In the newsletter, we wrote about the market shocks from earlier this week, the expansion of Ethena to Solana, and the launch of the much-anticipated Bitcoin app Fedi.

In the newsletter, we wrote about the market shocks from earlier this week, the expansion of Ethena to Solana, and the launch of the much-anticipated Bitcoin app Fedi.

Macro headwinds lead to weak market

Global risk assets repriced lower on Monday following last week’s surprise rate hike by the Bank of Japan, which severely impacted the USD/JPY carry trade . Equities, foreign exchange and cryptocurrencies all repriced lower on Monday morning, with the S&P 500 down nearly 9% on Monday from its July 16 all-time high. Last week, Bitcoin fell 23% to $49,000 and Ethereum fell 33% to $2,300, both of which were their lowest levels since February. Both assets have since recovered slightly, with Ethereum up 14% and Bitcoin up 19% from the end of the week. The recent market downturn can be attributed to a combination of macroeconomic factors, including weak U.S. data and global monetary policy shifts, as well as cryptocurrency-specific issues such as Jump Crypto’s large sale of ETH ($470 million) and various token offerings.

Bitcoin ETF net inflows were negative this week, while Ethereum ETF net inflows were more positive overall, with Grayscale ETHE outflows steadily declining since launch. Ethereum ETF net inflows were positive for the first time this week.

Other on-chain developments that rocked markets last week included the U.S. government moving $2 billion worth of Bitcoin seized from Silk Road to two new addresses on July 29, just days after Trump announced he would establish a “national bitcoin reserve.” It’s unclear if the tokens were moved to facilitate liquidation or if the U.S. Marshals simply moved the funds to Coinbase Custody, which they recently added as a custody and trading provider. In addition, the Chinese government also appears to be consolidating about $450 million worth of ETH seized from the 2019 Ponzi scheme PlusToken.

Our take:

Bitcoin’s recent 26% drop from its all-time high, while significant, is not unprecedented in the broader bull cycle. In 2017, Bitcoin fell 25% or more six times while setting new highs. While it’s important to note that market cycles don’t align perfectly — as evidenced by the drastically different pattern seen in 2021-2022 — these large declines are likely part of Bitcoin’s typical volatility during a bull market.

Looking ahead to the rest of the year, Bitcoin faces three major catalysts. First, a $12 billion cash distribution to FTX creditors could inject new capital into the cryptocurrency market, although the extent of this impact may be limited by the fact that most of the distribution will go to funds that purchase claims from individual creditors. Second, the U.S. presidential election is imminent, and if Trump's odds improve, his crypto-friendly stance could boost Bitcoin. If the Democrats remain hostile and Harris's odds improve, this could be a headwind. Interestingly, the correlation between Trump's odds and BTCUSD could break down if the Democrats soften their stance on crypto. Finally, the Federal Reserve's September rate decision remains critical, although its impact may be muted if it is in line with the currently widely expected rate cut. Given these factors, Bitcoin is expected to be mostly range-bound in the short to medium term. The main downside risks include further deterioration in the macro environment or moves in government-held cryptocurrencies, while potential upside risks come from FTX's distribution, an improving political climate, and an accommodative interest rate environment. - Alex Thorn, Gabe Parker

Ethena’s USDe faces first stress test

Ethena Expands USDe to Solana, Plans to Include SOL as Supporting Asset. On August 7, Ethana Labs deployed its delta-neutral stablecoin USDe on Solana, its second ecosystem launch following its initial launch on Ethereum in February 2023. The integration with Solana is facilitated by interoperability protocol LayerZero. Ethena’s Solana integration will also come with an incentivized “Sats Campaign” that will reward participants with points that can be redeemed for ENA tokens. USDe is already available on Solana DeFi applications including Kamino Finance and Drift, and will soon be available on re-staking protocol Jito.

The background is that USDe is a "synthetic dollar" collateralized by crypto assets (such as ETH, ETH LST, BTC, USDT) and a corresponding equivalent short futures position. This delta hedging mechanism helps maintain the stability of USDe's peg, as changes in the ETH spot price and minting/redemption are offset by changes in the size of the short perpetual position. This design generates income from both the staked ETH and the funding and basis of the futures position - currently, staking USDe as sUSDe provides an annual interest rate of 3.8%. With a market capitalization of $3.1 billion, USDe is the fourth largest stablecoin after USDT, USDC, and DAI.

According to the announcement post on X, Ethena Labs also hopes to add SOL as a supported asset for USDe, subject to governance (a vote is expected next week). Adding SOL as a collateral asset “will open up an additional $2-3 billion in open interest on major exchanges,” the Ethena team said, adding that funding rates for SOL have so far surpassed those for BTC and ETH. According to Solscan , the supply of USDe on Solana is 4.2 million, spread across 120 unique addresses.

Our take:

Ethena, since launching as an ETH-centric project less than a year ago, is quickly transitioning to a more general delta-neutral operation as it now looks to add SOL to USDe’s backing after adding BTC in April. The addition of BTC (which now represents 46% of USDe’s total collateral) improves USDe’s scalability, as BTC’s open interest levels are 2.5x that of ETH, and given trader interest (SOL ranks third in total open interest levels , behind only BTC and ETH), SOL would be the next logical asset for Ethena to integrate.

