The Story of Ethereum Staking So Far

By: Tanay Ved & Matías Andrade

Key Takeaways:

Ethereum’s staking ecosystem has come a long way, evolving from its PoW beginnings to PoS with The Merge, with the emergence of key innovations like liquid staking, restaking, and the arrival spot Ether ETFs shaping its journey.

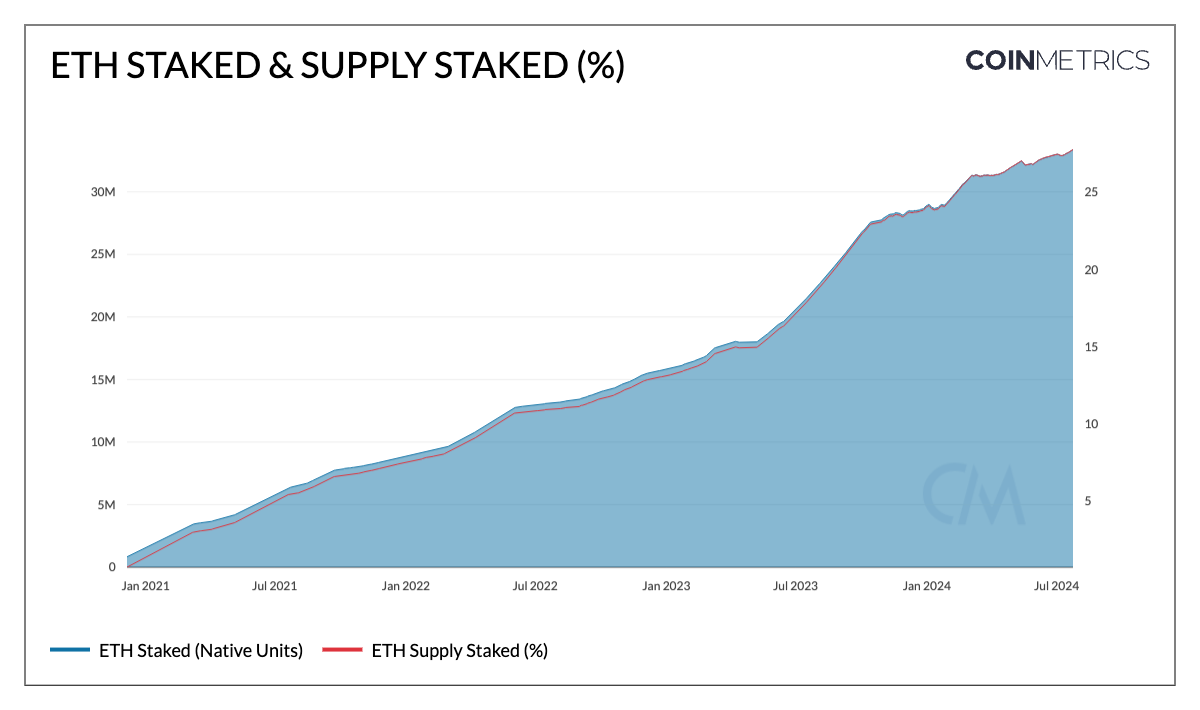

Approximately 33.5 million ETH, valued at ~$115 billion, is staked on the Ethereum consensus layer, representing 27.8% of the total ETH supply.

There are currently 1.05M active validators participating in the network, growing by 15% in year-to-date in 2024.

Brief Background on Ethereum Staking

Staking is the beating heart of proof-of-stake (PoS) blockchains like Ethereum. With its transition from a proof-of-work (PoW) network to proof-of-stake (PoS) in 2022, participants are now required to commit ‘stake’ by depositing a minimum of 32 ETH as collateral to become an active validator on the network—the central economic actor in this system.

Staking is fundamental to how the network reaches consensus—a process whereby network participants (validators) propose, verify and attest to new blocks on the blockchain, with the value of staked assets contributing to its economic security. A validator's stake serves as an economic incentive for participants to act in the best interests of the network. On the one hand, validators are rewarded with Ether in return for doing these duties honestly, or risk having their stake penalized or slashed for malicious behavior.

Introduction

In light of spot Ether ETFs going live on July 23rd, and the regulatory clouds surrounding staking, we believe it’s important to understand the fundamental role staking plays within the Ethereum network. In this issue of Coin Metrics’ State of the Network, we uncover Ethereum's staking journey so far, understanding how the $115B+ staking ecosystem emerged, developed and where it’s headed.

From the transition to PoS with The Merge, to withdrawals with Shapella, the emergence of liquid staking and restaking and most recently, the introduction of spot Ether ETFs—staking is undoubtedly one of the central pillars of Ethereum's roadmap, making it pivotal to the entire ecosystem.

