Source: Financial Time Difference

Bad news came one after another, Japan and South Korea collapsed across the board, and the US futures market also collapsed.

The Japanese stock market collapsed again after a 5.8% plunge. In the early trading of August 5, the Nikkei 225 index plummeted 7%, and the plunge in the Topix index triggered a circuit breaker.

Since its July high, Japanese stocks, including the Nikkei 225 and the Topix index, have fallen by more than 20% in total, falling into a technical bear market.

At the same time, the volatility of the Nikkei 225 soared 50%, reaching a new high since the global crash in April 2020.

In addition, the Japanese bond market also fluctuated violently, triggering the circuit breaker mechanism.

Meanwhile, South Korea's KOSPI index fell more than 4%, Australia's S&P/ASX 200 index fell 2.1%, and Nasdaq 100 futures fell 2%.

It is clear that global financial markets have collapsed again.

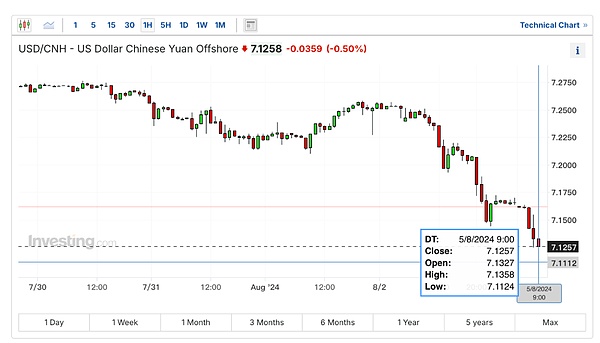

There are two types of assets that are very strong, the Japanese yen and the Chinese yuan.

After soaring 1,000 points last Friday, the offshore RMB exchange rate soared nearly 500 points again, breaking through 7.12 to 7.1124. It has now recovered to around 7.13.

The USD/JPY exchange rate continued to appreciate, reaching 144.7 at one point.

Why did the global market collapse again?

In addition to the global recession trade that prevailed last Friday, the carry trade collapsed, and profit taking was realized, there was another big news: expectations of war in the Middle East have increased sharply.

First there was a series of assassinations, the latest of which was the killing of Hamas political leader Ismail Hanija and Lebanese Hezbollah military leader Fouad Chokr.

Then the two sides began to retaliate against each other.

On August 5, the United States told the G7 that Iran could attack Israel within the next 24 hours.

Regardless of whether the Middle East war will escalate, the market expects that war is coming and then the market will collapse.

Another thing is that Buffett sold a large number of stocks and reserved a huge amount of cash.

Berkshire Hathaway reduced its holdings of Apple shares in the second quarter to about 400 million shares from 789 million shares in the first quarter, a drop of nearly 50%.

The stock sell-off has brought the company's cash reserves to a record $276.9 billion (about 1.98 trillion yuan), compared with $189 billion at the end of the first quarter.

The market believes that Buffett's selling of stocks and hoarding of cash is a sign that a global financial crisis is approaching. On the one hand, he has to sell stocks, and on the other hand, he has to hoard a large amount of cash to prepare for buy the dips.

So, the market followed suit and sold off, causing global stock markets to continue to collapse.

Finally, let’s talk about a question: why did the Japanese yen rise so sharply, but the Japanese stock market collapsed one after another?

Logically speaking, with the yen soaring, yen assets should be valuable, and with capital flowing into the yen in large quantities, the Japanese stock market should be rising, right?

Some people say that Japan is both an importing and exporting country. Energy and raw materials are imported, while industrial products such as automobiles are exported. Therefore, the yen has a range, and the Japanese economy will be good within this range. If it exceeds this range, there will be problems.

This statement has some truth to it, but it is not the reason for the trend of the yen and Japanese stocks, nor is it even the reason for the good or bad performance of the Japanese economy.

