Compared to the feudal division of Ethereum, the Solana ecosystem is smaller in scale but more agile. After the FTX collapse, Solana has risen from the ashes with its high performance, strong marketing, and various hardware products.

Specifically, high performance refers to the Firedancer upgrade, strong marketing is the MEME season, and the hardware includes various Web3 phones. However, this is not enough. The proposal of PayFi by Lily Liu, the chairman of the Solana Foundation, has also become a hot topic. Although the hot topics in July may seem a bit outdated in October, in the long run, the entire Web3 industry is shifting towards off-chain and real consumption scenarios.

"Long, long ago, you had me, and I had you."

This article is not a song for Solana, but a melody exploring the way out for Web3.

The Uneven Struggle of Crypto Wallets: The Prelude of PayFi

Before defining Lily Liu's concept of PayFi, let's first discuss Web3 wallets. In 2022 to 2023, with the flow anxiety of smart contract wallets, account abstraction (AA), and exchanges, a group of Web3 wallets are entering the second peak period after the 2017-2021 on-chain meme era.

From the perspective of exchanges, wallets are the main entry point for people to interact with the chain, and the subsequent traffic will flow in and out from here, and they may even have the potential to replace CEX. Furthermore, in the increasingly fierce competition of Ethereum L2, multi-chain wallets will definitely be the main battlefield for aggregating liquidity.

However, the 2024 wallet ecosystem is not very attractive. OKX's built-in Web3 wallet is already one of the best, but in most cases, it has not become an independent product. One important reason is that Web3 wallets have traffic but lack a closed-loop monetization mechanism. If they want to charge fees, users will directly open the desktop product to avoid an extra fee.

From a more "path-dependent" perspective, the problem of crypto wallets lies in the excessive pursuit of transaction characteristics. Note that this is not in conflict with the above-mentioned profitability dilemma. The core product feature of crypto wallets is to provide users with richer on-chain transaction feature support, from accessing more chains to a more competitive dApp recommendation mechanism.

And users' funds are not like Alipay, stored within the crypto wallet. The non-custodial mechanism may give users peace of mind, but it does not win their true heart. In short, crypto wallets have nothing to do with Web2 wallets - they neither manage money nor provide financial services.

All these factors make it impossible for crypto wallets to establish their own closed-loop payment system like PayPal or WeChat/Alipay. From a broader business perspective, Web3 wallets only have users, without the support of merchants. If dApps are considered as merchants, then only a small portion of on-chain merchants.

However, wallets do have a large amount of traffic, and the profits or losses in DeFi on the chain can indeed be converted into the possibility of off-chain consumption, but losses are also possible, depending on whether it is ETH-based, stablecoin-based, or fiat-based.

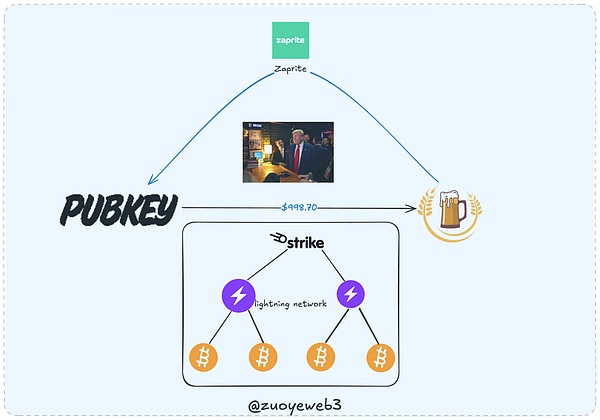

A normal Payments system requires the support of both merchants and users, but this is precisely the industry's shortcoming at the moment. We can use the top-tier male entrepreneur Chuanbo as an example to illustrate this problem. On September 19, 2024, Chuanbo visited the PubKey bar in New York and bought a beer for $998 to support his followers. Chuanbo used Strike to initiate the payment, and the merchant used Zaprite to receive the payment.

In this case, the payment system used by the merchant and Chuanbo is not the same, which is hard to imagine in the Web2 era, equivalent to Chuanbo using Alipay to pay, and the merchant using WeChat to receive. But in Web3, it makes sense, as both parties are using the Bitcoin network as the settlement layer. Let's go through the workflow:

Chuanbo uses Strike to initiate the payment request, Strike calls the Lightning Network to start the payment process, and the Lightning Network confirms the transaction through the Bitcoin network.

The merchant PubKey uses Zaprite for payment collection, Zaprite uses the Lightning Network to confirm the payment status, and the Lightning Network ends the transaction after confirmation through the Bitcoin network.

In this process, Zaprite only has a $25 subscription fee, and apart from that, the merchant only needs to deduct the miner processing fee, and the rest is their own income. We can compare this to Visa/MasterCard/AE, which charge around 1.95%-2% in fees, while the Bitcoin miner processing fee is currently around $1.46 on average, and accepting Bitcoin does not require any fees.