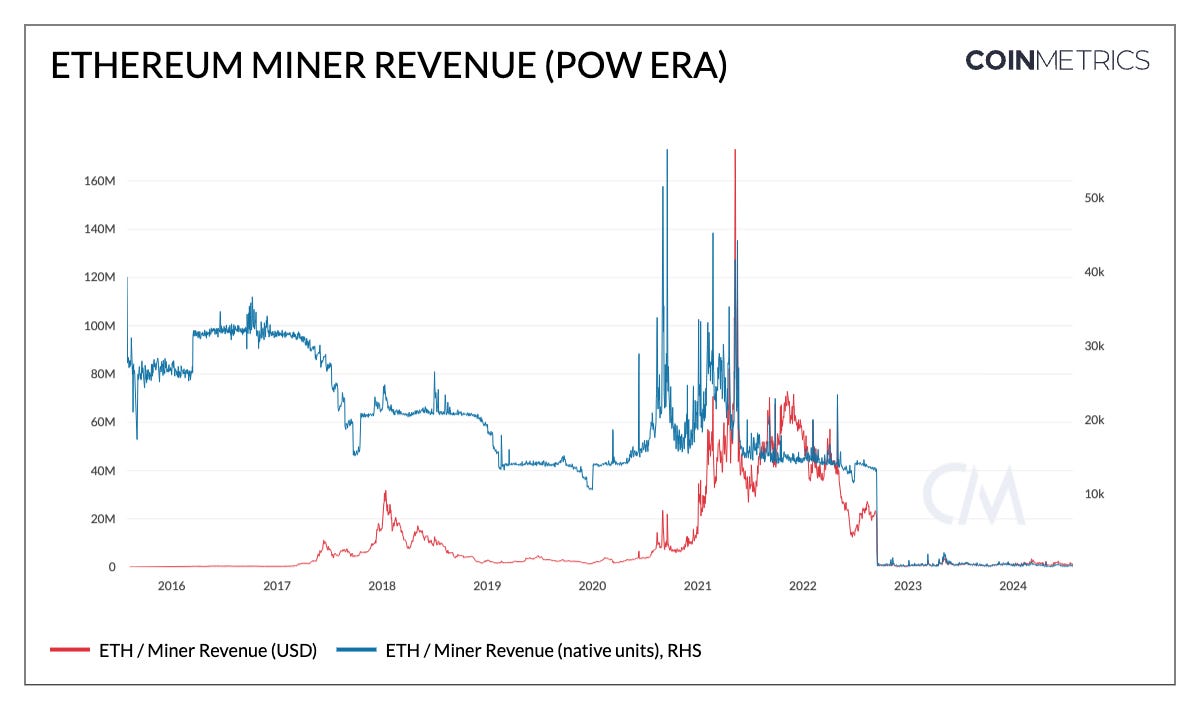

End of the PoW Era (2015 - 2022)

Ethereum’s genesis block was recorded on July 30th, 2015. For more than seven years since, the chain was secured by a proof-of-work (PoW) consensus mechanism. Similar to how the Bitcoin blockchain functions today, this entailed large clusters of hardware including general processing units (GPUs) and eventually application-specific integrated circuits (ASICs) which expend computational resources to find the hash of a nonce. The miner that found a valid nonce, would then broadcast the new block to the chain, being rewarded in the form of block rewards (issuance of ETH) and fees for the transactions included in a block.

However, as network difficulty (computational effort needed to find the nonce) increased, the energy resources consumed by miners grew even larger. In as early as 2016, Vitalik Buterin advocated for Ethereum to switch to proof-of-stake (PoS) to address bottlenecks such as energy consumption, scalability and network sustainability to position Ethereum for future growth. This marked the end of Ethereum miners giving way to validators.

Introduction of the Beacon Chain (2020)

In October 2020, the staking deposit contract was deployed on the Ethereum execution layer. This was the gateway to participants who wished to stake their ETH, whether through self-hosted infrastructure (solo staking) or through staking as a service providers like Figment, pooled staking platforms such as Lido & RocketPool or centralized-exchange staking programs that eventually emerged.

Source: Coin Metrics Network Data Pro

Currently, 33.5M ETH (valued at ~$115B) is staked on the Ethereum consensus layer, with 1.05M active validators participating in the network. This represents 27.8% of ETH’s total supply, also referred to as the “staking ratio”. Staking ratios can vary widely due to differences in implementation across PoS blockchains.

