Coin Metrics has just released its latest Bitcoin Network Status Report, which describes the impact of the recent Bitcoin halving on the network. Liquidity indicators show that miner selling pressure has now subsided. The long-term impact of the halving has not yet been seen - while there is no guarantee of future performance, Bitcoin's most important period of appreciation often occurs in the months after the halving.

Key points:

- Between record-breaking transaction fees and massive bids for collectible 'Epic Sat,' Bitcoin halving block miners earn $4.7 million

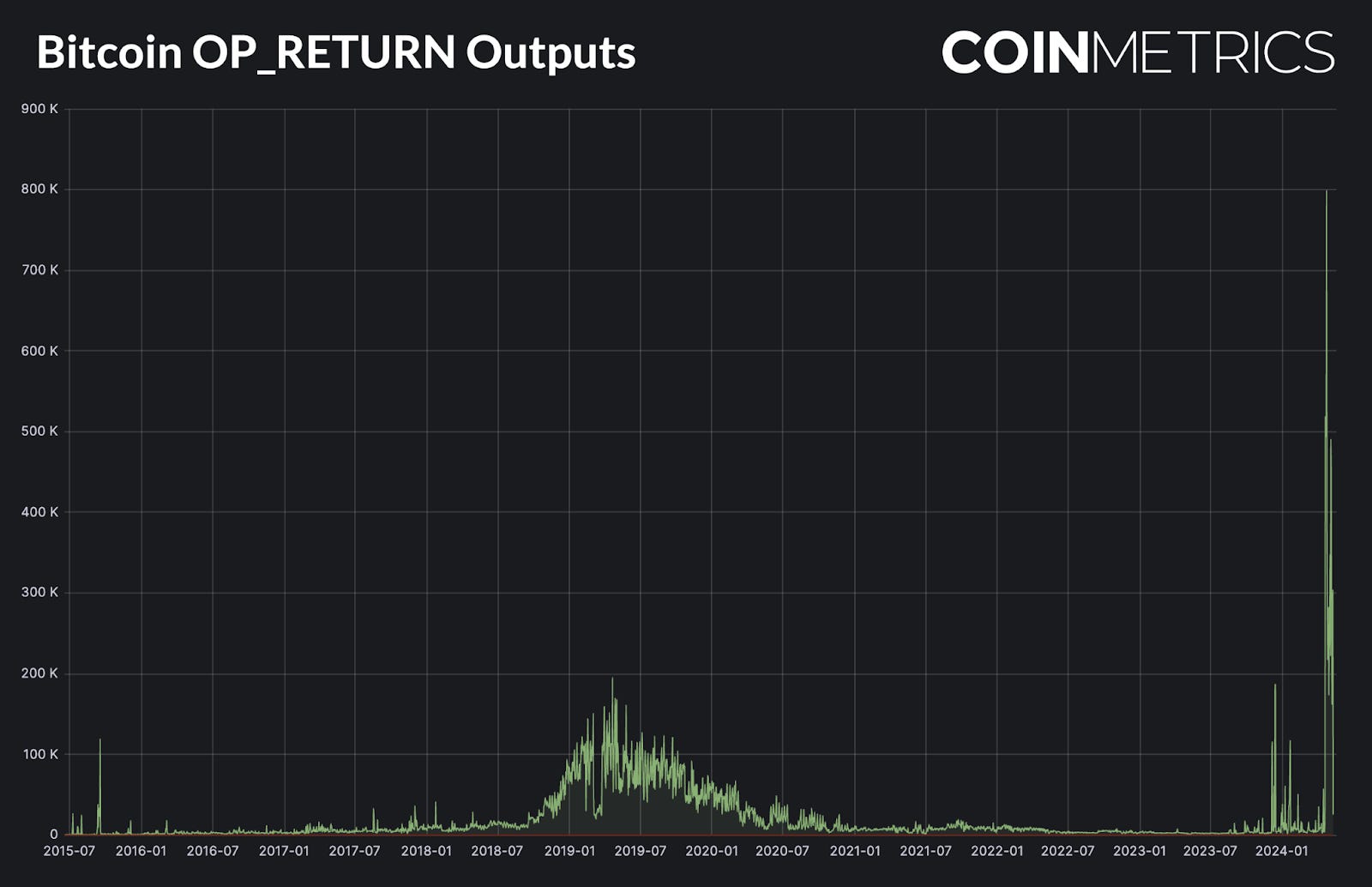

- The launch of the Runes protocol at block 840,000 triggered a surge in OP_RETURN transactions, with the number of OP_RETURN transactions reaching 518K on April 20 and an all-time high of 799K on April 23