To explain this "divergence", we have to start with the triggering factors of this round of "yen depreciation and Japanese stock market surge".

First of all, it is clear that the depreciation of the yen and the surge in the Japanese stock market are not the so-called "depreciation bull", which means that the currency has depreciated, exports have improved, the economy has improved, and finally the stock market has risen.

This round of Japanese currency depreciation and Japanese stock market surge since 2021 was entirely caused by "arbitrage", and the representative figure is Buffett.

How does Buffett make arbitrage?

In the early stage of the yen's depreciation, yen was borrowed to form yen liabilities, and then the borrowed yen was used to buy Japan's five major trading companies (Itochu Corporation, Marubeni, Mitsubishi UFJ, Mitsui & Co., and Sumitomo Corporation).

Why do you do this?

First, Buffett bet on the general trend of the depreciation of the Japanese yen. He borrowed Japanese yen in the early stage of the depreciation. When the Japanese yen depreciated, he could earn a Japanese yen exchange rate difference, thereby reducing the Japanese yen debt burden.

For example, when Buffett borrowed Japanese yen, 1 U.S. dollar was worth 103 yen, and finally the yen depreciated to 161, which means that the yen depreciated by more than 50% in nearly three and a half years.

If Buffett repaid the Japanese yen he had borrowed at 161, the US dollars he used could be reduced by at least 36%.

It used to take $100 to pay off the Japanese yen debt, but now only $64 is enough.

Note that the key to this operation is that the Japanese yen has been depreciating.

Secondly, after Buffett borrowed Japanese yen, why did he invest in the Japanese stock market?

In fact, to be precise, after Buffett borrowed the yen, he invested in high-dividend Japanese stocks, such as Itochu Corporation, Marubeni, Mitsubishi UFJ, Mitsui & Co., Ltd. and Sumitomo Corporation.

This kind of operation is a way to make money out of nothing, which can be called risk-free arbitrage.

Because the Bank of Japan had not yet raised interest rates, the interest rate on the yen was extremely low, and the 10-year US Treasury bond rate was only 0.5%. However, the dividends of these high-yield stocks in Japan were as high as 5%.

In other words, Buffett borrowed Japanese yen to invest in the Japanese stock market, which was equivalent to making money out of nothing, and he made a profit of 4.5%.

Note that the key to this operation is that Japan's interest rates have remained low.

Finally, more and more people followed Buffett's example, and the most obvious result was that the Japanese stock market continued to soar.

As the Japanese stock market soared, investors earned another profit, namely, price difference profit.

Note that the key to this operation is that the Japanese stock market must rise.

Therefore, over the past three years, Japanese yen interest rates have remained low, the Japanese yen exchange rate has continued to hit record lows, and the Japanese stock market has continued to hit record highs.

But recently, the situation has reversed, with one trigger: rising yen interest rates.

Japan ended its 17-year zero interest rate policy as early as March, and then after the market digested it and the anticipation of the Federal Reserve's policy, the yen exchange rate "bottomed out" in early July.

This logic is easy to understand. When the Japanese yen raises interest rates and expectations of a US dollar interest rate cut increase, the Japanese yen exchange rate will stop depreciating and start appreciating.

This market trend is contrary to the first and second points of arbitrage trading mentioned above.

In order to prevent the cost of Japanese yen liabilities from rising, the wise thing for investors to do is to repay their Japanese yen liabilities as soon as possible, so as to pay less interest.

In order to prevent losses from the yen exchange rate difference, the clear approach for investors is to quickly pay off their yen debts before the yen appreciates.

How can they pay back the yen? The money they borrowed is all in the Japanese stock market.

It’s very simple, just sell the Japanese stocks quickly!

As the yen interest rate rises and the yen exchange rate appreciates, people become more aggressive in "closing" arbitrage transactions, and the first step is to sell off Japanese stocks.

So we see the contradictory market combination of "Japanese stock market plummeting" and "appreciation of the yen exchange rate".