The origin of value investing

The emergence of the idea of “value investing” in the late 1920s was no accident. This school of thought, pioneered by Benjamin Graham and David Dodd at Columbia Business School (CBS), was largely a reaction to the unbridled financial mania that triggered the Wall Street stock market crash of 1929 and ultimately led to the Great Depression. The Roaring Twenties were a period of postwar optimism, rapid industrial growth, urban expansion, and technological advancement. These transformative societal shifts were catalyzed in part by an increasingly financialized economy and a surge in stock market participation. As businesses flourished and ordinary people experienced unprecedented prosperity, the belief that “stocks could only go up” became firmly ingrained in the public consciousness.

Of course, this trajectory, fueled by easy monetary conditions and excessive leverage, was unsustainable. Furthermore, the lack of regulation and standardized corporate financial statements made it impossible for most investors to implement a disciplined investment strategy. Insider trading was legal and deceptive accounting practices went unchecked, making it extremely difficult to tell whether a particular stock was a wise investment. As a result, the dominant investment style at the time was speculative in nature and driven by herd mentality, ultimately leading to a severely overvalued market that ultimately collapsed in spectacular fashion.

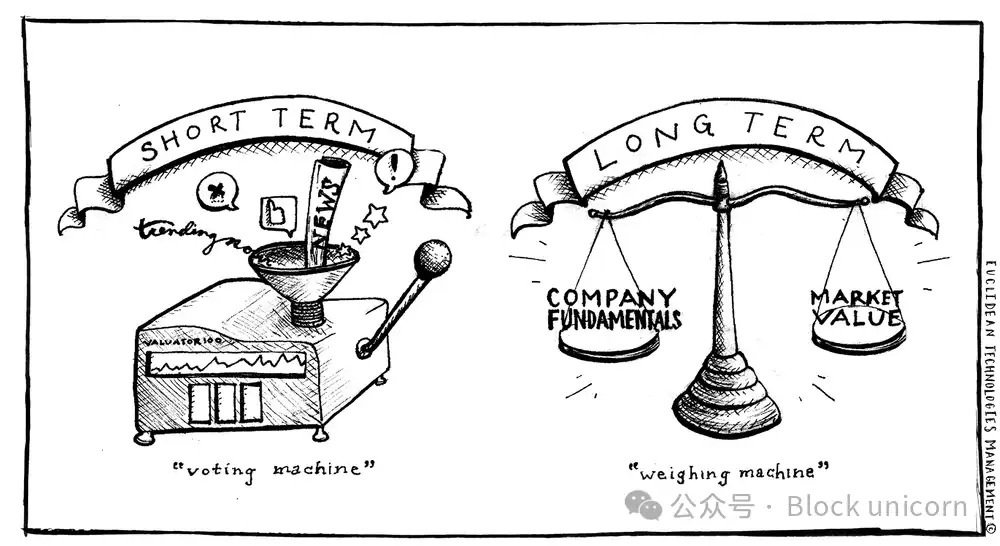

Graham, considered the father of value investing, witnessed this turbulent period firsthand, suffering severe losses during the Great Depression, which prompted him to rethink his investment approach from first principles. In the process, he created a detailed framework for determining a stock’s true, or intrinsic, value through fundamental research and analysis. Value investing is distinct from the speculative bubbles that prevailed in the 1920s, and is based on the idea that the market-clearing price of a particular asset is not always indicative of its true underlying value. Instead, Graham viewed the market as an erratic pricing mechanism driven by investor sentiment, a concept captured in his famous analogy of an investor’s business partner named “Mr. Market,” who is willing to buy and sell company shares at different prices each day, depending on his mood. In other words, the market is a short-term voting machine, but also a long-term weighing machine.

“Mr. Market’s job is to give you a price; your job is to decide whether it is in your best interest to act on it.” – Benjamin Graham, The Intelligent Investor (1949)

An evolving framework

Simply put, value investing is buying something for less than its actual value. This basic concept has been a core tenet of the professional investing community for nearly a century since Graham’s initial musings. His teachings inspired the likes of Warren Buffett, who was Graham’s student at Columbia Business School in the early 1950s and went on to create one of the greatest scores in investment management history. Over time, however, elements of the value investing framework have evolved and adapted to the changing financial landscape. For example, Buffett’s approach to value investing prioritizes more qualitative factors—rather than just the purely quantitative metrics that Graham relied on—such as competitive barriers, entry barriers, and superior management.

All of these principles are rooted in long-term fundamentals and are most often applied to the traditional equity space. However, it is worth considering how these principles apply to newer asset classes. Although not a traditional security, Bitcoin is a compelling case study that can be analyzed within this framework. By understanding the fundamental underpinnings of the asset and the likely trajectory of the network, a strong case can be made that Bitcoin represents a significantly undervalued investment opportunity , and its investment thesis may be understood through the lens of value investing .