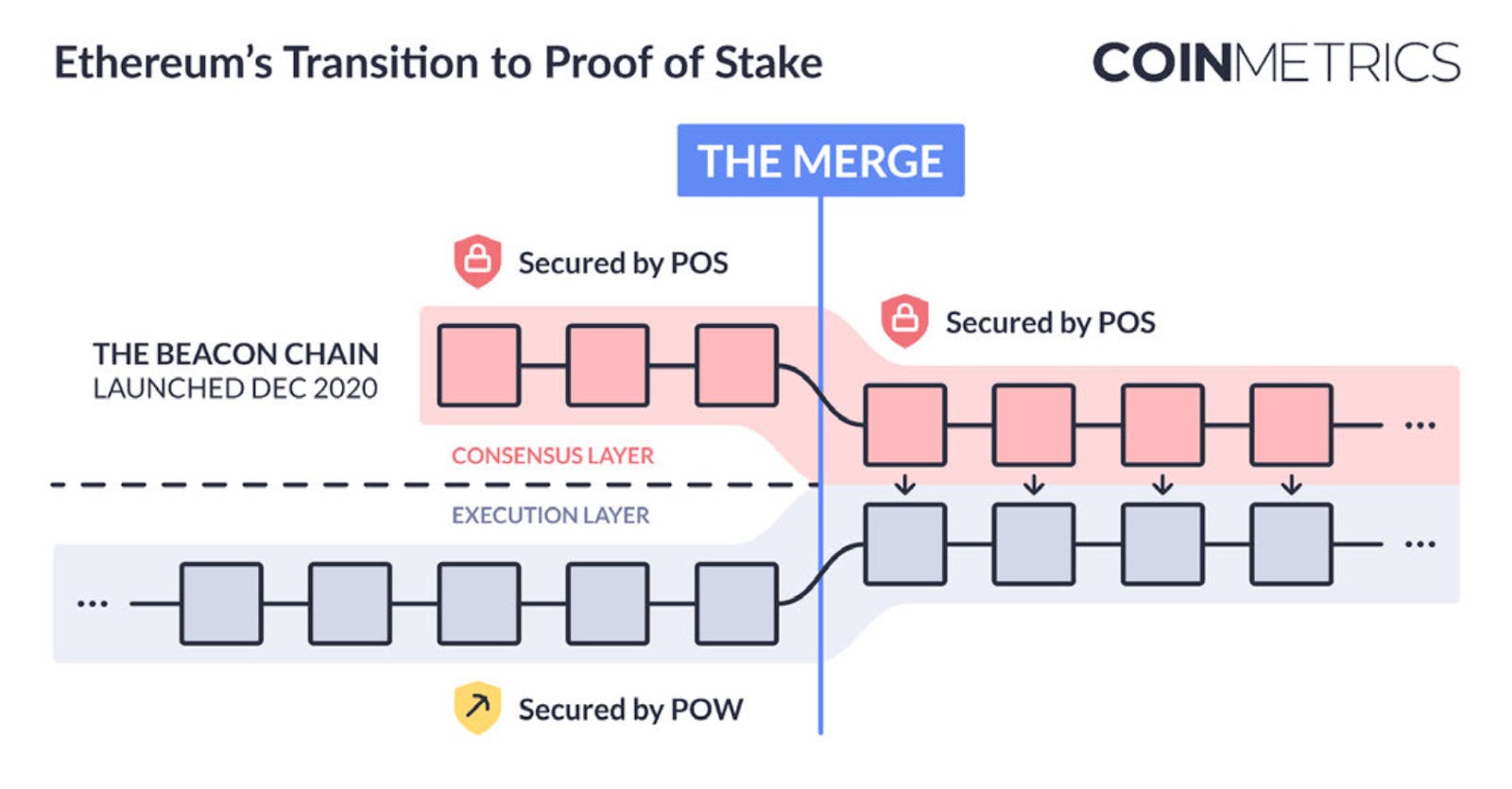

In December 2020, the Beacon Chain (also known as the Consensus Layer) was launched as a parallel blockchain to Ethereum's mainnet, adopted through EIP-3675. It marked the first step towards transitioning from Proof of Work (PoW) to Proof of Stake (PoS). This chain was specifically designed to handle the PoS process, managing validator balances, duties (attesting & proposing new blocks) and incentives (rewards & penalties) to achieve consensus. This laid the groundwork for the eventual merging with the mainnet, the layer that hosts a vast array of smart-contracts and dApps powered by the Ethereum Virtual Machine (EVM).

The Merge: Transition to PoS (2022–Present)

The integration of Ethereum’s two disparate systems, the “Execution Layer” (also known as mainnet) and “Consensus Layer” (also known as the Beacon Chain) is now widely recognized as “The Merge”. This represented the official switch to using the Beacon Chain as the engine of block production.