- Adjusting miner revenue for electricity consumption, miner revenue per megawatt is currently $1,300, close to the lowest level since the FTX crash in 2022

introduce

Following the predetermined monetary policy, Bitcoin experienced its fourth halving at block 840,000, cutting the block reward from 6.25 BTC to 3.125 BTC. With far-reaching impacts on miner economics, mining pools, and the entire Bitcoin ecosystem, it is critical to understand what happens after the halving. This week’s State of the Bitcoin Network explores the consequences of Bitcoin’s recent block reward halving.

Halving Review

The Bitcoin halving is the most closely watched event in the cryptocurrency industry, with a hard-coded token release schedule determining the rate at which Bitcoin will be issued since the network’s inception. Still, there are many unanswered questions ahead of the halving — can mining survive the change? Will transaction fees offset the reduction in mining revenue? And what impact will this have on the broader Bitcoin community?

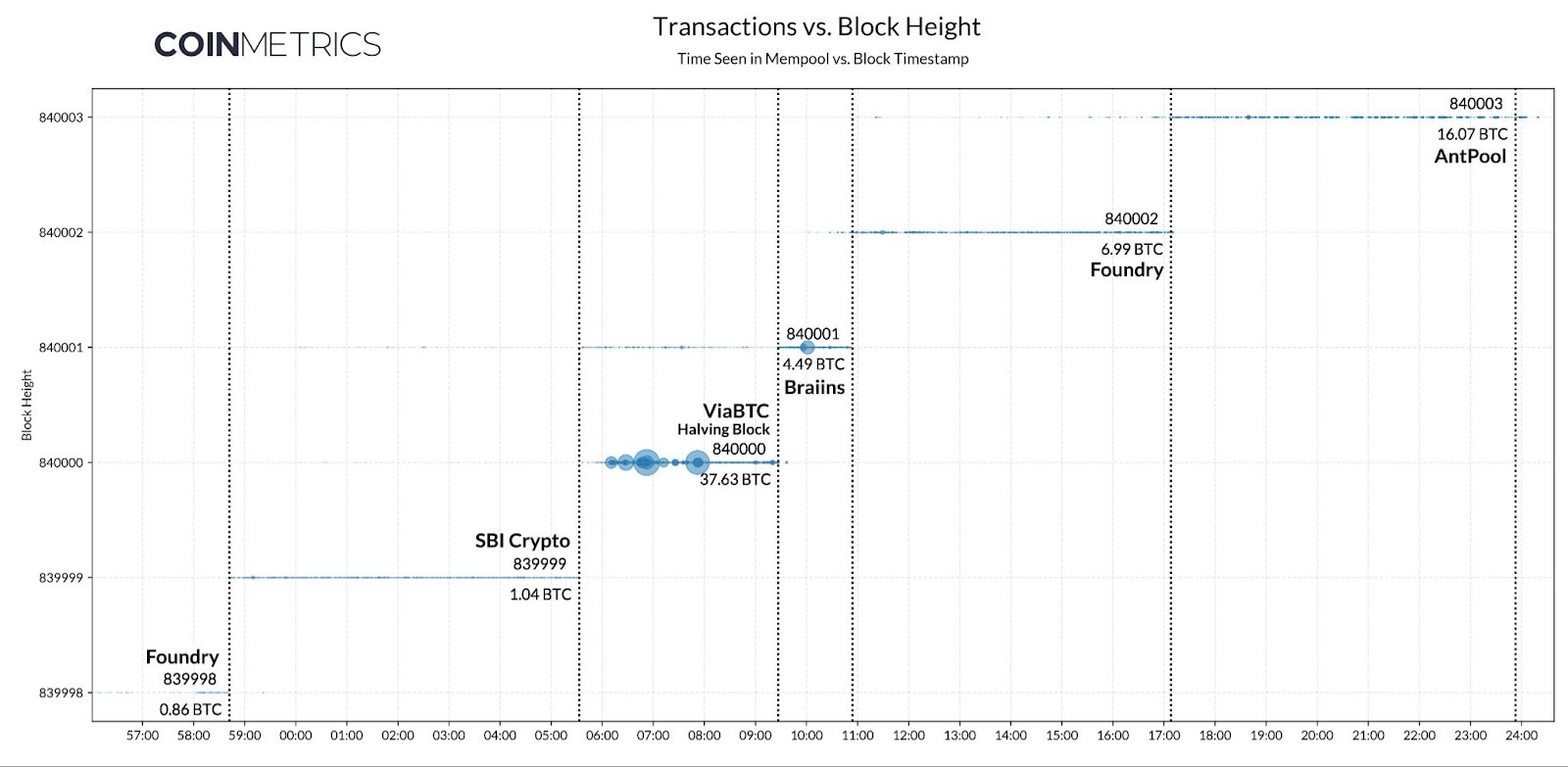

Although the block subsidy for block 840,000 was cut by 50% as expected, the ensuing cascade of fees temporarily eased concerns about mining revenue. The mining pool ViaBTC received the highest block reward, earning 37.63 BTC in transaction fees due to a sudden influx of fee bidding to secure an allocation for the earliest blocks in the halving process.

Between the block subsidy of 3.125 BTC and fees of 37.63 BTC, ViaBTC already makes a decent amount of revenue from mining halving blocks — however, this block has been particularly lucrative thanks to the “Epic Sat.” In addition to supporting NFT-style collectibles, the Ordinals protocol also proposes a (somewhat arbitrary) rarity rating for individual Sat (the smallest subunit of Bitcoin, worth 0.00000001 BTC). While the market value of a single Sat is less than a penny, the “Epic Sat” is designated as the first Sat in the halving block, giving it enormous (subjective) value, as only 4 Sat have been mined in Bitcoin’s history to date.