Application of the Value Investing Framework to the Bitcoin Investment Thesis

We believe that holding Bitcoin for the long term represents a modern and reasonable interpretation of value investing . While counterintuitive to some, many of the fundamental elements of value investing can be directly applied to the investment case for Bitcoin. Let’s explore how the concept of value investing fits in with the Bitcoin thesis:

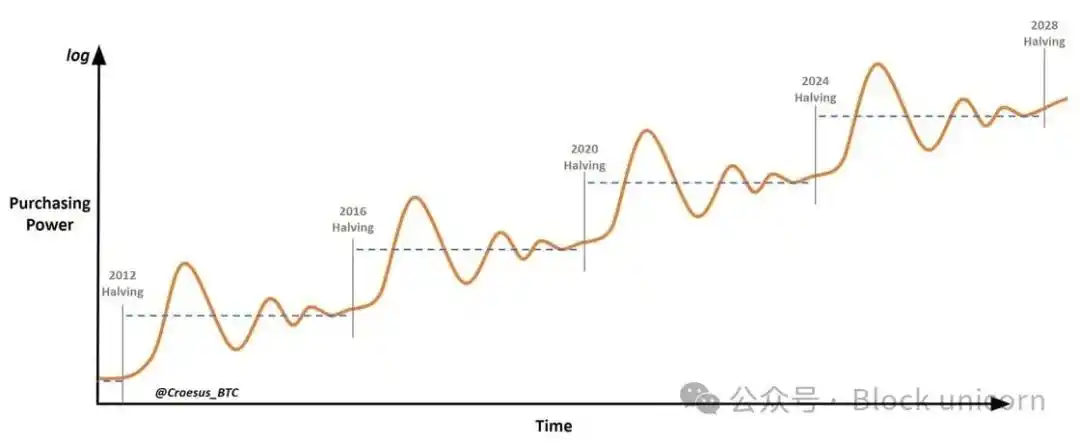

(1) Long-term investment perspective: Value investing requires investors to be able to ignore volatility and be willing to wait for the market to recognize the true value of an asset. The best investments are those that can be held indefinitely. Within the value investing framework, Bitcoin’s historically large volatility should not be viewed as a risk, but rather as an opportunity that can be seized by maintaining a long-term investment perspective and blocking out short-term noise.

“The stock market is designed to transfer money from the aggressive to the patient.”… “Uncertainty is actually the friend of the long-term value buyer.” —Warren Buffett

(2) Contrarian thinking: Following the herd and chasing performance run counter to the philosophy of value investing. Instead, investment decisions should be made from first principles by identifying information asymmetries. The widespread misunderstanding and lack of understanding of Bitcoin (and our existing monetary system) has kept it in the position of a contrarian investment.

“It’s always easiest to follow the crowd; sometimes it takes a lot of courage and conviction to stand out. However, staying away from the crowd is an essential component of long-term investment success.” - Seth Klarman

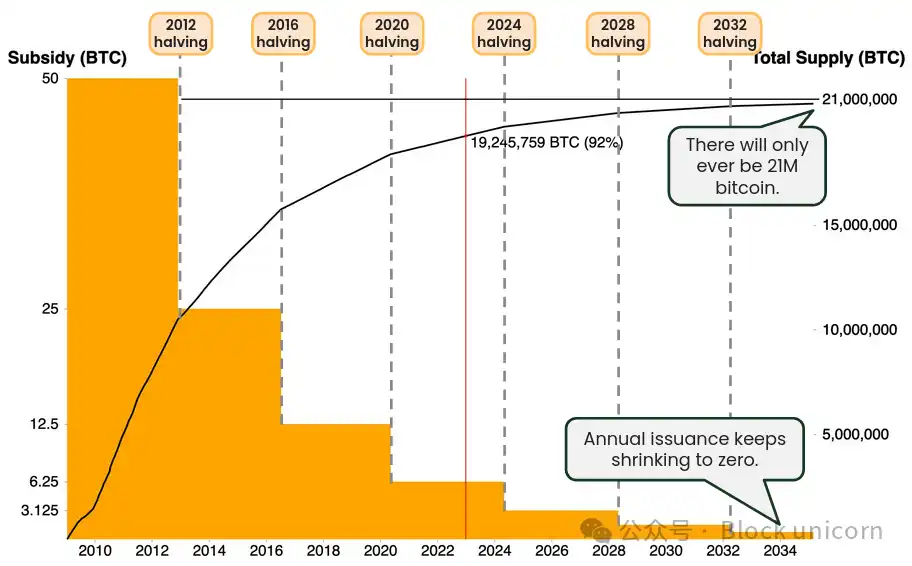

(3) The power of compound returns: The concept of compound interest in value investing is similar to a snowball rolling down a hill; with time and patience, small gains can accumulate and multiply the value of an investment. Importantly, this mathematical concept can also be applied to the hidden depreciation of currency - recognizing that inflation erodes purchasing power in a slow and hidden way is key to understanding Bitcoin's value proposition.