Miners were no longer the means of producing valid blocks. Instead, in proof-of-stake, validators adopted this role and are now responsible for proposing blocks and processing the validity of all transactions. In return for these duties, they earned rewards via newly issued ETH, transaction fees that users voluntarily pay as “priority tips,” and maximal extractable value (MEV).

As covered in our report: Mapping out the Merge, the shift to PoS brought about significant changes to Ethereum’s validator and monetary economics. Under PoW, Ethereum’s daily issuance was ~13.5K ETH, an annual inflation rate over 4%. However, with the changes implemented in EIP-1559, introducing a base fee burn mechanism and priority fees which go to validators, ETH’s daily issuance is closer to 0, with a current annualized inflation rate of 0.67%.

The Rise of Liquid Staking Derivatives

At the time, certain bottlenecks existed in Ethereum’s PoS system that prompted the rise of pooled staking providers and liquid staking tokens (LST’s). Some of these problems included:

Inability to Withdraw Stake: Staking was a one-way operation for many months. ETH being staked could only flow from the execution layer (where the staking deposit contract lives) to the consensus layer, preventing redemptions.

Illiquidity of staked ETH: Inability to withdraw meant that staked ETH was effectively illiquid, preventing any further utility.

Capital & Operational Requirements: The minimum capital requirement of 32 ETH, coupled with the need to run and maintain Ethereum node software (including execution and consensus layer clients), presented barriers to entry for many potential stakers, limiting widespread participation in the network's validation process.