As the lucky mining pool that got the halving block, ViaBTC isolated the newly born Epic Sat and auctioned it on CoinEx, an exchange run by ViaBTC CEO. After a 3-day bidding war, the collectible was sold for 33.3 BTC (about $2.1 million), making block 840,000 the most valuable batch of transactions in Bitcoin history.

Source: Coin Metrics ATLAS

Epic Sat made a significant contribution to ViaBTC’s revenue, but a series of subsequent blocks continued to climb, breaking records for miner revenue. With the exception of a large “fat finger” fee mistakenly paid by Paxos in block 818,087 (later refunded by AntPool), the top 20 blocks by total revenue (and 88 of the top 100) were all mined on the first day of Bitcoin’s fifth epoch.

Rune Legends

Since their launch in 2023, Ordinals and Inscriptions have been the main drivers of transaction fee revenue for Bitcoin miners. However, on the halving block, a new meta-protocol entered the fray. The Runes token standard (another invention of Ordinals creator Casey Rodarmor) was officially launched at block 840,000, bringing a new wave of on-chain speculation to Bitcoin.

From a technical perspective, Runes sought to improve upon earlier efforts to connect ERC-20-style fungible tokens to the Bitcoin blockchain. While Inscriptions was originally designed to enable on-chain NFTs, tinkerers quickly repurposed the technology to create “BRC-20,” embedding JSON-formatted text into transactions as a primitive mechanism for creating and transferring tokens. BRC-20s like ORDI soon soared to billions of dollars in market capitalization and were listed on exchanges like Binance and OKX.

While popular among speculators, BRC-20 has been widely derided for its technical inelegance, bloated blockchain, and need for complex indexing solutions. To bridge these gaps, Runes bypasses inscriptions entirely, leveraging Bitcoin’s long-standing OP_RETURN field to encode compact token protocol messages. In the 24 hours following Runes’ release on March 20, Bitcoin set a new record of 518.6K OP_RETURN outputs, followed by a record high of 798.7K OP_RETURN outputs on March 23.