Continuing the extension, the logic of Web2 Payments is similar to Chuanbo buying beer, but there are quite a few intermediate links, which is the drawback of Web2. The opportunity of Web3 Payments and PayFi lies in this.

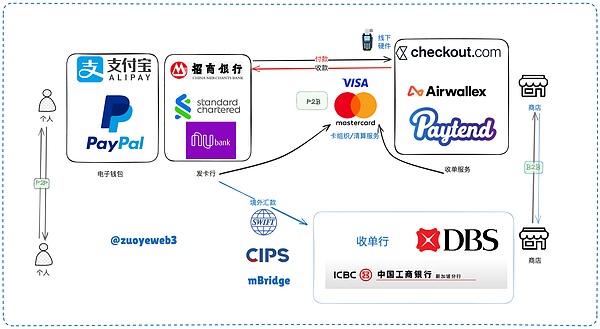

For the concept and product replacement, the payment products we commonly use, such as Alipay, WeChat Pay, and PayPal, belong to e-wallets targeting the C-end, and the corresponding B-end enterprise/merchant collection systems. As long as a settlement network similar to the Lightning Network is built, the simplest P2B (individual and enterprise) interaction system can be established. Generally, the intermediate settlement network requires card organizations and payment protocols to jointly constitute.

Taking the above diagram as an example, the Web2 payment system can be divided into P2P between individuals, P2B and B2B between individuals and enterprises, as well as payment behavior between merchants, and banks can also conduct transactions through systems such as SWIFT or CIPS, or cross-border CBDC transaction systems such as mBridge.

However, it should be noted that the payment behavior is strictly speaking between individuals and enterprises, as well as between enterprises. We include P2P and inter-bank transactions here for the convenience of comparison with Web3 payment behavior, because in Web3, the main payment scenario is between individuals, such as Bitcoin, which is a peer-to-peer electronic cash payment system.

If we refer to the Web2 payment system, the Web3 payment system is actually very simple. Of course, the theoretical simplicity cannot cover the fragmentation of the ecosystem. One obvious feature is that the traditional payment system has more banks and fewer card organizations, so it has a strong network effect, while Web3 goes against the trend, with many public chains/L2s, but the main assets are only US dollar stablecoins, with only a few products like USDT/USDC.

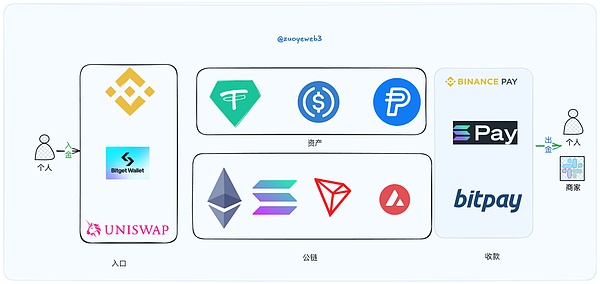

Even in the most optimistic estimate, the number of merchants globally supporting Bitcoin is only around 30,000, and although some large brands like Starbucks are included, the acceptance is still far from traditional card organizations or e-wallets.

Merchants accepting Binance Pay/Solana Pay are more concentrated in online merchants, such as the travel OTA platform Travala, and they are still a long way from the scale of card organizations with hundreds of millions of merchants.

We will elaborate on the content of the payment system in the following text, and now it's time to introduce the concept of PayFi.

The PayFi Stack: The Intersection of DeFi, RWA, and Payments

The reason for adopting the narrative structure of first discussing Payments and then introducing PayFi is that the two are very different. Overall, PayFi is more like DeFi + stablecoin + payment system, and it does not have a very close relationship with Web2 Payments, as mentioned earlier, which everyone can feel.

Let's start with an explanation from Lily Liu. PayFi utilizes the time value of money (TVM), such as earning profits in DeFi, which is the manifestation of TVM. The problem is that this may take time, such as staking tokens to obtain rewards, which usually requires a lock-up period. But as long as there are tokens, there is the possibility of appreciation. In previous operations, the earnings could be reinvested into DeFi in a circular manner to continuously seek profit opportunities.

Now, this part of the earnings can be directed to other directions, such as using the expected earnings for current consumption. For example:

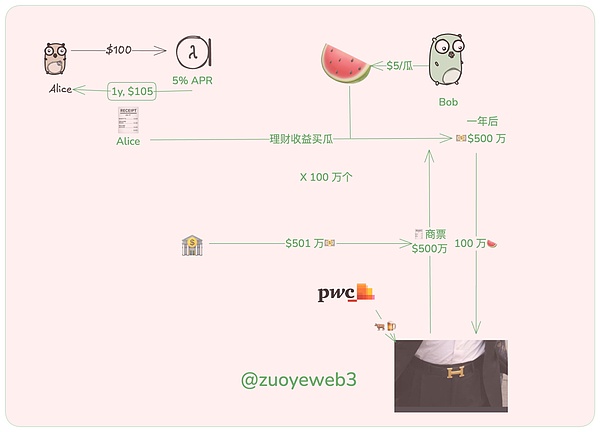

1. Alice invests 100 USDC in a financial product with an annual interest rate (APR) of 5%, and after one year, she can obtain $105 in principal and interest income.