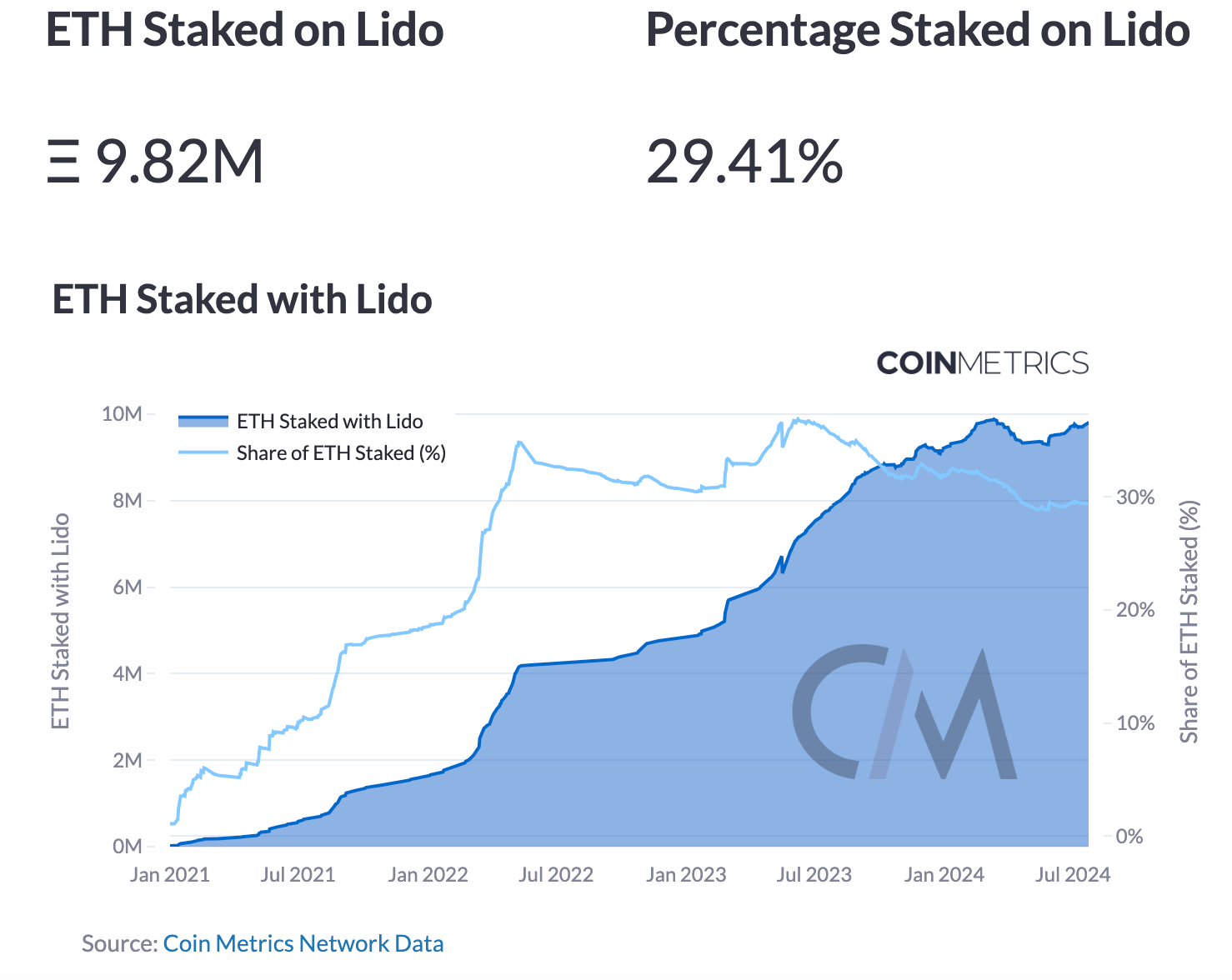

As a result, several pooling solutions such as Lido, Coinbase and RocketPool emerged, capitalizing on this lucrative opportunity. They enabled users to participate with any denomination of ETH, managing node operation by accumulating deposits across users to create a validator on the beacon chain. Users were provided with a liquid receipt token representing the underlying staked assets—known as a liquid staking token—which earned staking rewards without being “locked”. Ultimately, this lowered the barriers to entry for staking, fueling the growth of the sector and allowed a larger participant base to secure the Ethereum network.

Source: Coin Metrics Staking Dashboard

Currently, 9.8M ETH (valued at ~$32B) is staked through Lido. This is a 29% market share of all staked ETH, and is also referred to as “Lido dominance”. Exceeding a high threshold (33%) of ETH staked through a single entity can introduce centralization risks. This has prompted the need for a decentralized validator and node operator sets, managed through DAO governance or innovations like DVT.