Adding other types of collateral assets in addition to ETH also improves the risk profile of USDe, which just survived its first meaningful stress test earlier this week after ETH funding rates turned negative for the first time this year (funding rates for BTC and SOL remained mostly positive). Despite this, Ethena was able to successfully process $112 million in USDe redemptions while maintaining the stablecoin’s peg, as positive funding income from BTC and gains from ETH LST were able to offset the protocol’s losses from negative ETH funding. Ethena’s stablecoin alternative design is still relatively new and has not been fully battle-tested, but these periods of market turmoil can help demonstrate the protocol’s resilience. Additionally, with expectations growing for rate cuts later this year, USDe’s reliance on crypto-native collateral may offer advantages over traditional stablecoins that are primarily backed by U.S. Treasuries, such as USDT and USDC.

As for Solana, its DeFi ecosystem has received a huge boost from the expansion of Ethena (thanks to LayerZero’s fully fungible token (OFT) standard). Since the launch of PayPal’s PYUSD stablecoin on Solana on May 29, DeFi users have been rewarded handsomely for using the PYUSD stablecoin — the 17% APY offered on PYUSD deposits on Kamino has helped the PYUSD supply on Solana to quickly grow to nearly $320 million in just a few months, nearly surpassing the supply on Ethereum. Separately, the USDC supply on Solana has also increased by about $430 million since the beginning of July, totaling nearly $2.6 billion. The expansion of USDe should further bolster stablecoin momentum on Solana, which saw DEX volume surpass Ethereum throughout July. Still, the total market cap of stablecoins on Ethereum is more than 20x higher than Solana ($79.5 billion vs. $3.7 billion), suggesting that Solana still needs to make more progress to catch up with Ethereum and its thriving L2 ecosystem, at least on this metric. —Charles Yu

eCash returns to Bitcoin payments

The much-anticipated Bitcoin app Fedi was launched on Wednesday. The app provides a convenient way to securely store and use Bitcoin, primarily aimed at empowering underserved populations. The highly anticipated app leverages a novel technical architecture developed by Fedimint Protocol, introducing a community-driven Bitcoin custody and payment method. Notably, Fedimint has raised at least $23 million from venture capitalists to date, making it one of the most high-profile Bitcoin startups.

Fedi adopts a consortium model where a select group of entities control user assets through multi-signature wallets, eliminating single points of failure. Unlike other consortium models, Fedi is unique in that it allows users to choose a consortium that custody their Bitcoin, or to create their own. To enhance traditional custody solutions, the project implemented Chaumian eCash, a privacy-centric digital currency concept invented by cryptographer David Chaum in 1982. This innovative approach represents a dollarized claim on the community's Bitcoin reserves, enabling community members to conduct confidential transactions while protecting individual balances. In the Fedi application, users transact using eCash, which acts as an IOU and is backed by the sender's Bitcoin reserves on the platform. This innovation simplifies the user experience by abstracting the complexity of sending small Bitcoin transactions denominated in US dollars. In addition, the Fedi application also acts as an application layer for web developers; it now includes encrypted private messaging, and other network and social features may be added in the future.

Our take:

Bitcoin payments are an extremely competitive space that has been dominated by the Lightning Network since 2018. Although the Lightning Network has encountered difficulties in terms of technical complexity, Lightning is the premier Bitcoin payment layer. Despite Lightning's dominance in Bitcoin payments, the emerging second-generation Bitcoin Layer 2 shows that Lightning's dominance in Bitcoin payments is not unchangeable.

While competition in the Bitcoin payments space will intensify as these Bitcoin L2s come online, Fedi is positioned to stand out as a private payment and custody solution. While Fedi is not a self-custodial platform, its focus on catering to non-crypto native users will help the app attract a new group of Bitcoin users. More importantly, Fedi takes a different approach and markets their product in underbanked areas of the world, meeting a critical market need. - Gabe Parker

