove themselves again with something truly novel and useful.

Disclosure: This article does not constitute investment advice, nor does it represent endorsement of any product/project. At the time of writing, the author holds positions in $ZRO and $HYPE, as well as various private equity investments. All positions are subject to change.