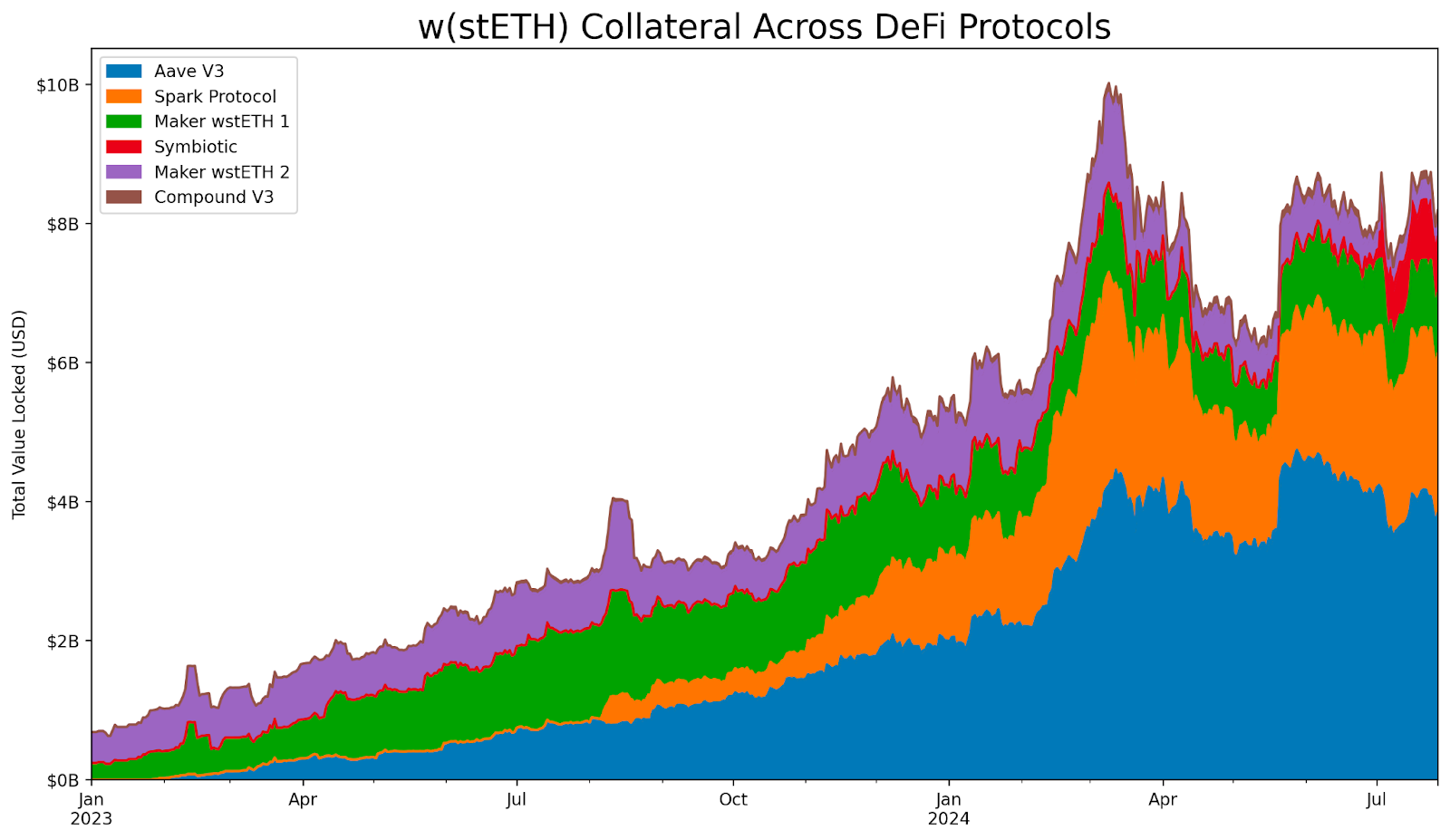

In addition to making participation more accessible, pooled staking fueled the utility of liquid staking tokens (LSTs) in the wider on-chain ecosystem. LST’s like stETH and wstETH (wrapped-staked Ether) issued by Lido have garnered significant network effects being widely utilized in decentralized finance (DeFi) applications, whether as collateral on the largest lending protocols or as liquidity on decentralized exchanges (DEX’s).

Source: Coin Metrics ATLAS

Currently, more than 2M ETH ( ~$10B in value) is used as collateral backing loans across DeFi lending protocols like Aave v3 & Spark. LSTs are also prevalent forms of liquidity reserves on DEX’s, layer-2’s as well as economic security on restaking protocols.

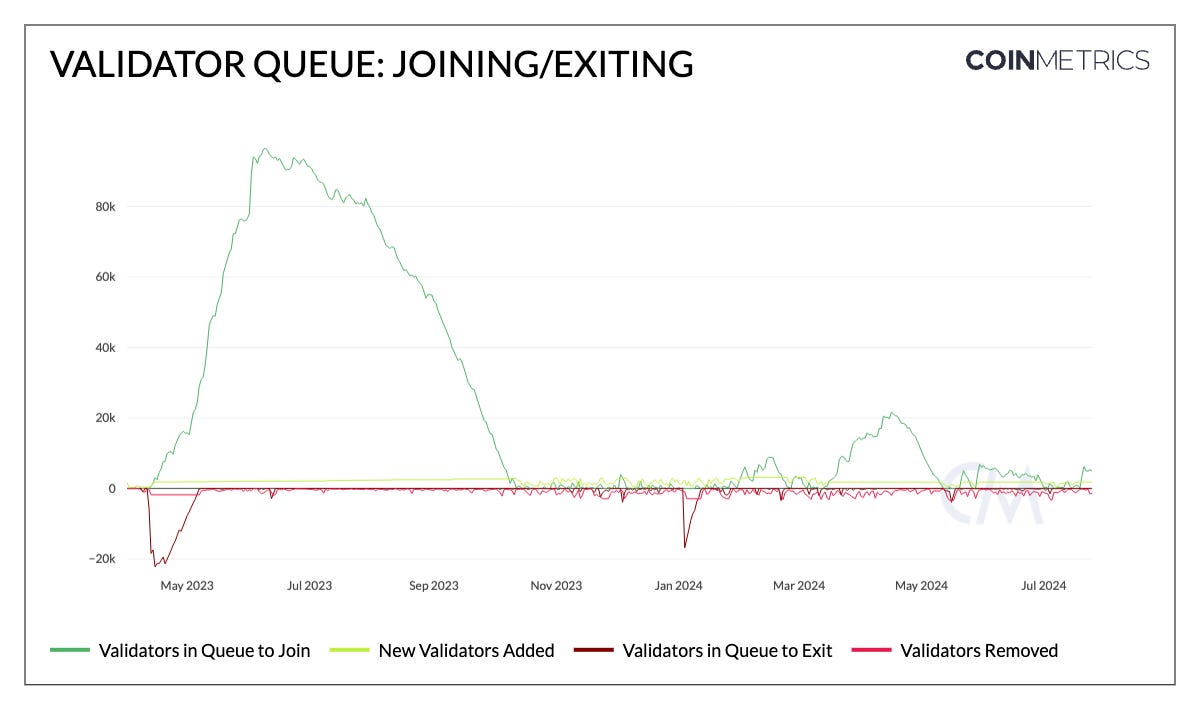

Shapella: Withdrawals Enabled (2023)

The arrival of the Shanghai and Capella upgrade on April 12th 2023 (dubbed Shapella), closed the loop on staked ETH, eventually enabling redemptions from the Beacon Chain. Validators were now able to enter and exit the PoS system subject to a validator queue and churn limit (a cap on how many validators can be activated per epoch, currently set to 8 through EIP-7514 in Dencun).