Source: TxStats

Excitement around Runecoin peaked after the halving, with 97% of fees in block 840,000 going to being one of the first to be etched. In the world of on-chain collectibles, there’s an aura of prestige associated with being one of the first to launch. The etcher of Runecoin 840000:1 (aka Z•Z•Z•Z•Z•FEHU•Z•Z•Z•Z•Z) paid miners 6.73 BTC for the first slot in the halving block. The bet appears to have paid off, as “FEHU” is now the highest-ranked Rune by market cap, with a valuation of $2.4 billion. Runecoin revenue has since declined in size, but remains a significant contributor to miner revenue, accounting for roughly 50% of fees per block over the past week.

Source: Coin Metrics ATLAS

Since the protocol launched at the halving block, miners have earned a total of 2,000 BTC through Rune fees. Nearly half of that occurred in the first 24 hours of Rune’s debut, with momentum stabilizing less than 5 days later. However, Rune is still in its infancy, and miners are benefiting from a small burst of revenue as highly anticipated projects enter the market. At block 842,166, the winner of the ViaBTC auction linked Epic Sat to a new rune called EPIC•EPIC•EPIC•EPIC, causing fees to spike in 4 hours as speculators minted 50 million tokens.

Source: Coin Metrics ATLAS

Despite setting fee records at launch, Runes was later seen as a flop, with interest waning and failing to match the pre-halving hype. Still, it took the Ordinals ecosystem months to build the infrastructure needed for meaningful liquidity, and Runes has yet to be validated in the form of a listing on a major exchange, trading primarily on niche collectibles platforms. Meanwhile, miners are holding their breath — revenues are falling to survival levels, requiring the industry to re-examine assumptions about forward-looking profitability.

Hash power withers

After the halving, simple revenue measures show that mining revenues remain relatively high, averaging close to $30 million per day. However, total revenue ignores an important consideration - miners are also spending significantly more on electricity. According to Coin Metrics estimates, the network currently consumes about 21.5 GW of electricity, a 2x increase over the past 2 years.

The ratio of mining revenue to electricity consumption gives us a better picture of how miners are earning relative to their main operating expense. Mining revenue per megawatt (MRPM) is currently around $1,300 per day, barely above the daily cost of $960/MW at ultra-low electricity prices of $0.04/kWh. This brings electricity-adjusted revenue to levels not seen since the collapse of FTX, highlighting how tight the situation is for miners. Larger miners earn more per megawatt (thanks to upgraded hardware) and have long-term contracts at lower electricity prices - nonetheless, MRPM suggests that the “average” miner is facing significant financial pressure in the post-halving era.

A major concern before each halving is the selling pressure that miners may bring to the market. Due to the direct impact on revenue, miners may need to sell newly issued Bitcoin or liquidate existing assets to pay for operating expenses or fund expansion efforts, such as acquiring more efficient ASIC mining machines.

However, Bitcoin’s daily issuance provides us with a baseline for selling pressure, which has dropped from 900 BTC to 450 BTC after the halving. Notably, the issuance of approximately $55 million before the halving correlates closely with Bitcoin’s 1% liquidity asking price, highlighting the market’s ability to absorb miner selling. With issuance reduced by approximately $26 million, Bitcoin’s sell-side liquidity remains strong, suggesting that the market can easily absorb additional selling pressure from miners without significantly affecting BTC prices.