“It is obvious that a change of just a few percentage points can have a huge impact on the success of a compounding [investment] program. It is also obvious that this impact grows larger over time.” -Warren Buffett

(4) Comfort with Concentrated Investing: A less traditional notion in value investing is that investors should be comfortable with concentrated investing, rather than subscribing to the common view that portfolio diversification is essential. When investors truly understand the intrinsic value of an asset, they should adjust their investment size in line with that belief, even if this results in a more concentrated portfolio. In the context of Bitcoin, a deep understanding of the technology, its unique properties as a digital store of value, and its overall adoption trajectory can lead to unconventional investments.

“Diversification is a protection against ignorance. If you know what you are doing, it doesn’t mean much.” —Warren Buffett

(5) Excellent Management: A core tenet of value investing is the excellence and integrity of a company’s management team. Investors should pay close attention to leadership to ensure that the stewards of their capital are both competent and trustworthy. An interesting parallel emerges when this view is compared to Bitcoin. Bitcoin is not based on a tangible team of executives, but on carefully written code and an immutable monetary policy. Trust is not built on fallible humans, but on the absolute mathematical principles that govern the protocol. Therefore, Bitcoin’s appeal in the realm of “excellent management” is that it is free of human intervention, providing investors with a transparent and predictable financial instrument.

“Modern life creates a successful bureaucracy, and successful bureaucracy breeds failure and stupidity.” - Charlie Munger

(6) Competitive barriers and entry barriers: Value investing places great emphasis on competitive advantage, ensuring that a company maintains its advantage and defends its position in the market. Bitcoin’s origins are often referred to as a “flawless concept,” representing a profound first-mover advantage in creating digital scarcity. Bitcoin’s growing network effects, coupled with its unparalleled degree of decentralization, support its dominant market position. Therefore, any new entrant attempting to replicate or introduce similar digital scarcity will face insurmountable barriers, which reinforces Bitcoin’s intrinsic value proposition.

“The key to investing is not to assess how big an industry’s impact on society is or how much it will grow, but to determine the competitive advantage of any given company and, most importantly, the durability of that advantage.” -Warren Buffett

Value investing is not dead yet

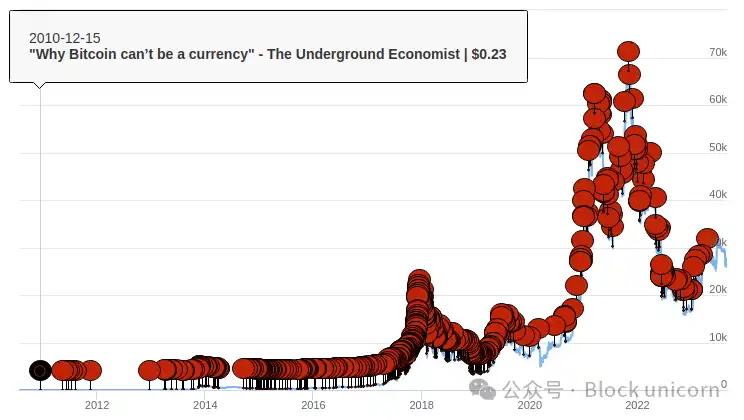

Just as the mainstream media has often declared “Bitcoin is dead” throughout its history, “value investing is dead” has been declared countless times over the past few decades. Indeed, the mantra of “growth at all costs” has dominated the market in the 21st century, and the ongoing shift from “active” to “passive” index investing has also played a major role in the perception that value investing is ineffective, as stock market performance has become increasingly concentrated in a small number of mega-cap growth stocks. That being said, value investing will always be somewhat out of favor due to the human behavioral tendency to chase performance.

“Value investing doesn’t appeal to the masses. If it did, you’d never get a bargain.” —Arnold Vandenberg

Furthermore, the phenomenon of continuous devaluation and artificially lowered capital costs through money printing over the past few decades is one of the reasons why growth stocks are favored over value stocks. However, despite the fact that "value" strategies have underperformed "growth" strategies in the stock market, the basic principles of value investing have timeless value. Value investing represents the ability to foresee future growth before the financial condition of an asset is apparent or before the market realizes its true value potential.

“When the gap between reality and perception becomes wide, opportunities emerge.” - François Rochon

Like Bitcoin, value investments will never go away. They may appear unpopular for a long time, but there is an asymmetric opportunity for investors willing to put in the effort to deeply understand the full value potential of digitally native, energy-backed, cryptographically secure, open source, equitably distributed, scarce commodities. Benjamin Graham, Warren Buffett, and their many disciples may not realize it yet, but they have provided a useful toolkit for understanding the investment case for Bitcoin.