Source: Coin Metrics Network Data Pro

Currently, 4000 validators are in the staking entry queue, down from a high of 96K in June 2023 and 21K this April.

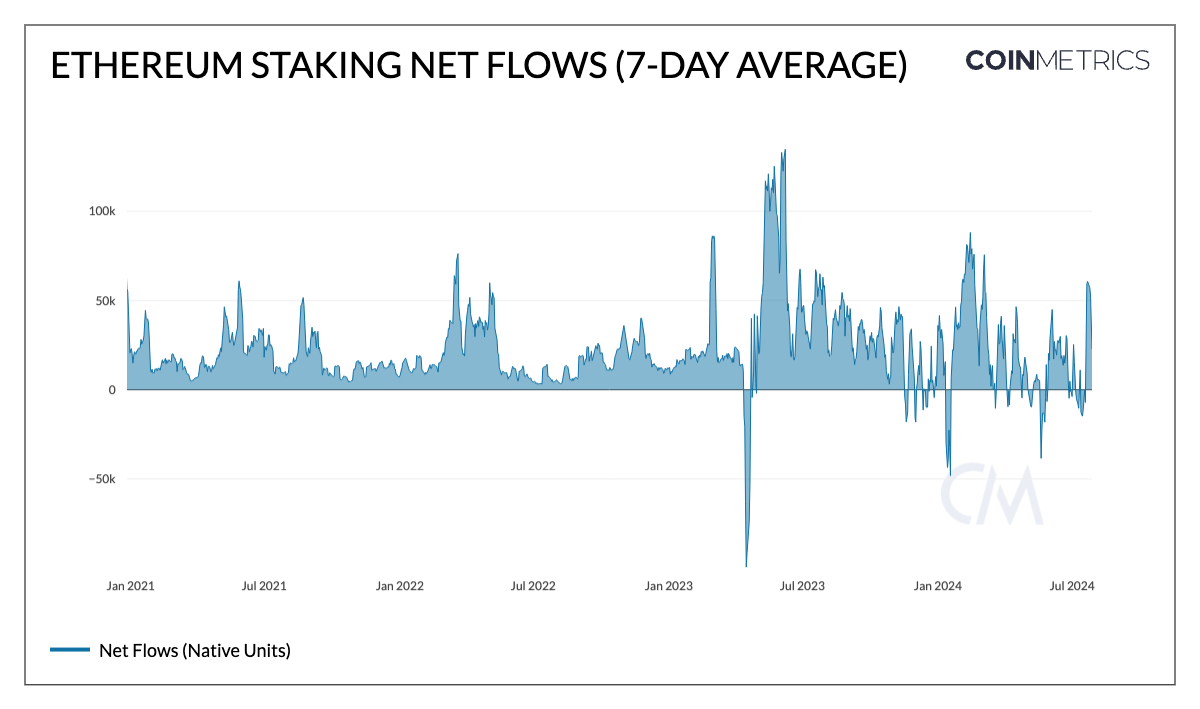

While the validator entry queue may have flattened out relative to last year, deposits of staked ETH continue to outpace withdrawals. Since the Shapella upgrade, 30M ETH has been deposited to the consensus layer, while 17M ETH has been withdrawn. The discrepancy seen between a lower number of validators in the entry queue and increasing deposits may be partially explained by the popularity of liquid staking, resulting in a growing amount of ETH staked without adding validators directly.

Source: Coin Metrics Network Data Pro

The Emergence of Restaking

With the launch of EigenLayer mainnet in 2023, restaking has quickly become one of the fastest-growing verticals in the crypto ecosystem. While staking ETH secures the Ethereum network, restaking allows the same staked assets to secure external services built on Ethereum, such as oracle networks, data availability layers, bridges and other middleware using either natively staked ETH or liquid staking tokens (LSTs). This innovation helps emerging protocols bootstrap security without the high costs of sourcing their own validators.

Restaking unlocks greater capital efficiency of staked ETH and extends Ethereum’s security model across the broader ecosystem. However, it also introduces risks in managing staked assets and liquid representations of restaked assets (LRTs) across various networks with different risk profiles. Although still nascent, the restaking landscape has expanded beyond Ethereum to other chains like Solana, with new entrants like Symbiotic and Jito restaking showcasing its growing significance.