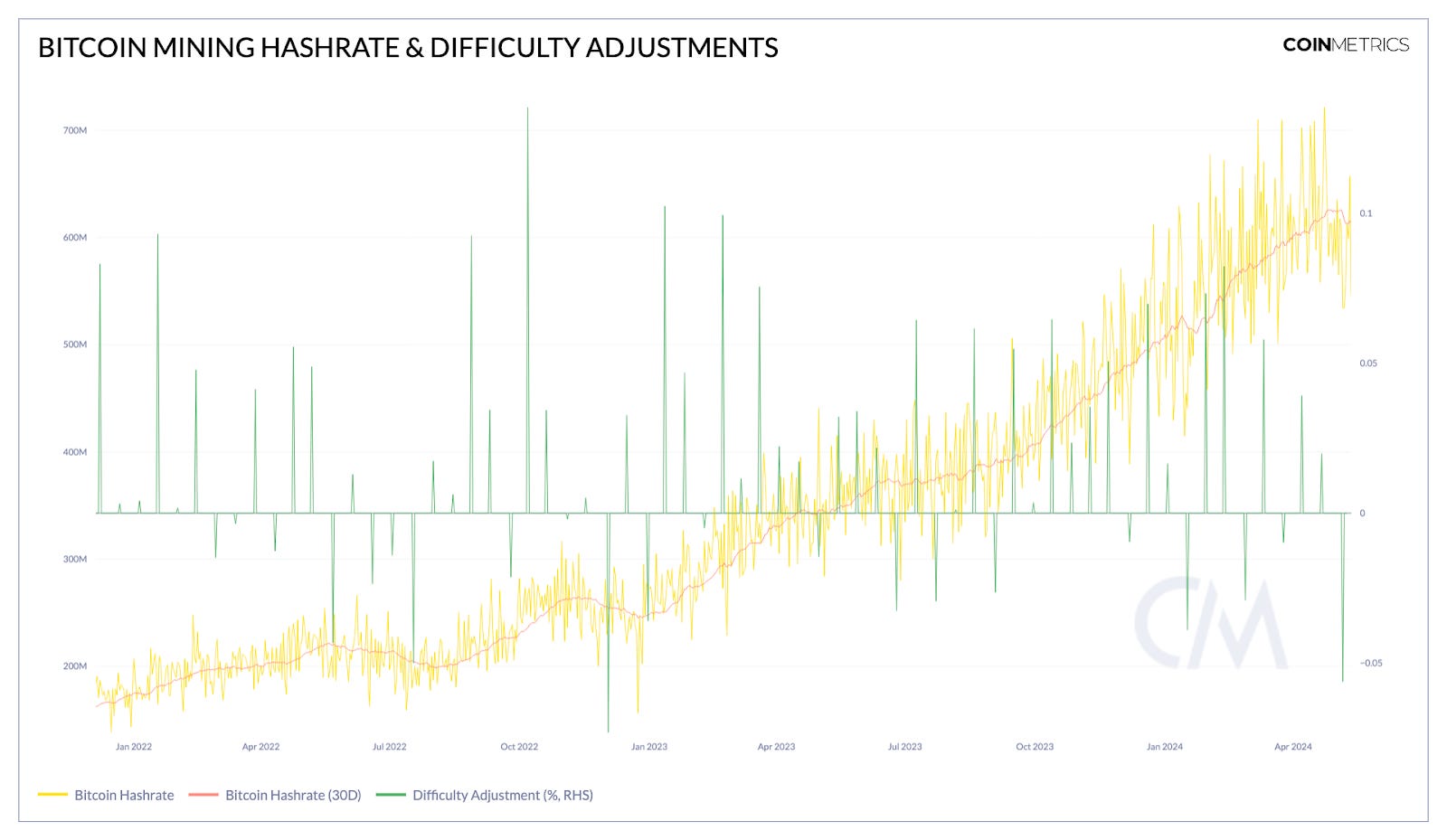

Financial pressure on miners has increased due to reduced profits caused by the reward halving, coupled with increased electricity costs. This is evidenced by the 11.2% drop in weekly hashrate from 650 EH/s to 577 EH/s, and miners are evaluating the feasibility of operating amid tightening margins. However, Bitcoin’s recent -5.62% difficulty adjustment (the largest drop since the end of 2022) will alleviate some of the pressure by reducing the work required to mine new blocks.

Source: Coin Metrics Network Data Pro

in conclusion

The reduction in Bitcoin issuance is the most predictable event in cryptocurrency, but the 2024 halving is a notable event for a number of reasons. Compared to past halvings, mining has reached unprecedented scale, with millions of dollars of investment in hardware and infrastructure. With fees unable to offset the decline in overall subsidies, it is questionable whether many large-scale operations can survive. New protocols like Rune provide a catalyst for increased revenue, but these markets are still immature, resulting in a large gap in mining profitability assumptions.

Regarding the impact of the halving on market structure, it can be said that this adjustment has been "priced in" for many years. However, liquidity indicators show that miner selling pressure has now weakened, and issuance is far below the threshold required to significantly drive BTC prices. In any case, the long-term impact has not yet been seen - while future performance is not guaranteed, Bitcoin's most important appreciation period tends to occur in the months after the halving. At present, the demand side has regained dominance and the impact of the halving on the cryptocurrency narrative has gradually disappeared.

{kind=link}

{kind=link}

{kind=link}