Chart of the Week

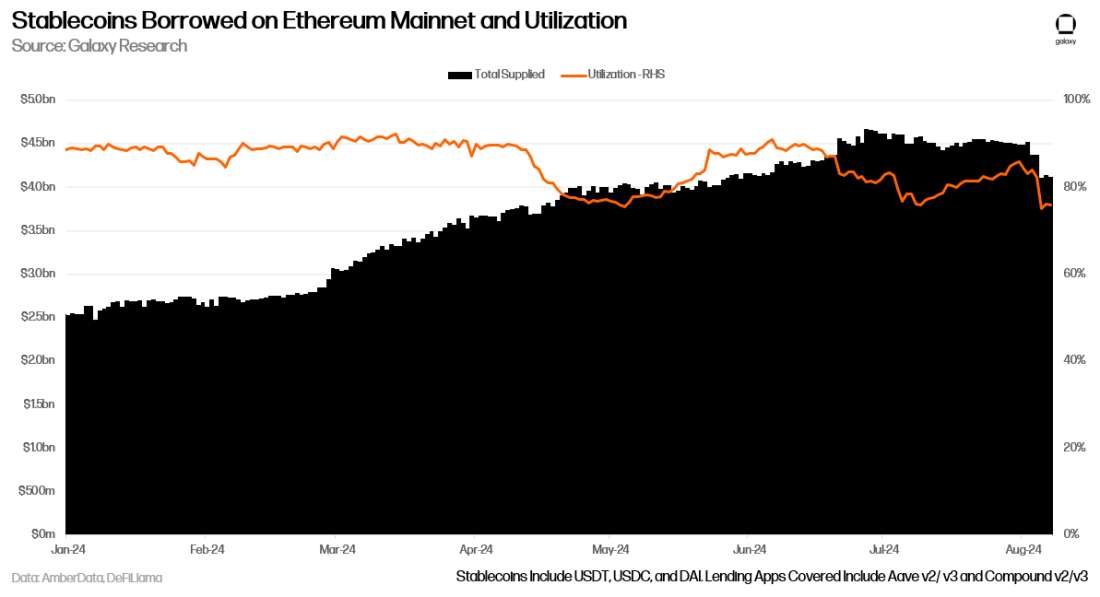

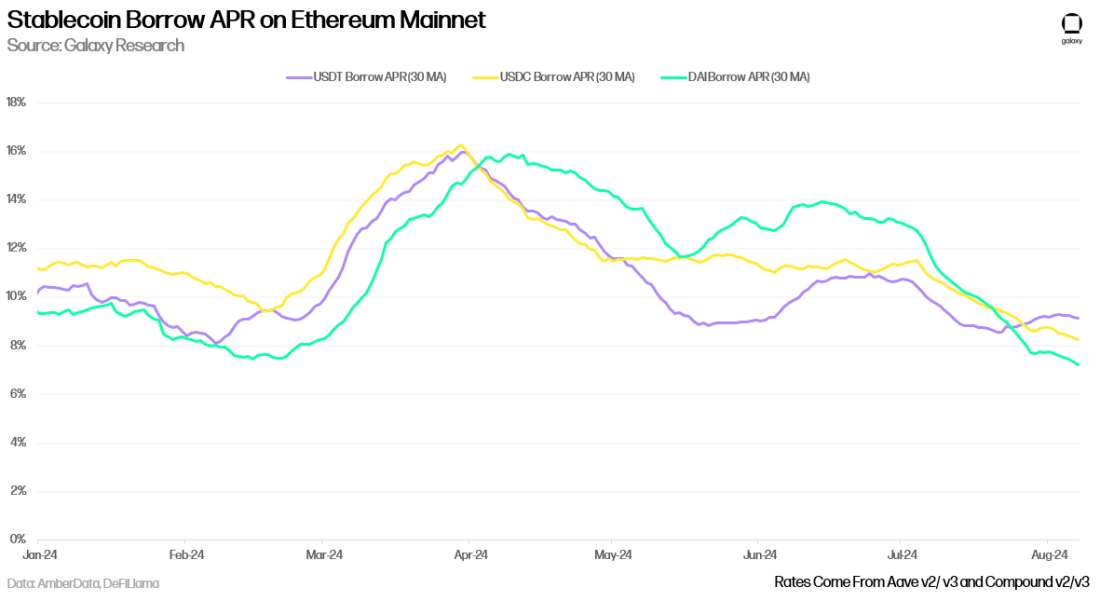

During this turbulent week, over $650 million in USDT, USDC, and DAI borrowing losses were recorded on Aave v2/v3 and Compound v2/v3 on the Ethereum mainnet from August 2 to August 7. This drop means that outstanding borrowings for these stablecoins fell by 17%, with the utilization ratio (borrowed amount/supply amount) falling to a year-to-date low of 75.9%. The drop in utilization was caused by a larger drop in borrowing amounts than supply amounts for these stablecoins. During the same period, $409 million worth of these stablecoins were withdrawn from the aforementioned applications, a drop of 9%.

Record low usage has led to record low costs to borrow these stablecoins, as there is a direct relationship between usage and borrowing costs. Both DAI and USDC set new low borrow APRs using their 30-day moving averages, at 4.27% and 4.98%, respectively. USDT’s borrow APR is still about 80 basis points higher than its year-to-date low of 8.3% in early February.

Record low usage has led to record low costs to borrow these stablecoins, as there is a direct relationship between usage and borrowing costs. Both DAI and USDC set new low borrow APRs using their 30-day moving averages, at 4.27% and 4.98%, respectively. USDT’s borrow APR is still about 80 basis points higher than its year-to-date low of 8.3% in early February.

Other News

Other News

- Franklin Templeton’s On-Chain Money Market Fund Launches on Arbitrum

- Polymarket data shows Kamala Harris's chances of winning are tied with Trump's at 49%.

- Ripple fined $125 million, court rejects all SEC requests

- Dormant wallets linked to PlusToken scam move large amounts of Ether

- Bitcoin miner Core Scientific to provide an additional 112 MW of power to CoreWeave

- Ronin Bridge suspended due to $11.8 million in outflows from MEV Robotics white hats