The Launch of Spot Ether ETFs

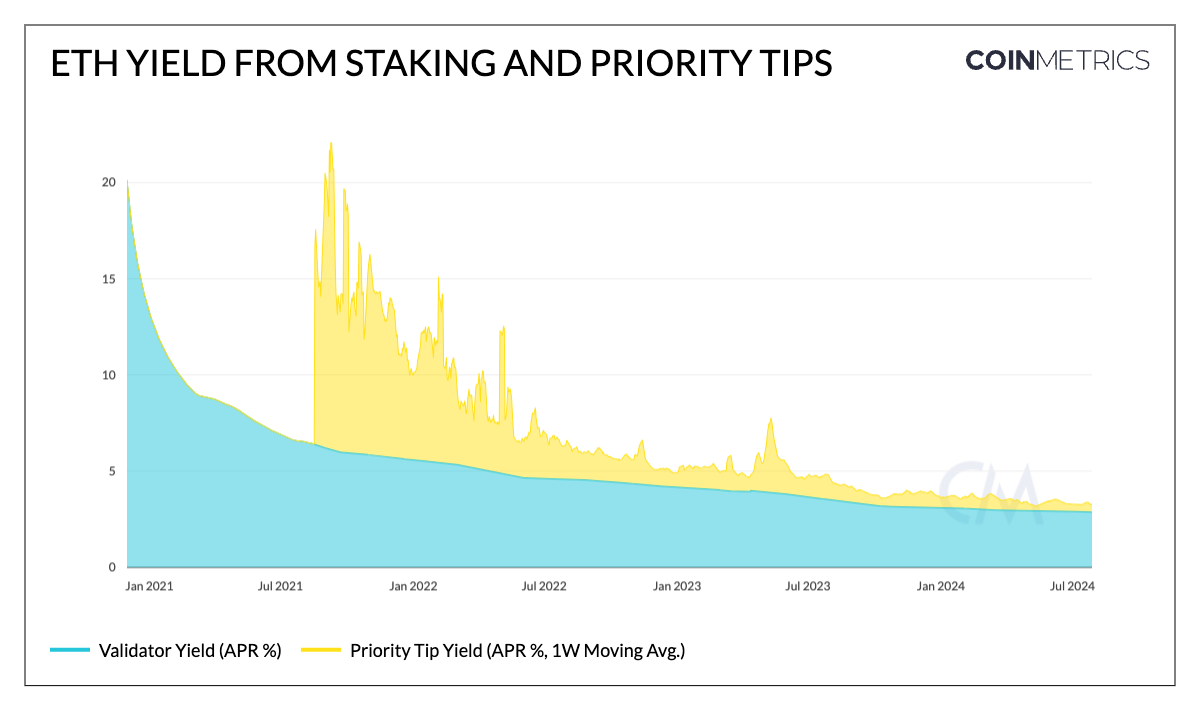

This brings us closer to today—with the launch of spot Ether ETFs commencing last week. While this is exciting news for the market, the current structure of Ether ETFs prevents issuers from participating in staking activities. This represents an opportunity cost for investors who would forego an additional ~3% in the form of staking rewards, a key component of staking.

Validators are incentivized to participate in the consensus process by being rewarded in the form of ETH issuance, priority tips and maximal extractable value (MEV), which are derived from the consensus layer (CL) and execution layer (EL). The current ETH staking annual percentage rate (APR %) excluding MEV, stands at just over 3%. While this may impact investor demand for ETFs, it has sizable ramifications for the Ethereum network, such as:

The expected APR return for validators, stakers and overall network inflation

Potential effects on staking participation and stake decentralization

Source: Coin Metrics Network Data Pro

Any decision to incorporate staking rewards would require a careful consideration of these factors to balance network security and economic sustainability of the Ethereum ecosystem.

What’s on the Horizon?

Ethereum’s staking ecosystem has come a long way since “The Merge” and its future direction hinges on a multitude of converging factors.

In light of Ethereum’s staking ratio exceeding 25% of total supply and the number of validators crossing the one millionth mark, researchers and the community alike are considering altering Ethereum’s issuance curve and increasing validators' max effective balance. These proposals stem from the concerns around ETH’s growing staking ratio and centralization tendencies around staking pools, with incentives favoring liquid staking tokens over plain ETH. Additionally, increasing the validators max effective balance from 32 ETH to 2048 ETH is being considered to control the exponential growth of the validator set, reducing overhead for the consensus layer.

Source: Coin Metrics Network Data Pro

The growth of liquid staking & restaking, the arrival of spot Ether ETFs, regulatory developments around staking and potential changes to validator & issuance dynamics present a complex, interconnected landscape that will steer Ethereum’s PoS system for the years to come.

Check out our new Ethereum Staking Dashboard, illuminating the staking ecosystem

Be sure to check out our previous issues on Staking, from upgrades like “The Merge” and “Shapella” to deep dives into liquid staking and their associated risks.

Coin Metrics Updates

This quarter’s updates from the Coin Metrics team:

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

Subscribe and Past Issues

As always, if you have any feedback or requests please let us know here.

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.