2. Bob runs a watermelon stall, and to sell more watermelons, he now allows Alice to eat a $5 watermelon with the financial product certificate, and after one year, Bob can redeem the $5 from the financial product.

This example is very simple, too simple to withstand scrutiny, such as how Alice and Bob can guarantee the smooth execution of the contract, and what if Alice's financial income decreases. But in the premise of not considering these, Alice can eat watermelon without any cost, and Bob gets a $5 receivable.

A year later, the bull market arrived, and Bob received a lot of $5 bills, ready to enter the large enterprise supplier market. After looking around, he saw that Evergrande was looking for watermelon sellers, and he placed an order for $5 million. Bob was very happy, but Evergrande gave him a commercial bill. With the cooperation experience with Alice, Bob happily accepted the commercial bill, and the two parties agreed that cash would be paid in a year based on the bill, and if not paid, the house would be used as collateral.

However, half a year later, Bob was preparing to enter the stock market, and he needed to cash in the commercial bill. After being rated by PricewaterhouseCoopers, Evergrande's commercial bill was a AAA-rated high-quality asset, and banks, non-financial institutions, and even individuals were frantically scrambling for it, because Evergrande's real estate has quality assurance and has great appreciation potential.

Bob successfully sold the commercial bill at a premium of $5.01 million, the bank obtained the commercial bill, Evergrande obtained the free lunch, and Bob obtained the stock market dividend, and everyone had a bright future. (Generally, cashing in commercial bills requires discounts and fees, but here we are just explaining the workflow, and Evergrande's commercial bills were only about 7/8 of the face value before its collapse.)

Another meaning of TVM is the monetization of non-tradable assets, and even non-tradable assets themselves can be currency or its equivalent, which is somewhat similar to the logic of re-pledging.

In the context of Web3, the monetization of non-tradable assets can only be achieved through DeFi, so PayFi is a natural extension of DeFi, except that it extracts a portion of the liquidity from the on-chain Lego and injects it into the off-chain to improve life.

The relationship between PayFi and Payments lies in the fact that payment is the simplest and most convenient way to satisfy the demand for off-chain capital, and PayFi and RWA intersect, but traditional RWA emphasizes "on-chain", such as the so-called tokenization process, which requires securities, gold or real estate to be tokenized first to meet the possibility of on-chain circulation, and many domestic alliance chains are doing this, such as blockchain electronic invoices or Gongjinbao.

It is difficult to say that PayFi is a subset of RWA, as a considerable part of PayFi's behavior is "off-chain", and whether there is an on-chain link is not the focus of the PayFi concept, but its behavior needs to involve interaction with the off-chain link.

However, there is no need to get entangled, as many concepts in Web3 lack large-scale products and user groups, and are more about concept hype and coin selling. Roughly speaking, products involving PayFi / Payments and RWA can be divided according to the following timeline:

Old era: Ripple, BTC (Lightning Network, BTCFi, WBTC), Stellar

2022 RWA concept trio: Ondo/Centrifuge/Goldfinch

New era-2024 PayFi: Huma (already established, will turn red in 2024), Arf

In fact, from the development history of the above products, it is not wrong to say that PayFi is a continuation of RWA. The traditional narrative, especially the business model of on-chain capital lending to off-chain entities, is the PayFi of 2024, while in 2022 they are all called RWA.

It can even be boldly argued that the lending in RWA, similar to Ripple's cross-border settlement, combined with the off-chain consumption of stablecoins, constitutes several aspects of the current PayFi, and in essence, these are the only contents.

It can be said that the software and hardware construction of Web3 is based on the material and ideological foundation of Web2, and Web3 PayFi is no exception. Its similarity to Payments is actually greater than its difference, and lending products are more about the direction of capital flow. If off-chain products can have more returns, those returns can also be used for payment behavior.

Being misunderstood is the destiny of the communicator, and I do not know whether Lily Liu agrees with this interpretation, but I believe that only by sorting it out in this way can the logic be smooth. As long as the on-chain returns can be used for off-chain consumption scenarios, it conforms to the concept of PayFi, so the focus of the market in the future will be on Web3 Payments, RWA Loans, and stablecoins, which are often included in a cyclical process.

For example, RWA corporate lending, priced in U, individuals enter the RWA on-chain lending pool through DeFi protocols, the RWA lending protocol lends to the real entity enterprise after evaluation, and after recovering the accounts receivable, the LP obtains the protocol's profit sharing, and cashes out through the Mastercard U card, which just happens to be supported by Binance Pay, forming a perfect closed loop.

History belongs to the pioneers, not the summarizers. How PayFi is defined is not important, the urgent task is to explore the real yield outside the on-chain involution of DeFi, the demand of tens of billions of people from the off-chain will bring more abundant liquidity and higher leverage valuation support to the on-chain, and only those who can make it through can define the market.